If you need cash to consolidate debt, cover an unexpected expense, or make a large purchase, a personal loan can be a flexible option. In the U.S., getting a personal loan usually takes just a few days, and sometimes less, if you know what lenders look for.

This guide walks you through 10 clear steps, from checking your credit to comparing lenders and signing your loan, so you can apply with confidence and avoid common mistakes.

Table of Contents

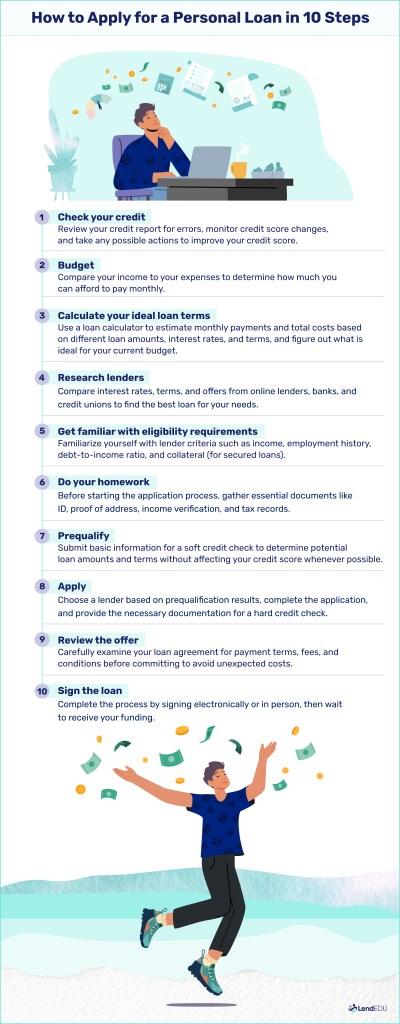

1. Check your credit report and credit score

Before shopping for a loan, review your credit report to understand how lenders may view your creditworthiness. You can request a free copy of your credit report on the AnnualCreditReport website from all three major credit bureaus—Experian, Equifax, and TransUnion.

Your credit report won’t show your credit score, but many credit cards’ benefits include free credit score monitoring. If you don’t have a credit card, you can sign up for free credit monitoring at companies such as Capital One’s free CreditWise plan to monitor and help improve your credit score.

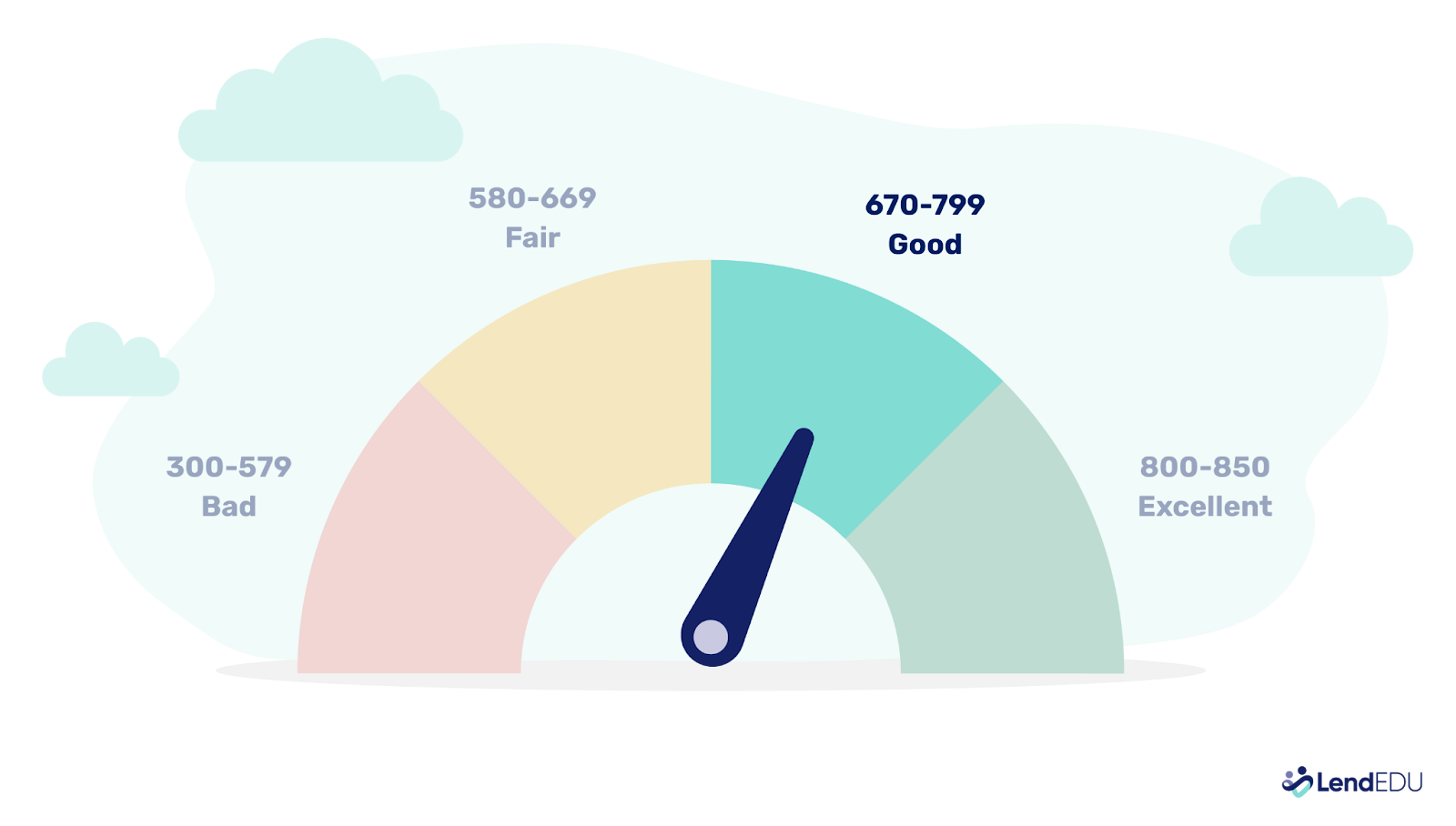

Lenders’ requirements vary, ranging from 300 to 680. If your credit score is good to excellent, your chances of getting desirable terms are typically better.

If you have fair or bad credit, you might be able to get a personal loan. However, the rate will likely be much higher than if you have a good or excellent credit score.

Review your credit report for errors or negative marks that should have dropped off after seven years. If you find errors or charges to dispute, notify the creditor to correct the mistakes.

2. Review or create a budget

To find out how much you can afford to pay each month, look at your current budget. If you don’t have a budget, several apps can help you create a budget, manage your finances, and save money for emergencies. You can also create a budget using online templates. You can also get free help creating a budget by meeting with a credit counselor at a nonprofit credit counseling agency.

3. Calculate your loan payments

Once you know how much you can afford each month, you can calculate payments for various scenarios with our personal loan calculator. Input the loan amounts you have in mind using different interest rates and repayment terms to calculate how much your loan payments may be.

For example, we used the calculator to create these scenarios:

If you get a $5,000 loan at a 10.73% interest rate with a three-year term, your monthly payment would be $163, and you’d pay a total of $5,870 for the loan.

If your rate for the same amount is 17.80%, your monthly payment would be $180, and the total repayment amount would be $6,489.

Experiment with various loan amounts, rates, and loan terms to get an idea of what you can expect to pay each month and how much you can afford. With this information, you’ll have a much better idea of what you can afford.

4. Understand other eligibility requirements

Having a good credit score goes a long way with lenders. However, lenders also determine your creditworthiness based on other factors, including:

- Income: Lenders ask about and verify your income to gauge whether you can afford to make the loan payments each month.

- Employment history: Lenders may ask for proof of employment so they know that you have an income source. They may also look at whether you’ve had steady employment over the years, which indicates stability.

- Debt-to-income ratio: Lenders also take a look at your credit report to learn how much debt you currently have. This way, they can determine the risk of loaning you money and the likelihood that you can loan payments each month.

- Collateral: For secured loans, you’ll need collateral such as a bank account or car, to secure the loan. That way, if you default on the loan, the lender can seize the property to recoup the loan amount—and in exchange for the collateral, you might qualify for a lower rate.

5. Get your documentation in order

Before you apply for a loan, gather all the documentation you must provide on the application. The table below lists the documents your lender is likely to accept.

| Required | Examples |

|---|---|

| 2 forms of ID | Valid driver’s license, State-issued ID card, U.S. passport, birth certificate, military ID, citizenship certificate, utility bills with your current address |

| Proof of address | Utility bills with a matching address to your ID, rental agreement, voter registration card, vehicle registration, government-issued ID, home, auto, or renters insurance card |

| Income sources | Bank statements, pay stubs, W-2 or 1099 statements, proof of child support, alimony statements, 2 years of tax returns, proof of disability benefits, pension or trust statements, retirement disbursements, documentation of dividends, rental income documentation |

6. Research lenders

Once you have an idea of how much you can afford to borrow, how much your monthly payment might be, and how much you’ll pay in interest for various terms, it’s time to shop for a loan. You have three main options for applying:

- Online lenders (or marketplaces)

- Brick-and-mortar banks

- Credit unions

Compare top personal loan lenders

Once you know what you’re looking for, comparing lenders side by side makes it easier to spot the best fit for your credit profile, budget, and timeline. Here are several lenders we’ve selected as the best personal loans, depending on your credit profile and intended use of funds:

To find the best loan, compare interest rates, loan terms, and the total amount, including interest. Add the monthly payment amount to your budget to ensure you can make timely payments.

Read more:

- Personal Loans After Bankruptcy

- Personal Loans for Non-U.S. Citizens

- Personal Loans for International Students

- Personal Loans for Single Mothers and Other Aid

- Best Personal Loans for Veterans

- Best Personal Loans for Students

- Fastest Personal Loans for Quick Cash

- How to Get a $20,000 Personal Loan

- How to Get a $35,000 Personal Loan

- How to Get an $80,000 Personal Loan

7. Prequalify

It’s smart to prequalify to see how much you may be able to borrow based on your credit history and financial situation. If you apply for prequalification online, most lenders perform a soft pull on your credit, which won’t affect your credit score. That way, the lender can determine from your basic financial and personal information how much you may be able to borrow.

Once you know the amount you can borrow, you can check out our loan calculator with various rates and loan terms to get an idea of monthly payment amounts.

8. Select a lender and apply

We recommend starting with the best lenders we listed above, reviewing the interest rates, loan amounts, loan terms, credit requirements, and who each is best for. An excellent way to compare lenders is to prequalify with an online loan marketplace.

Our favorite marketplace is Credible.

Once you select a lender and loan offer, it’s time to apply for the loan. When you apply, lenders ask for more detailed information and documentation and usually perform a hard pull on your credit, which may lower your credit score by a few points. If you have a lower credit score, you might get a better rate and terms if you apply with a cosigner or a co-applicant.

If you apply but your loan request is denied, I first recommend understanding the reason for the denial. Are there errors on your credit report? If so, you can have those corrected and might then be approved.

If your credit report is accurate, you might need to wait and improve your financial condition by paying down debt, limiting new loan applications, increasing income, or decreasing expenses.

If you need a loan in the short term, consider a trustworthy cosigner—for instance, a financially responsible parent or friend.

Erin Kinkade, CFP®

9. Review your loan documents

When you get your loan documents, review them before you sign anything. Look for information about your monthly payment and fees, such as origination fees, which can range from 1% to 10% of the total loan amount and are deducted from loan proceeds. Also, watch for late-payment fees, loan application fees, early payoff fees, and whether the lender charges an annual fee.

10. Sign the loan

Depending on the lender, you can often sign the loan documents electronically. If you sign in person at a local bank or credit union, you’ll sign with a loan officer. Many lenders provide funding the next day or within a few days.

See how personal loans work before you apply.

FAQ

How long does it take to get a personal loan?

Most personal loans take one to five business days to fund after approval. Online lenders and loan marketplaces often fund faster, sometimes within 24 hours, while banks and credit unions may take a few days longer, especially if additional documentation is required.

Can you get a personal loan the same day you apply?

Yes, some lenders offer same-day personal loans, but approval and funding depend on your credit, income verification, and how early you apply. Same-day funding is most common with online lenders that offer instant decisions and electronic document signing.

What credit score do you need to get a personal loan?

Many lenders accept credit scores as low as 580, but borrowers with scores 670 or higher typically qualify for lower interest rates and better terms. Each lender sets its own credit requirements, and some consider income, employment history, and debt-to-income ratio alongside your score.

Do you have to prequalify before applying for a personal loan?

No; prequalification is optional, but we strongly recommend it. Prequalifying usually involves a soft credit check, which doesn’t affect your credit score and lets you compare estimated rates and terms before submitting a full application.

Is applying for a personal loan bad for your credit?

Applying for a personal loan can cause a small, temporary dip in your credit score due to a hard credit inquiry. However, making on-time payments can help your score over time, especially if the loan improves your credit mix or lowers credit card balances.

About our contributors

-

Written by Deb Hipp

Written by Deb HippDeb Hipp is a freelance writer with more than a decade of financial writing experience about mortgages, personal loans, personal finance, and debt.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.