Residents of the Palmetto State have plenty of personal loan options. You can choose between online lenders and community credit unions. We’ve evaluated personal loans from each source and will walk you through how to select the best fit.

First, review these lender recommendations. Then we’ll discuss everything you need to know about South Carolina personal loans.

Table of Contents

Reviews of the best online personal loans in South Carolina

If you’re unfamiliar with online lending, it’s more similar to traditional lending than you might think. Both types of lenders require an application, and both aim to offer competitive rates.

The primary difference between working with an online lender and a local one is that you don’t need to (and often can’t) visit an online lender in person. You’ll apply for, manage, and contact customer support through digital channels.

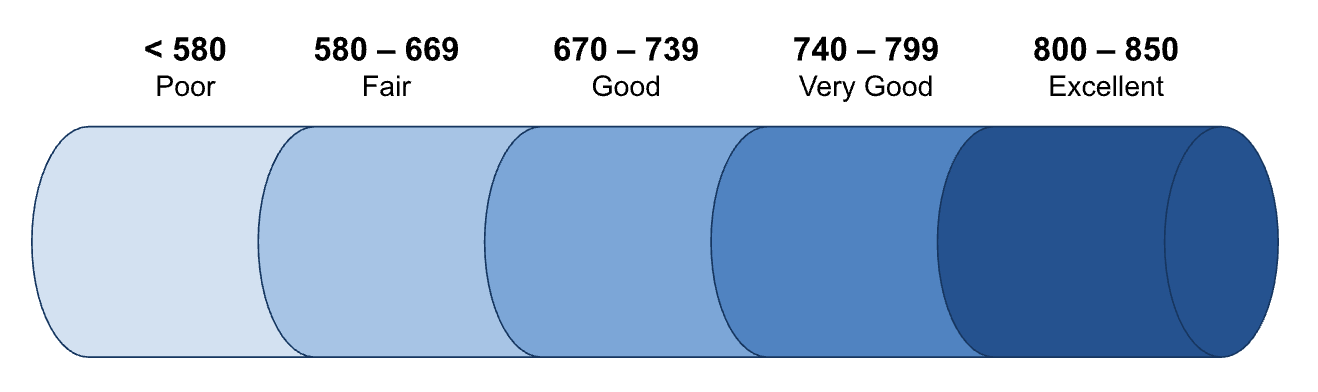

Whether your lender operates in cyberspace or in the physical space, it considers your credit when you request a loan. Some lenders set minimum credit score requirements, while others suggest a minimum credit category, like the FICO ranges shown below:

For example, one lender may only approve borrowers with very good or excellent credit, but another may accept fair-credit borrowers. While higher scores often qualify for the best rates, a lower score isn’t an automatic denial if you apply with the right lender.

To that end, our recommended lenders cater to a range of credit profiles. We weighted, scored, and combined these factors to produce a final editorial rating. This rating is expressed on a scale from 1 to 5, with 5 being the highest possible score. Each online lender’s rating is included below. We’re confident South Carolina residents will have a great borrowing experience with these four lenders.

Credible

Why Credible is the best marketplace

Credible is the premier online marketplace for comparing a broad array of loan offers. Its vast network of lenders allows South Carolinians to evaluate competitive rates without leaving their homes. Credible ensures a hassle-free experience. Checking rates doesn’t affect your credit score.

Your loan terms will depend on which of Credible’s partner lenders you choose. For example, you might pay origination fees to the lender, but you won’t pay any fees to use Credible’s service.

- Compare loans from multiple curated lenders

- Get prequalified loan offers in as little as 2 minutes

- Get funded within a few business days

- No option to apply for joint loans

| Rates (APR) | 6.99% – 35.99% |

| Loan amounts | $1,000 – $200,000 |

| Repayment terms | 1 – 10 years |

Eligibility requirements

- Soft credit check? Yes

- Minimum credit score: Varies

- Minimum income: Not disclosed

- States: Loan partners may not be available in all states

Repayment terms

Credible loans have repayment terms ranging from one to 10 years. Some lenders may charge a prepayment penalty if you pay your loan off early.

LightStream

Why LightStream is the best personal loan for excellent credit

LightStream is our top choice for South Carolina residents with excellent credit. Known for its competitive rates and no fees, LightStream offers customized loans that match your financing needs, and funds can be available the same day you’re approved.

A downside of LightStream is that it doesn’t offer a soft credit check to prequalify: You’ll undergo a hard credit check, which can lower your credit score, just to view your rates. For this reason, we think LightStream is best for excellent-credit borrowers who are confident they’ll be approved.

- Rate match guarantee ensures that you get the best rate possible

- Same-day funding may be available

- Take advantage of a longer repayment term if you need lower payments

- No option to prequalify or check rates with a soft credit pull

- Minimum loan amount is $5,000

| Rates (APR) | 7.49% – 25.49% |

| Loan amounts | $5,000 – $100,000 |

| Repayment terms | 2 – 12 years |

Eligibility requirements

- Soft credit check? No

- Minimum credit score: 660

- Minimum income: Not disclosed

- States: All 50 states and Washington, D.C.

Repayment terms

LightStream offers some of the longest repayment terms of any lender, giving you up to 12 years to repay your loan. You can pay your loan off early, without a prepayment penalty and rate discounts can help bring the cost of your loan down.

SoFi

Why SoFi is the best personal loan for good credit

We like SoFi for South Carolinians with good credit scores. It offers no required fees, quick funding times, competitive rates, and flexible loan options. SoFi allows you to check your rate in 60 seconds without affecting your credit score. However, its $5,000 minimum loan amount may be higher than you need.

- No origination fees, late payment fees, or prepayment penalties

- Check rates in as little as 60 seconds

- Some borrowers may qualify for same-day funding

- Higher minimum loan amount

- Autopay discount is lower than what some lenders offer

| Fixed rates (APR) | 8.99% – 29.99% with all discounts |

| Loan amounts | $5,000 – $100,000 |

| Repayment terms | 2 – 7 years |

Eligibility requirements

- Soft credit check? Yes

- Minimum credit score: 660

- Minimum income: Not disclosed

- States: All 50 states and Washington, D.C.

Repayment terms

SoFi personal loans feature terms from two to seven years. If you enroll in autopay, you’ll get a 0.25% rate discount. There’s no penalty if you decide to pay your loan off early.

Upgrade

Why Upgrade is the best personal loan for fair credit

Upgrade is a crucial resource for South Carolinians with fair credit. It offers accessible financial products and tools to help you improve your credit health. Upgrade will allow you to adjust your payment date during repayment if needed.

Upgrade accepts joint applications, so it could be an excellent fit if you’re considering applying with a co-borrower with a better credit score or higher income to be eligible for better rates and terms. You can check your rate without affecting your credit score.

- Choose your monthly payment and loan term

- Joint applications accepted

- Loan funds may be available in as little as 1 day

- Smaller loan maximum limit

- 1.85% to 9.99% origination fee

| Rates (APR) | 8.49% – 35.99% |

| Loan amounts | $1,000 – $50,000 |

| Repayment terms | 2 – 7 years |

Eligibility requirements

- Soft credit check? Yes

- Minimum credit score: 580

- Minimum income: Not disclosed

- States: All 50 states and Washington, D.C.

Repayment terms

Upgrade loans have repayment terms from two to seven years, and your monthly due date is adjustable to fit your budget. A short-term financial hardship program is available if you’re temporarily unable to manage payments.

Local South Carolina personal loan lenders

Some borrowers prefer working with a local credit union. South Carolina residents may find personal loan options through the following institutions, though eligibility and loan terms vary by membership requirements.

| Lender | Loan amounts | Estimated APR range | Notable details |

|---|---|---|---|

| South Carolina Federal Credit Union | $500 – $25,000 | 12.00% – 18.00% | 32 branches statewide; membership requires a $10 savings deposit |

| Founders Federal Credit Union | Not disclosed | 11.40% – 18.00% | Primarily serves Midlands and Upstate; offers Skip-A-Pay after six months |

| SPC Credit Union | $500 – $40,000 | 10.00% – 18.00% | Serves parts of eastern SC; offers virtual branch support |

About South Carolina personal loans

You have certain consumer protections when you borrow a personal loan in South Carolina. One requires lenders to be more transparent when charging interest rates above 18%.

It requires these lenders to post maximum rate schedules outlining their higher rates and file them with the state before they can charge rates over 18%. In other words, if your lender assesses above-average rates, you’ll know.

South Carolina doesn’t impose an interest rate cap; it just prohibits unconscionability. “Unconscionable” rates are those that exceed reasonable expectations to the borrower’s detriment.

Aside from legal protection, knowledge is the next-best defense against high interest rates. Become a well-armed consumer by learning how to spot a good rate on a personal loan.

The term unconscionability leaves plenty of gray area. Without a set rate cap, personal loan lenders in South Carolina have almost unlimited freedom when it comes to charging interest.

Keep that in mind as you shop for personal loans. Your interest rate influences your loan’s overall cost.

Say, for example, you borrow $10,000 over a 36-month term. Take a look at how different rates can affect your monthly payments and total borrowing cost:

| Interest rate | 12% | 16% |

| Monthly payment | $332 | $352 |

| Total interest paid | $1,957 | $2,657 |

| Total loan cost | $11,957 | $12,657 |

An extra $20 a month might not sound like much, but that adds up to $700 by the end of your loan term. We recommend knowing your rights under South Carolina law and being selective when it comes to choosing a lender.

Should you choose a national or local personal loan lender?

National and local lenders are beholden to the same regulations, so which one is right for you can depend on your ideal borrowing experience.

Are you partial to a high-touch lending relationship or prefer self-service account management? Can you work with a regional institution, or is multistate availability a must? Here’s a quick rundown of how national and local lenders compare along these lines:

| National lenders | Local lenders |

| Expanded service area | Limited service area |

| Often offer enhanced digital access | May prioritize in-person support |

| May have more innovative benefits | Approval criteria could be more lenient |

| Rates might be higher | Rates may be more competitive |

Larger lenders are more likely to operate across states and time zones, which could be helpful if you travel frequently or need support outside of standard business hours.

These lenders tend to rely on technology to serve their increased customer volume, sometimes at the expense of face-to-face assistance.

Many local lenders offer online account access, but you might be limited to basic features and tools. These lenders often prioritize personal interaction. You might view that as an advantage or an inconvenience, depending on your circumstances.

If you’re not limited to loans in South Carolina—say, if you work or go to school just over the border in Tennessee or Florida—check out your other personal loan options by state.

As you weigh these factors, consider your personal and financial priorities and how your needs may change over time. Use the table below to see how national and local lenders perform in different scenarios.

| If you… | Consider |

| Aren’t comfortable with technology | Local lenders |

| Plan to move before your loan is paid off | National lenders |

| Want to keep your money in your community | Local lenders |

| Don’t live within driving distance of a local lender | National lenders |

You might have made up your mind as to which type of lender is the best fit. Still, it’s worth getting preliminary loan offers from a range of national and local lenders before committing to one or the other.

Some lenders match or beat competitor rates, so you may be able to use your second-choice lender’s loan offer to snag a better rate with your top pick.

How to apply for a personal loan in South Carolina

Applying for a personal loan in South Carolina can be quick and easy, especially if you know what to expect. Here’s how to prepare for and submit your loan application:

- Gather your documents. You’ll need electronic copies of your government-issued photo ID and pay stubs. You can also use W-2s or tax returns in lieu of pay stubs.

- Prequalify online. Before you take out a loan, we recommend checking your rates with four to five lenders. Prequalifying only takes about 60 seconds and won’t affect your credit. This empowers you to make a more informed lending decision.

- Fill out your lender’s application. Once you find a suitable loan offer, complete an application on that lender’s site (or at a branch if you opt for a local lender and want one-on-one application support).

- Complete your lender’s credit check and verification processes. Credit checks happen behind the scenes, but your lender may request additional information to confirm your identity and income. The faster you respond to these requests, the faster your lender can get you a decision.

- Sign your loan agreement. If you’re approved, your lender will send you an official agreement. Review and sign this document to take out your loan.

You may be able to adjust your loan terms during your loan application. Use our personal loan payment calculator to see how different repayment periods affect your borrowing cost before you sign.

After accepting your loan, your lender will begin disbursing your loan proceeds. Some lenders, including LightStream and SoFi, can fund personal loans as soon as the same day. In general, expect to get your disbursement within one to two business days.

FAQ

What is the interest rate for a personal loan in South Carolina?

Interest rates for personal loans in South Carolina can vary depending on factors such as the borrower’s credit history, loan amount, and loan terms. However, South Carolina doesn’t impose a usury cap on consumer loans, so by law, lenders can charge high interest rates—in some cases, up to triple digits. It’s critical to compare rates from multiple lenders before committing to any personal loan.

Can you get a personal loan in South Carolina with bad credit?

Yes, getting a personal loan in South Carolina with bad credit is possible. Some lenders offer bad credit loans, which typically come with higher interest rates and stricter terms. We recommend improving your credit score as much as possible before applying for a loan because it decreases the overall cost of borrowing.

What credit score is needed for a personal loan in South Carolina?

Credit score requirements can vary by lender, but a score of 600 or higher should put you in solid standing for a personal loan. Some lenders may accept a FICO score as low as 300—the lowest possible—but it typically comes with higher interest rates. Lending criteria differ between lenders, so check with each lender to know its specific credit score requirement.

What is the easiest place to get a personal loan in South Carolina?

The ease of getting a personal loan can vary by lender. However, banks and credit unions have traditionally been the go-to sources for personal loans. Many people in South Carolina are turning to online lenders due to their easy application process and quick approval times. Before deciding, it’s essential to research and compare each option for the best fit for your financial needs.

Recap of the best online personal loans in South Carolina

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.