Imagine tapping into your home’s value—not just once, but as often as you need. Home equity lines of credit (HELOCs) let you do exactly that. Once you open your HELOC, you can easily draw from your equity to cover one-time or ongoing expenses.

Delaware homeowners especially can benefit from this financial product as home values in the state continue to increase. We’ve compared numerous HELOCs for Delaware homeowners and narrowed our list to the best. Keep reading to find the right Delaware HELOC for you.

| Company | Best for… | Rating (0-5) |

|---|---|---|

|

|

Best overall |

|

|

|

Best credit union |

|

|

|

Best marketplace |

|

Reviews of the best online HELOCs in Delaware

Online HELOCs leverage the power of technology and automation. You can apply right from your phone, and you may be able to forego an in-person appraisal, too. If innovation and convenience are a top priority, these online HELOC lenders are a solid match:

Figure

Why we picked it

Figure is our top pick for a HELOC due to its blend of competitive fixed rates, quick funding, and flexible terms.

Advanced technologies such as blockchain and AI ensure a fast and efficient approval process, with funds available in as few as five days. This makes Figure ideal for borrowers seeking quick and reliable access to home equity without the traditional banking hassle.

- Fixed interest rates

- No in-person appraisal is needed

- Option to redraw up to 100% of funds

- Funding can be available in as few as 5 days

- Check your rate without affecting your credit score

Loan details

| Rates (APR) | 6.55% – 15.54% |

| Loan amounts | $20,000 – $750,000 |

| Draw period | 2 – 5 years |

| Repayment term | 10, 15, 20 or 30 years |

| Funding time | As few as 5 days |

| Properties | Primary home, second home, or investment property |

| Minimum credit score | 640 |

Figure Disclosures

- The Figure Fixed Rate Home Equity Line is an open-end product where the full loan amount (minus the origination fee) will be 100% drawn at the time of origination. The initial amount funded at origination will be based on a fixed rate; however, this product contains an additional draw feature. As the borrower repays the balance on the line, the borrower may make additional draws during the draw period. If the borrower elects to make an additional draw, the interest rate for that draw will be set as of the date of the draw and will be based on an Index, which is the Prime Rate published in the Wall Street Journal for the calendar month preceding the date of the additional draw, plus a fixed margin. Accordingly, the fixed rate for any additional draw may be higher than the fixed rate for the initial draw.

- Approval may be granted in five minutes but is ultimately subject to verification of income and employment, as well as verification that your property is in at least average condition with a property condition report. Five business day funding timeline assumes closing the loan with our remote online notary, and where loan amounts are under $400,000 which would not require an appraisal. Funding timelines may be longer for loans secured by properties located in counties that do not permit recording of e-signatures or that otherwise require an in-person closing, or that require a waiting period prior to closing, or where loan amounts exceed $400,000.

- To check the rates and terms you qualify for, we will conduct a soft credit pull that will not affect your credit score. However, if you continue and submit an application, we will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

- A Figure HELOC is secured with your home as collateral, whereas personal loans and credit cards are not.

- Our loan amounts range from a minimum of $15,000 to a maximum of $750,000. For properties located in AK, the minimum loan amount is $25,001 and for properties located in TX, the minimum loan amount is $35,000. Your maximum loan amount may be lower than $750,000, and will ultimately depend on your home value, lien position, credit profile, verified income amount, and equity available at the time of application. We determine home value and resulting equity through independent data sources and automated valuation models or appraisal. Loan amounts above $400,000 are subject to appraisal.

- Available initial APRs range from 6.65% to 15.25%, which includes the payment of a higher origination fee in exchange for a reduced interest rate, which is not available to all applicants or in all states. The lowest APRs are only available to the most qualified applicants, depending on credit profile and the state where the property is located, and those who also select ten year loan terms; APRs will be higher for other applicants and those who select longer loan terms. Your actual rate will depend on many factors such as your credit, combined loan-to-value ratio, loan term, occupancy status, and whether you are eligible for and choose to pay a higher origination fee in exchange for a lower rate. Rates change frequently so your exact APR will depend on the date you apply. Additionally, for the variable rate HELOC, the APR is based on an interest rate index and the credit agreement margin, and an increase or decrease of the index value will cause a corresponding increase or decrease in the variable APR after account opening subject to a rate floor and rate cap, and your monthly payments may increase or decrease as the APR changes. APRs for home equity lines of credit do not include costs other than interest. You will be responsible for an origination fee of up to 4.99% of your initial draw, depending on the state in which your property is located and your credit profile. You may also be responsible for paying the costs of valuation if an AVM is not available for your property ($180), or an appraisal if your loan amount exceeds $400,000 ($500-$2,000, depending on property type, property value, and state), manual notarization if your county doesn’t permit eNotary ($350), and recording fees ($0 – $315) and recording taxes, which vary by state and county ($0-$1,400 per one hundred thousand dollars borrowed). Property insurance is required as a condition of the loan and flood insurance may be required if your property is located in a flood zone.

- You should consult a tax advisor regarding the deductibility of interest and charges to your Figure Home Equity Line.

- The Figure Variable Rate Home Equity Line is an open-end product where the full loan amount (minus the origination fee) will be 100% drawn at the time of origination. The initial amount funded at origination will be based on the selected rate at application and will be based on an Index, which is the Prime Rate published in the Wall Street Journal for the calendar month preceding the date of the initial draw, plus a stated margin; however, the rate and payment will adjust monthly based on the market and the fluctuation of the Index subject to a Rate Cap and Rate Floor. As the borrower repays the balance on the line, the borrower may make additional draws during the draw period. If the borrower elects to make an additional draw, the interest rate for that draw will be set as of the date of the draw and will be based on an Index, which is the Prime Rate published in the Wall Street Journal for the calendar month preceding the date of the additional draw, plus a fixed margin. The index can change at any time and the unpaid balance of all draws are subject to the monthly variable rate. Accordingly, variable rates are based on the market and may change after account opening. This product is not available in: MA, VA, MS, IL, WI, VT, DC, OK, TX, NY, CO, WY, WV, SC.

FourLeaf

Why we picked it

FourLeaf offers HELOCs with a low fixed introductory rate for creditworthy borrowers. This lender is an excellent option for homeowners needing lines of credit due to its lack of upfront fees and wide range of borrowing amounts. It provides the financial leverage required for home renovations or other major expenses.

FourLeaf’s commitment to customer service and flexible loan terms makes it an excellent choice for those looking to maximize their home equity. The straightforward application process and competitive rates further enhance its appeal, ensuring borrowers can access the necessary funds.

- Borrow $10,000 – $1 million

- No application, origination, or appraisal fees

- Convert some or all of your HELOC to a fixed-rate option

- 12-month fixed introductory rate for qualified borrowersⓘ

- $0 closing costs

Read our full FourLeaf HELOC review.

HELOC details

| Rates (APR) | 6.99% for 12 months, then variable starting at 6.75%ⓘ |

| Loan amounts | $10,000 – $1 million |

| Repayment terms | Up to 20 years |

| Funding time | 6 to 10 weeks on average |

| Properties | Primary homes, second homes, or condos |

| Credit score | 670 |

| Application | Apply online now |

LendingTree

Why we picked it

LendingTree is ideal for Delaware homeowners who want to compare multiple HELOC offers. LendingTree’s platform allows users to obtain quotes from various lenders, ensuring they find the best rate and terms for their needs. This service simplifies the shopping process, making it easier for Delaware residents to secure a competitive HELOC that fits their financial goals

- Access to multiple lenders

- Comprehensive comparison tools

- Competitive rates

- Customizable loan options

Loan details

| Rates (APR) | Starting at 6.24% |

| Loan amounts | $10,000 – $2 million |

| Draw period | 2 – 20 years |

| Repayment term | 5 – 30 years |

| Funding time | Varies |

| Properties | Varies |

| Credit score | Varies, 620 advisable |

Local HELOCs in Delaware

Face-to-face customer service is a comfort that online HELOCs simply can’t offer—but local lenders can. Local lenders are likely to have stronger community ties, too. For a homegrown HELOC with a human element, look no further than these Delaware credit unions:

| Company | Starting rates (APR) | Location |

| Del-One Federal Credit Union | 8.00% | Statewide |

| Community Powered Federal Credit Union | 8.50% | New Castle County |

| Dover Federal Credit Union | 8.00% | New Castle and Kent Counties |

| Tidemark Federal Credit Union | 8.50% | Sussex County |

When choosing a lender, your HELOC rate is one of the most important factors. However, if you scan these lenders’ starting APRs, you’ll notice they’re quite similar. When that happens, you may need to use additional criteria to make your selection, including:

- Whether you’re eligible for membership

- Whether you can prequalify

- How much you’ll pay in HELOC fees

- How long your draw period will last

- If your lender requires a minimum initial draw

Take note of any lenders that offer standout perks or benefits. For example, if Tidemark holds your first mortgage, you can finance up to 100% of your home equity. And with Dover Federal, you can convert your HELOC to a fixed-rate loan.

What’s the difference between online and local HELOCs in Delaware?

Online and local HELOCs share many commonalities, but one key distinction between them is that they rely more on technology, while local HELOCs rely more on relationships.

Because they don’t maintain brick-and-mortar locations, online lenders tend to invest more heavily in digital customer service options. By contrast, local lenders often provide a more traditional borrowing experience, complete with the option for in-person support.

Here’s a closer look at how each lending approach differs:

| Online | Local | |

| How to apply | Online | Online, in-person |

| Appraisal type | Standard or virtual | Standard |

| Account access | Website, app | Website, app, in-person |

| Contact methods | Chat, email, phone | Chat, email, phone, in-person |

| Bank accounts offered? | Sometimes | Usually |

Given their distinct advantages, you could make a case for either HELOC. Still, there are a few scenarios when one is a better choice than the other:

| If you… | Then consider… |

| Are partial to in-person customer service | Local HELOCs |

| Prefer self-service account management | Online HELOCs |

| Already bank with a lender near you | Local HELOCs |

| Can’t easily drive or walk to a physical branch | Online HELOCs |

| Aren’t comfortable using technology | Local HELOCs |

| Travel frequently or work during typical business hours | Online HELOCs |

No matter which HELOC type you’re leaning toward, it’s a good idea to consider lenders from both camps. At worst, you’ll spend a little extra time researching your options. At best, you’ll find a lender with lower rates and better benefits than you anticipated.

How do Delaware HELOC rates compare to other states?

Home prices may jump up or down from one zip code to the next, but HELOC rates don’t. In fact, HELOC rates have little to do with your location. You won’t always see significant changes in HELOC rates by state because rates depend far more on borrowers’ credit scores.

That said, average credit scores do vary somewhat across state lines. Differences in cost of living, economic development, and earning potential contribute to those fluctuations.

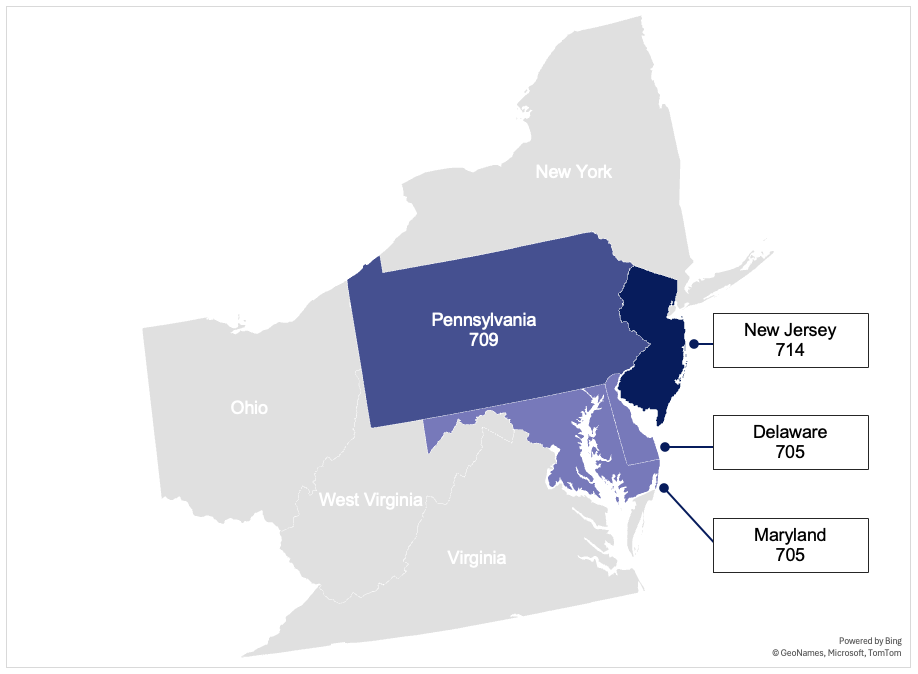

Still, you may not see much disparity in HELOC rates from one state to another. Take, for example, the average VantageScores for Delaware and surrounding states, as of May 2024:

None of these scores is considerably higher or lower than the others. It’s reasonable to assume that the typical HELOC rates in these states are also fairly similar.

How to get the best HELOC rates in Delaware

To get the best rate on your HELOC, do a pulse check on your credit before applying. Pull your credit reports and credit card statements to check for ways to boost your score. These are some of the most common ways to prepare your credit:

- Look for and correct any errors on your report.

- Reduce your credit card balances to 30% or less of your overall limit.

- Bring any past-due accounts current.

- Avoid applying for new credit before closing on your HELOC.

Taking charge of your credit is only the first step, though. What’s next? Prequalifying.

When you prequalify, lenders perform a soft credit check to give you personalized, preliminary rates. You can then use these rates to calculate your HELOC payments and measure your potential borrowing cost.

The national prime rate is generally considered the best possible rate. Compare your prequalified rates to the prime rate to gauge whether you’re getting a good deal or need to keep looking.

Because prequalifying doesn’t hurt your credit, we suggest checking your rates with four or five lenders minimum. That way, you’ll have plenty of options to choose from—and plenty of leverage.

Many lenders offer rate matching programs or other incentives if you can demonstrate that you’ve gotten a better rate elsewhere. Use that to your advantage so you can lock in the lowest possible rate with your preferred lender.

Are there any Delaware-specific requirements or regulations?

Title 5 of the Delaware Code outlines several requirements for mortgage lenders, mostly related to licensing and continuing education. However, Delaware state law doesn’t specifically address HELOCs.

Instead, any supplementary requirements you’ll need to meet will likely come directly from your lender.

Toward the end of the HELOC application process, your lender will send you a HELOC early disclosure form. This form details pertinent information including:

- When and why your APR may change

- What to expect when you enter repayment

- Your responsibilities and what may happen if you don’t meet them

These responsibilities may be as simple as repaying your HELOC as agreed and maintaining an adequate homeowners insurance policy for the duration of your HELOC.

Some lenders stipulate additional requirements, so read your disclosure form carefully and ask for clarification as needed.

FAQ

What credit score do you need for a Delaware HELOC?

Lenders typically require a minimum credit score of 620 for a HELOC. However, higher credit scores often secure better interest rates and terms. We recommend checking with individual lenders. Requirements can vary.

What are the typical fees for a Delaware HELOC?

Typical fees for a Delaware HELOC include application fees, appraisal fees, annual fees, and closing costs. These can range from 2% to 5% of the loan amount. It is important to review the fee structure with your lender to understand all associated costs.

Are there any special programs or incentives for Delaware HELOCs?

Delaware residents may benefit from special programs or incentives, such as introductory interest rates, no annual fees, or discounts for automatic payments.

Some lenders might also offer lower fees or better terms for members of certain credit unions or professional associations. Always inquire about any available programs when applying.

How we chose the best Delaware HELOCs

LendEDU evaluates HELOC lenders to help readers find the best HELOCs. Accessibility is important to this evaluation, so our editorial ratings system primarily focuses on companies available in most U.S. states. That’s why the lenders we selected in the online section have editorial ratings. They’ve gone through an extensive review process and were determined to offer superior products compared to other lenders. We’ve also independently verified that these companies are available in Delaware.

Since most local lenders aren’t available outside state lines, they haven’t gone through the same review process as the online lenders. Instead, we found them through separate research and determined that each offered solutions worthy of consideration by readers.

Recap of Delaware HELOC rates and lenders

| Company | Best for… | Rating (0-5) |

|---|---|---|

|

|

Best overall |

|

|

|

Best credit union |

|

|

|

Best marketplace |

|

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Gail Urban, CFP®

Reviewed by Gail Urban, CFP®Gail Urban, CFP®, AAMS®, has been a licensed financial advisor since 2009, specializing in helping individuals. Before personal financial advising, she worked as a business financial manager in several industries for about 25 years.