Your credit score plays an important role in the approval process, loan terms, and interest rates for any personal loan.

The minimum credit score requirements vary by lender, ranging from 300 to 700 in our research, and some lenders offer personal loans with no minimum credit score requirement. Lenders that don’t require high credit scores will rely on other factors in your finances, such as employment history, income, and debt-to-income ratio. They might also require collateral or a cosigner.

Table of Contents

What credit score is needed for personal loan approval?

Lenders assess your credit score to gauge the risk of loaning you money. FICO scores, ranging from 300 to 850, are commonly used, with fair credit starting at 580 and good credit at 670. FICO scores are based on payment history, amounts owed, credit history length, credit mix, and new credit.

Here are several top-rated lenders’ credit score requirements, along with more information about their loans:

Higher scores suggest responsible credit management, while lower scores indicate higher risk. You can check your credit score using free monitoring services, through your credit card issuer, or by purchasing it from FICO.

FICO credit scores are calculated based on the following categories:

More about the FICO score components

- Payment history (35%): The largest category is based on your record of paying back your creditors. On-time payments boost your score; late or missed payments damage it.

- Amounts owed (30%): The amount of debt you owe also affects your score, as does your credit utilization ratio, or the amount of credit you’re using compared to how much is available to you. Try to keep your credit utilization under 30% to protect your score.

- Length of credit history (15%): A longer credit history is better for your score.

- Credit mix (10%): Having a mix of credit, such as installment loans and revolving credit, can also help your score.

- New credit (10%): Recent loans or other debt can damage your credit and be a red flag to lenders.

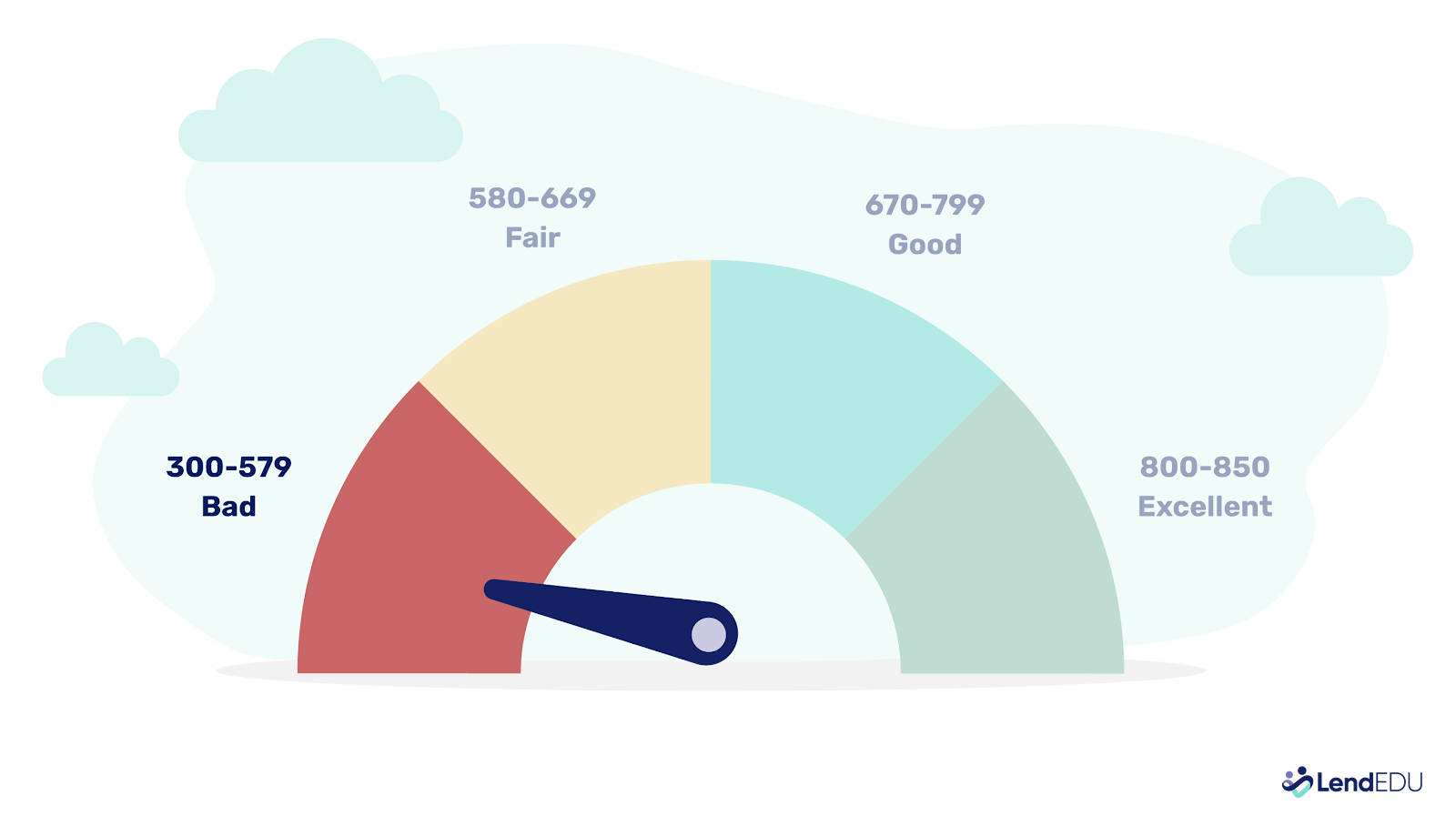

Personal loans for credit scores of 300 to 579 (poor credit)

Having poor credit can make it challenging to get approved for a personal loan.

Even if you are approved, you may get stuck with an interest rate on the high end of a lender’s range, which could go up to 36%.

Here are the best lenders we’ve found for this credit score range:

For more about these companies, check out our guide to the best bad-credit loans.

However, you can take steps to boost your chances of approval or access lower rates, including:

- Improve your credit score before you apply. If you don’t have an immediate need for a loan, work to improve your credit score before you start loan shopping. These could include making on-time payments on your debts, paying down balances, and reducing your credit utilization. You may also review a free copy of your credit report from AnnualCreditReport and dispute errors you find, if any.

- Apply with a cosigner. Some lenders let you submit a joint application with a cosigner or co-borrower. If your cosigner or co-borrower has good credit, you may have a better chance of getting approved or qualifying for a lower rate. Keep in mind that the personal loan and repayment will affect your and your joint applicant’s credit.

- Consider a secured personal loan. Most personal loans are unsecured, but some lenders offer secured options that you back with collateral, such as a car or savings account. Because lenders see secured loans as less risky, they may accept lower credit scores and offer better rates and higher loan amounts. However, you risk losing your assets if you fall behind on payments.

Read More Personal Loans for a Credit Score of 550

If conventional lenders reject your application for a loan, try peer-to-peer lending. These companies still check your credit score when you apply, and you can use the borrowed money for various purposes. The worse your credit score, the higher your interest rate will be, and you may still not get approved.

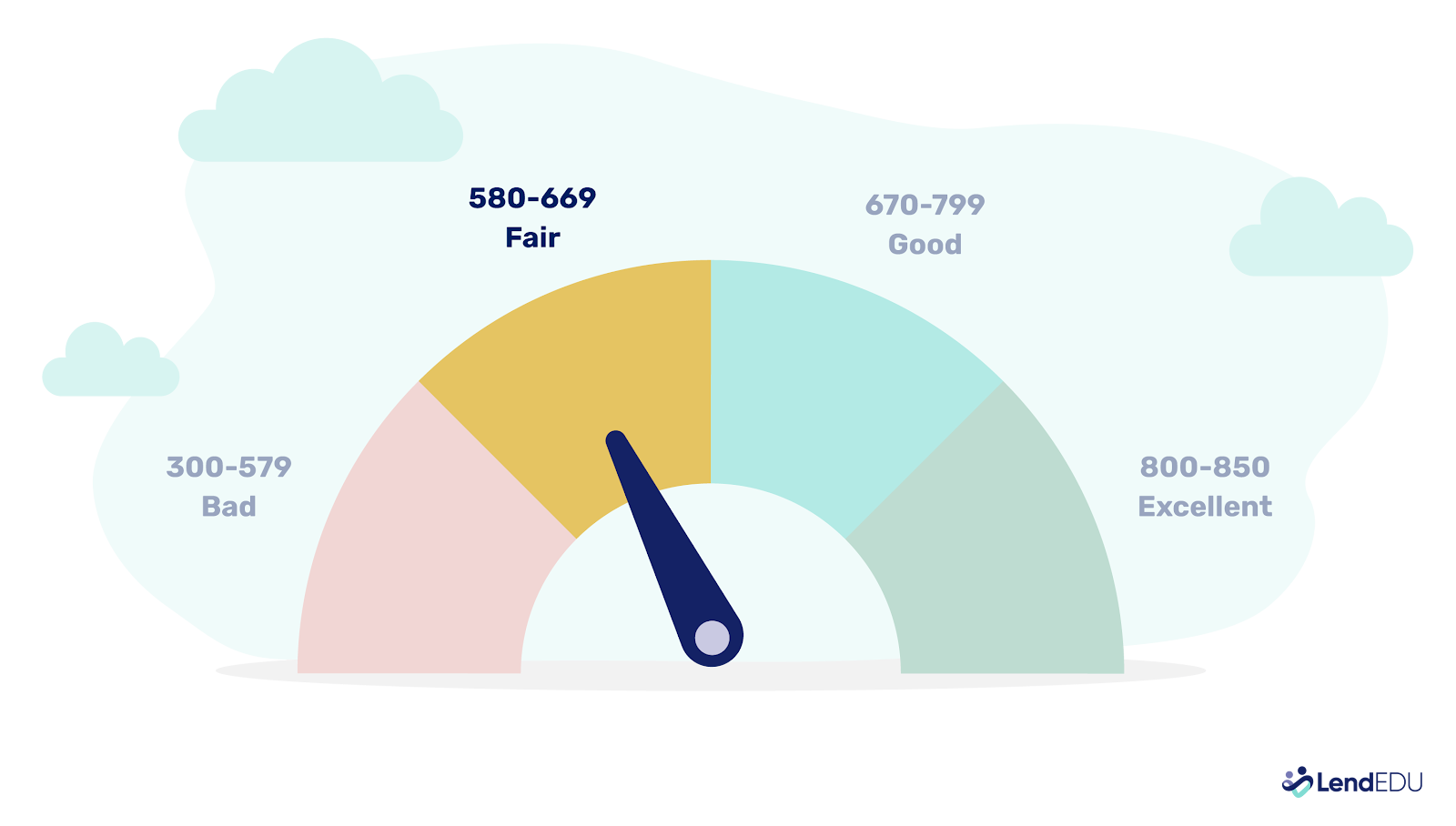

Personal loans for credit scores of 580 to 669 (fair credit)

Having fair credit will give you more options for personal loans and improve your chances of approval, and you won’t get the highest rates. According to the Federal Reserve, the average rate on a two-year personal loan in August 2024 was 12.33%.

Here are excellent lenders for fair-credit borrowers:

Some of these lenders let you check your rates through prequalification, which won’t affect your credit score, so it’s worth shopping around to find your best personal loan offer. For more information, check out our selections for the best fair-credit loans.

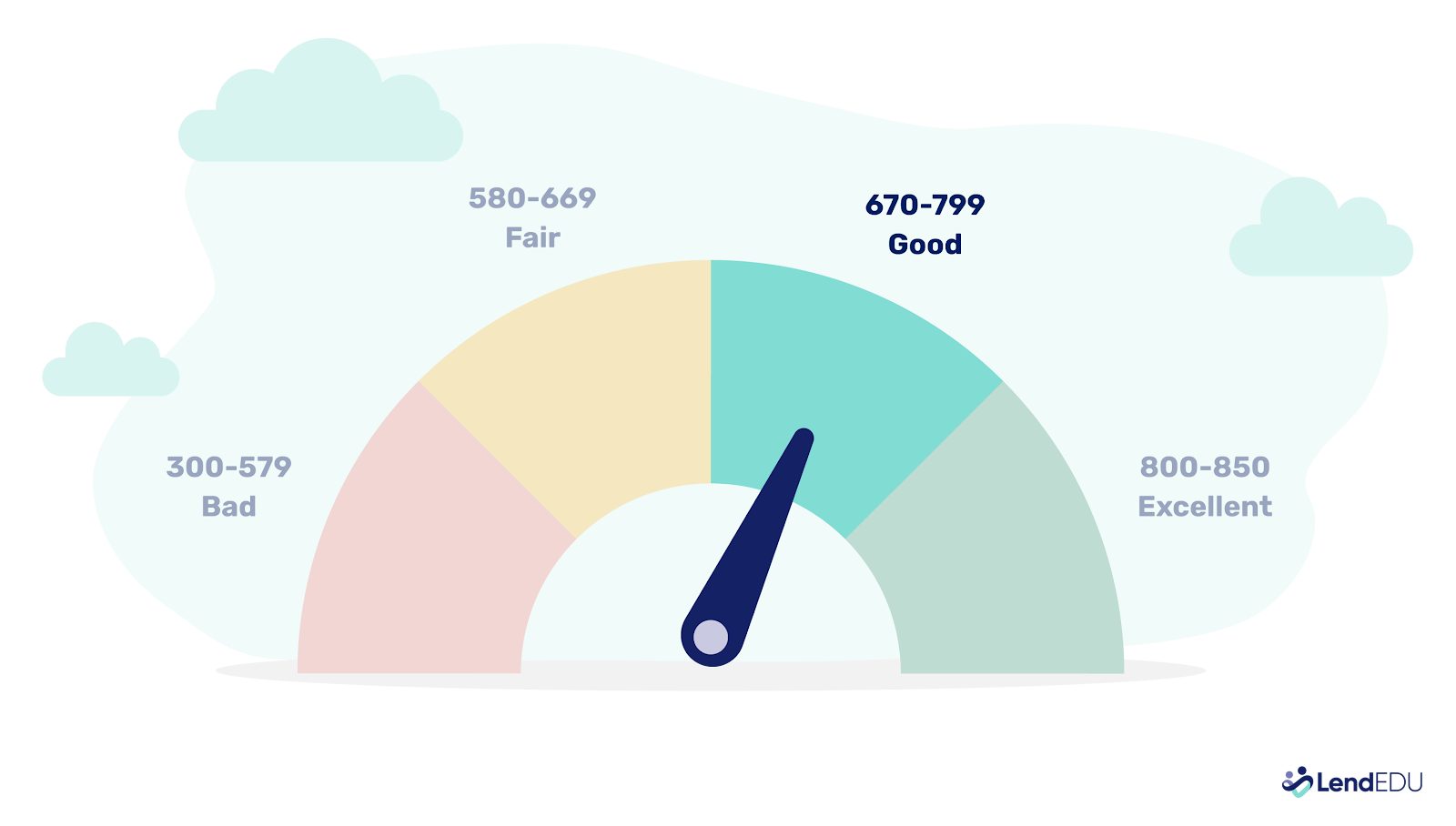

Personal loans for credit scores of 670 to 799 (good credit)

Borrowers with good credit will have an easier time getting approved for a personal loan and have access to a wider range of lenders. If you have very good or excellent credit, you could qualify for a lender’s lowest rates.

These are the best lenders for borrowers with good credit:

Comparing offers from multiple lenders can help you find the most affordable loan. See more about the best good-credit loans here.

How to qualify for a personal loan

While every lender sets its own specific borrowing criteria, taking these steps can help you qualify for a personal loan.

Check your credit

Review your credit score and report for errors or improvement areas. Knowing your score helps you target lenders that are a good fit. Improving your score before applying can boost your chances of better rates.

If you are repairing damaged credit, be patient. It takes time for negative items to fall off your credit history.

Research lenders

Explore banks, credit unions, online lenders, and peer-to-peer lenders to find the best fit for your financial profile. Check with your current bank; some offer benefits, such as rate discounts for customers.

Read More Best Hardship Personal Loans

Prequalify for personal loans

Prequalifying lets you check your rates with a soft credit check, which won’t affect your score. It provides a glimpse of your potential offers but isn’t a final commitment.

Read More How to Get a Loan With No Credit Check

Other factors that determine approval

Your credit score is a major factor in qualifying for a personal loan, but it’s not the only one. Lenders also consider other financial characteristics, including:

- Income: Lenders want to know you have a reliable source of income and so may require pay stubs or tax returns.

- Debt-to-income ratio: Your DTI compares your monthly debt obligations with your income. Lenders usually prefer a DTI lower than 36%.

- Repayment history: Lenders will examine your payment history on your credit report to assess the likelihood you’ll repay a loan.

- Free cash flow: Lenders may review your bank account transactions to ensure you have enough money left over each month to afford a personal loan payment.

- Verifiable bank account: Lenders generally want you to have a bank account where they can send the loan proceeds.

If you pursue a secured loan, you’ll need to pledge collateral with sufficient value to back the loan. Borrowers applying jointly will also need to provide information on their cosigner or co-borrower. The lender will take both applicants’ financial profiles into account.

Adding a cosigner with a good credit score and an established credit history can allow you to qualify for a lower rate or get approved.

You must also meet a lender’s requirements for age (usually 18 or older) and residency because some lenders only operate in certain states. Lenders typically require verifying documentation when you apply, such as proof of address, pay stubs, or bank statements.

How do you apply for personal loans?

Once you find the right lender, you can apply online or at a local branch if required. Getting a personal loan often involves filling out an application, providing documentation, such as pay stubs and bank statements, and consenting to a hard credit check.

If approved, you’ll sign the loan agreement and get funds, often within a day or two. Start repayments as agreed, and consider setting up automatic payments.

FAQ

Does applying for a loan affect my credit score?

Applying for a loan can affect your credit score. If a lender runs a hard credit inquiry, your score could decrease by a few points. However, the damage should be temporary, and your score can bounce back in a few months if you make on-time payments on your debts.

What’s the difference between a soft and hard credit inquiry?

A soft inquiry doesn’t affect your credit score or appear on your report; it’s often used when prequalifying for loans. A hard inquiry can lower your score slightly, and it shows up on your report when you apply for credit with a lender.

Can I do anything to help improve my loan terms?

Improving your credit score can help you get better loan terms. Lenders typically offer the best rates to borrowers with good or exceptional credit. Your loan amount and repayment terms can also affect your interest rate, so it’s worth adjusting your loan size and terms to see which could get you the best rate.

Do any lenders offer no-credit-check personal loans?

Most lenders check your credit to gauge your ability to repay the loan. However, a few reputable lenders offer no-credit-check personal loans. We’re wary of many lenders that offer no-credit-check loans because they tend to be high-rate payday loans.

If you need to borrow a smaller amount, like a few hundred dollars, check out cash apps.

About our contributors

-

Written by Rebecca Safier

Written by Rebecca SafierRebecca Safier is a personal finance writer with years of experience writing about student loans, personal loans, budgeting, and related topics. She is certified as a student loan counselor through the National Association of Certified Credit Counselors.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.