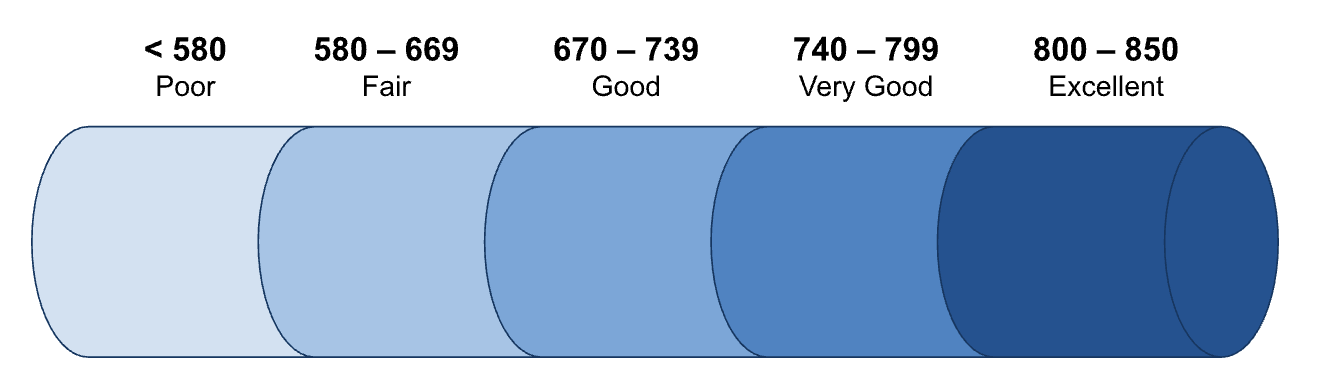

When we talk about good credit, we’re referring to FICO credit scores between 670 and 739. Scores above that range are considered excellent, and scores below are considered fair or poor.

If you have good credit, you’ll likely qualify for most forms of financing and enjoy more favorable interest rates. You can maximize the benefits of your high score by working with personal loan lenders that cater to borrowers like you.

Keep reading for the best personal loans for good credit and how to choose between them.

The best personal loans for good credit

Our lender recommendations are based on countless hours of research. We examine their APRs, loan amounts, and repayment flexibility. We also look for any special features or discounts that help these lenders stand out.

So how did these five lenders win out among the rest? The personal loan lenders below are our top choices for good-credit borrowers thanks to their low fees, competitive rates, and customer-centric experience.

Credible

Why Credible is the best marketplace

Credible isn’t a lender; it’s a one-stop loan shop. To get started with Credible, fill out the two-minute application. You’ll tell Credible about your credit profile and what you want in a personal loan. Credible then presents you with lenders that might be a match.

Credible’s lending partners offer personal loans from $1,000 to $200,000. You won’t have to borrow more than you need, but if you’re searching for a large personal loan, you’ll likely find it on the Credible marketplace.

There’s no cost and no obligation when you use Credible, though some of Credible’s lending partners may charge fees if you take out a loan with them. Use Credible’s side-by-side comparison feature to see which loan offers involve added costs and which don’t.

- Compare loans from multiple curated lenders

- Get prequalified loan offers in as little as 2 minutes

- Get funded within a few business days

- No option to apply for joint loans

| Rates (APR) | 6.99% – 35.99% |

| Loan amounts | $1,000 – $200,000 |

| Repayment terms | 1 – 10 years |

Eligibility requirements

- Soft credit check? Yes

- Minimum credit score: Varies

- Minimum income: Not disclosed

- States: Loan partners may not be available in all states

Repayment terms

Credible loans have repayment terms ranging from one to 10 years. Some lenders may charge a prepayment penalty if you pay your loan off early.

SoFi

Why SoFi is the best personal loan for good credit

SoFi is an online lender that boasts an easy application process, fast funding, and multiple ways to save. You can borrow up to $100,000, and well-qualified borrowers aren’t required to pay an origination fee on their loan proceeds.

SoFi also offers autopay, direct deposit, and direct pay discounts, giving you several options to reduce your APR.

As a bonus, 82% of SoFi personal loans are funded the same day borrowers apply. For the best chance at lightning-speed funding, apply on a business day, and sign your loan agreement before 7 p.m. Eastern.

- No origination fees, late payment fees, or prepayment penalties

- Check rates in as little as 60 seconds

- Some borrowers may qualify for same-day funding

- Higher minimum loan amount

- Autopay discount is lower than what some lenders offer

| Fixed rates (APR) | 8.99% – 29.99% with all discounts |

| Loan amounts | $5,000 – $100,000 |

| Repayment terms | 2 – 7 years |

Eligibility requirements

- Soft credit check? Yes

- Minimum credit score: 660

- Minimum income: Not disclosed

- States: All 50 states and Washington, D.C.

Repayment terms

SoFi personal loans feature terms from two to seven years. If you enroll in autopay, you’ll get a 0.25% rate discount. There’s no penalty if you decide to pay your loan off early.

LightStream

Why LightStream is the best personal loan for excellent credit

LightStream offers a fantastic borrowing experience. LightStream is so confident in its service quality that it will refund $100 if you aren’t completely satisfied.

LightStream will also lower your APR by 0.10 percentage points if you qualify for a better rate with another lender. If you apply and complete the verification process by 2 p.m. Eastern on a business day, you might even get your loan funds the same day.

The only catch, if you can call that, is that LightStream is selective. It prefers borrowers with good to excellent credit scores and a long credit history. LightStream doesn’t let you prequalify, so make sure you can meet its requirements before you apply.

- Rate match guarantee ensures that you get the best rate possible

- Same-day funding may be available

- Take advantage of a longer repayment term if you need lower payments

- No option to prequalify or check rates with a soft credit pull

- Minimum loan amount is $5,000

| Rates (APR) | 7.49% – 25.49% |

| Loan amounts | $5,000 – $100,000 |

| Repayment terms | 2 – 12 years |

Eligibility requirements

- Soft credit check? No

- Minimum credit score: 660

- Minimum income: Not disclosed

- States: All 50 states and Washington, D.C.

Repayment terms

LightStream offers some of the longest repayment terms of any lender, giving you up to 12 years to repay your loan. You can pay your loan off early, without a prepayment penalty and rate discounts can help bring the cost of your loan down.

Happy Money

Why Happy Money is the best personal loan for credit card debt

Happy Money created its Payoff Loan to help borrowers get out of credit card debt for good. While you’re knocking down your revolving debt, you might see a score increase: Happy Money reports that its customers’ credit scores went up by an average of 40 points after they took out and paid off a loan.

Happy Money lets you optimize your repayment plan to get the lowest payment, best APR, or quickest payoff. You can also choose to receive your funds or let Happy Money pay your creditors for you. That puts you in the driver’s seat from start to finish.

You can check your rates with Happy Money before you apply, but this lender is more transparent than others about its underwriting criteria. As long as your credit score is above 640, you have solid approval odds with Happy Money, but delinquencies could be grounds for denial.

- Send payments directly to creditors

- Choose your loan repayment term and due date

- Free monthly credit score monitoring

- Origination fee from 1.5% to 5.5%

- Not available for uses other than credit card debt

| Rates (APR) | 12.45% – 17.99% |

| Loan amounts | $5,000 – $40,000 |

| Repayment terms | 2 – 5 years |

Eligibility requirements

- Soft credit check? Yes

- Minimum credit score: 640

- Minimum income: Not disclosed

- States: Loans not offered in Nevada or Massachusetts

Repayment terms

Happy Money lets you choose personal loan terms ranging from two to five years, so you can get a payment that reflects your budget. There are no prepayment penalties, and you won’t be charged a fee if your payment is late. Happy Money doesn’t offer rate discounts at this time.

Upgrade

Why Upgrade is the best personal loan for fair credit

Consider Upgrade if your credit score is between fair and good. Upgrade lends to borrowers with credit scores as low as 580, so good-credit borrowers stand a reasonable chance of getting approved.

In addition to its more generous underwriting criteria, Upgrade also offers three rate discounts. You can get a lower rate by enrolling in autopay, using your vehicle as collateral, or putting some or all of your loan toward debt payoff.

What really puts Upgrade in a league of its own is its joint application acceptance. Many personal loan lenders require borrowers to apply solo, but not Upgrade. If you know someone with better credit, applying together could help you qualify for a lower rate or larger loan.

- Choose your monthly payment and loan term

- Joint applications accepted

- Loan funds may be available in as little as 1 day

- Smaller loan maximum limit

- 1.85% to 9.99% origination fee

| Rates (APR) | 8.49% – 35.99% |

| Loan amounts | $1,000 – $50,000 |

| Repayment terms | 2 – 7 years |

Eligibility requirements

- Soft credit check? Yes

- Minimum credit score: 580

- Minimum income: Not disclosed

- States: All 50 states and Washington, D.C.

Repayment terms

Upgrade loans have repayment terms from two to seven years, and your monthly due date is adjustable to fit your budget. A short-term financial hardship program is available if you’re temporarily unable to manage payments.

How good credit affects personal loan approval

While you don’t need a specific credit score for personal loan approval, better scores generally mean better odds. Good credit scores can also help you qualify for larger loan amounts, more repayment options, and lower interest rates.

The differences between rates across the credit score spectrum are worth noting if you’re shopping for a loan. Here are the average personal loan interest rates as of July 2023:

| Credit range | Avg. rate |

| 720 – 850 | 11.30% |

| 690 – 719 | 15.60% |

| 630 – 689 | 22.30% |

| 300 – 629 | 25.20% |

Notice how the average rate decreases as scores increase. Some lenders, like Upgrade, accept borrowers with scores down to around 580, but that approval comes at the cost of a higher interest rate.

On the other hand, higher credit scores—very good or excellent—tend to have no trouble getting approved. These borrowers can take out higher personal loans at lower interest rates.

To give yourself the best chance at an affordable interest rate, don’t rush into a loan application. Pull your credit reports first, and find ways to increase your score. When your credit is in a better position, shop around with different lenders to find the best personal loan offer for you.

How to identify the best personal loans for good credit

As you look for a personal loan, pay close attention to each lender’s fine print. Just because you’re preapproved doesn’t mean you’re getting the best deal.

Here are important features to look for and compare:

- Rates: Which lender offers you the lower APR? Does the lender provide ways to reduce that rate, perhaps through an autopay discount?

- Terms: How long does each lender give you to pay back your loan? Can you choose your repayment period? How do the available repayment terms affect your monthly payment?

- Loan limits: How much does each lender let you borrow? Are these loan amounts sufficient to cover your needs?

- Fees: Do these lenders charge additional costs, such as late fees or origination fees? Can you avoid or prevent these fees, or are you obligated to pay them if you accept the loan?

- Perks: Do any lenders offer special benefits? What, if anything, are they bringing to the table that sets them apart?

Ideally, you’ll prequalify with several lenders before submitting a full application, giving you a wide pool of options. Dissect each loan offer before you sign your loan agreement, and weigh each of these characteristics against your individual financial situation.

Maybe one lender offers extended repayment terms, but another provides hardship assistance. If you work in a high-layoff industry, that hardship assistance might be more important than shaving a few bucks off your monthly payment.

Once you find a loan package that meets at least some of your criteria, you’re ready to apply for and accept your personal loan offer.

How to apply for a good credit personal loan

When it comes time to apply for your personal loan, you’ll need to furnish proof of identity and income to your lender. Here’s how it works with most lenders:

- Prequalify online. Don’t jump straight into an application without first getting prequalified. If you haven’t checked your rates with a soft pull yet, do that first.

- Provide your identifying and financial information. If you didn’t do this during prequalification, you’ll need to enter your name, full Social Security number, and employment details.

- Submit verification documents. You might do this now or later in the application process, but at some point, your lender will need to see a government ID and pay stubs or W-2s to confirm your income.

- Consent to a hard credit check. Before a lender can fund your personal loan, it needs to run your credit. Read through your lender’s disclosures, and agree to the credit check to move forward.

- Wait for a decision. Our recommended personal loan lenders can offer decisions in a matter of minutes, but this might take a day or two, especially if your lender requests additional information.

- Sign your loan agreement. Review it, ask your lender for clarification where needed, and when you’re ready, sign to accept your loan.

- Get your funds. Most lenders will disburse your personal loan proceeds to your bank account. You’ll often get your funds one to two business days after signing your agreement, but some lenders (like SoFi) can fund loans the same day.

In all, expect the personal loan process to take a day or two. Although personal loan applications generally don’t take long to fill out, your lender needs time to review your information and make a decision.

To expedite your personal loan, gather any necessary documents ahead of time. Have your driver’s license or another form of government ID ready, and download your bank statements, pay stubs, or tax returns (if you’re self-employed) before you begin the application.

FAQ

Could a personal loan hurt a good credit score?

Because personal loans involve a hard credit inquiry, they can hurt your credit score. Opening a new loan also adds to your outstanding debt balance and decreases your average age of accounts.

Any immediate negative impact on your credit score will lessen over time as long as you pay back your loan as agreed.

Is a personal loan the best financing option for good credit?

Whether a personal loan is the best financing option for good credit depends on how you want to use the money and how much you need to borrow.

Home equity loans and lines of credit often allow you to borrow more, while credit cards give you ongoing access to funds. However, you can’t use most personal loans to cover tuition or business expenses, so if that’s why you need funding, look into student loans or business loans instead.

Recap of the best personal loans for good credit

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.