Federal student loan rates over the years

In the following table, you will find the current and historic interest rates for federal loans. These rates coincide with the academic year the loans were taken out, i.e., fall 2023 to spring 2024. All rates shown are fixed.

| Loan type | ’25–’26 | ’24–’25 | ’23–’24 | ’22–’23 | ’21–’22 | ’20–’21 | ’19–’20 | ’18–’19 | ’17–’18 |

|---|---|---|---|---|---|---|---|---|---|

| Subsidized (undergrad) | 6.39% | 6.53% | 5.50% | 4.99% | 3.73% | 2.75% | 4.53% | 5.05% | 4.45% |

| Unsubsidized (undergrad) | 6.39% | 6.53% | 5.50% | 4.99% | 3.73% | 2.75% | 4.53% | 5.05% | 4.45% |

| Unsubsidized (grad) | 7.94% | 8.08% | 7.05% | 6.54% | 5.28% | 4.30% | 6.08% | 6.60% | 6.00% |

| PLUS (grad & parent) | 8.94% | 9.08% | 8.05% | 7.54% | 6.28% | 5.30% | 7.08% | 7.60% | 7.00% |

The Department of Education issues federal student loans. Students who fill out the Free Application for Federal Student Aid (FAFSA) are considered for these loans. Federal student loan interest rates are set once a year by Congress and are based on the 10-year Treasury note.

Here’s how interest works for different borrowers.

| Loan type | Who they’re for | How interest accrues |

|---|---|---|

| Direct Subsidized | Undergrad students with financial need | Does not accrue while in school or during deferment |

| Direct Unsubsidized | Undergrad, grad, & professional students enrolled at least half-time | Accrues while in school & during deferment |

| Grad PLUS | Grad students | Accrues while in school & during deferment |

| Parent PLUS | Parents of dependent undergrad students | During all deferment |

Federal student loan origination fees over the years

Federal student loans come with an origination fee deducted from your loan amount before disbursement. You’ll see a slight difference in the amount of loan funding you accept and the amount you receive.

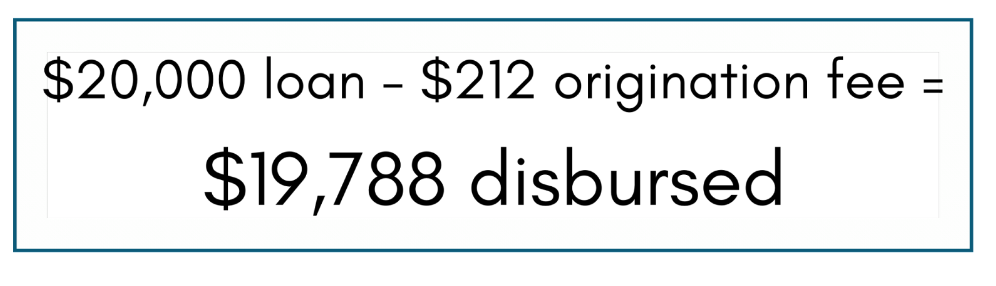

Here’s an example of how the origination fee works:

Here are the current and historical origination fees for federal student loans. Note that the fee for PLUS loans is around four times higher than the fee for other loan types:

| Loan type | ’20–’26 | ’19–’20 | ’18–’19 | ’17–’18 | ’16–’17 |

|---|---|---|---|---|---|

| Subsidized (undergrad) | 1.057% | 1.06% | 1.06% | 1.07% | 1.07% |

| Unsubsidized (undergrad) | 1.057% | 1.06% | 1.06% | 1.07% | 1.07% |

| Unsubsidized (grad) | 1.057% | 1.06% | 1.06% | 1.07% | 1.07% |

| PLUS (grad & parent) | 4.228% | 4.24% | 4.25% | 4.26% | 4.28% |

How Congress sets federal student loan interest rates

Congress passes legislation each year to set interest rates for student loans. The rates apply from July 1 of the first year to June 30 of the second year.

The Bipartisan Student Loan Certainty Act, signed into law in August 2013, ties federal student loan interest rates to prevailing market rates.

The interest rates for all federal student loans are based on the 10-year Treasury note auction yield plus a fixed increase. The Treasury Department auctions bonds monthly to raise money to support government spending. Congress uses the yield or interest rate the government pays to bond investors from the May auction to calculate student loan interest rates each year.

Current private student loan interest rates

Federal and private student loans have different interest rates. Private lenders can determine your rate based on your (or your cosigner’s) credit score and income, loan size, and other factors.

Private student loan interest rates may vary based on your year of enrollment. Undergraduate students often have the highest interest rates because many have no credit history or income. Lenders can use credit scores and income to gauge your ability to repay loans and the likelihood that you’ll pay on time.

Graduate students, meanwhile, may qualify for lower rates if they have an established credit history. Parents with good credit scores and high incomes may qualify for low interest rates when taking out loans on behalf of their children. Below, you’ll find private student loan interest rates from several top-rated lenders.

Undergraduate student loan rates

Most private student loans require you to be a U.S. citizen or permanent resident to qualify. It’s possible for DACA recipients or international students to get student loans if they have an eligible cosigner. Remember that a cosigner may be required for any student with an insufficient credit history or income.

Here are undergraduate student loan rates from several private lenders:

| Company | Fixed | Variable | |

|---|---|---|---|

|

|

4.07% – 15.48% | 5.59% – 16.69% |

|

|

|

4.50% – 15.49% | 6.37% – 16.70% |

|

|

4.11% – 15.90% | 5.42% – 16.20% |

|

|

|

3.98% – 14.22% | 3.98% – 14.22% |

|

Graduate student loan rates

Graduate student loans can help you pay for graduate and professional degrees, including medical, law, veterinary, dental, and pharmacy school. Loan limits are often much higher than you could borrow with a federal Grad PLUS Loan.

Private lenders are less likely to require a cosigner for graduate students, though adding one may help borrowers qualify for a lower interest rate.

Here are graduate student loan rates from several private lenders:

| Company | Fixed | Variable | |

|---|---|---|---|

|

|

4.07% – 15.48% | 5.59% – 16.69% |

|

|

|

4.50% – 15.49% | 6.37% – 16.70% |

|

|

|

4.11% – 15.90% | 5.42% – 16.20% |

|

|

|

3.98% – 14.22% | 6.00% – 14.22% |

|

Parent student loan rates

Parents who want to pay for their child’s college education can take out a parent student loan. The loan can cover tuition, fees, room and board, and more. Parents must have a good credit score and a current source of income to qualify.

Many lenders do not offer student loans for parents. Instead, parents can cosign for a child, so they remain the primary borrower. Here are some lenders that offer parent student loans:

| Company | Fixed | Variable | |

|---|---|---|---|

|

|

4.07% – 15.48% | 5.59% – 16.69% |

|

|

|

4.11% – 15.90% | 5.42% – 16.20% |

|

|

|

3.98% – 14.22% | 6.00% – 14.22% |

|

Current student loan refinance interest rates

Refinancing your student loans is a smart option if you can qualify for a lower interest rate, which may help you pay less interest over the life of the loan. Interest rates for student loan refinancing are often lower than rates for private student loans because borrowers have an established credit history, presenting less risk to lenders.

Refinancing is only available through private lenders, not the federal government. Federal borrowers who refinance their loans with a private lender must give up benefits, including income-driven repayment plans, long forbearance options, and student loan forgiveness programs. A Direct Consolidation Loan preserves those benefits but won’t result in a lower interest rate.

Here are the student loan refinance rates from several lenders:

| Company | Fixed | Variable | |

|---|---|---|---|

|

|

5.19% – 9.74% | 5.99% – 9.74% |

|

|

|

5.48% – 8.69% | 5.28% – 8.99% |

|

How to calculate how much interest you will owe

Every month, the interest amount you owe on your loan is recalculated using a daily interest formula based on your total outstanding loan amount:

Total interest = outstanding principal balance x number of days since last payment x interest rate factor

The interest rate factor is your annual interest rate divided by the number of days in the year. Your loan servicer is responsible for billing you monthly and explaining how your payments are applied to the principal balance.

Here’s an example. Say you borrowed $30,000 at 6.00% with a 10-year repayment term.

- You’d first calculate your interest factor, which would look like this: 0.60/365 = 0.00016

- You’d then multiply your outstanding principal balance by the interest rate factor to determine how much interest accrues daily: $30,000 x 0.00016 = $4.80

- Next, you’d multiply the interest that accrues daily by the number of days since your last payment, which we’ll assume to be 30: $4.80 x 30 = $144

If you apply for forbearance or deferment or sign up for an income-driven repayment plan, your loans will accrue more interest over time, increasing the total interest paid.

Difference between variable and fixed rates

If you’re a student or a parent of a student taking out or refinancing a student loan, it helps to understand the different types of interest rate options that are available.

All federal student loans have fixed rates, meaning the rate won’t change during the loan term. Private student loans, including refinance loans, may have fixed or variable interest rates. Variable interest rates may increase or decrease during the loan term, which can change your monthly payments.

Here’s how the interest rate types compare:

| Fixed rates | Variable rates | |

| Monthly payments | ⌛ Permanent | 🔄 Subject to change |

| Rate change frequency | 🔒 No change after origination | 📅 Monthly, quarterly, or annually |

| Student loan types | 🏛 🏦 Federal and private | 🏦 Private |

Fixed interest rates

The interest rate you pay remains stable over the life of the loan so your monthly payments won’t change until the loan is paid off, forgiven, or refinanced.

Pros

-

Fixed monthly payments make it easier to budget.

-

Future rate increases won’t affect you.

-

Easily calculate the total cost of borrowing.

Cons

-

Fixed-rate loans may be higher than variable-rate loans.

-

Rates are locked, so you won’t benefit from future rate decreases.

Variable interest rates

Variable rates, which are only offered by private lenders, change over time based on a market rate, such as the LIBOR or the federal funds rate.

The new interest rate applies for the reset period, which can be a month, several months, or a year. For example, interest on a variable-rate student loan with a term length of 20 years with an annual reset period would be recalculated every year and applied for the following 12 months.

Rates might increase, decrease, or remain unchanged depending on economic conditions, the lender’s costs, and prevailing interest rates.

Pros

-

Initial rates could be lower than fixed-rate loans.

-

If rates remain low, you might save more in interest over the life of the loan.

-

Annual and lifetime rate caps can protect borrowers during periods of high inflation.

Cons

-

Budgeting may be challenging when payments are subject to change.

-

Rising rates could make your loan more expensive.

-

Rate caps can help, but they don’t always offer the same level of protection.

Student loan interest rates FAQ

What is interest?

Interest is a fee you pay to the lender in exchange for a loan, and lenders use interest proceeds to cover the cost of providing the loan. Loan interest rates may be fixed or variable, and the rate you pay may be based on your credit scores, income, and overall financial health.

What is a good fixed interest rate for a student loan?

The best fixed interest rate for student loans is the lowest rate you can qualify for. Federal and private student loan interest rates are influenced by the overall interest rate environment.

Federal interest rates don’t depend on the borrower’s credit score or income, while private interest rates consider those factors. It’s helpful to compare federal and private rates before taking out a loan to find the best fixed-rate option.

How does the interest rate affect the total cost of a loan?

The interest rate has a significant impact on the monthly payment and the total interest paid over the life of a student loan. For example, a $50,000 loan with a 4% interest rate and a 10-year term will cost $60,748 in total.

However, if that loan has an 8% interest rate and a 10-year term, the total cost will be $72,797. That’s why it’s crucial to choose the lowest interest rate possible.

How do you find a student loan with the lowest rate?

Finding a low interest rate on a student loan starts with comparing rates among lenders. Getting at least three rate quotes with no hard credit check required can give you a better idea of what you might qualify for.

Generally, the shortest repayment term available will result in a lower rate. Lenders may also offer better rates if you have a cosigner. And the lower the loan amount, the lower the interest rate is likely to be.

Many borrowers have a combination of private and federal loans. You might be able to get a low fixed rate with a federal loan, but if it only covers a portion of your tuition, you can explore private loans to cover the rest.

About our contributors

-

Written by Rebecca Lake, CEPF®

Written by Rebecca Lake, CEPF®Rebecca Lake is a certified educator in personal finance (CEPF®) and freelance writer specializing in finance.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.