Personal loans are an incredibly useful and flexible form of financing, but if you’re seeking a personal loan with fair credit, you may have fewer options.

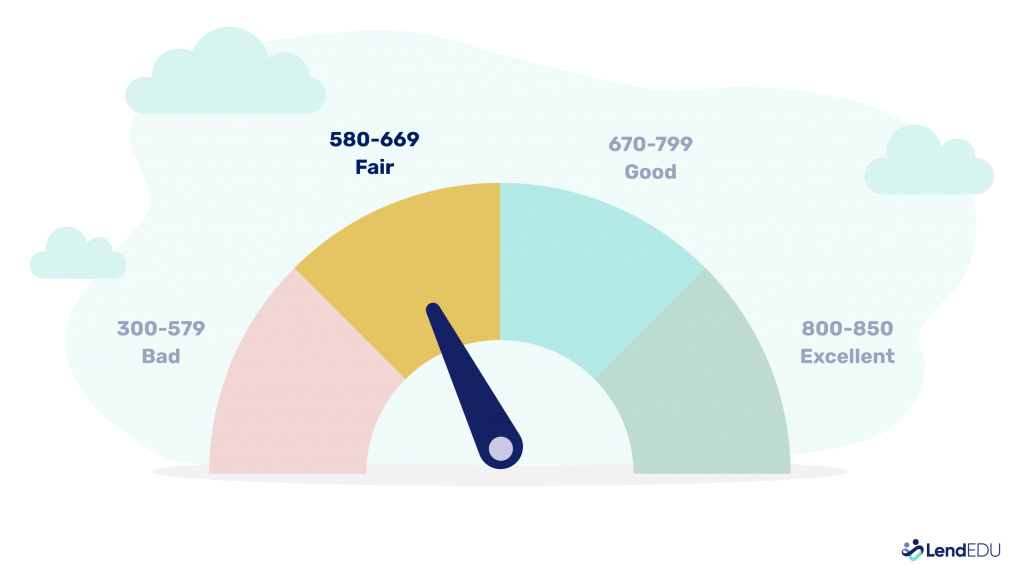

Fair credit is defined as a FICO score between 580 and 669. The meaning of this number represents the risk you present to a lender.

Luckily, some lenders offer fair credit personal loans. You may not qualify for the best personal loan rates, but these loans may still have lower rates than credit cards and other financial products.

Here’s a closer look at how fair credit affects your approval odds for a personal loan, how to identify the best personal loans for fair credit, and our suggestions for the best fair-credit personal loan lenders.

How fair credit affects your approval odds for a personal loan

Your credit score is made up of several components: payment history, amounts owed, length of credit history, new debt, and credit mix. Negative reporting on one of these elements can affect your credit score.

Fair credit borrowers might have some combination of:

- High credit utilization

- Late or missed payments

- Shorter credit histories

- Collections

- Bankruptcy

- Too many credit inquiries

- Too many credit accounts

Some of these factors can exclude fair credit borrowers from qualifying for personal loans. A high credit utilization ratio, for example, affects your ability to qualify for a loan based on how much credit has already been extended to you.

Other factors—like a few late payments on a shorter credit history—mean borrowers have fair credit but still have the ability to repay a loan. You just need to know where to look for loans for people with fair credit.

How to identify the best personal loans for fair credit

When you begin your search for the best loans for fair credit, you’ll want to get the most favorable terms you can find, so keep the following factors in mind:

| Factor | What it is | What to keep in mind |

| Annual percentage rate (APR) | Tells you the yearly cost to borrow your loan, including interest and fees | Higher APRs generally mean you’ll pay more over time. |

| Fees | Origination fees, returned check fees, prepayment penalties, application fees | Larger loans and lower credit scores can increase fees |

| Monthly payments | How much you pay each month toward principal, interest, or both | Increasing monthly payment amount can reduce overall borrowing cost |

| Borrower requirements | Minimum criteria borrowers must meet for approval | Qualifying for the loan doesn’t mean qualifying for the best rates |

| Repayment terms | The years you have to pay your loan | The longer you take to repay, the more you’ll pay overall |

| Time to fund | How long it takes the lender to disburse your loan proceeds | Depends on how early in the day you apply and how soon you send supporting documents |

| Payment flexibility | Options offered to customize your repayment schedule | Choose a plan that’s affordable in the short term and minimizes interest paid in the long term |

All of these elements work together to determine whether a personal loan offer makes sense financially.

Your APR influences what you can pay monthly, which in turn influences what you’ll pay overall. That’s why it’s so important to take advantage of soft-pull prequalifications so you can shop around for the best rate and repayment terms before you apply.

While you’re evaluating loan offers, also consider the lender’s funding time. Most lenders fund loans within a couple of business days after approval, but if you need money now, take a look at our list of quick personal loans for lenders that can fund loans the fastest.

Best personal loans for fair credit

With the above considerations in mind, we’ve identified four of the best personal loans for borrowers with fair credit. Each lender lets you prequalify with a soft credit check, with loans boasting unique features, fast funding, and competitive rates.

| Company | Best for… | Rating (0-5) |

|---|---|---|

|

Fair Credit |

|

|

Thin Credit |

|

|

|

Choosing Payment Date |

|

|

|

Credit Card Debt |

|

Best for fair credit: Upgrade

- Customizable loan options

- Repayment terms from 24 to 84 months

- Borrow $1,000 to $50,000

Upgrade is a great option for borrowers with fair credit, since eligibility is based more on free cash flow than credit alone. Plus, Upgrade’s small minimum loan amount means you don’t have to borrow more than you need.

Origination fees can be as much as 9.99%, and APRs vary from 8.49% to 35.97%. You can check your individual rate without damaging your credit score, and if approved, you could receive your funds by the next business day.

Best for thin credit: Upstart

- Check your rate in 5 minutes without affecting your credit score

- Fully automated loan process

- Innovative eligibility criteria

- No prepayment fees

- No limitations on how you use your funds

- Repay your loan in 36 or 60 months

Upstart offers APRs from 6.7%% to 35.99%%, loan amounts from $1,000 to $50,000, and funding as fast as one business day. It also takes into account future income for new-to-credit borrowers. If, for example, you are graduating from college and have a job offer, you may be able to qualify for a personal loan.

Most of Upstart’s loans are fully automated, so you can upload your documents online and receive your money quickly. There’s little friction in the process—you don’t have to talk to a human if you don’t want to.

Best for choosing payment date: Achieve

- Personalized experience with agent

- Same-day decision

- Multiple rate discounts

Achieve personal loans combine the guidance of a dedicated loan agent with the streamlined experience of an online application. You can borrow as little as $5,000 or as much as $50,000, and you could get a decision the same day you apply.

APRs fall between 7.99% and 35.99%, but you can shave down your rate using Achieve’s generous discounts. Adding a co-borrower, flashing your retirement assets, or letting Achieve use your loan to pay off existing debt can all lower your APR, saving you money over the life of your loan.

Best for credit card debt: Happy Money

- Easy and quick online application

- Transparent pricing

- No fees beyond origination fee

Happy Money specializes in personal loans for consolidating credit card debt, even going so far as to name its product “The Payoff Loan.” Loan amounts are capped at $40,000, and Happy Money’s highest APR is much lower than most other lenders at just 29.99%.

That’s good news for borrowers who want to pay as little as possible in interest and fees. Keep in mind, however, that Happy Money prefers borrowers with scores of 640 or above and no outstanding delinquencies. If you have major credit blemishes, clear them up before you apply.

How to get the best personal loan with fair credit

While there are certainly personal loan options borrowers with fair credit can pursue, you can also make moves to strategically improve your credit score and increase your odds of approval.

Focus on your debt-to-income ratio

Your debt-to-income ratio isn’t just a part of your credit score—it determines whether or not you have enough income or too much debt to qualify for a new personal loan.

If your ratio is too high, the lender won’t be able to issue you a loan regardless of your credit score. Increasing income or reducing existing debt can help improve your odds of approval.

Improve your credit score

Improving your credit score is one of the best ways to get better loan offers and qualify for personal loans with more lenders.

To improve your credit score, follow these steps:

- Dispute errors on your credit report. Check your credit report for mistakes and dispute any incorrect information with the credit bureaus and the business that reported the error. Credit bureaus are required to investigate within 30 days and will send you the results in writing.

- Ask for a credit line increase. If a credit issuer will increase your credit limit, you can instantly improve your credit utilization ratio. Just be sure not to use your newly available credit, as that will harm your credit score, debt-to-income ratio, and approval odds for a loan.

- Automate your payments. Be sure to make any payment obligations you already have on time every time. A consistent repayment history is the number one indicator to a lender about how you will treat new credit. If you’ve been on time in the past, odds are you’ll be on time in the future.

- Ask for forgiveness. Consider writing a professional letter to creditors asking if they’re willing to remove a record of a past late payment from your report.

- Become an authorized user. See if someone with good credit may be willing to add you as an authorized user to one of their accounts. It’ll show up on your credit report, and you’ll benefit from the positive payment history.

- Report rent to the credit bureaus. If you rent your home and consistently pay your rent on time, you can ask your landlord to report the payments so they appear on your credit report. Since on-time payments account for 35% of your credit score, it’s a great way to boost your score.

Identify lenders with more lenient requirements

A lender that’s willing to approve a fair-credit borrower is key. In addition to the lenders featured above, you might explore the following lender types when looking for a personal loan:

- Credit unions. Because they are member-owned non-profits, credit unions can be more lenient in granting loans to people with imperfect credit. They often also offer lower interest rates. You must become a credit union member before you can apply for a credit union personal loan.

- Online lenders. Some online lenders consider college education or use AI to predict your repayment behavior and grant you access to loan products that your credit score can’t.

- Your local bank. A local bank may have a lender who will consider your unique situation and submit your application to underwriting with these important details.

Get prequalified

One of the most powerful tools you have at your disposal is an online prequalification tool. This lets you see if you would qualify for a personal loan with average credit—before fully applying. You can avoid a ding to your credit and see loan options that could work for you.

Add a cosigner or a co-applicant

If you have a family member or friend with good credit, you could ask them to cosign on a personal loan for you. A cosigner is jointly responsible for loan repayment, so lenders consider the cosigner’s credit and income when deciding whether to lend to you.

A co-applicant can also improve your odds of approval. A co-applicant has equal rights in the property along with an equal obligation to repay it. Personal loan lenders that allow for a co-application can include their income in your application.

Just be aware your borrowing behavior reflects on the cosigner. Don’t ask someone to cosign for you if you aren’t 100% sure you can afford to repay the loan without any late payments.

How to apply for a fair credit personal loan

Applying for a personal loan is easy and can mostly be done online. Banks, credit unions, and online lenders have technology that can approve or deny your application without a hard credit check. You don’t have to sacrifice your credit score to get the best rates and terms.

When you apply for a personal loan online, you’ll need to provide some basic information so a lender can assess your qualifications. Some of the information you may be asked to provide include:

- Your name, address, phone number, email, and other contact details

- Your birth date or Social Security number

- Details about your income and employment history

- Information about your other debts

- What you plan to use your personal loan for

- Cosigner information (if applicable)

Once you’ve submitted your application, many lenders can tell you within minutes if you are approved for the loan.

FAQ

Will a personal loan help or hurt a fair credit score?

Three main credit categories are affected when you apply for a personal loan: payment history, recent credit inquiries, and credit utilization.

Making on-time payments on your personal loan can boost your credit score by improving your payment history. Late payments can hurt it. Your score can also go down if you apply for too many personal loans over an extended period.

Taking on additional debt in the form of a personal loan increases your credit utilization, and your credit score may temporarily decrease. Your credit score will increase, however, as you pay down the principal loan amount.

Is a personal loan the best financing option for fair credit?

A personal loan isn’t the only financing tool you have with fair credit. There are other options to consider, including:

- Secured loans

- Balance transfer credit cards

- Lending circle

- Family or friend loan

About our contributors

-

Written by Alene Laney

Written by Alene LaneyAlene Laney is a personal finance writer specializing in mortgages, home equity, and consumer financial products. A credit card rewards enthusiast and mother of five, Alene enjoys sharing money-saving and money-making strategies.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.