Refinancing your student loans involves applying for a new private loan to pay off one or more federal or private student loans. This repayment strategy could save you hundreds of dollars if you can secure a lower interest rate than you currently pay.

But refinancing isn’t a one-size-fits-all solution—saving money depends on several factors, including your credit score and income.

To help you decide whether it’s the right strategy for you, we’ll walk you through some scenarios where you could save money and discuss the benefits and drawbacks of student loan refinancing.

Table of Contents

Does refinancing student loans save you money?

Whether refinancing your student loans saves you money depends on your unique financial situation. But there are some steps you can take to assess your chances of qualifying for a refinance loan at a lower interest rate.

- Prequalify. Some lenders allow you to prequalify online to preview rates and terms you could receive without harming your credit. However, prequalifying doesn’t guarantee a lender will approve you after submitting a full application.

- Compare quotes. Get estimated rates and terms from multiple lenders to find the best deal. If you want to save money, look for a lender that offers a lower rate than the average rate on your outstanding student loans.

- Use a loan calculator. You can use a student loan refinance calculator to estimate your savings based on the lower rates you prequalify for.

In some cases, refinancing from a fixed-rate to a variable-rate loan could save you money, but it’s more difficult to estimate your savings because your interest rate could increase over the life of the loan.

How refinancing student loans can save you money

Refinancing your student loans could save you money if you swap your existing loan for a new one with a shorter repayment term or get approved for a lower rate.

For instance, refinancing from a 10-year, $20,000 loan at 8% interest to a five-year, $20,000 loan at 8% interest could cut your total borrowing costs in half, provided you can comfortably afford the higher monthly payments.

Here’s how the payments and costs break down.

| 10-year loan | 5-year loan | |

| Monthly payment | $243 | $406 |

| Total interest paid | $9,119 | $4,332 |

| Total borrowing costs | $29,119 | $24,332 |

You could also save money if you refinance to a loan with the same term but a lower rate.

| 10-year loan at 8% interest | 10-year loan at 6.5% interest | |

| Monthly payment | $243 | $227 |

| Total interest paid | $9,119 | $7,252 |

| Total borrowing costs | $29,119 | 27,252 |

When refinancing student loans won’t save you money

In some cases, even if you qualify for a lower rate, refinancing your student loan won’t save you money.

For example, say you have a five-year, $10,000 student loan at 7% interest and refinance to a 10-year loan at 7% interest to lower your monthly payments. In that case, your monthly payments would be lower, but you’d pay more interest over the life of the loan.

| 5-year loan | 10-year loan | |

| Monthly payment | $212 | $116 |

| Total interest paid | $2,748 | $3,933 |

| Total borrowing costs | $12,748 | $13,933 |

How much could you save by refinancing student loans?

Some lenders like ELFI have reported that their customers save hundreds of dollars per month on average after refinancing. But the amount you could save varies based on many factors, such as:

- The amount you’re refinancing

- Your current annual percentage rate (APR)

- Your new loan’s annual percentage rate

- Your new repayment terms

You can use our student loan refinance calculator to estimate your savings.

When deciding to refinance student loans, every borrower’s situation is unique and should be addressed in light of their current and potentially future situation. For example, some income-driven repayment programs work great if you file your taxes as single. But if you get married and find that filing jointly is better, that impacts your loan repayment terms. Bottom line: It really depends on your unique situation and the options presented, especially given recent changes to federal repayment plans.

Catherine Valega, CFP®

Weigh the pros and cons of refinancing

Before applying for a refinance loan, weigh the advantages and disadvantages.

Pros

-

You could save money

If you can qualify for a lower annual percentage rate (APR), you can save thousands of dollars in student loan interest.

-

Lower monthly payments

A lower rate could also lower your monthly payment.

-

Release a cosigner

Refinancing your loan is one way to release a cosigner. It might be the only way to release them if your lender doesn’t offer cosigner release.

Cons

-

Loss of federal benefits

Think twice before refinancing federal student loans because doing so means you’ll give up access to federal perks like student loan forgiveness, federal forbearance, and income-driven repayment (IDR) plans.

-

Lenders typically require good credit

You usually need stellar credit to qualify for a refinancing loan without a cosigner.

-

Hard credit inquiry

Most lenders perform a hard credit check to review your credit history when you apply, which can temporarily lower your credit score.

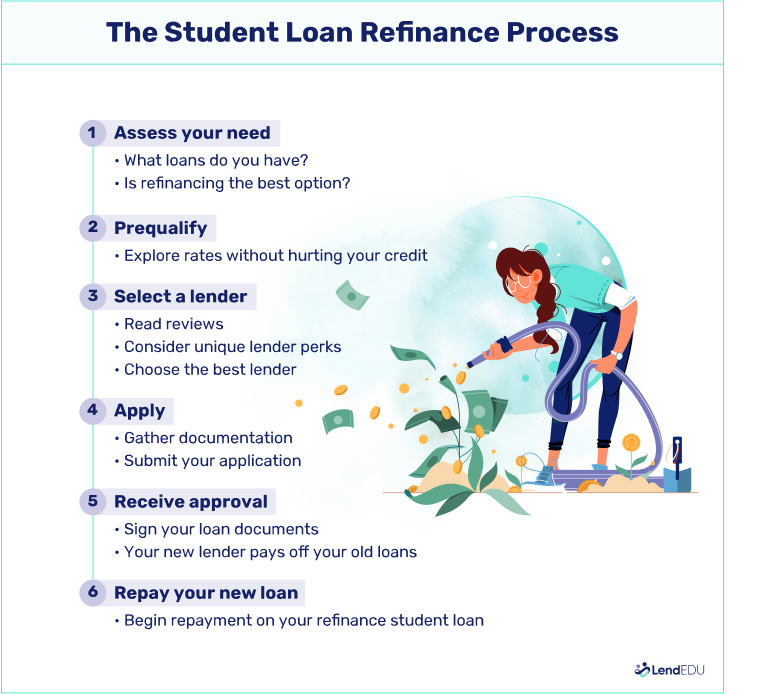

How to refinance your student loans

Once you’ve found a lender that best matches your needs, the next step is to submit a refinance application and complete the refinancing process.

Even after refinancing, it’s important to continue reviewing your repayment strategy. For example, as your income increases, you may decide to pay more on your loans to get rid of them faster.

Revisit your repayment strategy any time something changes that can greatly impact your financial life, such as a new job, a new spouse, children, a raise, or a job loss.

Catherine Valega, CFP®

Student loan refinancing FAQ

Am I eligible to refinance my student loans?

Eligibility to refinance student loans depends on several factors, including your credit score, income, and amount of debt. Different lenders have distinct criteria.

Some may require you to have a minimum credit score, cosigner, or specific employment status. We recommend exploring multiple lenders to identify the best fit for your situation.

Can I refinance federal and private student loans?

Yes—but it’s crucial to understand that you lose federal benefits once you refinance federal loans, such as income-driven repayment plans and potential loan forgiveness programs. Private loans don’t provide these benefits, so there’s less associated risk with refinancing them.

How does my credit score affect refinancing?

Your credit score plays a significant role in the refinancing process. A higher credit score indicates you’re a low-risk borrower, often leading to more favorable interest rates.

A low score might disqualify you from refinancing or result in higher interest rates. It’s crucial to understand your credit score before beginning the refinancing process.

Can refinancing student loans help improve my credit score?

Yes. When you refinance, the new lender pays off your student loans and replaces them with a single new loan. This consolidation can reduce your credit utilization and increase the average age of your credit accounts.

Regular on-time payments on the new loan can also boost your credit score over time.

Is there a cost to refinance my student loans?

Typically, the process of refinancing a student loan incurs minimal upfront cost. However, some lenders may charge origination fees or prepayment penalties.

Before agreeing to a refinance, it’s worth reviewing the loan agreement for any hidden charges or fees associated with the process.

How often can you refinance student loans?

There’s no limit on how often you can refinance student loans. It comes down to whether it makes financial sense for you.

For example, if interest rates plummet or your financial situation improves, you might find benefits in refinancing more than once. Refinancing multiple times may affect your credit score, so it’s important to consider it carefully.

About our contributors

-

Written by Jess Ullrich

Written by Jess UllrichJess is a personal finance writer who's been creating online content since 2009. She specializes in banking, investing, tax relief, and loans. She is a former financial editor at two popular online publications.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Catherine Valega, CFP®, CAIA®

Reviewed by Catherine Valega, CFP®, CAIA®Catherine Valega, CFP®, CAIA®, founded Green Bee Advisory LLC to help women, philanthropists, investors, and small businesses build, manage, and preserve their financial resources. She's been practicing financial planning for more than 20 years.