If you’re shopping for a personal loan, chances are you’re prioritizing affordable monthly payments. You’re looking for repayment options that suit your budget without costing you an arm and a leg in interest.

You’re a smart borrower, and you understand the importance of being able to calculate your loan payment yourself. Keep reading for a step-by-step guide on calculating your loan payments and your interest.

Table of Contents

How to calculate personal loan payments

Knowing what goes into your personal loan payments is the first step in calculating them. Before we move on to equations and examples, familiarize yourself with these terms:

| Term | Definition |

| Principal | The initial loan amount before adding interest |

| Interest | The price you pay to borrow money |

| Interest rate | The percentage of your outstanding principal that gets charged as interest |

| Rates (APR) | A percentage that tells you your total borrowing cost, including interest and fees |

| Fixed rate | An interest rate or APR that doesn’t change |

| Variable rate | An interest rate or APR that can fluctuate |

| Installment loan | A loan with consistent monthly payments |

| Amortization | The dollar amount you pay each month toward your loan balance |

| Loan term/repayment term | How long you’ll make payments toward your loan balance |

| Amortization schedule | Schedule that determines how your monthly payments are split between principal and interest |

Now, let’s get to the fun part. To calculate your loan payments, we’ll use this equation:

The math will make more sense when we go through an example. If you’ve already prequalified or been approved for a loan, you can follow along with your own numbers. But what numbers do you need, and where do you find them?

Information you need when calculating personal loan payments

To accurately calculate your personal loan payments, have this information handy:

- Your loan amount

- Your APR

- Your loan term

You can find this information in your prequalification or approval offer.

Forgot to save a copy of your offer? Check your email for a message from your lender. Many lenders send follow-up emails after you prequalify, either with a summary of your terms or instructions on pulling up a recent quote.

If you haven’t yet checked your rates with any of our recommended personal loan lenders, you can use these figures instead:

- How much you plan to borrow

- The average rate for your credit score

- Your ideal repayment period

When you start the prequalification process, try to get quotes from four or five lenders. Each time you do, use our guide to determine what your payments would be with each one before accepting a loan.

Example of calculating your personal loan payment

We’ll go through our first calculation step by step. Then, we’ll show you how changing each variable—principal, interest rate, and loan term—can affect your payment amount.

While you can do these calculations by hand, we recommend using a calculator. Not only will a calculator help you work more quickly, it’ll also ensure a higher degree of accuracy.

Let’s dive in.

Step 1: Understand your numbers

For our first example, say you’re in the market for a $15,000 debt consolidation loan. You prequalified for a 24.99% APR, and you want a 48-month repayment term. Here’s how to classify each of those numbers:

- Principal: $15,000

- APR: 24.99%

- Term: 48 months

Eventually, we’ll plug these numbers into our equation. Notice, though, that we’re working with APR, which is an annual rate. We’re calculating our monthly payment, which requires a monthly rate. That leads us to step two.

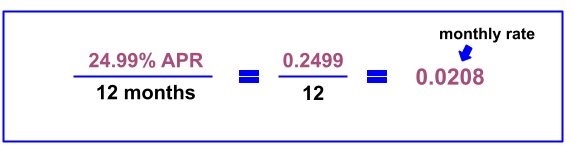

Step 2: Turn your annual rate into a monthly rate

Before we can fill in our formula, we have to convert our APR into a monthly rate. Here’s how:

- Change 24.99% into a decimal by moving the decimal point two places to the left.

- Divide our annual rate—now expressed as 0.2499—by 12. We’re dividing by 12 because you’ll make 12 payments each year of your repayment period.

- Round your monthly rate to four decimal places. Dividing 0.2499 by 12 should give you 0.020825. You can use that full number if you’d like, but since 0.2499 has four decimal places, we’ll go ahead and round down to four in our answer.

Those three steps will give us our monthly rate, 0.0208, which we’ll use for the remainder of our calculations.

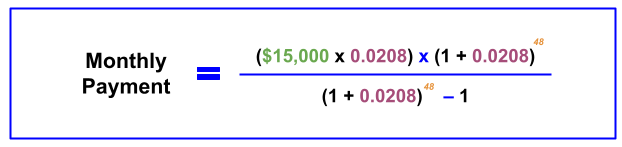

Step 3: Plug in your numbers

Now that we’ve figured out our monthly rate, we can fill in our formula. Here’s an update on the numbers we’re using:

- Principal: $15,000

- Monthly rate: 0.0208

- Term: 48 months

All we have to do is place these numbers where they belong in our equation, like so:

If you’re thinking of your repayment term in years, multiply it by 12 to get the total payments. For example, a four-year term equals 48 total payments.

Now that our equation is filled in, we’ll move on to our parentheses.

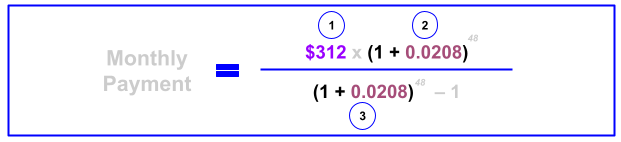

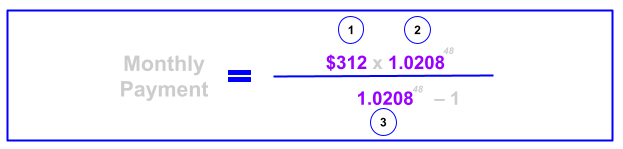

Step 4: Perform the calculations inside parentheses

If you remember PEMDAS—parentheses, exponents, multiplication, division, addition, subtraction—from your elementary school math days, this is your time to shine. In step four, we’ll do the calculations inside parentheses, in this order:

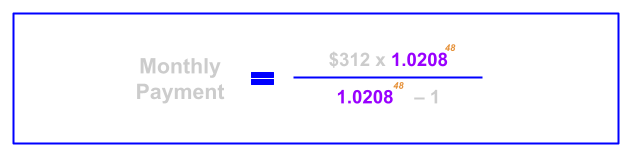

For our first parenthetical calculation, we’re multiplying the amount we borrowed, $15,000, by our monthly rate, 0.0208. This gives us an even $312:

Our next two parentheses involve the same calculation. We’re just adding one to our monthly payment rate. Once we do this for the second set of parentheses, we can replace our third parentheses with that same answer, 1.0208.

Your formula should now look like this:

With the parentheses gone, we can take care of the exponents.

Step 5: Get rid of your exponents

Technically, what we’re doing in step five is called exponentiation. That’s the mathematical way of saying we’re working with our exponents next. For this step, we’re focusing on these numbers:

Like our parentheses, these two sets of numbers involve the same calculation. We only need to do the math once, then we’ll replace each set of numbers with our result.

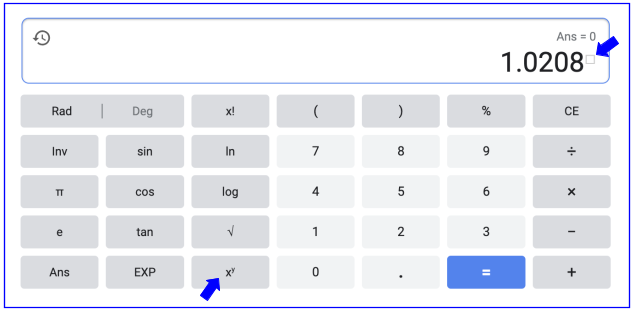

If you haven’t used a calculator yet, you may want it for this step. Google’s search engine has a built-in calculator, which we’ll use here. When you have your calculator of choice, this is what you’ll do:

- Type in our results from our parenthetical calculation, 1.0208.

- Click the “xy” button. After you click it, you should see a small box in the calculation pane.

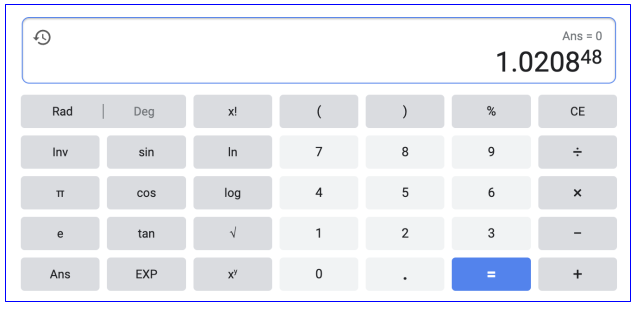

- Type in your total number of monthly payments, 48. Notice how the “48” replaces the small box.

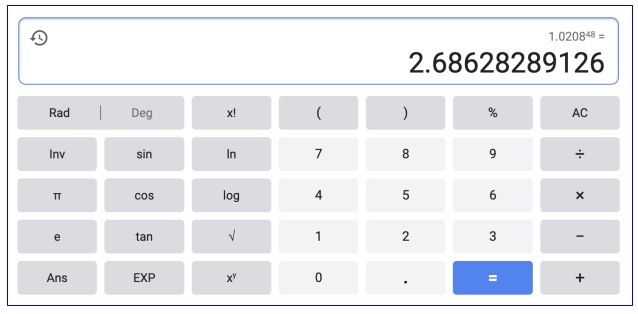

- Click the equal sign to see your result.

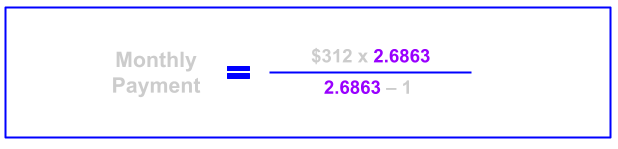

We will round this down to four decimal places to get 2.6863. Then, we’ll go back to our formula and replace the appropriate fields with 2.6863, like this:

If you’ve made it this far, breathe a sigh of relief. The hardest part of calculating your personal loan payment is behind you. All that’s left is simple multiplication, subtraction, and division.

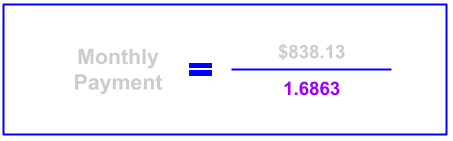

Step 6: Solve your numerator and denominator

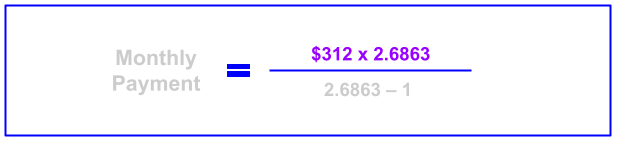

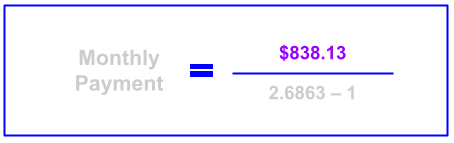

The final two steps are quick and easy. For step six, start with your numerator (the numbers above the blue line) and multiply $312 by 2.6863:

After multiplying, this is how your equation should look:

Next, solve your denominator (the numbers below the blue line) by subtracting 1 from 2.6863:

This one’s straightforward, resulting in 1.6863:

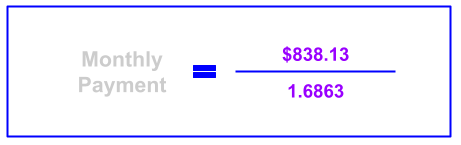

We only have one step left—and it’s the step you’ve all been waiting for.

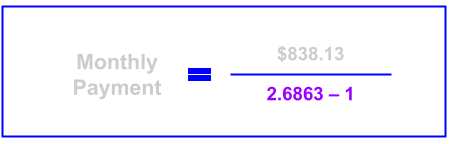

Step 7: Divide to get your monthly payment

Step seven is our last step. All you need to do here is divide $838.13 by 1.6863:

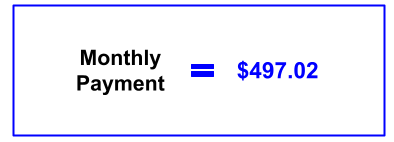

Now, we know that the monthly payment amount for a $15,000, 48-month personal loan with a 24.99% APR is $497.02:

To recap, these are the seven steps we used to find our monthly personal loan payment:

- Gathered our loan information, including principal, APR, and loan term

- Divided our APR by 12 to get our monthly rate

- Plugged our numbers into our formula

- Performed the calculations inside parentheses

- Solved for our exponents

- Solved the equations in our numerator and denominator

- Divided the numerator by the denominator

You can follow this same process to compare loan offers and find your monthly payment for each one.

You can also use our personal loan calculator to get an idea of your monthly payment or to check your math. Due to differences in rounding, your math and the results you get with our calculator may be off by $1 to $2.

A good rule of thumb is to have a debt-to-income ratio of 36% of your gross income or less. This amount includes all debts, such as your mortgage, car payment, student loans, or other personal debts. If your debt ratio is higher, you’re probably not in a good position to take out a personal loan.

Chloe Moore, CFP®

How do interest rate and loan terms change your personal loan payment?

As you compare offers, you’ll find that different interest rates and repayment periods can drastically change your monthly payment.

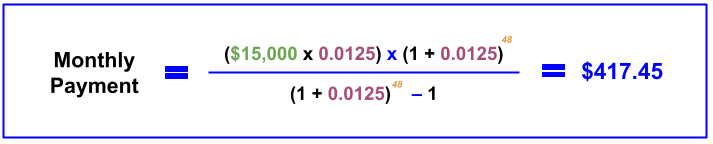

In our last example, we had a hypothetical $15,000 loan with a 24.99% APR and 48-month terms. But what if our APR was much lower at 14.99%?

After converting that APR to a monthly rate and using the steps in the previous section to work through our formula, we’ll find that our monthly payment at this lower rate is $417.45:

That’s roughly $80 less than our monthly payment at 24.99%.

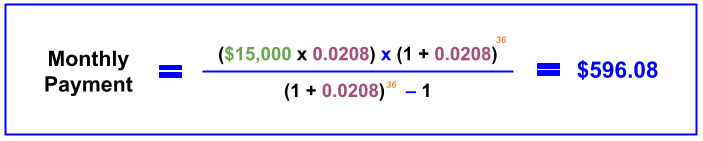

And what if, instead of a lower interest rate, we wanted to see how a shorter loan term impacted our monthly payment amount?

If we borrow $15,000 at the same 24.99% APR we used in our first example, but this time with 36-month terms, here’s how our formula and monthly payment would change:

That shorter repayment window resulted in a much higher monthly payment. We went from $496.62 to $596.08.

That doesn’t necessarily mean it’s a bad offer, though. Now that you’re comfortable calculating your total monthly payment, it’s time to learn how to calculate your monthly interest expense.

How to calculate your personal loan interest

Calculating your personal loan interest is just as important as calculating your personal loan payment. How much you pay in interest ultimately determines how much you pay for the loan itself, so adding this equation to your loan comparison arsenal is key to finding the best offer.

Use this formula to find the total interest due on your loan:

Notice that we’re using interest rate instead of APR here. The distinction between these two numbers is a subtle but important one. Your interest rate is part of your APR, but your APR also includes personal loan fees, such as your origination fee.

Using your APR for this calculation will throw off your numbers, and you won’t get an accurate measure of how much interest you’ll pay for your loan. Your loan offer may distinguish how APR is split between interest and fees, but if not, ask your lender to clarify.

Now, let’s see the interest equation in action.

Example of calculating your personal loan interest

You’ll use your loan’s principal amount, interest rate, and repayment term to calculate your personal loan interest.

You don’t need to convert your interest rate to a monthly rate this time, but you must convert it to a decimal. You also need to convert your repayment term from months to years.

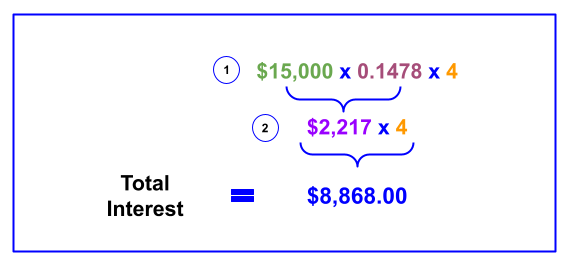

Using the numbers from our previous example, say we borrow $15,000 with a 24.99% APR and 48-month terms. Our lender confirms that our APR includes a 14.78% interest rate. When we plug those numbers into our equation, we get this:

After prepping our equation, we’ll multiply across from left to right.

First, we’ll multiply $15,000 by 0.1478. Then, we’ll multiply that number by four, like this:

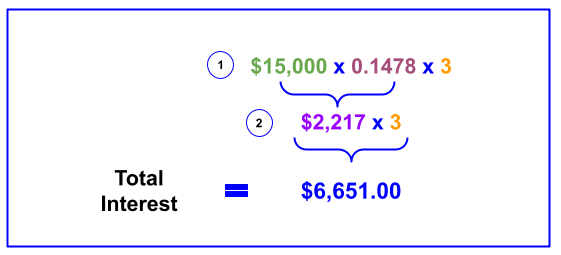

We know this loan will cost us around $8,868 in interest by the time it’s paid off. If we chose 36-month terms instead, our equation and total interest would look like this:

Granted, the shorter 36-month repayment period results in a $100 monthly payment increase. As we can see from our interest calculation, however, it saves us $2,217 in interest.

Whatever your interest expense, remember that it may not be divided evenly from month to month or year to year.

If your interest is amortized, your interest payment changes based on your outstanding principal. The majority of your first several payments go toward interest, and the majority of your final payments go toward principal.

You can calculate your monthly amortized interest payment yourself, or you can ask your lender for both annual and monthly amortization schedules. Assuming a $496 monthly payment, your annual amortization schedule may look like this:

| Year | Interest | Principal |

| 1 | $3,475.87 | $2,491.41 |

| 2 | $2,776.77 | $3,190.51 |

| 3 | $1,881.49 | $4,085.79 |

| 4 | $734.99 | $5,232.29 |

Your interest is front-loaded in the first year. By year two, the portion of your payments going to interest gradually tapers off. You’re still paying interest, but a larger percentage of your monthly payments is applied to the principal the closer you get to repayment.

What affects my personal loan payments?

As you’ve seen from our calculations, these factors have the biggest impact on your monthly payments:

- Principal: Borrowing more upfront often means paying more monthly and in interest over the life of your loan.

- Interest rate or APR: Higher rates generally lead to higher monthly payments and a higher overall borrowing cost.

- Loan term: Shorter loan terms usually result in increased monthly payments. The tradeoff is that those higher payments help you pay down your loan faster, and you’ll pay less in the long run.

These aren’t the only factors, though. Your monthly payments also depend on:

- Your credit score: People with higher credit scores generally qualify for larger loan amounts, lower rates, and more flexible repayment terms.

- Your lender: Choosing a lender with higher personal loan fees or higher starting APRs can increase your total borrowing cost, even if you have good credit and even if your payments seem affordable.

That’s why reliable loan comparison involves more than just calculating your monthly payments.

When you look beyond payments and examine how interest, APR, terms, and fees work together, you’ll get a glimpse at your loan’s actual cost—and that’s how you’ll know if you’re getting the best deal.

If you don’t qualify for a loan you can afford, you have a few options. Consider reducing the loan amount or increasing the loan term. Remember that a longer loan term could mean a slightly higher interest rate. In all cases, it’s important to understand your financial situation before taking on debt to feel confident that the loan does not create an additional burden.

Chloe Moore, CFP®

Can I pay off my loan early?

Regardless of your monthly payment amount or forecasted loan cost, you can (almost) always pay off your loan early. Lenders like SoFi and Upstart don’t assess prepayment fees. If your lender doesn’t either, you stand to save hundreds—if not thousands—in interest charges.

When you pay down your principal ahead of schedule, you whittle down your future interest expense at the same time. This is especially true if your interest is amortized.

The best part is you don’t have to throw tons of extra money at your loan to reap the benefits of an early payoff. Any action you take to reduce your debt, no matter how small that action seems, is worth the effort—and worth being proud of.

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Chloe Moore, CFP®

Reviewed by Chloe Moore, CFP®Chloe Moore, CFP®, is the founder of Financial Staples, a virtual, fee-only financial planning firm based in Atlanta, Georgia, and serving clients nationwide. Her firm is dedicated to assisting tech employees in their 30s and 40s who are entrepreneurial-minded, philanthropic, and purpose-driven.