When repaying your student loans, the minimum payment is the lowest amount you can pay each month to keep them in good standing. As a result, it’s crucial to learn how to calculate your minimum payment so you avoid late fees or defaulting.

Aim to make extra payments if you want to pay off your student loans sooner. Below, we cover how to calculate the minimum payment on student loans and provide an example of how much you could save by making additional payments.

How to calculate your minimum student loan payment

How you calculate your minimum payment varies depending on your repayment plan. You can often calculate your minimum payment on your current private student loan—or a new one—by taking these steps:

- Gather your loan information. Locate the terms of your loan, including the amount you owe, your interest rate, and your repayment term.

- Plug the details into a loan calculator. Once you’ve found those details, enter them into a student loan calculator to estimate your minimum monthly payment. (See more about how to do this below.)

If you have a federal student loan, use the federal loan simulator to estimate your minimum payments based on different federal student loan repayment plans.

Whatever the minimum payment, I recommend setting up an automatic monthly payment to pay the minimum balance due. This will help you ensure you don’t miss a payment.

Erin Kinkade, CFP®

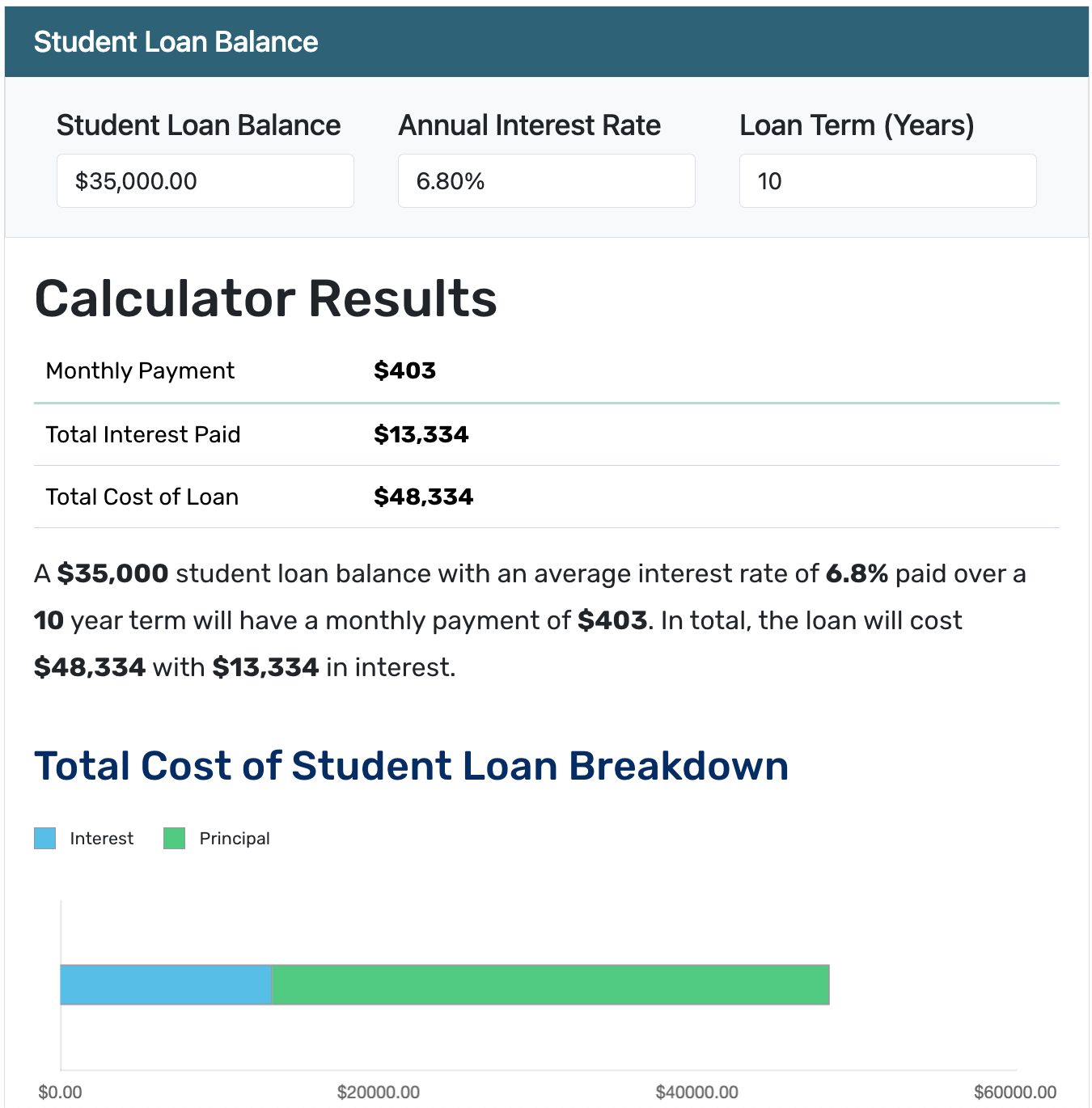

How to use a student loan minimum payment calculator

You can use our student loan payment calculator to estimate your minimum payment. Just enter the following information:

- Your student loan balance

- Your loan’s annual percentage rate (APR)

- Repayment term

After you’ve entered those details, you’ll see an estimated monthly payment.

It will also show you the amount of interest you’ll pay over the life of the loan if you only make the minimum payments and your total borrowing costs.

Should you pay more than the minimum student loan payment?

Paying more than the minimum is always smart, especially because most private and federal loans don’t charge prepayment fees. Doing so helps you pay off your student loans faster and save on interest.

For example, if you have a $25,000, 10-year student loan at 8%, you’d pay $11,398 in interest if you only made minimum payments. However, you’d save $3,319 in interest if you paid an extra $75 a month.

Before you pay more than the minimum payment, review your budget to see whether you can afford to do so while covering your necessities. If you have debts with higher interest rates than your student loans, consider paying those off first to save the most on interest.

What if you can’t pay your minimum student loan payment?

If you can’t afford your minimum student loan payment, contact your loan servicer to ask whether it offers relief programs.

For example, you may qualify for deferment or forbearance if you have federal student loans. Both of these options allow you to pause payments so you can avoid defaulting on your student loans.

While it’s less common, some private lenders provide forbearance or deferment options. The rules vary, so check with your lender to see what it offers and what you might need to qualify.

| Debt relief option | Best for |

| Forbearance | Borrowers with federal loans, though some private lenders offer forbearance options |

| Economic hardship deferment | Borrowers facing financial hardship who have federal student loans (some private lenders may also offer economic hardship options) |

| Income-driven repayment (IDR) plan | Borrowers with federal loans who want to make payments based on their income and family size |

About our contributors

-

Written by Jerry Brown, CFEI®

Written by Jerry Brown, CFEI®Jerry Brown is a freelance personal finance writer and Certified Financial Education Instructor℠ (CFEI®) who lives in New Orleans. He covers a range of personal finance topics, including credit, personal loans, and student loans.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.