If you’re shopping for HELOC rates in New Jersey, you might consider looking for a lender online. Comparing HELOC rates online is a convenient way to find the best loan option for your needs. It also helps to know a little about how HELOC rates in New Jersey are set.

Reviews of the best HELOC lenders in New Jersey

Searching for the best HELOC lenders in New Jersey can be time-consuming, so we’ve put together a list of top lenders for you. Here’s how they compare at a glance, with a deeper dive into each loan offering below.

Figure: Best HELOC overall

Why we picked it

Figure is our top pick for a HELOC due to its blend of competitive fixed rates, quick funding, and flexible terms.

Advanced technologies such as blockchain and AI ensure a fast and efficient approval process, with funds available in as few as five days. This makes Figure ideal for borrowers seeking quick and reliable access to home equity without the traditional banking hassle.

- Fixed interest rates

- No in-person appraisal is needed

- Option to redraw up to 100% of funds

- Funding can be available in as few as 5 days

- Check your rate without affecting your credit score

Loan details

| Rates (APR) | 6.55% – 15.54% |

| Loan amounts | $20,000 – $750,000 |

| Draw period | 2 – 5 years |

| Repayment term | 10, 15, 20 or 30 years |

| Funding time | As few as 5 days |

| Properties | Primary home, second home, or investment property |

| Minimum credit score | 640 |

Figure Disclosures

- The Figure Fixed Rate Home Equity Line is an open-end product where the full loan amount (minus the origination fee) will be 100% drawn at the time of origination. The initial amount funded at origination will be based on a fixed rate; however, this product contains an additional draw feature. As the borrower repays the balance on the line, the borrower may make additional draws during the draw period. If the borrower elects to make an additional draw, the interest rate for that draw will be set as of the date of the draw and will be based on an Index, which is the Prime Rate published in the Wall Street Journal for the calendar month preceding the date of the additional draw, plus a fixed margin. Accordingly, the fixed rate for any additional draw may be higher than the fixed rate for the initial draw.

- Approval may be granted in five minutes but is ultimately subject to verification of income and employment, as well as verification that your property is in at least average condition with a property condition report. Five business day funding timeline assumes closing the loan with our remote online notary, and where loan amounts are under $400,000 which would not require an appraisal. Funding timelines may be longer for loans secured by properties located in counties that do not permit recording of e-signatures or that otherwise require an in-person closing, or that require a waiting period prior to closing, or where loan amounts exceed $400,000.

- To check the rates and terms you qualify for, we will conduct a soft credit pull that will not affect your credit score. However, if you continue and submit an application, we will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

- A Figure HELOC is secured with your home as collateral, whereas personal loans and credit cards are not.

- Our loan amounts range from a minimum of $15,000 to a maximum of $750,000. For properties located in AK, the minimum loan amount is $25,001 and for properties located in TX, the minimum loan amount is $35,000. Your maximum loan amount may be lower than $750,000, and will ultimately depend on your home value, lien position, credit profile, verified income amount, and equity available at the time of application. We determine home value and resulting equity through independent data sources and automated valuation models or appraisal. Loan amounts above $400,000 are subject to appraisal.

- Available initial APRs range from 6.65% to 15.25%, which includes the payment of a higher origination fee in exchange for a reduced interest rate, which is not available to all applicants or in all states. The lowest APRs are only available to the most qualified applicants, depending on credit profile and the state where the property is located, and those who also select ten year loan terms; APRs will be higher for other applicants and those who select longer loan terms. Your actual rate will depend on many factors such as your credit, combined loan-to-value ratio, loan term, occupancy status, and whether you are eligible for and choose to pay a higher origination fee in exchange for a lower rate. Rates change frequently so your exact APR will depend on the date you apply. Additionally, for the variable rate HELOC, the APR is based on an interest rate index and the credit agreement margin, and an increase or decrease of the index value will cause a corresponding increase or decrease in the variable APR after account opening subject to a rate floor and rate cap, and your monthly payments may increase or decrease as the APR changes. APRs for home equity lines of credit do not include costs other than interest. You will be responsible for an origination fee of up to 4.99% of your initial draw, depending on the state in which your property is located and your credit profile. You may also be responsible for paying the costs of valuation if an AVM is not available for your property ($180), or an appraisal if your loan amount exceeds $400,000 ($500-$2,000, depending on property type, property value, and state), manual notarization if your county doesn’t permit eNotary ($350), and recording fees ($0 – $315) and recording taxes, which vary by state and county ($0-$1,400 per one hundred thousand dollars borrowed). Property insurance is required as a condition of the loan and flood insurance may be required if your property is located in a flood zone.

- You should consult a tax advisor regarding the deductibility of interest and charges to your Figure Home Equity Line.

- The Figure Variable Rate Home Equity Line is an open-end product where the full loan amount (minus the origination fee) will be 100% drawn at the time of origination. The initial amount funded at origination will be based on the selected rate at application and will be based on an Index, which is the Prime Rate published in the Wall Street Journal for the calendar month preceding the date of the initial draw, plus a stated margin; however, the rate and payment will adjust monthly based on the market and the fluctuation of the Index subject to a Rate Cap and Rate Floor. As the borrower repays the balance on the line, the borrower may make additional draws during the draw period. If the borrower elects to make an additional draw, the interest rate for that draw will be set as of the date of the draw and will be based on an Index, which is the Prime Rate published in the Wall Street Journal for the calendar month preceding the date of the additional draw, plus a fixed margin. The index can change at any time and the unpaid balance of all draws are subject to the monthly variable rate. Accordingly, variable rates are based on the market and may change after account opening. This product is not available in: MA, VA, MS, IL, WI, VT, DC, OK, TX, NY, CO, WY, WV, SC.

Aven: Best for customer reviews

Why we picked it

Customers praise Aven’s HELOC for its easy-to-understand terms and excellent customer service. It’s ideal for homeowners who want a transparent borrowing experience with ongoing support. Aven’s focus on customer satisfaction is reflected in its positive reviews, making it a strong option for anyone looking to tap home equity without hassle.

- Lowest rate guarantee

- Optional foreclosure protection program

- Approval in as little as 15 minutes

- Excellent Trustpilot reviews from thousands of customers

- 100% digital application process

- Increases credit line for select customers

- Automated appraisals

- High maximum loan-to-value ratio (LTV)

- Fast funding after signing

- Fixed interest rates from start to finish

- Check your rate with no credit impact

- Short draw period

- First-draw fee of 4.90%

- Only available in 32 states*

HELOC details

| Rates (APR) | 6.99% – 15.49% |

| Loan amounts | $5,000 – $400,000 ($100,000) |

| Draw period | 5 years |

| Repayment terms | 5, 10, 15, or 30 years |

| Funding time | As little as 3 days after signing |

| Properties | All types |

| Credit score | 640 |

FourLeaf FCU: Best credit union

Why we picked it

FourLeaf offers HELOCs with a low fixed introductory rate for creditworthy borrowers. This lender is an excellent option for homeowners needing lines of credit due to its lack of upfront fees and wide range of borrowing amounts. It provides the financial leverage required for home renovations or other major expenses.

FourLeaf’s commitment to customer service and flexible loan terms makes it an excellent choice for those looking to maximize their home equity. The straightforward application process and competitive rates further enhance its appeal, ensuring borrowers can access the necessary funds.

- Borrow $10,000 – $1 million

- No application, origination, or appraisal fees

- 12-month fixed introductory rate for qualified borrowersⓘ

- $0 closing costs

Read our full FourLeaf HELOC review.

HELOC details

| Rates (APR) | 6.99% for 12 months, then variable starting at 6.75%ⓘ |

| Loan amounts | $10,000 – $1 million |

| Repayment terms | Up to 20 years |

| Funding time | Varies |

| Properties | Primary homes, second homes, or condos |

| Credit score | 670 |

| Application | Apply online now |

About HELOC rates in New Jersey

HELOC rates are influenced by two things:

- Your creditworthiness

- The current interest rate environment

In New Jersey, lenders can use a benchmark such as the Prime rate to set HELOC rates. The Prime rate represents the lowest rate banks charge their most creditworthy customers.

As of February 2024, typical New Jersey HELOC rates range from 7% to 10%, though some lenders charge higher rates. For perspective, at the time of writing, the average rate for a 30-year purchase mortgage was 6.94%. HELOC rates in New Jersey and other states are higher than traditional mortgage rates because they present a greater risk to lenders.

HELOCs are a floating rate type of line of credit. They will move up and down with the Prime rate, which follows the federal funds rate. HELOCs present more risk to the lender, not the borrower, hence the higher rate. If an individual were to become delinquent on their mortgage or HELOC, the mortgage lender is the first to get paid, as the HELOC is in the second lien position. Therefore, to cover the additional risk, banks offer HELOCs at higher rates than they do conventional mortgages.

Kyle Ryan, CFP®

State usury laws impose caps on how much interest lenders can charge, but exceptions exist for loans over $50,000. Financial institutions, including mortgage lenders, can set rates up to the criminal usury cap of 30%, but it’s unlikely anyone would agree to a HELOC at that rate.

Costs of a HELOC in New Jersey vs. other states

Factors specific to New Jersey can influence the costs of a HELOC, including regulations, property values, and other economic factors.

State regulations and fees

New Jersey has unique state-specific regulations that limit HELOC fees, including:

- No financing credit insurance

- No encouraging default

- Late payment fees can’t exceed 5% of the amount due

- No acceleration of indebtedness

- No charging for payoff information

Consider all fees—origination and administrative hit the hardest. Next, look for the APR and where it is in relation to the Prime rate. Compare fixed vs. variable rates while remaining aware of potential interest rate movements in the future. The lender you choose should depend on your purpose for borrowing and how fast you will pay off the HELOC. You will also want a lender with a good service department you can reach out to if you ever have questions.

Kyle Ryan, CFP®

Property values and market trends

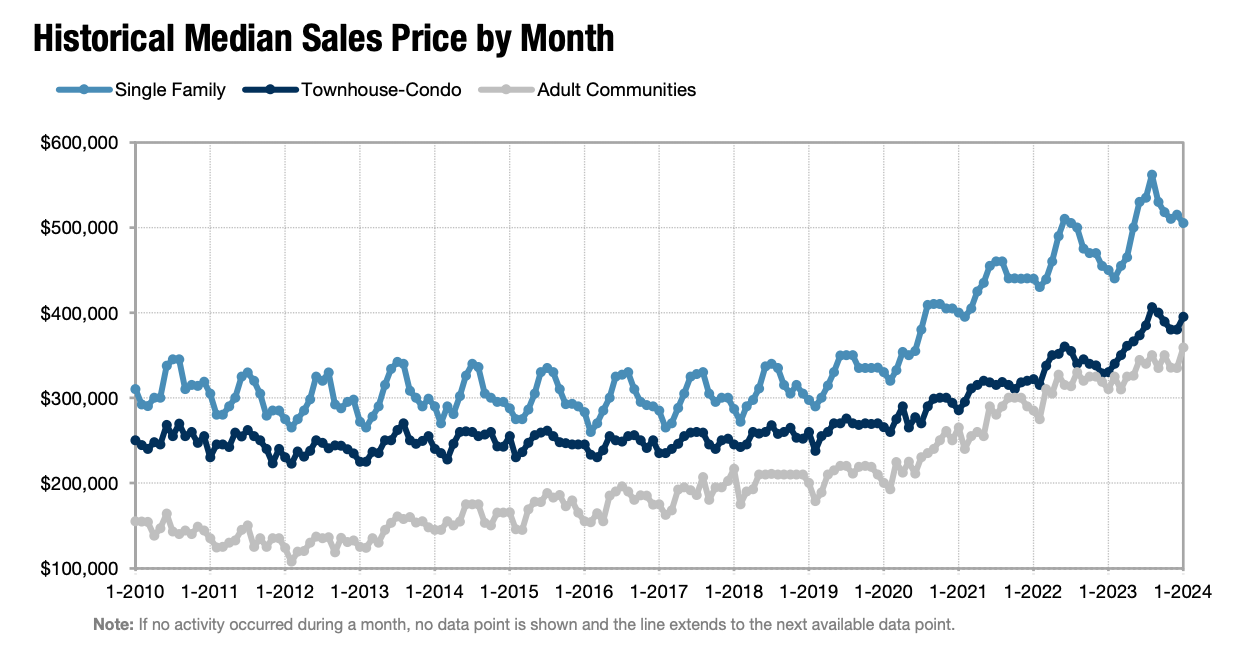

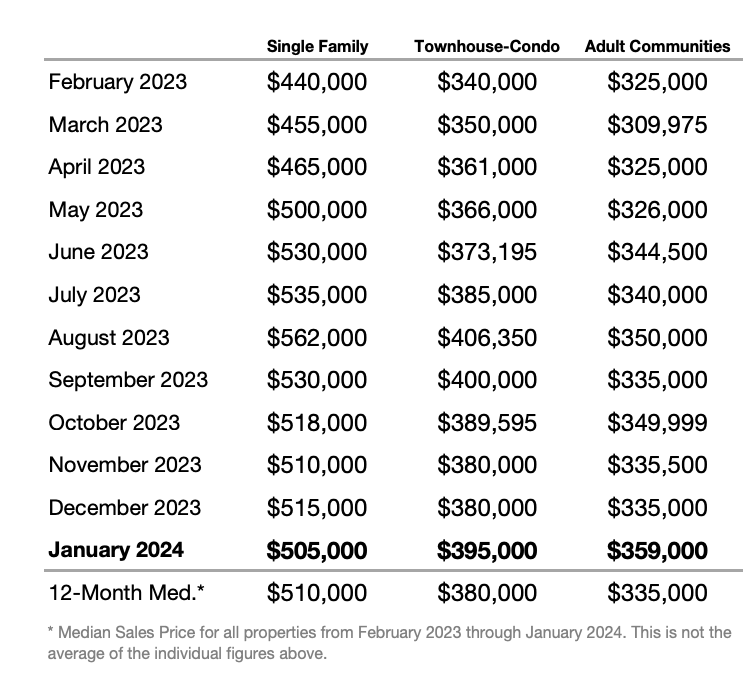

The real estate market in New Jersey can affect HELOC terms and availability. According to New Jersey Realtors® (NJR), the state’s property values are higher than the U.S. median. The median sales price of a single-family home in New Jersey in January 2024 was $505,000. Nationwide, the median home price was $420,700.

Homeowners in New Jersey may, on average, have more home equity. Home equity is the difference between the current market value of the home and any outstanding mortgage balances. Higher property values mean homeowners might have more equity to borrow against, which could lead to larger HELOCs.

As you can see, New Jersey’s home prices have skyrocketed since 2010:

They’ve also seen a dramatic overall rise in the past 12 months in the state:

This dramatic increase can boost lenders’ confidence. Rising home values typically reduce the loan-to-value ratio (LTV), a key risk metric for lenders. A lower LTV ratio means less risk for lenders, which can result in more favorable HELOC terms, such as lower interest rates or higher credit limits, compared to states where home values are stagnant or falling.

High property values in the state are even more significant in certain counties. For example, here are the median sale prices of a single-family home in January 2024 in three counties:

- Cape May County (Southern New Jersey): $702,500

- Monmouth County (East Central New Jersey): $727,000

- Bergen County (Northeast New Jersey): $690,000

This underscores the strength of local real estate markets, which can influence HELOC availability and terms even within the state. Lenders might offer more competitive rates or larger credit lines in these areas, recognizing the lower risk associated with higher-value properties.

How your HELOC rate affects your overall loan cost

A solid reason to search for the best HELOC rates in New Jersey (or whichever state you may be borrowing in) is this: A lower rate can mean a lower cost of borrowing overall.

Your HELOC rate can affect your monthly payments, as well as the total amount of interest you pay for the life of the loan. So it makes sense to search for the best rates possible when planning to borrow against your home equity.

For example, say you’d like to borrow $100,000, and you have a choice between two lenders. One offers you a HELOC at 8.50%, and the other wants to charge 8.75%. Here’s how the difference works out:

| Loan A (8.50%) | Loan B (8.75%) | |

| Draw period payment (interest-only for 10 years) | $708.33 | $729.17 |

| Regular payment (20-year term) | $867.82 | $883.71 |

| Total interest paid | $193,270 | $199,520 |

A difference of just 0.25% means paying over $6,200 more for your HELOC over the entirety of the loan term. That’s an excellent reason to shop around to find the lowest HELOC rates. Finding a lender that offers an autopay discount could yield additional savings.

Keep in mind that these calculations assume you have a fixed-rate HELOC. If you choose a variable-rate HELOC instead, your monthly payments could be lower or higher at different points in the loan term. A changing rate could also mean paying more or less in interest.

How to get the lowest HELOC rates in New Jersey

Eligibility for a HELOC in New Jersey is similar to eligibility requirements in other states. Some of the most important things lenders consider include:

- Your credit scores

- Income and debt-to-income ratio (DTI)

- How much equity you’ve accumulated in the home

A good to excellent credit score can help you qualify for lower HELOC rates, but a poor credit score could mean paying a much higher rate. If you’re considering a HELOC in New Jersey, it’s helpful to check your credit before looking into loans to get a better idea of what you might qualify for.

Keep in mind that the best time to get a HELOC is when rates are low. Since the Federal Reserve began implementing rate hikes to curb inflation, HELOC rates in New Jersey and other states have increased.

However, if you need a HELOC now, here are a few helpful tips to keep in mind so you can find the lowest rates in New Jersey.

- Check your current bank or mortgage lender first. It may be worth checking HELOC rates at your bank or current mortgage lender to see what’s on offer. Your bank might offer a relationship rate discount or fee waivers as an incentive to get your business.

- Review your credit. If you haven’t checked your credit yet, it’s wise to do so. That can make it easier to narrow down which HELOCs you have the best odds of being approved for.

- Compare lenders online. When comparing online HELOC lenders, first check to see whether they offer loans in New Jersey. Many lenders offer HELOCs nationwide, but not all of them. Once you find New Jersey HELOC lenders, you can get rate quotes to see how the terms compare.

- Consider things other than rates. Getting the lowest rate might be your primary goal, but remember to review the other details of any HELOC you’re weighing. That includes the draw period, repayment term, minimum credit score requirements, LTV requirements, and any fees you might pay.

At a minimum, you may want to get HELOC rate quotes from three different lenders. That can give you an idea of the range of rates you might expect. Most lenders should let you check your rates online without performing a hard pull of your credit history.

How to apply for a HELOC in New Jersey

If you’ve done the preliminary work of finding a HELOC lender in New Jersey, applying for a loan is the next step. The exact process can vary from lender to lender, but here’s what you can expect.

- Complete the application. A HELOC application should ask for personal information about yourself, including your name, date of birth, and Social Security number. You’ll also need to share information about your income and debts, as well as details about your home. That includes the address, property type, and estimated mortgage balance.

- Provide any supporting documentation. Your lender may ask for copies of bank statements, pay stubs, and tax returns to verify your income. You may also need to share recent mortgage statements so the lender knows how much you owe on your home.

- Complete the appraisal. An appraisal is often a requirement for a HELOC because the lender needs to know how much your home is worth. The form the appraisal takes—whether in-person, virtual, or drive-by—can depend on the lender. You’ll pay the appraisal fee at the time it’s scheduled.

- Wait for approval and review the loan terms. Assuming you’re approved, your lender will provide you with details regarding your HELOC. That includes the amount you’re approved for, your interest rate, and any fees. It’s important to read through these documents to understand what you’re agreeing to before you sign.

- Sign the paperwork and access your credit line. If everything on the loan paperwork looks correct, you can move forward with closing. You’ll pay any closing costs due, if necessary, and sign all the loan paperwork. Once that step is complete, your lender will arrange to give you access to your credit line.

How you access your credit limit can depend on the lender. You might have the option to write checks from your credit line, make cash withdrawals at a branch if you applied at a bank or credit union that operates in New Jersey, or spend with a debit or credit card.

Once your credit line is open and accessible, you can use it however you see fit. And remember that if you’re opening a HELOC in New Jersey just in case of emergency, you’re not obligated to use it unless you need to.

FAQ

What is the lowest HELOC rate in New Jersey?

The lowest HELOC rate in New Jersey will depend on which lender you’re considering. It’s possible to find HELOC rates in New Jersey as low as around 8% as of February 2024, but some lenders charge more for home equity loans. Getting rate quotes from multiple lenders can help you find the best rates.

What HELOC has the highest rates in New Jersey?

There is no single highest-rate HELOC in New Jersey. The rates lenders charge are determined by the interest-rate environment and a borrower’s qualifications. Generally speaking, the lower your credit score, the higher the rate will be when getting a HELOC.

What is the current average HELOC rate in New Jersey?

Our analysis found that in February 2024, HELOC rates in New Jersey range between 7% and 10% on average, but some lenders charge above 10% for a home equity line of credit. In general, HELOC rates in New Jersey and elsewhere have increased due to the Federal Reserve’s decision to implement multiple rate hikes.

Will my New Jersey HELOC have insurance requirements?

If you’re getting a HELOC in New Jersey, your lender may expect you to meet the same insurance requirements associated with purchasing mortgage loans. That includes having homeowners insurance to protect the property against damages from covered perils.

Do any lenders not offer HELOCs in New Jersey, and why not?

Plenty of lenders offer HELOCs to New Jersey residents, but just as many don’t operate in the state. Hitch, for example, does not offer HELOCs in New Jersey. Why lenders operate in some states but not others may be due to their business model or a lack of licensing.

About our contributors

-

Written by Rebecca Lake, CEPF®

Written by Rebecca Lake, CEPF®Rebecca Lake is a certified educator in personal finance (CEPF®) and freelance writer specializing in finance.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.