Repaying a home equity line of credit (HELOC) isn’t always straightforward—your payment and interest rate can vary, and in some cases, you may even need to pay off your full balance all at once.

Considering a HELOC to access your home equity? Understanding the fine print is essential. Wondering how to manage repayments or avoid surprises as you transition from the draw to repayment period? Here’s what you need to know.

Table of Contents

Can you pay off a HELOC early?

Yes, you can pay off a HELOC early in most cases, whether during the draw period or the repayment period. Paying off your HELOC ahead of schedule can save you money on interest and help free up your home equity for other purposes. However, early repayment may come with specific considerations and potential fees, depending on your lender’s terms.

How paying off a HELOC early works

- During the draw period: If your lender allows it, you can repay your HELOC balance in full during the draw period. This not only minimizes interest costs but also restores your available credit line, allowing you to borrow more if needed. However, some lenders may charge prepayment penalties or require you to reimburse closing costs if you close the account within a specific time frame (e.g., 24 or 36 months). Always review your HELOC agreement for details.

- During the repayment period: Once the draw period ends, you’ll start repaying principal and interest. Paying off the balance early during this phase can eliminate future interest costs, but since the credit line is no longer available, early repayment won’t allow for further borrowing.

Benefits of paying off a HELOC early

- Interest savings: The sooner you repay your balance, the less you’ll accrue in interest over time.

- Debt freedom: Paying off your HELOC early reduces your financial obligations and frees up equity in your home.

- Avoid balloon payments: For HELOCs with balloon payments at the end of the repayment period, early repayment can prevent a large lump-sum payment.

- Credit improvement: A lower HELOC balance can improve your debt-to-income ratio, which could boost your credit score.

When paying off early might not make sense

- Prepayment penalties: If your lender charges significant fees for early repayment, the cost might outweigh the interest savings.

- Other higher-interest debts: It may be more financially sound to tackle higher-interest debt first, such as credit card balances.

- Emergency fund concerns: If your HELOC acts as a financial safety net, closing it early could leave you without accessible funds in case of an emergency.

Many lenders allow early HELOC repayment during the draw period but may charge fees if you close your account early.

For instance, TD Bank charges a fee for closing the account within 24 months, Bank of America assesses similar penalties within 36 months, and FourLeaf Federal Credit Union, which pays closing costs for HELOC borrowers, will require you to repay if you close your account within 36 months.

🤔 How to decide

If your HELOC agreement includes prepayment penalties or fees, calculate whether the interest savings outweigh the cost of repaying early.

Say your HELOC balance is $40,000 with a 9.25% interest rate. Interest-only payments would amount to $308.33 per month. Compared to typical early account closure fees, it generally makes sense to pay off your balance.

As you can see in the table below, the breakeven point between interest payments and penalty fees ranges from just one to six months.

| Penalty type (within first 3 years) | Total fee | Interest breakeven point |

| $450 flat fee | $450 | 1.5 months |

| 1% of credit line amount | $400 | 1.3 months |

| Repay closing costs | $2,000 | 6.6 months |

Can you repay a HELOC during the draw period?

Yes, you can repay a HELOC during the draw period, which can reduce your interest costs and replenish your line of credit for future use.

How repaying during the draw period works

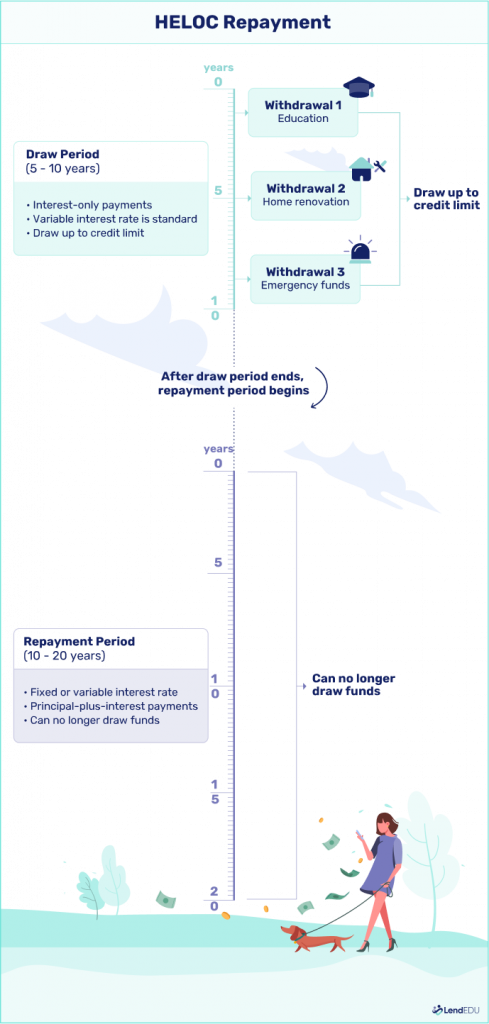

During the draw period—typically the first 10 years of your HELOC term—you might be required to make interest-only payments on the amount you borrow. However, most lenders allow you to pay back part or all of the principal during this time.

Making principal payments reduces your outstanding balance, which has two crucial benefits:

1. Interest reduction: As the principal balance decreases, the interest you owe also decreases.

2. Credit line replenishment: Repaying principal restores your available credit line, allowing you to borrow more later if needed.

- Interest reduction: As the principal balance decreases, the interest you owe also decreases.

- Credit line replenishment: Repaying principal restores your available credit line, allowing you to borrow more later if needed.

Example

- Imagine you have a $50,000 HELOC and borrow $25,000.

- Six months later, you earn a $5,000 bonus and pay it toward your HELOC balance.

- Your balance decreases to $20,000, and your available credit increases to $30,000.

Partial vs. full payments during the draw period

You can make partial principal payments during the draw period to lower your interest costs or repay your total balance if your lender allows it. While most lenders won’t penalize you for partial repayments, some may charge prepayment penalties or require you to cover initial closing costs if you repay the full balance and close the account early.

Check your HELOC agreement for any penalties or fees. If avoiding penalties is important, consider lenders that allow penalty-free early repayment.

What is the fastest way to pay back a HELOC?

The fastest way to repay a HELOC depends on your financial situation. Here are two primary strategies:

⚡ Lump-sum payment (fastest)

If you receive a financial windfall, such as a bonus, inheritance, or tax refund, putting that money toward your HELOC can significantly reduce your balance. This strategy minimizes accrued interest and frees up your line of credit for future use.

➕ Pay more than the minimum each month

During the draw period, most HELOCs require interest-only payments. Paying additional principal each month reduces your balance faster and decreases the interest that accrues over time. This strategy is especially effective if you have a predictable income and can budget for higher monthly payments.

Always check for prepayment penalties in your HELOC agreement. Some lenders may charge fees for paying off your balance early or closing your account within a specific time frame. If penalties apply, calculate whether the savings in interest outweigh these fees.

What is the best way to pay off a HELOC?

The best method for paying off a HELOC depends on your financial circumstances and goals. The following table highlights options that are ideal for different scenarios.

| If… | Pay off your HELOC by… |

| You can afford to pay it off all at once | Making a one-time payment |

| You can’t afford a lump-sum payment | Making extra principal payments |

| You want to switch to a fixed-rate loan | Using a cash-out refinance |

If you can afford to pay it off all at once

If you can afford to pay off what you owe, a lump-sum payment might be the best option for you. Just remember to check with the lender to see whether it charges a prepayment fee.

If you can’t afford a lump-sum payment

Making extra principal payments could be your best strategy if you can’t afford to pay your balance in full but want to pay down your loan faster. Doing so helps lower your total interest costs.

If you want to switch to a fixed-rate loan

Applying for a cash-out refinance might be your best option if you want to swap out your HELOC’s variable rate with a fixed one.

Transition from the draw period to the repayment period

The transition from the draw period to the repayment period is automatic. So once you’ve finished out month 120 (if you have a 10-year draw period), your HELOC will pivot into the repayment period, and you’ll start repaying your balance.

Your lender should send a HELOC reset or maturity notification as you get closer to the end of your draw period. If you haven’t received any communications, contact your lender. Missing a payment could result in late fees, extra interest costs, and damage to your credit.

If you’re struggling to make your payments, your lender might allow you to sign a HELOC modification agreement to change the terms.

Your lender can also freeze your HELOC in certain instances, and you can request that your lender freeze your line of credit. Once your draw period ends, you can explore other options, which we’ll cover later.

FAQ

What are the options for repayment after the draw period ends?

When your draw period ends, you can repay your HELOC in four ways. Consider each option below, and work with your lender to choose the best fit for your finances.

| Repayment option | When it makes sense |

| Accept the original repayment terms | If you can afford the principal and interest; If you don’t need to use your HELOC again |

| Convert to a fixed-rate loan | If you prefer consistent monthly payments; If you can meet credit requirements |

| Renew the HELOC | If you still need to draw from your HELOC |

| Make a lump-sum payment | If you can afford to pay a large amount at once |

Will fees affect my repayment amount?

HELOCs come with fees, both upfront and over time. The upfront ones—the application fee, for example—you’ll pay as part of your closing costs. Others may come up during the draw and repayment periods and could affect your monthly payments.

Here are a few HELOC fees you should look out for:

| Fee | Average cost |

| Origination fee | Up to $125 or a percentage of the loan |

| Annual fees | $25 – $75 |

| Inactivity fees | Up to $49 per month |

| Early termination or prepayment fees | $500 |

| Conversion fee | $75 |

This list of fees isn’t exhaustive, either. The exact fees you’ll owe will depend on your lender and loan terms, so make sure to read the fine print. You can find much of this information on your HELOC statement.

Can my lender close my HELOC if I pay it off during the draw period?

Lenders can close out a line of credit at any time for reasons laid out in the Truth in Lending Act. But even if you pay off your HELOC balance during the draw period, your lender is unlikely to close the account without your approval or a direct request.

A HELOC is, by design, an open-ended line of credit that you can pull from as needed at any point during the draw period. Whether you withdraw the entire amount in month one or never need to touch a penny is up to you.

However, outstanding HELOCs represent a potential risk to lenders, so a lender may opt to freeze or close certain lines of credit to protect itself. The lender may close the account without your approval if you aren’t using your HELOC and have a $0 balance. An account closure is more likely if your home value has significantly declined. In this scenario, the lender could either freeze or close the account, or lower your credit limit.

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Reviewed by Eric Kirste, CFP®

Reviewed by Eric Kirste, CFP®Eric Kirste, CFP®, CIMA®, AIF®, is a founding principal wealth manager for Savvy Wealth. Eric brings more than two decades of wealth management experience working with clients, families, and their businesses, and serving in different leadership capacities.