Our take: Alliant Credit Union’s HELOC stands out as a great low-fee option for eligible borrowers who prefer a digital-first credit union, but it’s only available in select states and doesn’t offer a fixed-rate conversion. (Check out our picks for the best HELOCs.)

Details

- No closing costs

- No appraisal required for HELOCs up to $250,000

- 6-month fixed introductory rate for qualified borrowers

- Prequalify with no impact on your credit

- Federally insured by the NCUA

- Only available in AZ, CA, CO, CT, FL, GA, HI, IL, IN, KY, MA, MI, MN, MO, NC, NJ, NV, NY, PA, TN, UT, VA, WA, WI, & DC

- Must join the credit union

- $50 annual fee after year one

- $1,000 fee if borrowing over $250,000

| Rates (APR) | 6-month introductory rate starting at 4.99%, with variable post-introductory rates of 8.75% – 16.00% |

| Loan amounts | $10,000+ |

| Repayment terms | 10 yr. draw / 20 yr. repayment |

| Min. credit score | 620 |

Alliant HELOC alternatives

Alliant’s HELOC is a strong option for digital-savvy borrowers who live in eligible states and want to minimize upfront costs. But it may not be the best fit if you want faster funding, broader availability, or fixed-rate conversion options.

Here’s how it compares to top competitors:

- Alliant vs. Figure: Figure offers a fully digital HELOC alternative with funding in as little as five days and fixed interest rates. It’s available in more states and doesn’t require membership. However, Figure charges up to 4.99% in origination fees, making it more expensive upfront than Alliant if you qualify for the $0-fee tier.

- Alliant vs. Aven: Aven offers a fully digital HELOC, Aven Home Equity Cash, with a fixed interest rate, no closing costs, and approval in as little as 15 minutes for well-qualified applicants. It’s available in 38 states and includes a Lowest Rate Guarantee and optional foreclosure protection.

- Alliant vs. FourLeaf Federal Credit Union (formerly Bethpage FCU): FourLeaf offers a 12-month fixed intro rate (6.49% APR) and lets you convert portions of your balance to a fixed-rate loan. It also covers closing costs for lines up to $500,000.ⓘ

Alliant Credit Union offers a no-frills HELOC with a low introductory rate and no closing costs on lines up to $250,000. You can prequalify with a soft credit check and avoid an appraisal if your loan is under that limit.

But it’s not available in all states, and membership is required to close. If you’re eligible and want to save on fees, it’s worth considering. Here’s how the Alliant HELOC works and how it compares to lenders with broader availability or digital-first experiences.

Table of Contents

How does Alliant Credit Union HELOC work?

A home equity line of credit (HELOC) from Alliant Credit Union gives you flexible access to cash based on the equity in your primary or secondary residence. You can borrow as little as $10,000, or $25,001 in Washington, D.C., and Wisconsin, with a draw period of 10 years and a 20-year repayment window.

The first six months come with a low fixed interest rate, followed by a variable rate for the remainder of the loan. You can use the line for any purpose, whether you’re renovating your home, covering large expenses, or consolidating debt.

For credit lines up to $250,000, Alliant waives appraisal and closing costs, making it a cost-effective option for many borrowers. The online application process is straightforward, and you can prequalify without hurting your credit.

Alliant Credit Union HELOC terms

| Terms | Details |

| Eligible properties | Owner-occupied 1–2 unit homes, condos; no investment properties |

| Rates (APR) | 6-month introductory rate starting at 4.99%, with variable post-introductory rates of 8.75% – 16.00% |

| Rate discounts | 0.25% with autopay from an Alliant account |

| Loan amounts | Minimum $10,000* |

| Draw period | 10 years (interest-only payments) |

| Repayment period | 20 years |

| LTV limit | Up to 85% (80% in some states) |

| Fees | None for loans ≤ $250,000; $1,000 setup fee if over; $50 annual fee after year one |

| Prepayment penalty | None, but $200 early closure fee if loan is closed within 36 months |

| Access | Online/mobile transfers, checks (on request), phone |

Pros and cons of Alliant Credit Union

Pros

- Low 6-month fixed intro rate

- No closing or appraisal costs under $250K

- Borrowers save on upfront costs if their line is $250,000 or less.

- Soft credit check prequalification

- You can see your potential rate without affecting your credit score.

- Digital-first experience with strong app ratings

- Apply online and manage your account through a well-rated mobile app.

- Up to 85% loan-to-value (LTV)

- Lets you borrow more against your home than many competitors, depending on your location.

Cons

- Limited state availability

- Membership required

- You’ll need to join the credit union and open a savings account to close on your HELOC.

- Annual and early closure fees

- A $50 annual fee kicks in after the first year, and you’ll pay $200 if you close the account within 36 months.

- No fixed-rate conversion option disclosed

- Unlike some competitors, Alliant doesn’t advertise the ability to lock in fixed-rate segments.

Alliant Credit Union customer reviews

Alliant Credit Union earns mixed customer reviews, especially regarding general banking services. Here’s a snapshot of recent review data:

| Source | Customer rating | Number of reviews |

| Trustpilot | 3.2/5 | 132 |

| 4.2/5 | 1,570 | |

| Better Business Bureau (BBB) | 1.47/5 | 47 |

On Trustpilot and Google, reviewers often mention helpful mobile features and favorable loan rates. But many complaints focus on customer service issues, slow response times, and frustrating dispute resolution processes, though these aren’t always specific to the HELOC product.

Despite those concerns, Alliant’s mobile banking apps are well rated, which suggests a good digital experience for borrowers.

Do I qualify?

Alliant considers several factors when reviewing your application, including your income, credit history, and how much equity you have in your home. Here’s what we know about eligibility:

| Requirement | Details |

| Credit score | 620 minimum (720+ for best likelihood of approval and lower rates) |

| LTV | Up to 85% (80% in some states) |

| Min. home equity | Must retain at least 15% equity |

| Employment/income | Income verification required |

| Property types | 1–2 unit owner-occupied homes, including condos |

| Ineligible properties | Co-ops, manufactured homes, and investment properties not listed |

| Insurance requirements | Homeowners insurance required; flood insurance may be required |

How do I apply with Alliant?

You can apply for an Alliant HELOC entirely online, even if you’re not yet a member. The application is straightforward and includes several steps.

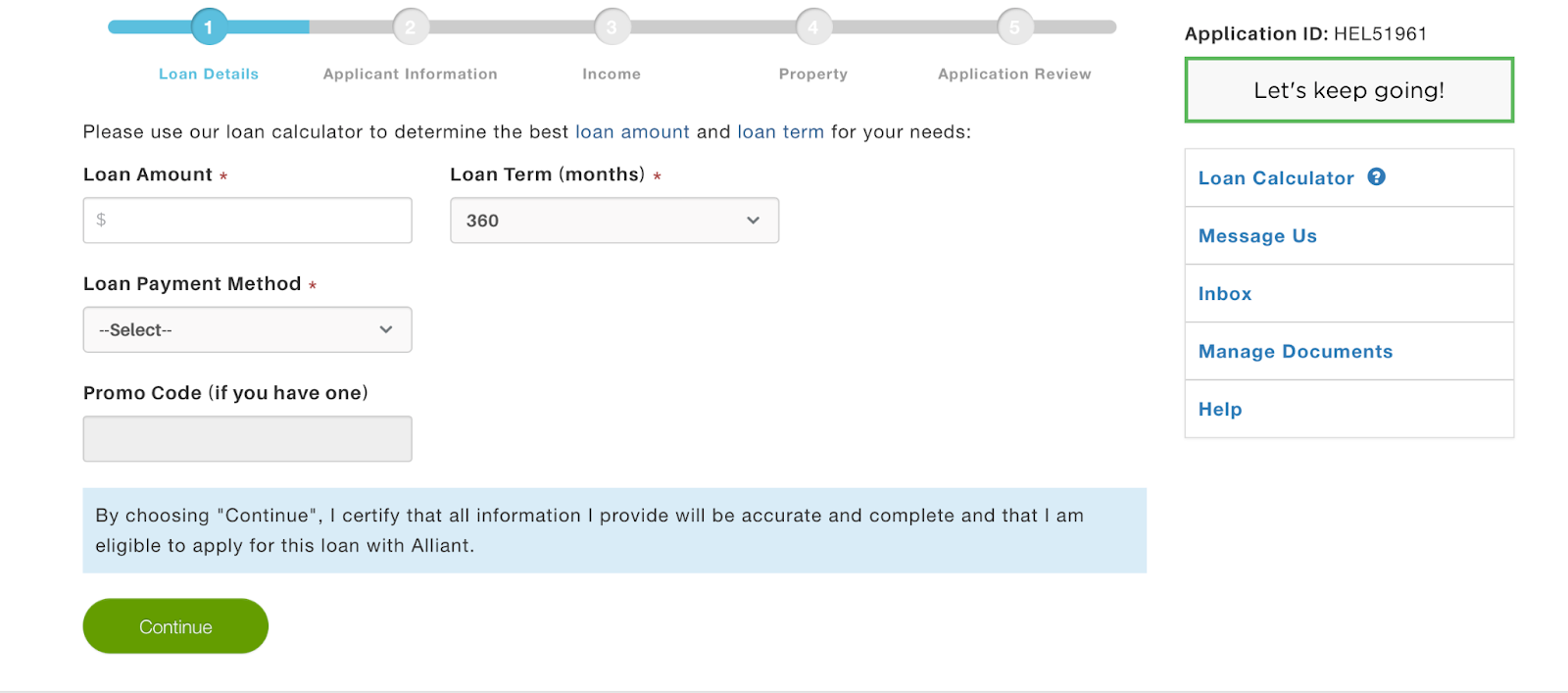

- Start the online application. Visit Alliant’s website and click “Apply Now.” You’ll select your state and the type of property you’re borrowing against.

- Input basic loan details. Provide information about your desired loan amount, how you plan to use the funds, and any co-applicants.

- Submit personal and financial information. Alliant will request details about your income, employment, and existing debts. You’ll also upload recent pay stubs or other income documents.

- Prequalify with no credit impact. You can see your potential rate and loan terms without a hard credit pull.

- Join the credit union. If you’re approved and ready to move forward, you’ll open a savings account with at least $5 to finalize your membership.

- E-sign and close remotely. Alliant uses DocuSign for most closings, and you can receive final paperwork via FedEx if needed.

Alliant says funding typically takes 10 to 30 days, depending on your location, documentation, and whether an appraisal is required.

What does the appraisal process look like?

For credit lines up to $250,000, Alliant does not require an appraisal. This is a major benefit that helps speed up the approval process and reduce costs.

If your property doesn’t qualify for automated valuation (AVM), or if your line exceeds $250,000, Alliant may require a full appraisal. You’ll cover that cost unless otherwise stated.

Appraisals may be required in situations like:

- AVM is unavailable or inaccurate

- Your home is in a federally declared disaster area

- Your property is unusual or hard to value

Appraisals typically involve an in-person visit by a licensed appraiser and can add a few weeks to the process.

Alliant customer service

Alliant is a digital-first credit union, so it doesn’t operate physical branches for in-person support like many traditional banks or credit unions.

Here’s how to get help:

- Phone: Call 800-328-1935 anytime (24/7 general support; loan specialists available Monday–Friday, 7 a.m. to 7 p.m. Central time)

- Secure message: Use the messaging center in your Alliant online portal

- Chat: Available on the website for real-time assistance

- Mailing address: Alliant Credit Union P.O. Box 2387 Des Plaines, IL 60017-2387

While Alliant’s remote support options are robust, some reviewers note long response times or frustrating interactions, especially during busy periods.

How we rated Alliant Credit Union

We designed LendEDU’s editorial rating system to help readers find companies that offer the best home equity products. Our system awards higher ratings to companies with affordable solutions, positive customer reviews, and online transparency of benefits and terms.

We compared Alliant to several home equity lenders, using hundreds of data points from company websites, public disclosures, customer reviews, and direct communication with company representatives. We weighted, scored, and combined each factor to produce a final editorial rating. This rating is expressed on a scale from 1 to 5, with 5 being the highest possible score. Our take is represented in our rating, recapped below.

| Company | Rating (0-5) | |

|---|---|---|

|

|

|

About our contributors

-

Written by Amanda Hankel

Written by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.