A home equity line of credit (HELOC) can give you access to cash for debt consolidation, home improvements, or other expenses. Knowing how to shop for a HELOC matters if you hope to get the lowest rate, so we reviewed HELOC lenders to find the best. Compare our top picks below to find the right fit for you.

Table of Contents

- Reviews of the best HELOC lenders

- How we chose the best home equity line of credit lenders

- What are HELOC requirements?

- HELOC type comparisons: How to choose the best company for a HELOC lender

- Do HELOC lenders and terms vary by state?

- What can I use a HELOC for?

- How to apply for a HELOC

- Alternatives to a HELOC

- FAQ

Reviews of the best HELOC lenders

LendEDU’s picks for the best HELOC lenders are based on interest rates, loan terms, ease of applying, funding speed, and overall borrower experience.

A HELOC lets you tap into the equity you’ve built in your home as flexible cash. This cash is commonly used for home improvements, consolidating high-interest debt, or covering large one-off expenses. Rates, fees, draw periods, and application requirements vary from lender to lender, so we did the digging to help you find a strong fit.

Figure: Best company for a HELOC overall

Why Figure is one of the best

Figure is our choice as the best overall home equity line of credit because of its speedy approval and funding process for applicants with a credit score of 720 and higher. Some HELOC lenders can take weeks to make a decision and might require you to sign in person. However, with Figure, you can complete the application online and get approved in minutes.

- All HELOCs come with a fixed rate

- 100% online application and appraisal

- Get funds in as little as 5 days

- Redraw up to 100% of your funds

- Check your rate without affecting your credit score

- Figure offers online and video notary support, with an average response time of less than 45 seconds.

- No closing costs

- No annual fees

- Borrow against a primary home, second home, or investment property

- Charges an origination fee

- The full loan amount must be drawn at origination

Loan terms

| Rates (APR) | 7.45% – 16.15%* |

| Loan amounts | $15,000 – $400,000 |

| Repayment terms | Draw: 5 years / Repayment: 5, 10, 15, or 20 years |

| Prequalify | Get your estimate in under 5 minutes |

Eligibility requirements

- The property must be a single-family residence, townhome, or planned urban development. Most condos are eligible properties

- Ineligible properties include co-ops, commercially zoned real estate, and others mentioned in the outline

- Title changes within the last 90 days or properties in below-average condition are also ineligible

- Eligible in 45 U.S. states and Washington, D.C. (not available in Hawaii)

- You must have 30% or higher equity in your home

- Maximum loan-to-value (LTV): Up to 85% LTV

- Maximum debt-to-income: Up to 50%

- Minimum credit score: 640 (almost exclusively approves credit scores of 720+)

Aven: HELOC lender with best customer reviews

Why Aven is one of the best

Aven’s HELOC offers several unique benefits you won’t find with other lenders. It features a fixed interest rate throughout the life of the loan, a Lowest Rate Guarantee, and the ability to check your rate without affecting your credit score. The 100% digital application process allows for approval in as little as 15 minutes for applicants with a credit score of 720+.

Aven offers an optional Foreclosure Protection Program that will cover payments for qualified borrowers for up to a year if you lose your job. With thousands of positive reviews on Trustpilot, most of Aven’s customers agree that it’s an excellent home equity option.

- No closing costs

- No annual fees

- Offers a Lowest Rate Guarantee

- Available in 19 states

- Optional Foreclosure Protection Program

- Approval in as little as 15 minutes

- 100% digital application process

- Excellent customer reviews

- Check your rate without affecting your credit score

- 4.90% first-draw fee

- Must draw 100% of credit line at origination

Loan terms

| Rates (APR) | 6.99% – 15.49% |

| Loan amounts | $5,000 – $400,000 ($100,000) |

| Repayment terms | Draw: 5 years / Repayment: 5, 10, 15, or 30 years |

| Prequalify | Get your estimate in minutes |

Eligibility requirements

- Excluded states: South Carolina, Texas, Missouri, Nevada, Hawaii, Washington, D.C., Massachusetts, New York

- Maximum loan-to-value (LTV): Up to 89%

- Minimum credit score: 640 (720+ recommended)

FourLeaf: Best credit union HELOC lender

Why FourLeaf is one of the best

FourLeaf Federal Credit Union offers competitive rates on its HELOCs, including a low introductory rate for the first year. FourLeaf allows you to borrow up to $1 million. It covers all closing costs for lines under $500,000, saving its customers thousands in fees.

Once approved, you’ll have a draw period of 10 years, during which you can use your HELOC as needed. Once that period ends, you enter a 20-year repayment period.

- Competitive fixed introductory rateⓘ

- HELOC converts to a variable rate after 12 months

- No closing costs

- $0 in application, origination, and appraisal fees

- No annual fees

- Convert portions of your HELOC to fixed-rate loans

- Rate discounts are available if you schedule payments from a FourLeaf personal savings or checking account

- No prequalification form with a soft credit check

- FourLeaf doesn’t disclose income or debt-to-income (DTI) requirements online

- Required minimum credit score of 670

Loan terms

| Rates (APR) | 6.99% for 12 months for qualified borrowers, then variable starting at 6.75%ⓘ |

| Loan amounts | $10,000 – $1 million |

| Repayment terms | Draw: 10 years / Repayment: 20 years |

| Application | Apply online now |

Eligibility requirements

FourLeaf doesn’t disclose every eligibility requirement, such as which properties qualify and the income or DTI you need to be approved. However, here are the eligibility requirements listed on the FourLeaf website:

- For FourLeaf’s introductory rate, the maximum LTV is 75%

- Minimum credit score for borrowers is 670

- Membership at FourLeaf is required

- Hazard insurance and/or flood insurance are required for loans secured by property

LendingTree: Best Marketplace HELOC lender

Why LendingTree is one of the best

LendingTree gets our vote for the best HELOC marketplace. It isn’t a lender; rather, you can use the marketplace to compare several HELOC offers to ensure you’re getting the best rates and terms.

- Filling out the form to compare lenders doesn’t affect your credit score

- Compare offers from multiple lenders

- No costs to submit an online form

- No impact on your credit for checking offers

- Only matches you with its partner lenders

- The terms available will depend on the lenders you’re matched with

Loan terms

| Rates (APR) | Varies by lender |

| Loan Amounts | $10,000 – $2 million |

| Repayment Terms | Draw: 2 – 20 years / Repayment: 5 – 30 years |

| Application | Compare offers from multiple lenders in minutes |

Eligibility requirements

Because LendingTree is a marketplace, no one set of eligibility requirements applies to all lenders. However, most lenders on LendingTree will require good credit and a max LTV of around 85%.

Alliant Credit Union: HELOC lender with best intro rate

Why Alliant Credit Union is one of the best

Alliant Credit Union earns its spot for offering one of the more competitive introductory rates among HELOC lenders, along with low upfront costs for smaller lines. Qualified borrowers can take advantage of a six-month fixed intro rate, prequalify with a soft credit check, and avoid closing and appraisal fees on HELOCs up to $250,000.

Alliant is a good fit for borrowers who want a low-fee, digital-first credit union experience and don’t need fixed-rate conversion options. The tradeoffs are limited state availability, a required credit union membership, and fees that apply to larger credit lines. Still, for eligible borrowers focused on minimizing early borrowing costs, Alliant is worth a close look.

- 6-month fixed introductory rate for qualified borrowers

- No closing costs on HELOCs up to $250,000

- No appraisal required for HELOCs up to $250,000

- Prequalify with no impact on your credit score

- Federally insured by the NCUA

- Fully digital application experience

- Must join Alliant Credit Union

- Only available in select states

- No fixed-rate conversion option

- $50 annual fee after the first year

- $1,000 fee for HELOCs over $250,000

Loan terms

| Rates (APR) | 6-month introductory rate starting at 4.99%, with variable post-introductory rates of 8.75% – 16.00% |

| Loan Amounts | $10,000+ |

| Repayment Terms | 10-year draw / 20-year repayment |

Eligibility requirements

- Minimum credit score: 620 (720+ improves approval odds and rates)

- Maximum loan-to-value (LTV): up to 85%

- Maximum LTV in certain states: 80% in Arizona, California, Colorado, Florida, Georgia, Indiana, Michigan, Missouri, North Carolina, Nevada, Tennessee, and Utah

- Minimum home equity: must retain at least 15% equity

- Income verification required

- Eligible properties: owner-occupied one- to two-unit homes and condominiums

- Ineligible properties: co-ops, manufactured homes, and investment properties not listed

- Insurance requirements: homeowners insurance required; flood insurance may be required depending on location

- State availability: available in Arizona, California, Colorado, Connecticut, Florida, Georgia, Hawaii, Illinois, Indiana, Kentucky, Massachusetts, Michigan, Minnesota, Missouri, North Carolina, New Jersey, Nevada, New York, Ohio, Pennsylvania, Tennessee, Utah, Virginia, Washington, Wisconsin, and Washington, D.C.

For more lenders without origination, appraisal, or annual fees, check out our picks for the best no-fee HELOCs

How we chose the best home equity line of credit lenders

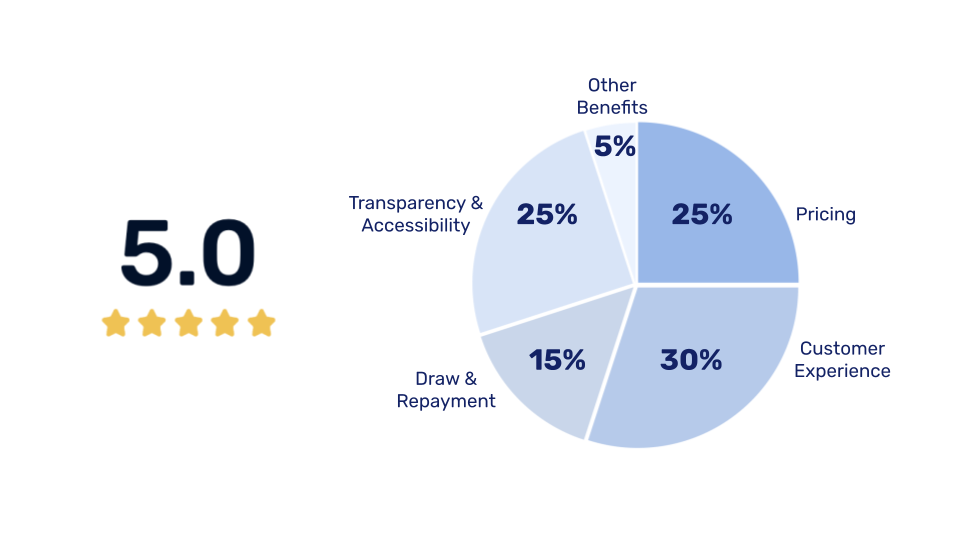

Since 2018, LendEDU has evaluated home equity companies to help readers find the best home equity loans and HELOCs for them. Our latest analysis reviewed 900 total data points across 36 lenders and financial institutions, evaluating 25 lender metrics for each.

900 data points

Across 36 lenders

25 lender metrics

We score and rank home equity lenders using five weighted categories designed to measure value, convenience, and transparency. Here is how we evaluate each category to determine our final star ratings:

Customer Experience: 30%

We evaluate a lender’s application process, company history, and customer reviews to measure overall reliability.

Pricing: 25%

We analyze interest rates, APRs, and fees to rate lenders on overall borrower affordability.

Transparency & Accessibility: 25%

We assess qualification and information sharing by checking for upfront disclosures and soft-credit check prequalification tools.

Draw & Repayment: 15%

We grade funding speed and flexibility based on payout timelines, minimum draw requirements, and repayment terms.

Other Benefits: 5%

We reward lenders for offering unique features and perks that support borrowers throughout the life of their loan.

We don’t believe two companies can be the best for the same purpose, so we only show each best-for designation once. Higher star ratings are ultimately awarded to companies that create an excellent borrower experience. This includes offering online eligibility checks, cost transparency, competitive interest rates and fees, flexible repayment plans, and unique benefits that support borrowers throughout repayment.

What are HELOC requirements?

To qualify for a HELOC, approval comes down to a few core factors:

- Credit score: While some lenders advertise minimums in the low 600s, strong credit (720 or higher) typically leads to easier approval and better rates

- Income and DTI: Lenders want to see enough income to comfortably handle payments

- Home equity (LTV): Most lenders cap borrowing at 80% to 85% of your home’s value

Use the calculator below to estimate how much you might be able to borrow based on your home value, mortgage balance, and target LTV.

If you want a deeper breakdown of lender requirements and what to expect during approval, see our full guide to home equity loan and HELOC qualification requirements.

What’s the best HELOC for excellent credit?

If you have a FICO credit score of 800 or better, you’ll have your choice of HELOC lenders. Consider FourLeaf FCU, our highest-rated credit union. With excellent credit, you’re likely to qualify for FourLeaf’s low introductory rate. The credit union’s benefits include no fees, appraisal costs, or closing costs,ⓘ the ability to lock in purchases at a fixed rate, and a longer 10-year draw period.

What credit score do you need for a HELOC?

Most HELOC lenders require a minimum credit score of 620, but borrowers with scores of 720 or higher typically get better rates and easier credit approval.

Lenders reserve their lowest annual percentage rates for borrowers with a strong credit history and proven repayment behavior, making 720 the standard threshold for competitive pricing.

If your score falls below 720, you may face a higher rate, a lower credit limit, or stricter equity requirements. Lenders also weigh other factors, like your debt-to-income ratio and how much equity you hold.

For a full breakdown of your options, see our guide to HELOCs for fair credit scores.

Tips for getting the best HELOC rate

You get the best HELOC rate by strengthening your borrower profile before you apply and comparing offers from multiple lenders.

A few moves can lower the rate you qualify for:

- Improve your credit score before applying: Pay down your balances and fix any reporting errors. A higher score signals lower risk and unlocks better pricing.

- Reduce your DTI: Lenders look closely at your debt-to-income ratio (DTI), so paying off existing debt can improve the rate you’re offered.

- Compare multiple lenders: Rates and fees differ from one lender to the next. Prequalify with a few before you commit.

- Choose the right loan-to-value ratio (LTV): Borrowing a smaller share of your home’s value often earns a better rate, since you keep your credit line amount in proportion to your equity.

- Consider rate lock options: Some lenders let you lock in your rate at account opening, which protects your budget if rates climb.

For more ways to shop smart, see our guide on how to get the best HELOC rate.

HELOC type comparisons: How to choose the best company for a HELOC lender

Finding the best company for a HELOC means evaluating more than just the advertised rate. HELOC rates, fees, draw terms, and qualification standards vary widely across lenders. The following are important considerations when comparing HELOC lenders and rates so you can find the best fit.

Introductory rates

Some HELOC lenders offer introductory rates that can lower your costs early on. These promotions usually give you a fixed, below-market rate for a limited time before the line switches to a variable rate.

| Company | Best for… | Introductory Rate | Rating (0-5) |

|---|---|---|---|

|

|

Best Credit Union | 12-month introductory rate at 6.99% for borrowers with VantageScores of 720 or higher.ⓘ |

|

|

|

Best Intro Rate | 6-month introductory rate starting at 4.99% |

|

Fixed vs. variable rates

Fixed-rate HELOCs can be a good fit if you want predictable monthly payments and less exposure to rate changes. With some lenders, each draw can be locked in at its own fixed rate, so your payment stays the same for that portion of the balance.

Variable-rate HELOCs typically start lower and can be appealing when interest rates are down, but the rate can change over time, which means your payment can too.

| Company | Best for… | Rating (0-5) |

|---|---|---|

|

|

Best Overall |

|

|

|

Best Customer Reviews |

|

Read more about fixed-rate HELOCs

Rate discounts

Many HELOC lenders offer rate discounts that can reduce your interest cost over time. Common discounts include enrolling in autopay or making payments from a lender’s account.

For example, FourLeaf offers a discount when you pay from a FourLeaf account. When comparing HELOCs, look for discounts you can easily qualify for to keep your rate as low as possible.

Learn more about current HELOC rates in this guide.

Fees and closing costs

Closing costs are upfront fees tied to opening a HELOC and can include things like appraisals, origination fees, and third-party charges. These costs often range from a few hundred to a few thousand dollars, depending on the lender. Some lenders, including Figure and FourLeafⓘ, don’t charge closing costs, which can lead to meaningful savings.

| Company | Best for… | Rating (0-5) |

|---|---|---|

|

|

Best Overall |

|

|

|

Best Credit Union |

|

Read more HELOCs with no closing costs

Maximum LTV ratio allowed

Loan-to-value, or LTV, refers to how much you can borrow compared to your home’s value. With most HELOC lenders, that cap falls between 80% and 85% of your home’s current value.

Some lenders take a different approach and base their limit on your home’s after-renovation value, allowing borrowing up to 95%, which can significantly increase how much you can access.

Convertibility

If you’re considering a variable-rate HELOC, it’s worth checking whether you can switch to a fixed rate later. Not all lenders offer this option, but it can provide flexibility if rates rise after you open your line.

Learn more about HELOC fixed-rate conversion options

Other considerations

It’s also important to look beyond rates and LTV limits. Details like loan size, credit requirements, timelines, and repayment structure can directly affect how usable and affordable a HELOC is for your situation.

That includes:

- Minimum and maximum loan amounts

- Minimum credit score and income requirements

- Application, approval, and funding speed

- Draw periods

- Repayment terms

- Fees

The easiest way to see what different lenders offer is to use our top-rated marketplace, LendingTree, to compare rates and terms.

- Up to $2 million in funding

- No fees or credit impact to compare

- Cash-out refinance options included

- $260 billion in funded loans

What is the draw period and repayment period on a HELOC?

Every HELOC runs in two stages: a draw period, which is usually 5 to 10 years, when you can borrow and pay back as you like, followed by a repayment period of 10 to 20 years.

During the draw period, you can pull from your line as needed and often make interest-only payments. Once it ends, the line closes to new borrowing and you repay the principal plus interest, so your monthly payment typically rises. Draw lengths vary by lender, with some stretching the draw period to 25 years, which keeps your access open far longer than the standard term.

Do HELOC lenders and terms vary by state?

Yes, HELOC lenders and terms can vary by state. Availability, interest rates, fees, and borrowing limits often depend on state regulations and local market conditions. Because of this, the best HELOC option in one state may look different in another.

Check out our state-specific HELOC guides to help you understand what’s available where you live.

State-specific HELOC resources

Check out the best lenders in your state:

- Alabama

- Alaska

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Iowa

- Indiana

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming

Are online HELOC lenders safe compared to local?

Online HELOC lenders are generally safe and reliable, often offering lower fees and faster approvals than traditional banks. Many of the HELOC best lenders now operate fully online.

The biggest trade-off is support. If you prefer face-to-face guidance or want to sit down with a loan officer, an online lender may feel less personal.

Some online lenders also rely more heavily on automated underwriting, which can make it harder to explain unique income situations or borderline credit profiles. That said, many online HELOC lenders make up for this with clearer pricing, fewer fees, and a faster overall process.

For borrowers who are comfortable managing the process digitally, online HELOC lenders are often just as reliable as banks and credit unions, and in many cases, more convenient.

What can I use a HELOC for?

A HELOC works well when you need flexible access to funds over time rather than a one-time lump sum. Borrowers often use it for things like home repairs, debt consolidation, education costs, or covering unexpected expenses.

Because your home secures the line of credit, how you use a HELOC matters. Some uses can strengthen your finances or add home value, while others can introduce unnecessary risk.

For a full breakdown of the best and worst ways to use a HELOC, including examples of when it makes sense and when it doesn’t, see our guide on HELOC uses.

Read more: Should you get a HELOC just in case?

How to apply for a HELOC

Applying for a HELOC generally follows a few simple steps:

- Estimate how much you can borrow based on your home equity, credit, and income

- Compare lenders and rates, often by prequalifying online

- Submit required documents to verify income, assets, and homeownership

- Complete a home valuation, which may be automated or require an appraisal

- Finalize approval and access your line of credit

If gathering paperwork feels like a hurdle, borrowers who want a lighter documentation process can look into a no-doc HELOC, which streamlines the verification step.

The video above walks through the process visually. For a deeper, step-by-step breakdown, see our full guide on how to apply for a HELOC.

Alternatives to a HELOC

A HELOC isn’t the right fit for every borrower or every property. Some homes don’t qualify, and some borrowers prefer options that don’t use their home as collateral or offer more predictable repayment.

Common alternatives include home equity loans, home equity investments, personal loans, and credit cards, each with different trade-offs around rates, risk, and repayment structure.

Homeowners who want cash without taking on a new monthly payment sometimes consider a sale-leaseback, which lets you sell your home and rent it back.

The right option depends on how much you need to borrow, how you plan to use the funds, and how comfortable you are using your home as collateral.

For a side-by-side breakdown of home equity and non-equity alternatives, including when each option makes sense and when it doesn’t, see our full guide to HELOC alternatives.

HELOC vs. a home equity loan

A HELOC is a revolving line of credit you draw from as needed, while a home equity loan gives you a single lump sum upfront at a fixed rate.

A home equity loan carries a fixed monthly payment, so you always know what you owe. A HELOC lets you borrow and repay during the draw period, so your payment can change depending on your balance and rate. A home equity loan is a good match for a known, one-time cost, while a HELOC suits ongoing or hard-to-predict expenses.

For a closer look at fixed-rate options, check out our researched recommendations for the best home equity loans.

HELOC vs. HEA

A HELOC is borrowed money you repay with interest, while a home equity agreement (HEA) — which can also be known as a Home Equity Investment (HEI) or Home Equity Sharing Agreement (HESA) — gives you cash today in exchange for a share of your home’s future value.

Because an HEA isn’t a loan, it doesn’t add a new monthly payment or count as new debt. Repayment happens when you sell the home or buy out the agreement at the end of its term. An HEA can suit homeowners who want access to their equity without added payments, while a HELOC fits those comfortable with regular repayment.

To compare the two approaches more in depth, see our breakdown of HEI vs. HELOC and our picks for the best home equity agreement.

HELOC vs. cash-out refinance

A HELOC is usually the better choice when you want flexible access to funds or already hold a low mortgage rate, while a cash-out refinance can make more sense when you need a large lump sum and current rates are at or below your existing rate.

- Structure: A HELOC adds a revolving line of credit on top of your current mortgage, while a cash-out refinance replaces your existing mortgage with a new, larger one and pays you the difference.

- When a HELOC makes sense: Rising rates favor a HELOC, since you keep your original mortgage rate untouched and borrow only what you need.

- When a cash-out refinance makes sense: A large, one-time funding need can favor a refinance, especially if you can lock a rate at or below what you currently pay.

- Cost considerations: A cash-out refinance often carries higher closing costs because it’s a full mortgage, while a HELOC typically has lower upfront costs but a variable rate that can rise.

FAQ

Can you deduct HELOC interest on your taxes?

HELOC interest is tax-deductible when you use the funds to buy, build, or substantially improve the home that secures the loan, under current IRS rules.

If you spend the money on anything else, such as paying off credit cards or covering tuition, the interest generally isn’t deductible. The deduction also applies only if you itemize, and it falls under the same combined mortgage-debt limits the IRS sets for home loans. Tax situations vary, so check with a tax professional to confirm how the rules apply to you before you file.

What is the easiest HELOC to get?

The easiest HELOCs to get are fully online options that skip the upfront draw requirement and fund within a few days. These products often work more like a credit card backed by your home, so the application feels more straightforward than a traditional HELOC.

That said, any lender will still review key details such as your credit profile, available home equity, and property eligibility. While the process can be streamlined, approval isn’t guaranteed, and the best home equity line for you will depend on your circumstances.

Where do I find a high-LTV HELOC?

You can find a high-LTV HELOC by prequalifying with several lenders and comparing their maximum LTV limits, since the ceiling varies from one to the next.

A high-LTV HELOC lets you borrow more than the 80% to 85% of your home’s value, which is where most lenders cap. If you’re borrowing for renovations, some renovation-focused HELOCs go higher still, up to 95% of what your home will be worth once the work is done, because they base the limit on its projected value rather than its current one.

What is the best HELOC with no closing costs?

The best no-closing-cost HELOC is one that waives those upfront fees entirely, which several top-rated lenders do. This offers considerable savings, since closing costs typically run 2% to 5% of your loan amount.

Watch the fine print, though. Some lenders skip closing costs but still charge an origination fee or a first-draw fee, so compare the full cost before you commit.

What is the best HELOC with no origination fees?

The best home equity line of credit with no origination fees is one that waives that charge while keeping its other rates and terms competitive. Origination fees can run as high as 5% of your loan amount, so choosing a lender that skips them can mean meaningful upfront savings. Compare a few options to find one that pairs no origination fee with a strong rate.

What is the best HELOC with no annual fees?

The best HELOC with no annual fees is one that lets you keep the line open year to year at no recurring cost, which several top-rated lenders offer. Avoiding an annual fee keeps more money in your pocket over the life of the line. For added flexibility, look for a lender with no prepayment penalty, which gives you more control over how and when you repay.

How do I know if I got a good HELOC rate?

The simplest way to evaluate whether a HELOC rate is “good” is to compare it to HELOC rates from other lenders.

However, it’s essential to remember that what constitutes a good rate for you may differ from someone else. Your credit scores and income can influence the rates you pay. The best HELOC rate is the lowest one you can be approved for based on your credit and other qualifications, considering what fits in your budget.

> Learn more about how to get the best HELOC rates

Do interest-rate hikes affect my HELOC rate?

Interest-rate hikes can affect your HELOC rate if you have a variable-rate loan. Variable-rate HELOCs are tied to an index rate; when that index rate goes up, the rate on your HELOC can also increase. HELOCs are indexed to the prime rate, which follows movements in the federal funds rate.

The federal funds rate is the rate at which banks lend to one another overnight. When the Federal Reserve adjusts the federal funds rate up or down to steer economic policy, HELOC rates can follow suit.

> Read more about how HELOC interest is calculated

How long does HELOC funding take?

The time it takes to get HELOC funds after approval can vary by lender—from a few days to several weeks. Funding may be faster with online HELOC lenders versus traditional banks or credit unions.

What is a good HELOC rate right now?

A competitive HELOC rate in 2026 generally falls between 7% to 8.5% APR, with the national average sitting around 7.5%.

HELOC rates move with the prime rate, which lenders use as a benchmark. Your individual rate then depends on your credit score, your loan-to-value ratio, and how much you draw, so a borrower with a 780 score and low LTV will see a much better offer than someone borrowing near the cap with fair credit. For up-to-date averages and how they’re trending, see our guide to current HELOC rates.

List of home equity companies we evaluated

- Alliant Credit Union

- AmeriSave

- Aven

- Bank of America

- FourLeaf FCU

- BMO Harris Bank

- Central Pacific Bank

- Citizens Bank

- Connexus

- Discover

- Flagstar Bank

- Rate

- Hitch

- Keybank

- LendingTree

- loanDepot

- Lower

- M&T Bank

- Navy Federal Credit Union

- New American Funding

- PenFed

- PNC

- Prosper

- Randolph-Brooks FCU

- Regions Bank

- RenoFi

- SECU

- Spring EQ

- Third Federal

- Trovy

- Truist

- TD Bank

- Upstart

- U.S. Bank

- Utah Community Credit Union

- Valley National Bank

Keep Learning about HELOCs

-

Where to Get a No-Closing-Cost HELOC: Best Lenders and What to Know

-

580 – 669 Credit Score? Here Are the Best HELOCs for Fair Credit

-

What Is a Home Equity Agreement? Compare the Best HEA Lenders in 2026

-

The Best No-Appraisal HELOCs and Home Equity Loans in 2026

-

The Fastest HELOCs and Home Equity Loans: Same-Day Approval and Quick Funding

1 [1] APR = Annual Percentage Rate. The introductory APR is fixed for one year (twelve months). After one year, the APR is variable based on the U.S. Prime Rate as published in the Wall Street Journal, plus a margin. To obtain an introductory rate, borrower must meet credit and loan program requirements, including (but not limited to): 1) maximum Combined Loan-to-Value (CLTV) of 75%, 2) minimum VantageScore 4.0 credit score of 720 3) borrower must take an initial draw of $25,000 and maintain this balance for 12 months, 4) borrower must have automatic transfers from a FourLeaf personal savings or checking account for the monthly HELOC payments, and 5) borrower must not have had a previous introductory rate for a FourLeaf HELOC within the past five years. The introductory rate applies to the variable line in use only and is not applicable to any Fixed-Rate Loan Option, (see below)[3]. Loan amounts over $500,000 are not available for the introductory rate. For Closing costs, see below[2].

[2] The standard APR is variable based on the U.S. Prime Rate as published in the Wall Street Journal, plus a margin (if applicable) and is subject to increase after consummation. The current standard APR is as low as 7.50% as of 7/10/2025. Not all applicants will qualify for the lowest rate and may be offered credit at higher rates and other terms based on creditworthiness. The minimum floor APR is 3.25%. HELOC rates may not exceed the maximum legal limit for Federal credit unions (currently 18%). The Prime Rate as of 7/10/2025 = 7.50%. Rates shown are based on a borrower’s primary residence, a maximum CLTV of 65%, a minimum initial draw of $25,000 taken at HELOC account opening, and automatic transfers from a FourLeaf personal savings or checking account.

Closing costs for the first $500,000 will be paid by FourLeaf but must be repaid by the borrower(s) if the HELOC is closed within first 36 months of account opening. These fees generally range between $500.00 and $15,000.00 depending on the line amount, property value, location, and/or property type. Line amounts over $500,000 may be available on a case-by-case basis to qualified applicants, are not eligible for the discounted introductory rate at any time, and the borrower(s) will be responsible for mortgage-related taxes and title insurance costs on the line amount over $500,000 (up to the approved credit limit). The total third party fees generally range between $500.00 and $60,000.00 depending on the line amount, property value, location, and/or property type. Property insurance (including flood insurance, if applicable) is required.

[3] A Fixed-Rate Loan Option (FRLO) allows you to convert an outstanding variable rate HELOC balance(s) to a fixed rate loan(s), which results in fixed monthly principal and interest payments at a fixed interest rate. A FRLO is optional and is available at the time of disbursement (account opening), or during the 10-year Draw Period. Borrowers may only have a maximum of three (3) FRLOs open at any one time. The minimum amount for each FRLO is $10,000. The minimum loan term is 5-years, and the maximum term cannot exceed the account maturity date. If you choose to convert any portion of your balance to a FRLO, the APR will be the U.S. Prime Rate as published in the Wall Street Journal that is in effect at the date of conversion, plus a margin. The margin applied will be based on your credit history, CLTV ratio, and lien position at the time of application and the term selected for the FRLO. Rates for a FRLO are typically higher than the variable rates on the HELOC account.

About our contributors

-

Written by Catherine Collins

Written by Catherine CollinsCatherine Collins is a personal finance writer and author with more than 10 years of experience writing for top personal finance publications. As a mother to boy/girl twins, she is passionate about helping women and children learn about money and entrepreneurship. Cat is also the co-host of the Five Year You podcast.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.