Getting a personal loan as an H-1B visa holder can be challenging, but it’s not impossible. Many lenders consider credit history, visa duration, and income stability when determining eligibility. While traditional banks may be hesitant, some online and specialty lenders offer options tailored to non-U.S. citizens.

This guide explains how to qualify for a personal loan as an H-1B visa holder, where to find lenders, and strategies to strengthen your application.

| Company | What to know | |

|---|---|---|

|

Total validity of immigration status must be at least 2 years |

|

|

Must be in the U.S. |

|

|

|

Only available in 11 states (listed below) |

|

|

|

0% interest loans; small amounts (up to $2,500) for specific purposes |

|

Can you get a personal loan as an H-1B visa holder?

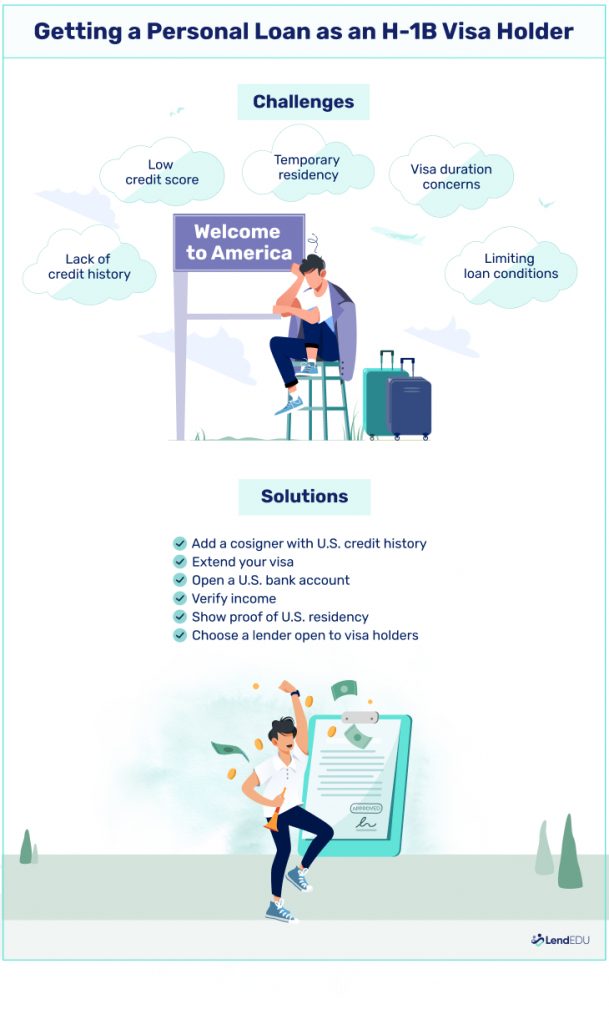

Yes, but it comes with challenges. Many lenders hesitate due to limited U.S. credit history and temporary visa status. Some also restrict loan use to immigration-related expenses.

To improve your chances of approval, be prepared to provide:

- Proof of income – Pay stubs, W-2s, or an employment letter

- U.S. address – Required for residency verification

- Visa documentation – Must show your visa lasts through the loan term

Some lenders specialize in loans for non-U.S. citizens, making it possible to secure financing even with these hurdles.

When choosing a personal loan lender as a visa holder, understand the fine print and repayment terms, and choose an amount that fits the budget. Next, identify the purpose for your loan, and research lenders that meet those needs.

Where to find personal loans in the USA for H1-B visa holders

We’ve found that traditional banks may have strict requirements, but certain online and specialty lenders offer loans to non-U.S. citizens with proof of income, residency, and a valid visa.

Below, we review lenders that provide personal loans to H-1B visa holders, outlining their key terms, eligibility requirements, and what makes them a good option. Whether you need a loan for moving expenses, education, or other financial needs, these reviews will help you compare your options and choose the best fit.

SoFi

Why SoFi is one of the best for H1B visa holders

SoFi offers personal loans available to non-permanent resident aliens, including H-1B visa holders. You can access the full range of loan amounts based on your financial history and current income and debt levels.

To be eligible, you must show that the total validity of your immigration status is at least two years.

| Fixed rates (APR) | 8.99% – 25.81% |

| Loan amounts | $5,000 – $100,000 |

| Repayment terms | 24 – 84 months |

Eligibility requirements

- Must be physically present in the U.S.

- Must have a U.S. address

- Available in all 50 states, plus Washington, D.C.

- Minimum credit score: 670

- Minimum income: You must be employed, have sufficient income from other sources, or have a job offer that starts within 90 days

- Immigration status must last at least two years

Upgrade

Why Upgrade is one of the best for H1B visa holders

Upgrade offers more flexible credit requirements—a minimum credit score of just 580—which can be helpful for H-1B visa holders with less established credit history. Funding times are fast, typically taking just a few days.

While not required, Upgrade recommends setting up autopay with a checking account, so you may want to open a checking account before you apply.

| Fixed rates (APR) | 8.49% – 35.99% |

| Loan amounts | $1,000 – $50,000 |

| Repayment terms | 24 – 84 months |

Eligibility requirements

- Must be physically present in the U.S.

- Available in all 50 states, plus Washington, D.C.

- Minimum credit score: 600

- Minimum income: Requires proof of monthly income

Capital Good Fund

Why it’s one of the best for H1B visa holders

Capital Good Fund is designed specifically to finance immigration-related expenses. You may use the loan funds to apply for a green card or citizenship or to petition family members to come to the U.S. You can also use the funds to pay immigration detention bonds.

Capital Good Fund is available in 11 states as of January 2025: Colorado, Connecticut, Delaware, Florida, Georgia, Illinois, Massachusetts, New Jersey, Pennsylvania, Rhode Island, and Texas.

| Fixed rates (APR) | 15.99% |

| Loan amounts | $1,501 – $20,000 |

| Repayment terms | 48 months |

Eligibility requirements

- Have a U.S. bank account in your name

- Have a U.S. address

- Available in Colorado, Connecticut, Delaware, Florida, Georgia, Illinois, Massachusetts, New Jersey, Pennsylvania, Rhode Island, and Texas

- Minimum income: Must have stable income

- Must have a referral form from a community agency or immigration attorney showing your proof of immigration eligibility

Mission Asset Fund (MAF)

Why it’s one of the best for H1B visa holders

MAF is another lender that offers opportunities for H-1B visa holders to apply for citizenship.

Its loan structures include credit building loans, business loans, and loans that cover the costs to apply for citizenship, adjustment of status or green card, or temporary protected status renewal. All loans are 0% interest.

| Rates (APR) | 0% |

| Loan amounts | $495 – $2,500 |

| Repayment terms | Not disclosed |

Eligibility requirements

- Loans must be used for specific reasons [e.g., Citizenship ($760); adjustment of status for green card ($1,440); Temporary Protective Status Renewal ($600)]

- Must be eligible to file with United States Citizenship and Immigration Services for citizenship financing

- Must complete financial education courses

- Must have a checking account for autopay

How to strengthen your personal loan application

Knowing which lenders can provide personal loans to you as an H-1B visa holder is the first step in securing the right loan for your financing needs. However, you can take other steps to improve your ability to get approval from lenders.

- Establish credit in the U.S.: Most lenders require a credit score in the U.S. unless you’re applying for immigration-specific personal loans.

- Add a co-applicant: Having a U.S. citizen as a cosigner or co-applicant can help you get approved for a personal loan.

- Extend your visa: H-1B visas are initially issued for three years and can be extended by an additional three years. Maximizing your allowable time in the U.S. may help you qualify for a personal loan.

- Verify income: Many lenders want to see consistent income. Documentation includes W-2s or a few months of bank statements.

- Open a U.S. bank account: Having a bank account in the U.S. makes it easy to get loan funds. Some lenders either require automatic payments or offer a rate discount for automatic withdrawal of funds each month.

What if your personal loan application is denied?

If you have a hard time getting approved for a personal loan as an H-1B visa holder, here are alternatives and solutions to consider.

- Add rent or utility payments to your credit report (if you’re denied due to credit history)

- Add a U.S.-based co-applicant or cosigner (if you’re denied due to credit history)

- Renew your visa up to the six-year maximum (if you’re denied because of the amount of time left on your H-1B visa)

- Focus on shorter loan terms that finish before you’re scheduled to leave the country (if you’re denied because of the amount of time left on your H-1B visa)

- Consider a cash advance app: If you have a regular income and a U.S. bank account and just need to borrow a few hundred dollars, apps such as EarnIn (our highest-rated cash advance provider) might be better than personal loans. This is especially true if you were denied due to your credit history: Many of the best cash advance apps don’t require credit checks for approval.

If you are denied a personal loan, consider borrowing funds from a trusted friend or family member or delaying the need for funds and building up savings. If the need is urgent and there are no other options, consider applying for a credit card, but be sure to understand the payment terms.

FAQ

Can I get a personal loan without a Social Security number?

Yes, you can get a personal loan without a Social Security number. Instead, you can apply with an Individual Tax Identification Number (ITIN). The IRS can obtain an ITIN for both residents and non-residents.

What happens to my personal loan if my visa expires or I move out of the country?

You are still responsible for repaying the funds regardless of visa status or residency changes. While it may be difficult for a lender to enforce repayment when you’re in another country, they may outsource the collection process if the home country’s laws allow it.

You’ll also have a poor credit history and may face additional consequences if you ever decide to return to the U.S.

Can a personal loan help me build U.S. credit history?

Yes; as long as you make on-time monthly payments, a personal loan can help you build your U.S. credit history as an H-1B visa holder.

Adding an installment loan in addition to a credit card (or even instead of one) also helps create a diverse mix of credit on your report and tends to be viewed more favorably than revolving credit.

How we chose the best personal loans in the USA for H1B holders

Since 2017, LendEDU has evaluated personal loan companies to help readers find the best personal loans. Our latest analysis reviewed 1,029 data points from 49 lenders and financial institutions, with 21 data points collected from each. This information is gathered from company websites, online applications, public disclosures, customer reviews, and direct communication with company representatives.

These star ratings help us determine which companies are best for different situations. We don’t believe two companies can be the best for the same purpose, so we only show each best-for designation once.

Recap of the best personal loans for H1B visas

| Company | What to know | |

|---|---|---|

|

|

Total validity of immigration status must be at least 2 years |

|

|

|

Must be in the U.S. |

|

|

|

Only available in 11 states (listed below) |

|

|

|

0% interest loans; small amounts (up to $2,500) for specific purposes |

|

About our contributors

-

Written by Lauren Ward

Written by Lauren WardLauren Ward is a personal finance writer who regularly covers topics like mortgages, real estate, tax relief, home equity, business loans, and investing.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.