Home equity line of credit

- Generous credit line with up to $1 million available, making it ideal for significant expenses

- Rate discounts available for autopay, initial withdrawals, and Preferred Rewards members

- Flexible rate options allow conversion from a variable rate to a fixed rate without additional fees, offering predictability in payments

- No application, annual, or closing fees for credit lines up to $1 million

- No home equity loans, which limits options for those who prefer a lump-sum payout

- Requires in-person closings, which may be inconvenient for busy or remote applicants

- Potential in-home appraisal, which could be time-consuming and uncomfortable

- Lack of transparency in some processes, such as appraisal and eligibility requirements, making it harder to gather necessary information

| Rates (APR) | 7.49% variable introductory APR for 6 months; 9.90% variable APR after intro period |

| Loan amounts | $25,000 – $1 million online; lower amounts possible in person |

| Repayment terms | 10-year draw; 20-year repayment |

Bank of America’s (BoA) HELOC is well-suited for current BoA customers looking to leverage their home equity. It offers competitive rate discounts if you already bank with BoA and the flexibility to convert a variable rate to a fixed rate with no additional fees.

Given these features, if you’re already a BoA customer—or considering becoming one—this HELOC option should be on your radar. Here, we’ll help you decide whether Bank of America’s home equity product aligns with your financial goals.

Table of Contents

Note: If your credit score is below 720, it is unlikely that you will pass the prequalification stage for most HELOC lenders. If your score is higher than 580, see our highest-rated HELOCs for fair credit. Below 580, look into home equity agreements as an alternative.

About Bank of America

A longtime U.S. institution, Bank of America has established itself as a pillar in the American banking landscape. It aims to provide financial solutions that empower people to lead better lives, evident in its wide range of offerings—from personal banking and investment services to mortgage products.

For homeowners, Bank of America offers a robust HELOC so you can tap into your home’s value for various needs. Whether you’re considering home renovations, debt consolidation, or covering emergency expenses, its HELOC provides a flexible way to access funds.

Ideal customers for Bank of America should be confident a HELOC—not a home equity loan—is the right product for their needs. They might value a large, reputable institution with a variety of financial services and the convenience of in-person branches nationwide.

Bank of America HELOC at a glance

Let’s dive into the specifics of Bank of America’s home equity line of credit (HELOC). The table below offers a snapshot.

Keep reading, though: We’ll delve deeper into what each term means for you, how you can maximize rate discounts, and why the option to convert rates between fixed and variable is a unique advantage.

| Terms | Details |

| Rates (APR) | 7.49% variable introductory APR for 6 months; 9.90% variable APR after intro period |

| Loan amounts | $25,000 – $1 million online; lower amounts possible in person |

| Draw period | 10 years |

| Repayment period | 20 years |

| Repayment assistance | Depends on eligibility (See details below.) |

| Fees | None |

| Unique features | Convert variable rate to fixed rate with no fees |

Rate discounts include:

- Up to 1.5% on initial withdrawal (Get a 0.1% interest rate discount for every $10,000 in your first withdrawal up to 1.5%)

- 0.25% for autopay from a Bank of America checking or savings account

- 0.0625% for Preferred Rewards members

Eligibility for repayment assistance requires:

- A change in loan payment or income

- A home equity account open for at least nine months

- A minimum of six full payments made

- No other home equity modification in the past 12 months and no more than two modifications in the past five years

- All borrowers on the loan must agree to the terms

How does a Bank of America HELOC work?

When you get a Bank of America HELOC, you sign up for a variable interest rate loan with a low six-month introductory APR. After that, the rate climbs.

The draw period lasts for 10 years, giving you a decade to use your credit line. You then have 20 years to repay the amount you drew. You can get a credit line as low as $25,000 if you apply online and as high as $1 million.

You can manage your Bank of America HELOC online, but phone options are available. Online management offers the benefit of immediate updates and easy access to account features.

Home value doesn’t significantly affect the APR or other terms, but it affects how much you can borrow. However, home equity, not just home value, is a significant factor in determining your borrowing amount.

How to calculate your home equity

Calculating your home equity is a straightforward process. Here’s a simple formula you can use:

Home equity = Home value – Remaining mortgage balance

- Home value: This is the current market value of your home. You can get an approximate idea from online real estate websites or get a professional appraisal for an accurate figure. (Bank of America will set up an appraisal during the HELOC approval process.)

- Remaining mortgage balance: This is the amount you still owe on your home loan.

Let’s say your home is worth $300,000, and you still owe $120,000 on your mortgage.

Home equity = $300,000 (home value) – $120,000 (remaining mortgage balance)

Home equity = $180,000

So in this example, you would have $180,000 in home equity.

The value of your home can set the upper limit of your HELOC, but your equity determines how much of that value you can borrow against. For example, owning your $200,000 home outright could offer you a larger line of credit than someone who has a $1 million home but still owes $900,000 on their mortgage.

However, keep in mind that the APR and other loan terms are influenced by factors beyond your equity or home value, such as your credit score.

During the draw and repayment periods, you’ll pay interest and principal. If you set up auto-debit from a Bank of America account, you can earn rate discounts.

Who’s eligible for a Bank of America HELOC?

If you’re wondering whether you can tap into a Bank of America HELOC, the option is available to homeowners with primary or secondary residences in the U.S. Investment property owners may qualify but must contact Bank of America to find out.

| Requirement | Details |

| Eligible properties | Primary and secondary homes only for online application |

| Eligible states | All 50 states and Washington, D.C. |

| Maximum loan-to-value | 85% |

| Maximum debt-to-income | Not stated |

| Minimum credit score | Not stated |

| Minimum income | Not stated |

What is loan-to-value?

Loan-to-value (LTV) is a crucial term you’ll encounter when applying for a HELOC. It refers to the ratio between the amount you want to borrow and the appraised value of your home. The higher the LTV, the more you’re borrowing in relation to your home’s value.

LTV = (Loan amount / Appraised home value) x 100

For a HELOC with Bank of America, the maximum LTV is 85%. So you could borrow up to 85% of your home’s appraised value minus any current mortgage balances.

Combined loan-to-value (CLTV)

CLTV considers all loans secured by the property, not just the HELOC you’re applying for. Here’s how to calculate it:

CLTV = [(Sum of all loans secured by property) / Home value] x 100

Let’s assume:

- Your home appraises at $400,000.

- You still owe $200,000 on your mortgage.

Here are the steps to take:

- Calculate the maximum amount you could borrow with an 85% LTV:

$400,000 (appraised value) x 0.85 (max LTV) = $340,000

- Figure out your potential HELOC amount:

$340,000 (max amount at 85% LTV) – $200,000 (current mortgage) = $140,000

So in this example, you could be eligible for a HELOC up to $140,000, and your CLTV would be at the maximum limit of 85%.

Understanding LTV and CLTV helps you gauge how much you can borrow.

What are the costs and fees of a Bank of America HELOC?

Understanding the costs and fees of a Bank of America HELOC can help you make a smart borrowing decision. Rates are crucial.

Bank of America starts with a variable introductory APR for the first six months and then the rate adjusts.

Rates can vary based on your location and any discounts you may qualify for, such as autopay or initial withdrawal discounts.

Bank of America’s rates and lack of fees are competitive. Some lenders might offer lower introductory rates but compensate with origination or annual fees.

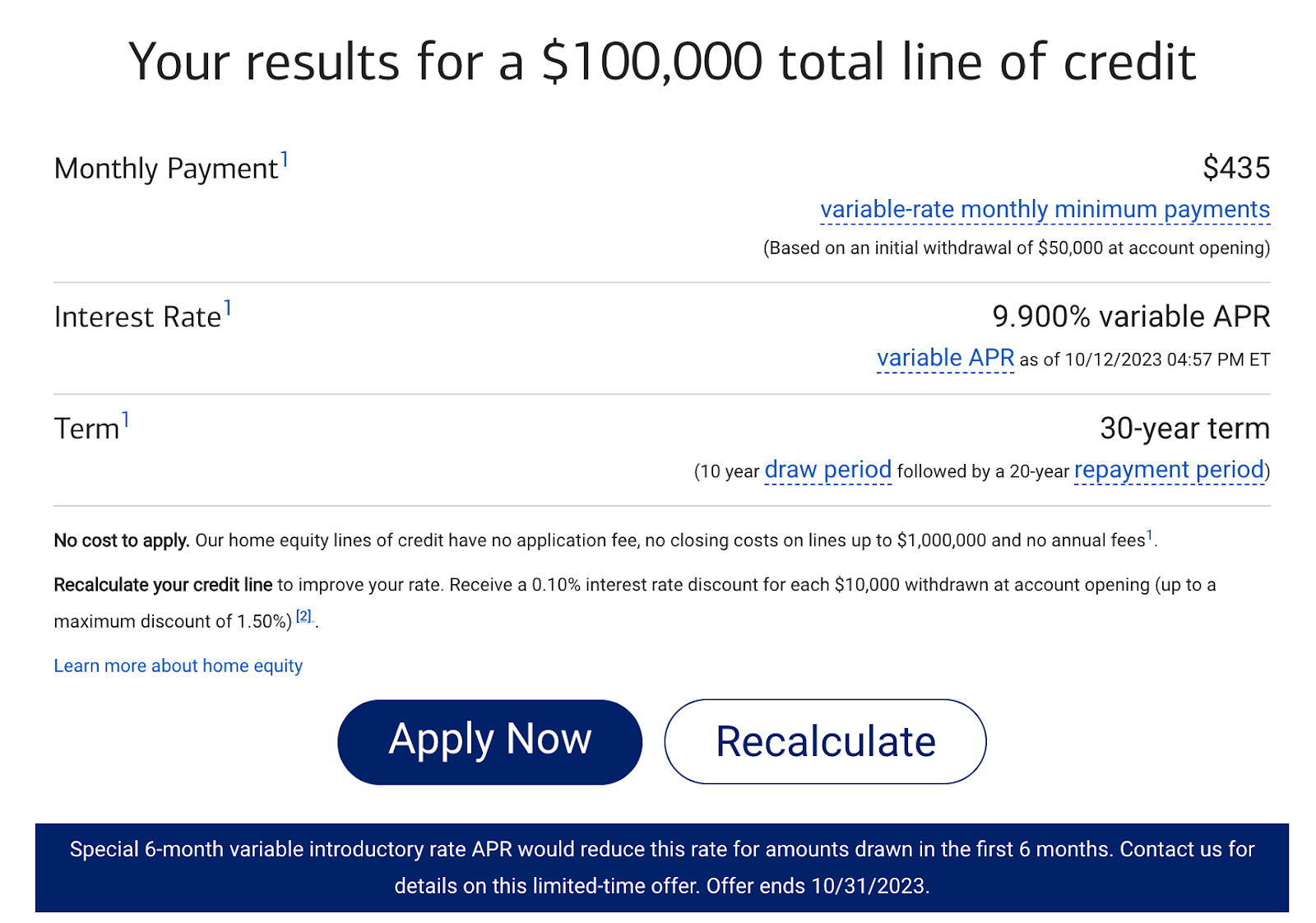

Your rate determines your interest cost, which is added to the principal amount you borrow. If you initially draw $50,000 at a 7.49% APR and switch to a 9.90% APR after six months, you’d see an increase in monthly payments.

Say you borrow $50,000 at the introductory rate of 7.49% for six months, and then the rate jumps to 9.90% and stays there for a year. Your interest cost for the first six months would be approximately $1,872.50.

After the rate jumps, your interest cost would be about $4,950 that year ($2,475 every six months).

How do you repay a HELOC from Bank of America?

Repaying a HELOC involves two main periods: the draw period and the repayment period. Understanding how they work can give you more control over your finances.

- Draw period: 10 years to borrow against your line of credit as needed. With Bank of America, you’ll pay principal and interest during this time.

- Repayment period: 20 years to pay back the principal and interest.

This differs from a home equity loan, where you get a lump sum upfront.

We used Bank of America’s home equity calculator to determine monthly payments on a $50,000 initial draw from a $100,000 HELOC:

Source: Bank of America

If you draw the full amount you’re approved for, you can’t borrow more until you’ve paid down your credit line.

Setting up autopay from a Bank of America account gets you a 0.25% rate discount, but it offers three ways to make payments:

- Online

- Via mobile app

- By phone

You can pay off your HELOC early without penalty. Doing so could save you a considerable amount in interest over the long term.

Since a BoA HELOC defaults to a variable rate, keep an eye on market trends if you’re considering one. It could influence your decision to switch to a fixed-rate option.

How does the fixed-rate option work?

Bank of America offers a noteworthy feature on its HELOC: the fixed-rate loan option. You’re not just stuck with a variable rate; you can switch.

Here’s how it works:

- At account opening: You can convert a minimum of $5,000 to a fixed rate. The most you can convert is 90% of your maximum credit line (e.g., $90,000 on a $100,000 line). The loan term can range from one year to the account maturity date (10 years after you open the account).

- During loan term: Already have a variable-rate balance? You can convert all or part of it to a fixed rate. The minimum amount for this conversion is $5,000. Just like at the opening, the loan term is at least one year and can’t exceed the account maturity date.

What you need to know:

- Number of fixed-rate loans: You can have up to three fixed-rate loan options open at once.

- Fees: No fees for this conversion.

- Rates: Rates for the fixed-rate loan option may be higher than the variable rates on your HELOC.

- Payments: Monthly payments on a fixed-rate loan option cover principal plus interest.

- Funds replenishment: As you pay down the fixed-rate balance, those funds become available again at the variable rate.

This feature gives you flexibility and predictability in your repayment strategy. If you like knowing exactly what your payments will be, this might be the option for you.

How does your home’s value affect your terms?

As we mentioned above, the value of your home plays a crucial role in your HELOC eligibility and terms. Because your home secures the line of credit, the lender uses its value—along with your home equity—to determine how much you can borrow.

Your home’s value doesn’t directly affect the APR, but it influences your borrowing amount. If your home’s value fluctuates significantly while you have a HELOC, that could adjust your loan-to-value ratio and even cause a lender to change your credit limit.

What does Bank of America’s appraisal process look like?

Bank of America, like many home equity lenders, requires an appraisal. However, the bank’s website doesn’t specify whether this must be an in-person evaluation.

Typically, you’ll need to provide property details and might need to allow access for a home evaluation. Compared to other lenders, Bank of America’s process seems less transparent.

Many lenders offer online tools for a quick home value estimate and provide clearer timelines and methods for the official appraisal.

Pros and cons of Bank of America

Understanding the pros and cons of a financial product before you make a decision is crucial. Here’s what to consider about BoA:

Pros

-

Generous line of credit

If you qualify, you could get a credit line up to $1 million.

-

Variable APR discounts

Autopay, initial withdrawals, and Preferred Rewards membership can cut down your rate.

-

Fixed-rate option

Bank of America lets you switch from a variable to a fixed rate without additional fees.

-

Minimal fees

No application fee, no annual fee, and no closing costs on lines of credit up to $1 million.

Cons

-

No home equity loans

If you’re looking for a straightforward loan, consider another lender.

-

Inconvenient closings

In-person requirements can be a hassle for busy or remote individuals.

-

Possible in-home appraisal

This could be time-consuming and perhaps uncomfortable for some.

-

Lack of transparency

Our team had difficulty gathering information about the appraisal process and several eligibility requirements on BoA’s website.

Bank of America offers flexible APR discounts and a convenient fixed-rate option. The absence of various fees sweetens the deal, but it falters with its lack of home equity loans and potentially inconvenient in-person requirements.

Is Bank of America a reputable lender?

Customer reviews can provide valuable insights when shopping for home equity products. They offer a glimpse into the borrowing experience, helping you gauge the lender’s reliability, customer service, and ease of application.

Here’s how Bank of America fares in customer reviews.

| Source | Customer rating | Number of reviews |

| Trustpilot | 1.3/5 | 1,815 |

| Better Business Bureau | 1.06/5 | 899 |

Trustpilot and the Better Business Bureau are credible platforms for consumer reviews. Trustpilot provides a broad range of customer experiences, and the BBB, in addition to reviews, gives accreditation and ratings based on various factors, including customer complaints.

Bank of America’s ratings from Trustpilot and the Better Business Bureau are poor. Several reviews noted a burdensome application process for the HELOC. These ratings give us a snapshot, but they cover all Bank of America services, not just HELOCs.

Bank of America has an A-minus rating from the BBB, which indicates it generally meets standards for business practices, despite the low customer review scores. For a well-rounded view, we like to consider ratings from multiple sources and read reviews to understand the nuances.

Does Bank of America have a customer service team?

Bank of America maintains a robust customer service team to assist with your HELOC needs, among other services. The team is accessible in several ways, ensuring that you can reach out for help at your convenience.

Whether you have questions about your application, need assistance with managing your account, or want to understand the intricacies of your HELOC, you can get answers.

Ways to contact Bank of America:

- Phone: 1-866-290-4674 (Monday to Friday, 8 a.m. – 10 p.m. Eastern; Saturday, 8:30 a.m. – 6:30 p.m.)

- In person: Visit any Bank of America branch

- Appointment: Schedule to meet with someone at a location or speak over the phone

With these options, you’ll find it easy to get the help you need when navigating your HELOC with Bank of America.

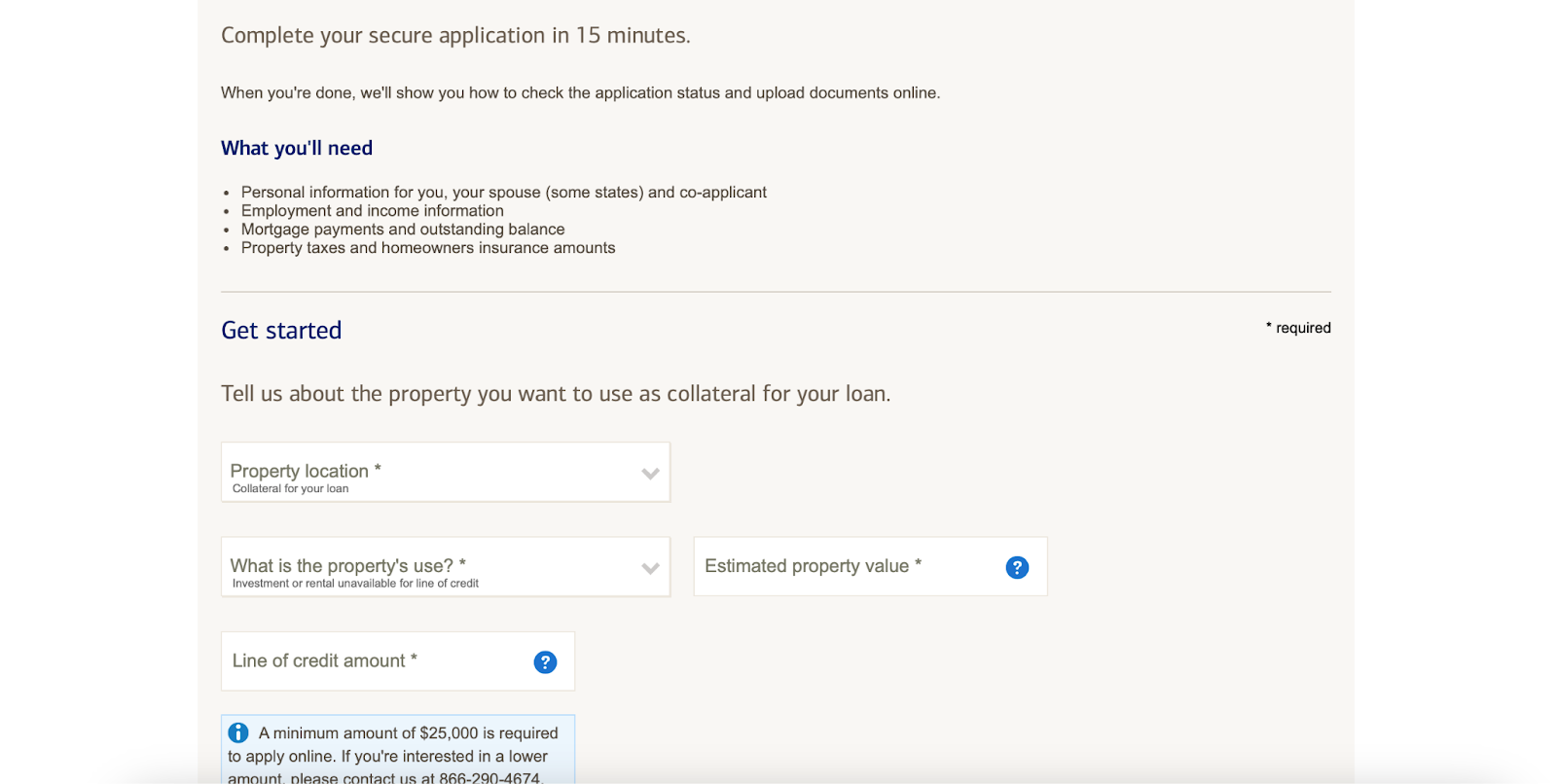

How to apply for a Bank of America HELOC

When it comes to applying for a HELOC with Bank of America, the process feels traditional compared to fintech companies that have streamlined online platforms.

The application is thorough, requiring various forms of documentation. One downside is the potential hit to your credit score; Bank of America doesn’t offer a prequalification option to assess your rates without a hard credit check.

Here’s how to apply for a Bank of America HELOC:

Source: Bank of America

- Start online: Navigate to the “Get Started” link on Bank of America’s website, and fill in personal details for you and your spouse or co-applicant, as well as employment, insurance, mortgage, and property information.

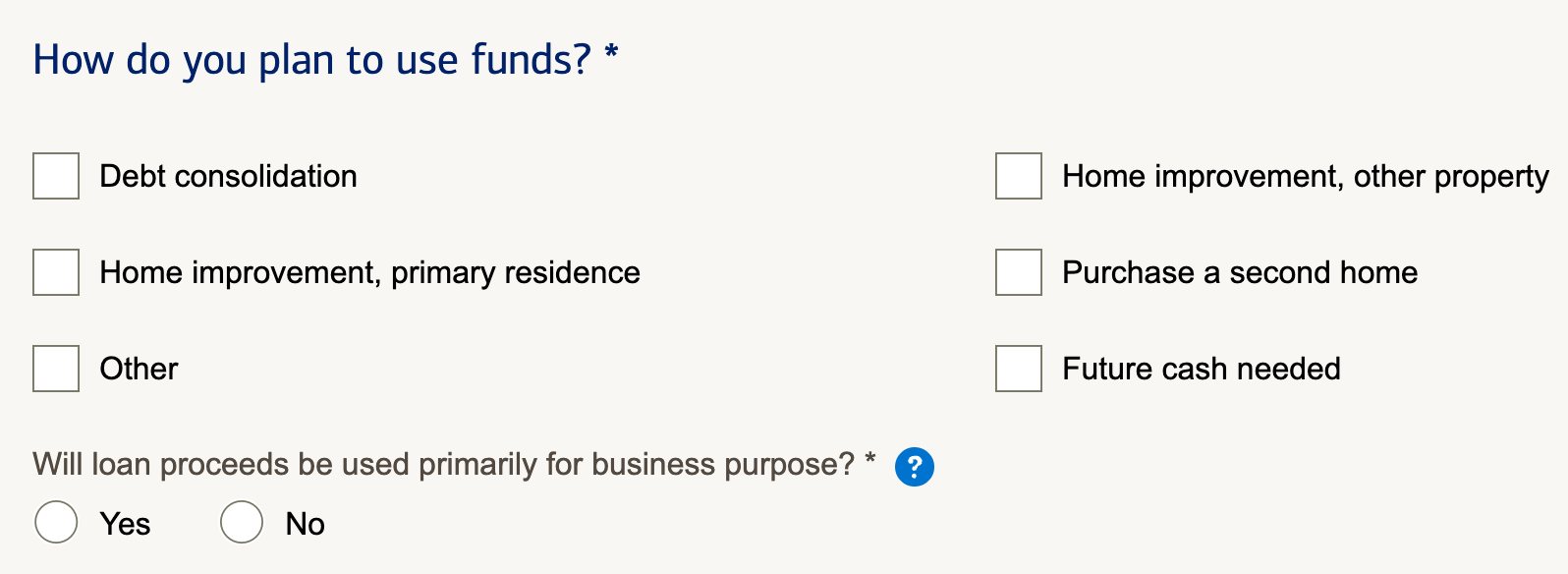

- Choose purpose and amount: Indicate what you’ll use the loan for and the amount you wish to borrow.

Source: Bank of America

- Consult a specialist: Work with a Bank of America representative to complete your application.

- Closing: If approved, you’ll need to close on the line of credit in person at a Bank of America center.

In all, expect to invest a fair amount of time to gather the required documents and go through each step.

What if I’m denied a HELOC from Bank of America?

Bank of America should provide a reason for a HELOC denial, in compliance with federal laws. You have the right to know why your application was not approved, and you can also reapply.

However, you might want to wait until you’ve improved the circumstances that led to the denial.

Common reasons for denial and next steps:

- Low credit score: If credit was the issue, work on improving your credit before you reapply, and get a copy of your credit report from each of the three credit bureaus to ensure no errors appear. (If you notice errors, dispute them right away.)

- High debt-to-income ratio: Look into ways to increase your income or reduce your debt.

- Insufficient home equity: If your home’s value isn’t high enough to support a HELOC, you may want to explore other types of loans or lines of credit, such as personal loans.

- Incomplete application or documentation: Ensure all the information you submitted was correct and that BoA received all required documents.

By addressing these issues, you improve your chances for approval—not just at Bank of America, but at most other lenders.

How do other home equity products compare to Bank of America?

A Bank of America HELOC offers flexibility that other home equity products may not provide. While similar in that they all use your home as collateral, they each serve unique financial needs and come with their own set of terms and features.

We’ve laid out the general differences below:

| Product | Rate | Flexible | Best for |

| Bank of America HELOC | Variable; can convert to fixed rate | ✅ | Multiple costs over time |

| Home equity loan | Often fixed | ❌ (get a lump sum) | One-time large expense |

| Reverse mortgage | Variable or fixed | ✅ (choose line of credit, monthly payout, or lump sum) | Ages 62+ w/out mort. debt |

| Cash-out refi | Fixed or variable | ❌ | Reduce mort. rate & take out cash |

A home equity loan gives you a lump sum upfront but lacks the draw period flexibility a HELOC offers.

Reverse mortgages are more tailored to older homeowners who want to tap into their home’s equity without selling.

Cash-out refinances offer the chance to take out a lump sum and potentially get a better mortgage rate, but they reset your mortgage term.

Consider your needs to pick the best option for you.

Bank of America HELOC FAQ

How long does it take to receive funds from Bank of America?

After you submit your application with Bank of America, approval can take anywhere from a couple of weeks up to 45 days.

This time frame includes the appraisal process and any other verifications that might be needed. Once you’re approved, you can expect to access your funds within a few days.

Do you need to tell Bank of America what the funds are used for?

For Bank of America, you’ll select what you want to use the HELOC funds for during the application process, but your intended use generally won’t influence your eligibility.

Does Bank of America have insurance requirements?

Yes, Bank of America does require you to have homeowner’s insurance, and in some cases, you may also need flood insurance. Be sure to check its specific policy requirements during your application process.

Can you back out of a HELOC contract?

You can withdraw your application at any stage before you close on the HELOC with Bank of America. If you’re approved but haven’t received the funds, you can still back out, often without a financial penalty.

After receiving the funds, the process for exiting the contract gets more complicated and might involve fees.

Can you close your HELOC account at any time?

With Bank of America, you can generally close your HELOC account, but be aware of any early termination fees outlined in your contract. Always read the fine print, and consult your agreement for any penalties that might apply.

About our contributors

-

Written by Kristen Barrett, MAT

Written by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.