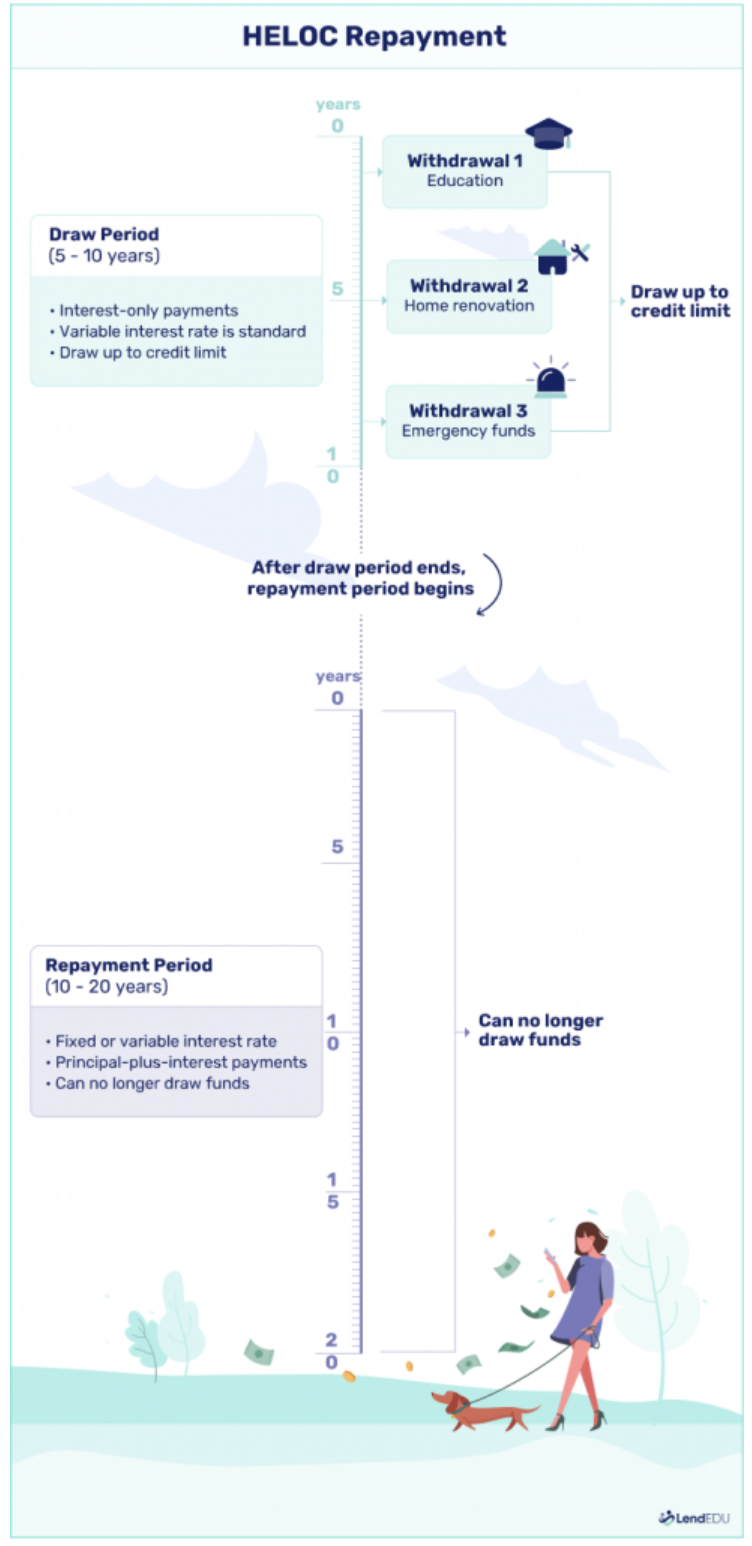

A HELOC—or home equity line of credit—is a way for homeowners to tap into their home equity, and borrow up to a certain limit. The two phases of a HELOC are the draw period and the repayment period. The draw period is the time when you can keep borrowing as much as you want up to the loan limit. You may be responsible for part of your loan until this period ends.

If you’re considering a HELOC, it’s critical to understand how the draw period works. Use this guide to learn what it can mean for your budget now, and when the draw period is over.

Table of Contents

- What is a draw period on a HELOC?

- HELOC draw period vs. repayment period: What’s the difference?

- How does the draw period work?

- How much money can I access during the draw period?

- Are there any requirements or restrictions during the draw period?

- Is the repayment amount the same throughout the draw period?

- Can you repay a HELOC during the draw period?

- Do lenders offer HELOCs with different draw periods?

- How to maximize your HELOC draw period

- What to do at the end of your draw period

What is a draw period on a HELOC?

When you get approved for a HELOC, you can access a line of credit and draw from it as needed (much like a credit card) for a certain period. This “draw period” lasts two to 10 years in most cases, but it depends on your lender.

Once the draw period on your HELOC expires, you can no longer withdraw funds. You will then enter the repayment period, which is when you begin repaying the amount you borrowed—plus interest—to the lender.

The end of the draw period is called the HELOC’s maturity date.

HELOC draw period vs. repayment period: What’s the difference?

At its simplest, the draw period is when you can use your HELOC funds, and the repayment period is when you pay that money back.

In the draw period, most lenders require interest-only payments—meaning you’ll only pay the interest on what you’ve withdrawn. In the repayment period, you’ll make payments toward both the interest and the principal balance.

Here’s a look at the key differences between these phases:

| Draw period | Repayment period | |

| Length | 2 – 20 years | 5 – 30 years |

| Can withdraw funds? | Yes | No |

| Payment requirements | Interest-only | Interest + principal |

| Interest rate | Usually variable, but some lenders may offer fixed rates | Usually variable, but some lenders may offer fixed rates or allow you to convert to a fixed rate during repayment |

How does the draw period work?

During the draw period, you can use your HELOC much like a credit card, withdrawing funds from your account up to your maximum credit limit. This differs from other home equity products, which often offer a lump-sum payment upfront.

Here’s an example of how that might work if you had a $50,000 HELOC with a 10-year draw period:

- Year 1: Withdraw $10,000 to cover roof repairs.

- Year 2: Withdraw $2,000 to cover a medical bill.

- Year 7: Withdraw another $20,000 to buy a car.

In the example above, you would withdraw $32,000 of your available $50,000 during the draw period. With HELOCs, you only pay interest on what you borrow, so limiting your withdrawals to what’s necessary can help keep your long-term costs in check.

Most lenders require interest-only payments during the draw period, so you’ll just cover the interest on what you’ve spent thus far.

Using the above example, here’s how the interest payments would work if your HELOC had an 8% annual interest rate:

- Year 1: At $10,000, you’ll pay $66.66 in interest each month.

- Year 2: Now that your balance is $12,000, your monthly interest payments are now $80.

- Year 7: At a total of $32,000, you’ll pay $213.33 in interest-only payments.

You can pay extra toward your principal balance to reduce your long-term interest costs. This will also give you the option to withdraw more later because the amount you repay goes back toward your available credit, similar to a credit card.

How much money can I access during the draw period?

Your HELOC limit depends on your equity, home value, and personal financial situation, including your debt-to-income ratio (DTI) and credit score. Many lenders will allow you to borrow up to 80% of your home value minus the balance on your mortgage and other loans against the property, including the HELOC you want to borrow. This percentage is your combined loan-to-value ratio (CLTV).

Lenders will first use your loan-to-value ratio (LTV) to calculate how much you can borrow. The LTV only includes the primary mortgage you have on your home.

Take a look at the example below to see how lenders work out the amount you can borrow:

| Detail | Amount |

| Home value | $400,000 |

| Outstanding mortgage | $200,000 |

| Max LTV (80%) | $320,000 |

In this case, HELOC lenders might only let you borrow up to $320,000 in combined loans. Because you have an outstanding mortgage of $200,000, your HELOC with most lenders might be limited to $120,000. Keep in mind you might not qualify for this full amount. Your credit score and other factors also influence what you can borrow.

Are there any requirements or restrictions during the draw period?

Many lenders have rules and restrictions during the draw period. For example, you may need to make an initial withdrawal as soon as you open your HELOC, or the lender might set minimum amounts every time you want to withdraw. For example, Figure and Aven are HELOC lenders requiring you to withdraw your full loan amount immediately.

Borrowers must pay interest on the amount they withdraw but can make principal payments to replenish the credit line and borrow more. Some lenders may charge annual fees, and in some cases, you may be limited to a maximum number of draws.

Is the repayment amount the same throughout the draw period?

During the draw period, most lenders only require interest payments, so these will fluctuate based on how much of your credit limit you’ve spent. Once you enter the repayment period, payments will depend on your balance, your interest rate, and whether you have a fixed or variable rate. In other words, your payments will go up during the repayment period because you’re paying back the amount you borrowed and the interest charged.

If you have a variable rate, your interest rate will change as often as every month based on the index rate it’s tied to. For example, if your HELOC is tied to the prime rate, and the prime rate increases, your HELOC rate will increase too, along with your payments.

Your monthly statements should detail whether your interest rate is changing and your next payment amount.

Can you repay a HELOC during the draw period?

You’ll need to cover any interest you owe on your balance during the draw period, but you can pay more if you want. Doing so can reduce long-term interest costs and help you pay off your balance faster. It can also replenish your HELOC credit line, allowing you to borrow more later.

You can even pay off your full HELOC balance. You only need to repay the principal balance (plus any interest you owe), not the full line of credit. If you’re considering this, read the fine print first. Some lenders charge prepayment penalties, so you may owe extra fees if you pay off the entire balance within a certain period.

Find out more about repaying your HELOC during the draw period.

Do lenders offer HELOCs with different draw periods?

HELOCs vary by lender, so some may offer shorter or longer draw periods. They also might have different withdrawal limits and fees, so be sure to compare your options before deciding on a company.

If you know you’ll need access to funds for many years, you might choose a HELOC with a 15-year or 20-year draw period rather than 10 years. Longer withdrawal periods also might be wise if you intend to cover a recurring cost, such as college tuition or renovations that will take several years.

Here’s a look at how HELOC draw periods vary by lender:

| Lender | Draw period | Repayment period |

| Figure | 2 – 5 years | 5 – 30 years |

| Aven | 5 years | 5, 10, 15, or 30 years |

| Citizens Bank | 10 years | 15 years |

| FourLeaf FCU | 10 years | 20 years |

| PenFed | 10 years | 20 years |

| Truist | 10 years | 5 – 30 years |

Check out our guide to the best HELOC lenders to start comparing options.

How to maximize your HELOC draw period

The HELOC draw period is your opportunity to borrow what you need. By being strategic about this time, you can maximize your HELOC’s benefits. Here are some ways you can make the most of your draw period:

- Make a plan: Decide what you want to use your HELOC for, and plan strategically. Are you looking to borrow what you need while making home renovations? Or are you looking to borrow smaller amounts over time to help your child pay for college? Knowing the reason you want a HELOC will help you to know how much and when to make withdrawals.

- Assess your budget: Although you’re only required to make interest-only payments, this amount can change the more you borrow. Be sure to map out your budget to see what you can afford before you make additional withdrawals.

- Consider making principal payments: It’s possible to borrow more than the HELOC limit as long as you make payments toward the principal amount. If you want to go this route, make sure to budget carefully so you can pay back the principal amount and additional interest payments.

What to do at the end of your draw period

Once your draw period ends, you’ll enter the repayment period. In most cases, your lender will notify you, usually around six months before your draw period ends. Be sure to check to see what your monthly payments are during this time so you can budget in advance.

If your HELOC has a variable rate, be sure to ask the lender when you’ll be notified if rates (and therefore your monthly payments) change. You can also consider refinancing or converting to a fixed-rate loan so you have more predictable monthly payments. However, refinancing can come with additional fees, so be sure to consider your options.

About our contributors

-

Written by Sarah Li Cain

Written by Sarah Li CainSarah Li Cain, AFC®, is a finance writer with more than 10 years of experience in consumer financial products, mortgages, banking, and insurance. She also works with brands to launch and produce podcasts.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.