If you’re considering tapping into your home equity to consolidate debt or fund a renovation project, a home equity line of credit (HELOC) is a common option.

A home equity line of credit (HELOC) is a revolving credit line secured by your home. In this article, we’ll tell you everything you need to know about HELOCs. By the time you’re finished reading, you’ll know what it is, how to qualify for one, its pros and cons, and whether or not it’s right for you.

Table of Contents

What is a home equity line of credit (HELOC)?

A HELOC is an incredibly popular lending product, with the total balance in the U.S. now at $422 billion as of Q3 2025. A home equity line of credit works similarly to a credit card: it is a revolving line of credit you can tap into when you need it, up to a certain limit. The difference is that a HELOC is a secured loan that uses your house as collateral.

In one sense, HELOCs are preferable to credit cards because HELOC interest rates are typically much lower. On the other hand, because your house is the collateral for a HELOC, there is more risk involved for the borrower because your lender can foreclose on your house if you’re not able to make your payments.

How it works

When you get a HELOC, you have it for a set period, divided into a draw period and a repayment period. During the draw period, you can access funds as needed, up to your approved credit limit, and you typically make interest-only payments on what you borrow.

HELOCs usually have variable rates, though they vary by lender. Some of our most-recommended HELOC lenders offer fixed rates, allowing you to lock in a rate for each draw. This can help keep payments manageable.

The draw period generally lasts two to 20 years, and the repayment period lasts five to 30 years.

At the end of the draw period, you can no longer use your line of credit, and you start making payments toward your full balance, including principal and interest. That’s another way that HELOCs differ from credit cards. Credit cards don’t have a set start and an end date, whereas HELOCs do.

How much can you borrow?

How much money you can borrow with a home equity line of credit depends on the value of your home, the percentage of your home that you own, your loan-to-value ratio, and your creditworthiness. Generally, it’s a good idea to only borrow what you can afford to pay back, both during the draw period and the repayment period.

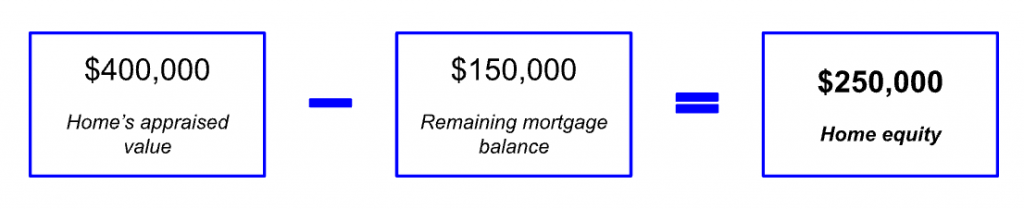

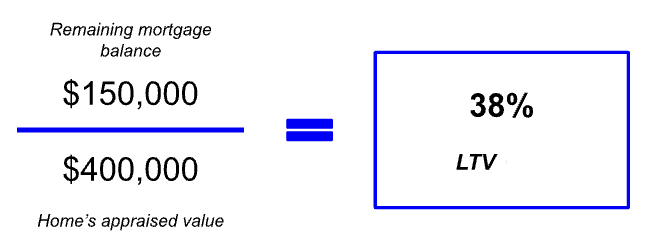

Home equity is the difference between your home’s value and your mortgage balance. LTV is a risk assessment measure that quickly tells lenders how much you owe on your mortgage relative to what your home is worth.

When you apply for a HELOC, lenders use your home equity and your loan-to-value ratio (LTV) to determine your credit limit.

Say you own a $400,000 home and owe $150,000 on your mortgage. Your home equity would be $250,000.

To calculate your LTV, we’d use these same numbers and divide your mortgage balance by your home’s value, giving us a 38% LTV.

Lower LTVs generally indicate lower debt, higher home values, or both. Many lenders won’t give you a HELOC that puts you above an 85% LTV. If you’re already near or above that threshold, what you can borrow with a HELOC may be limited.

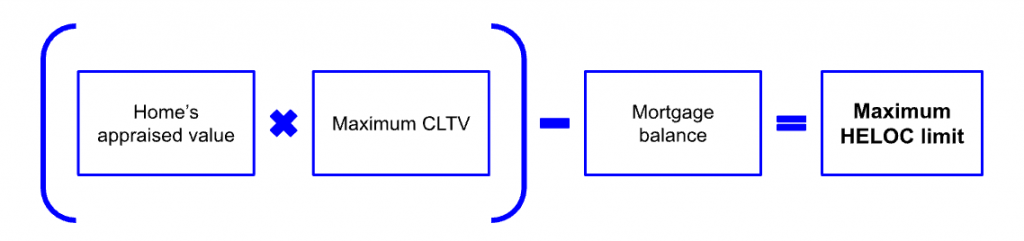

If you’re below 85%, lenders will see how large a HELOC you can get without maxing out your equity. They’ll do this by calculating your combined loan-to-value ratio (CLTV).

Where your regular LTV just compares your mortgage to your home’s value, CLTV weighs your HELOC, too. This formula shows how lenders use your CLTV to find out once and for all what you can borrow:

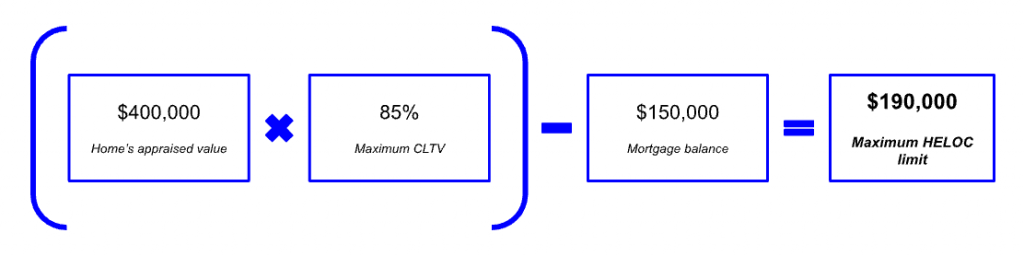

If we use the same numbers as before, the most you could borrow using a HELOC would be $190,000.

Some companies allow you to draw as needed, while others require you to withdraw the full balance upfront. It’s important to ask potential lenders what their requirements are and how you’ll receive the balance. This is especially important if you prefer a lump-sum payment or would rather use it like a typical line of credit.

How is a HELOC different from a home equity loan?

A HELOC is different from a home equity loan in a few ways. A home equity loan has a fixed interest rate, whereas HELOCs usually have a variable interest rate (though some lenders, like Aven, also offer fixed rates). Both products require you to have a specific amount of home equity, good credit, and a solid work history to qualify.

With a home equity loan, you get one lump-sum payment, whereas with a HELOC, you typically draw down on your credit as needed. Check your lender requirements, though, as some will require you to withdraw the total amount of credit upfront.

With a home equity loan, you’ll have equal monthly payments, which can make budgeting and planning easier. With a home equity line of credit, you’ll have a draw period where you make interest-only payments, and a repayment period where you’ll pay down the principal and outstanding interest. That means some payments might be higher and some might be lower.

How to qualify

If you want to research lenders and learn how to get a HELOC, first make sure that you meet the eligibility requirements. HELOCs tend to have stricter requirements than other types of loans, but the benefit is that the interest rates are lower than those of personal loans and credit cards.

Here are a few key prerequisites you should have before a lender will approve you for a HELOC:

- Excellent credit: Lenders like to see a 720 credit score or above for HELOCs, though some will accept 680 or above.

- Low debt-to-income ratio: Lenders prefer 43% or less, but the lower the better.

- Adequate home equity: Make sure you have 15% to 20% equity in your home before applying.

- Good loan-to-value ratio: This is your total loan balance divided by the current value of your home. Usually, lenders prefer an LTV of 80% or less, though some accept higher LTVs.

- Proof of income: Lenders will ask for pay stubs, tax returns, and bank statements to confirm you’ve had steady income for at least two years.

And, although it’s not a specific lender requirement, it’s also a good idea to ensure you have a solid emergency fund before applying for a HELOC. That way, you always have extra money to make your HELOC payments in case you experience financial hardships.

The clients who tend to be the best fit for a HELOC are those with great to excellent credit, dependable income, substantial equity built up in their home, and have a repayment plan established.

Learn more about getting a HELOC in this video.

How do you use a HELOC?

You can use your HELOC to pay for just about anything, but some uses are more financially prudent than others. Your lender might ask why you’re taking out a HELOC, but most don’t have restrictions on how you can use the funds. Even if you say you’re going to use it for a specific purpose, you are allowed to change your mind later.

Here are examples of ways you can use a HELOC:

- Consolidating high-interest debt

- Renovating a home

- Paying for assisted living or medical care

- Buying a new car

- Starting a business

- Buying a vacation property

- Paying for costly home repairs

- Paying for a child’s college education

- Repaying medical bills

- Funding a wedding

- Paying off your mortgage

- Paying off student loans

Make sure to research alternative ways to pay for these expenses first. For example, if you have medical bills, ask your doctor’s office or hospital for a payment plan before using your home as collateral to make the payment. Similarly, if you can fund a wedding or pay for home repairs by saving over time, that can help you avoid extra debt.

Also, note that using a HELOC for some uses should only be done when it really makes sense. For example, a HELOC should be used to pay off your mortgage only if the HELOC has a lower fixed interest rate, you need to extend the terms to allow lower monthly payments, or you’re paying off the mortgage of a rental property.

Most importantly, keep in mind that if you pay off federal student loans using a HELOC, you’ll lose access to federal relief programs, flexible repayment plans, and loan forgiveness (if you qualify). These are a few reasons why it’s important to do your research and consider the pros and cons of HELOCs if you need funding for a specific purpose.

There are several reasons I recommend a HELOC to certain clients. A common scenario is when a client wants an added layer of liquidity beyond their emergency fund, allowing them to avoid selling investments during unfavorable market conditions. In other cases, a HELOC can serve as a short-term backstop while they are in the process of building their emergency reserves. As with any borrowing strategy, it should be used intentionally and paired with a repayment plan that fits comfortably within their cash flow.

Where to get a home equity line of credit

Here are a few top-recommended HELOC lenders according to our research.

Article sources

At LendEDU, our writers and editors rely on primary sources, such as government data and websites, industry reports and whitepapers, and interviews with experts and company representatives. We also reference reputable company websites and research from established publishers. This approach allows us to produce content that is accurate, unbiased, and supported by reliable evidence. Read more about our editorial standards.

- New York Fed, Center for Microeconomic Data, Household Debt and Credit Report Q3 2025

Related articles

About our contributors

-

Written by Catherine Collins

Written by Catherine CollinsCatherine Collins is a personal finance writer and author with more than 10 years of experience writing for top personal finance publications. As a mother to boy/girl twins, she is passionate about helping women and children learn about money and entrepreneurship. Cat is also the co-host of the Five Year You podcast.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.