Personal loans offer maximum flexibility, but borrowing money costs money. The interest rate, loan terms, and fees impact how much you pay for the loan. Total interest charges—how much interest you pay throughout the repayment term—are usually the best indicator of the overall cost.

With those factors in mind, here’s how to find the cheapest personal loan from a reputable lender.

Table of Contents

What are cheap personal loans?

Your goal is to find the cheapest loan from a reputable lender. But here’s where it can get confusing—different factors impact the cost of a loan. Before you start reviewing offers, make sure you understand the following terms.

- APR: The interest rate is how much you pay to borrow money. It’s usually a percentage of the loan. The APR is the interest rate plus additional fees. If your loan has fees, the APR is higher than the interest rate.

- Fees: Some lenders charge additional fees, usually a percentage of the loan amount and deducted from the loan. Origination fees and application fees are the most common for personal loans. Some lenders do not charge fees, especially for applicants with solid credit.

- Length of repayment term: The repayment term is how long you repay the loan. Most personal loans have terms from 24 to 72 months.

- Total interest charges: The total loan cost includes interest charges, fees, and term length. It’s the most straightforward metric to use when comparing loan offers.

You also need to know how each factor affects the total cost of the loan. For example, the total cost of the loan increases with a longer repayment term, but the monthly payment decreases.

A lower monthly payment might be tempting—and in some cases, it’s worth the extra cost—but it’s not the best indicator of the overall cost. That’s why it’s essential to look at the total interest charges.

Here’s how each factor impacts the price of borrowing money.

| Factor | Impact on total cost | Tips to lower costs |

| APR | Higher rates cost more money | Check if you qualify for rate discounts, like autopay. |

| Fees | Increases the cost | Search for lenders with no fees or ask to negotiate fees. |

| Length of repayment term | Longer terms cost more money | Pick the shortest repayment term you can afford. |

There are general guidelines for getting a cheap personal loan, but it’s still essential to review the details of each offer. Here’s an example of the difference a slightly higher interest rate and a slightly lower origination fee can make in the overall cost of two example loans.

| Detail | 1 | 2 |

| Loan amount | $10,000 | $10,000 |

| Repayment term | 36 months | 36 months |

| Origination fee | 1% | 0.5% |

| Interest rate | 10% | 11% |

| APR | 10.69% | 11.35% |

| Total loan cost | $1,716.19 | $1,835.94 |

Where to find the cheapest personal loan

Loan marketplaces allow borrowers to compare offers from multiple lenders in one place, including offers from central banks, online lenders, and credit unions. The main perk is getting preapproved with multiple lenders at once. It simplifies the loan process and makes it easier to compare.

Reviewing offers from a marketplace requires a soft credit pull, which won’t impact your credit score. However, you must input personal information—including your Social Security number—to view the offers. Those requirements are standard for preapproval but might seem jarring if it’s your first time.

How you plan to use the loan can impact your loan offers and interest rate. For example, you might have a higher interest rate if the loan is for a significant expense.

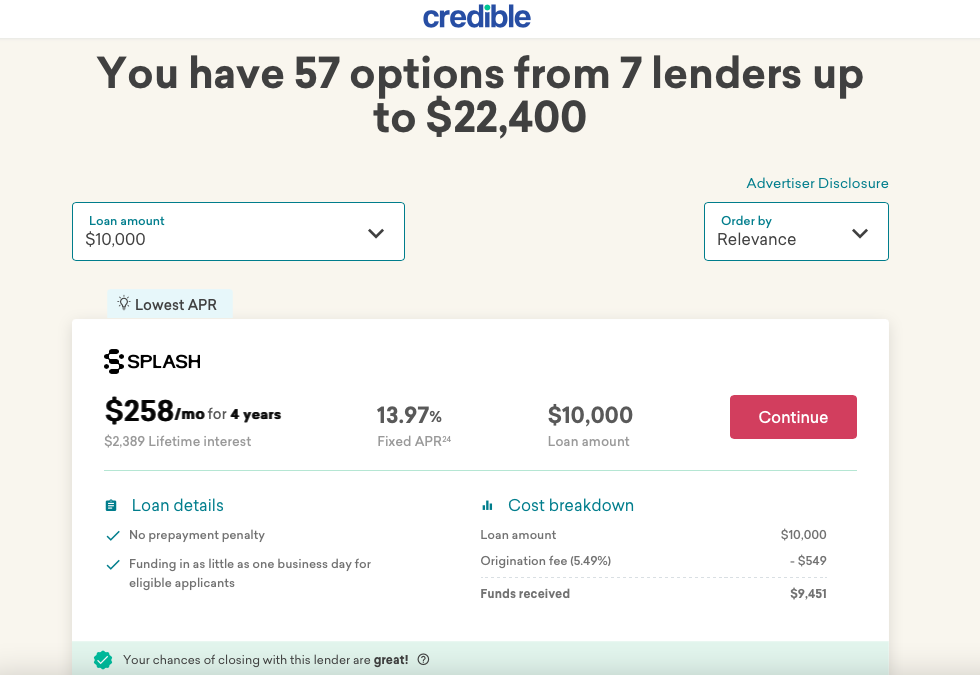

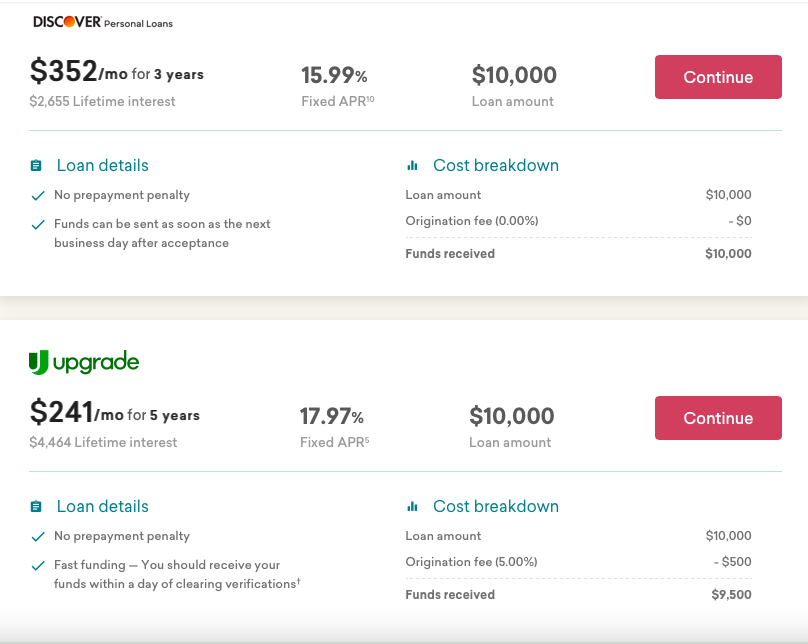

Here’s what the loan marketplace results look like on Credible.

Most marketplaces, including Credible, do not organize the results by loan terms, so different term lengths are mixed. For example, the results below have a loan with a three-year term right above a loan with a five-year term.

The loan offers usually include the loan’s monthly cost, fixed APR, origination fee, and term length. You can use those numbers to calculate the total cost with a personal loan calculator, making it easier to accurately compare loan offers.

| Marketplace | Rates (APR) | LendEDU rating |

| Credible | 7.49% – 35.99% | 4.9/5 |

Credible: Best marketplace

LendEDU rating: 4.9 out of 5

- 17 lender partners

- Does not sell personal data to third parties

Credible partners with lenders, including SoFi, PenFed, LightStream, Upstart, Avant, and LendingClub. It offers a wide range of personal loan options for debt consolidation, home improvement, medical expenses, and more, with loan amounts ranging from $1,000 to $200,000.

Known for its user-friendly interface, Credible quickly compares personalized prequalified rates from its partner lenders without affecting the user’s credit score due to the initial soft credit pull. Credible has strong security measures to protect user information and does not sell personal data to third parties.

We also like Credible’s commitment to helping its users find the best rate. Close with a better rate than you prequalify for on Credible and get a $200 gift card. Terms Apply. It offers the ability to add a cosigner to improve loan terms and provides various loan products beyond personal loans, including student loans and mortgage refinancing.

What has the biggest effect on how cheap a personal loan is?

Different factors impact the loan cost, including some that don’t have to do with the loan offer.

- Credit score: Your credit score provides a snapshot of your history as a lender. Borrowers use your credit score as an indicator of whether or not you’re a responsible borrower. It’s one of the most significant factors that impact your loan rates and terms.

- Loan purpose: How you plan to use the money from the personal loan impacts your loan rates and terms. Lenders might charge more if you use the funds for expenses like travel instead of debt consolidation or home renovations.

- Loan amount: Larger loans usually have higher interest rates because the loans are riskier for the lender. To offset the risk, lenders might charge more for a larger loan.

How to know you’ve found the cheapest personal loan

The total cost of the loan is the most effective way to determine that you’ve found the cheapest loan. Loan marketplaces don’t break down the total cost of the loan, so you have to complete a few extra steps to calculate the price.

The good news is that you don’t need to compare countless offers to get a good deal. Reviewing offers from three to five lenders is usually enough.

As you search for the cheapest personal loan, balance the cost with your financial reality. For example, you might save a few hundred dollars by choosing a shorter term length. But it’s not worth it if you can no longer afford the monthly payments.

Just as important as the financials involved, it’s important to understand your credit score before you start applying for personal loans! Reviewing your credit for any possible errors or incorrect information can mean a big difference in your credit score and, thus, your rate!

Eric Kirste, CFP®

How to get a cheaper personal loan

If you’re not happy with your loan offers, you can take steps to get a lower rate. Here’s what to do to get a cheaper rate for your loan.

- Improve your credit score: Your credit score is one of the biggest factors impacting your loan offers and interest rates. Borrowers with higher scores typically pay less for loans because they qualify for better rates. Take steps to improve your credit score by paying off debt, asking for a higher credit limit, and paying your bills on time.

- Check your credit report: You can review your credit report at AnnualCreditReport.com. Check for errors, overdue bills, or delinquent accounts that you might not know about. If you find anything that seems out of place, you can report it to your bank and the credit bureaus.

- Add a cosigner: Some lenders allow borrowers to add a cosigner responsible for repaying the loan if you cannot. A qualified cosigner with a higher credit score or income can help you get a better loan offer. Most borrowers ask a close friend or family member.

- Increase your income: A higher income indicates that you have more room in your budget for the payment and can afford the loan. You can increase your income by getting a raise, switching jobs, or starting a side gig.

About our contributors

-

Written by Taylor Milam-Samuel

Written by Taylor Milam-SamuelTaylor Milam-Samuel is a personal finance writer and credentialed educator who is passionate about helping people take control of their finances and create a life they love. When she's not researching financial terms and conditions, she can be found in the classroom teaching.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Eric Kirste, CFP®

Reviewed by Eric Kirste, CFP®Eric Kirste, CFP®, CIMA®, AIF®, is a founding principal wealth manager for Savvy Wealth. Eric brings more than two decades of wealth management experience working with clients, families, and their businesses, and serving in different leadership capacities.