Solar panels can lower your electric bill and increase your property value, all while having a positive impact on the environment.

You can fund your renewable energy upgrade with personal loans or home improvement loans to reduce out-of-pocket installation costs. We’ve weighed the pros and cons of every option to help you make your financing decision.

Table of Contents

Best lenders for solar panel loans

We evaluated lenders offering solar panel loans, and our selections are based on the features and service quality extended to customers. To help you identify which lenders may give you better approval odds, we’ve organized our recommendations by credit score.

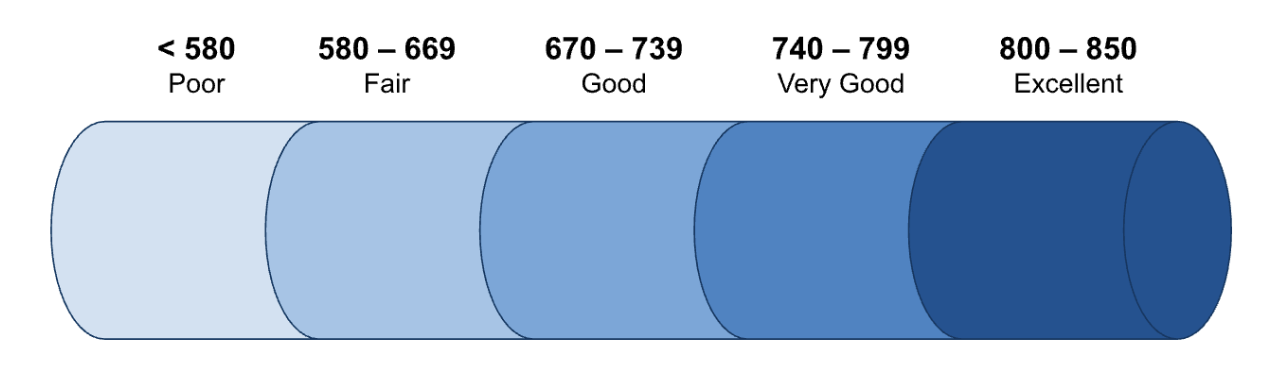

Lender may classify excellent, good, and fair credit differently, but you can use the FICO score ranges below to get an idea of where you stand:

To get a clearer idea of which lenders target credit profiles like yours, click the link below to jump to our review of each lender.

| Lender | Best for |

| LightStream | Excellent credit |

| SoFi | Good credit |

| Upgrade | Fair credit |

| Upstart | Little to no credit |

Best for excellent credit – LightStream

LendEDU rating: 4.8 out of 5

- Rate Beat program: Will beat competitors’ rates by 0.10 percentage points

- No fees

- Get funds as soon as the same business day

LightStream offers solar financing for homeowners with good to excellent credit. LightStream’s solar loan doesn’t require a certain amount of home equity or an appraisal, and you can use any excess funds for other home improvement projects.

In addition to fee-free borrowing, LightStream offers a 0.50% autopay rate discount. With no prepayment penalties and terms as long as 144 months, you can pay off your loan at a pace that works for you.

Best for good credit – SoFi

LendEDU rating: 5.0 out of 5

- No required fees

- Same-day funding

- Multiple rate discounts

SoFi offers unsecured home improvement loans, which you can use to finance solar panels. The process is fast and convenient: You don’t need to use your home as collateral or get an appraisal, and you can get loan funding as soon as the same day you apply.

The lender doesn’t require borrowers to pay origination fees, but you can choose to pay up to 7% at loan origination to lower your rate. However, you can save money by taking advantage of the 0.25% autopay interest rate discount and a 0.25% direct deposit rate discount. If you need to borrow from SoFi again, you may also get a 0.125% member rate discount.

Best for fair credit – Upgrade

LendEDU rating: 4.9 out of 5

- Credit health tools (free credit monitoring, credit score tracking, and personalized insights)

- Lower credit score requirements than many lenders

- Offers job loss protection and hardship programs

Upgrade offers personal loans for home improvement purposes, including purchasing and installing solar panels. While interest rates may be higher for borrowers with fair to bad credit, Upgrade considers scores down to 580.

Similar to other lenders, Upgrade’s approval process is fast and straightforward. Funds are generally available as soon as the next business day after approval. The company doesn’t charge prepayment penalties, but you’ll pay an origination fee of at least 1.85%.

Best for little to no credit – Upstart

LendEDU rating: 4.8 out of 5

- Minimum credit score is 300 (the lowest possible)

- Uses an AI-driven lending model to evaluate creditworthiness and offer personalized loan terms

- Generous 0.50% autopay discount

For borrowers with little to no credit history, Upstart’s unsecured home improvement loan could be a solid option to finance your solar panel installation. You don’t need to put up your home as collateral, and you can use the loan proceeds for other renovations or home repairs.

Although its origination and late fees are much higher than those of other lenders, Upstart allows a 15-day grace period for payments before charging a late fee. You may also be eligible to divide your monthly payment into two installments to better align with a biweekly pay schedule.

How to get the best solar loans

Getting a solar loan is similar to applying for personal loans. Here are the steps you should take:

Let’s examine these steps in more detail so you can best approach each stage of the process.

1. Shop around

Compare lenders to find the one that offers the best terms for your needs. Consider the following factors to help make your decision:

- Interest rates: Compare each loan’s annual percentage rate (APR), which considers your interest rate and any fees, calculated as an annual cost. Lower solar loan rates mean lower monthly payments, but they also tend to have stricter eligibility requirements.

- Loan amounts: Different lenders offer unique maximum loan amounts. When it comes to loans for solar systems, the amount you can apply and qualify for will depend on the estimated cost of the system, your credit score, and other factors.

- Loan repayment terms: The repayment term is the time it takes to repay the loan. Longer terms result in lower monthly payments, but they also come with higher interest costs.

- Fees: Be sure to check for any costs associated with the loan, such as origination fees, late payment fees, and prepayment penalties. These fees can add hundreds or thousands of dollars to your loan.

- Discounts: Some lenders offer interest rate discounts, such as autopay discounts or reduced rates, to set up qualifying direct deposits.

- Requirements: Some loans require collateral, home equity percentages, or appraisals. These can be time-consuming and difficult to qualify for, depending on your situation.

2. Prepare your documents

Once you’ve chosen a lender, ensure you have all the necessary documents to apply for the loan. This often includes:

- Proof of income: Pay stubs or tax returns

- Proof of identification: Driver’s license or passport

- Proof of address: Utility bills or mortgage statements

- Bank statements: These allow the lender to check your financial situation

For solar loans, you may also need to provide documents related to the solar panel installation, such as price quotes and contractor details.

3. Check your rates

You can (and should) prequalify for a loan to get an idea of what rates you may be offered. This requires a soft credit check, which won’t decrease your credit score.

Our experts recommend prequalifying with four to five lenders before you commit to a loan offer.

To prequalify, you only need to provide basic information, such as your name, address, and income. The lender will use this to determine whether you’re eligible and what loan terms you qualify for. However, prequalification does not guarantee you’ll get the loan, and failing to prequalify does not mean you won’t be able to get the loan if you apply.

4. Apply for the loan

You can apply for most loans online quickly. Processing your application could take a day to a week, and you may need to provide additional documents at this stage. The lender should notify you whether your application has been approved within a few days.

Once you are approved, your funds will be available within a few business days. Lenders that charge origination fees often subtract the fees from the loan amount they disburse, so the amount you receive may be less than you borrowed.

Alternatives to solar financing companies

If personal loans don’t seem like the right option, consider the following financing methods:

| Alternative | Consider if you… |

| Government loans | Are a veteran or have an FHA loan |

| Home equity loans and lines of credit | Don’t mind using your home as collateral |

| Solar panel leasing | Are cash-strapped or credit-challenged |

| Power purchase agreements (PPAs) | Can’t afford to buy but don’t want a lease |

| In-house financing | Won’t qualify with a traditional lender |

| Cash | Won’t max out your savings by purchasing outright |

Government loans for solar panels

Energy Efficient Mortgage Program (EEM)

In the United States, the Federal Housing Administration (FHA) offers an Energy Efficient Mortgage Program (EEM), allowing borrowers to finance energy-efficient home improvements, such as solar panels. You can add this “energy package” to your FHA loan amount.

Borrowers must meet specific eligibility requirements, and the loan amount is based on the expected energy savings of the improvements as identified by a qualifying home energy assessment. Loan amounts can also be calculated based on a percentage of house prices in the area or other value calculations.

Veterans Cash-Out Refinance Loan

The Department of Veteran Affairs (VA) offers a Cash-Out Refinance Loan. This loan allows veterans to refinance their VA mortgage and borrow a certain percentage of the home’s value for personal or home improvement needs, such as energy-efficiency upgrades.

Additional government resources

In addition to the two we mentioned above, other types of government loans may be available for solar panels, depending on the state you where live. The U.S. Office of Energy Efficiency and Renewable Energy has a comprehensive list of energy-related federal financial assistance programs.

Home equity-based solar loans for homeowners

Homeowners with sufficient home equity can take advantage of a home equity loan or line of credit (HELOC) to finance their solar panel installation. Home equity is your home’s value minus what you still owe on your mortgage.

Both types of loans allow you to borrow against the equity in your home, and they often come with lower interest rates than personal or home improvement loan options.

- A home equity loan provides you with a lump sum you must repay over a certain period.

- A HELOC works like a credit card and allows you to borrow up to a specific limit over a set period as you need it. Interest only accrues on the amount you borrow as you borrow it rather than on a large lump sum from the date of disbursement. You can withdraw funds from the line of credit during the draw period. In the repayment period, you must pay off any outstanding balance.

We’ve summarized the differences between a home equity loan and a HELOC below:

Solar panel leasing

Leasing may be a favorable option for those who don’t have the cash or credit to purchase solar panels. With a lease, you don’t need to pay upfront because you don’t own the solar panel system. Instead, you pay a monthly fee for a specific period, and the company that owns the panels is responsible for all repairs and maintenance.

Solar panel leasing often requires a long-term commitment—usually 20 to 25 years (the average “life” of a well-maintained solar panel). Because you’re not the owner, you’re also ineligible for any available tax credits or rebates that come with owning a solar panel system.

Power purchase agreements (PPAs)

A power purchase agreements (PPA) is a type of agreement between a homeowner and a solar energy provider in which the solar company installs, owns, and maintains the system. The homeowner then agrees to purchase the electricity the system produces at a predetermined rate.

This is similar to a solar panel lease, but the payment terms differ. With a PPA, you don’t pay a fixed monthly fee. Instead, you purchase the electricity generated at a lower rate than your current utility charges.

In-house financing from solar companies

Some solar energy companies offer in-house financing for their products. This may be a solid option for those with limited credit because in-house financing is often designed to make buying solar panels more accessible.

However, solar companies offering in-house financing may require you to purchase a specific model and charge higher interest rates than other financing options.

Such companies include SunPower, Blue Raven Solar, and ADT Solar.

Cash payments

If you have the funds, a cash payment is the most economical way to purchase solar panels. You’re not subject to interest payments or credit checks, and you may qualify for additional incentives, such as federal solar tax credits.

Keep in mind you may need to pay cash for additional equipment, installation, and maintenance, so be sure to factor that into your budget.

Solar panel costs and savings

Solar panel system and installation costs can be pricey, ranging from $14,000 to $40,000. It takes an average of eight to nine years to break even when it comes to energy savings versus initial installation costs. A high-interest loan or a longer loan term can increase the time it takes to recoup your investment.

What is the average cost to install solar panels?

According to Consumer Affairs, a 6-kilowatt (kW) solar panel system costs between $14,321 and $21,960 (before federal solar tax credits). Installation costs can vary from $14,000 for a small solar panel system to at least $40,000 for more complex and higher-tiered systems.

How can I calculate how long it will take to benefit from the savings solar panels offer?

The solar payback period refers to the time it takes to break even on your investment and benefit from your solar panel electricity savings.

- To calculate the solar payback period: Subtract the tax incentives or rebates from the total amount of installation. This is the total cost of your investment. Then, divide the total investment cost by your monthly electricity cost savings. This is the solar payback period in months.

- To calculate the monthly electricity/utility cost savings, Multiply the kilowatt-hour (kWh) of electricity you used from your solar panels by the utility’s billing rate per kWh. Even with solar panels installed, you’ll still get an electric bill, and you will need to subtract these fees from your cost savings. You can expect to be billed for mandatory utility fees, such as transmission and distribution fees.

On average, it takes between eight and nine years to recover the initial cost of solar. However, this can vary depending on individual circumstances, such as location and energy use.

How does interest affect the potential savings and time it takes to break even?

The longer you take to pay off the loan, the more interest you will pay. If you take several years to repay the loan, it will take longer for the solar panels to reach their breakeven point. If you have a high interest rate due to poor credit, your loan will accrue more interest and take longer to pay off and break even.

FAQ

What are the best solar loan rates?

Solar loan rates can vary from 6% to 36% (as of April 2024), depending on your credit and the type of loan you choose. To determine the best solar loan rates, get prequalified for various loans and compare the APRs.

HELOCs and home equity loans may offer the lowest rates, but they require you to use your house as collateral. Personal and home improvement loans may have higher rates but don’t have home equity or collateral requirements.

Can you get government loans for solar panels?

Yes, the Federal Housing Administration (FHA)’s Energy Efficient Mortgage Program (EEM) allows homeowners to get a loan to install solar panels. The Department of Veteran Affairs (VA) has a Cash-Out Refinance Loan that can be expanded to cover the cost of solar panels.

Some states also offer financing programs for solar installation. Check with your state government to see what options are available.

Can I get special solar loans for homeowners?

You can get a designated solar loan or use a home equity loan or HELOC. Because installing solar panels is considered a substantial home improvement, your home equity loan or HELOC interest may be tax-deductible.

Does it make sense to finance solar panels?

A solar loan may make financial sense for a borrower if the savings from using solar power outweigh the costs associated with financing. It’s essential to consider several factors, such as:

- Electricity rates

- Available solar incentives (i.e., tax benefits and rebates)

- Financing terms and rates

- The amount of energy the system produces

- Solar payback period

It’s also important to consider solar’s long-term potential. Electricity rates may rise, so a solar investment now could lead to more significant savings later.

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.