Student loans make higher education accessible to thousands of students. Still, you should approach student loans with the same prudence you would any other form of debt.

Whether you’re mapping out your college plans or managing student loans, we’ll help you chart a path forward. Keep reading to learn how much debt is too much—and how to keep your student loan debt to a minimum.

Table of Contents

The rule of thumb for student loan debt

You’ve likely heard the advice to borrow only what you need. But there’s another way to gauge how much student debt you can handle postgraduation: Your total loan balance shouldn’t exceed your anticipated starting salary.

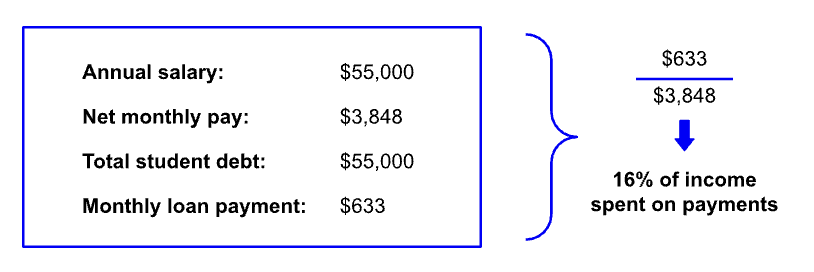

Say you forecast your first-year salary to be around $55,000. According to this rule, you should graduate with $55,000 or less in student loans.

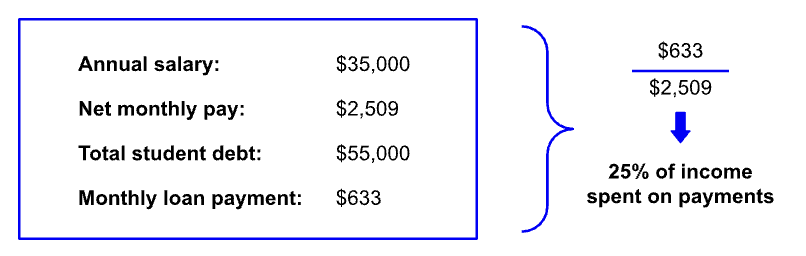

To better illustrate why this rule is important, imagine your starting salary will be around $35,000—but you still have $55,000 in student loan debt.

When you earned the same as your cumulative balance, your monthly loan payments were around 16% of your monthly income. Now that your student loan balance exceeds your salary by $20,000, your loan payments eat up 25% of your take-home pay.

You might wonder why you should limit your student loans to my first-year salary because you plan to make more than that eventually. And you’re right: With most careers, your salary should increase as you gain experience.

But the risk is that those salary increases won’t keep pace with inflation. You also can’t predict the twists and turns your life will take after you graduate.

Maybe you’ll move to a city with a higher cost of living. Perhaps you’ll start a family. Your student loan payments may not change in response to those developments, but your disposable income sure will.

Carrying student loan debt doesn’t just affect your budget. Become a better-informed borrower, and learn more about the true impact of student loans.

By capping your student loans based on your projected early-career earnings, you give yourself an insurance policy of sorts. If you can afford your loan payments when you’re just starting out, your payments should remain manageable when you’re making more.

Your school’s career services department can help you determine how much you’ll likely make after finishing your degree—the maximum you should borrow in student loans. You can also use the National Association of Colleges and Employers (NACE) Salary Survey.

Here’s a quick look at the average starting salaries across several majors as of 2023:

| Field/major | Avg. starting salary |

| Secondary education | $44,900 |

| English literature | $50,000 |

| Psychology | $54,500 |

| Communications | $59,000 |

| Human resources | $60,000 |

| Environmental science | $62,000 |

| Political science | $62,250 |

| Finance | $64,000 |

| Physics | $72,500 |

| Computer science | $74,000 |

| Chemical engineering | $75,000 |

If you anticipate needing more in student loans than your predicted salary can accommodate, consider adding a minor in a more lucrative field.

As long as this doesn’t substantially increase your tuition—say, if coursework toward your minor counts as electives for your major—you could increase the likelihood that you’ll earn more straight out of college.

Your debt may be unmanageable if your budget or cash flow doesn’t leave space for discretionary spending, other forms of debt begin to accumulate to help make ends meet, and savings for future life or financial goals is not an option due to servicing your debt payments.

Erin Kinkade, CFP®

What to do when your student debt is too much

In some cases, taking on student loans that exceed your starting pay is unavoidable. If you’re having trouble making payments on your loans, you still have options. These depend on whether you have federal or private student loans.

Take a brief look at your possible courses of action in the following table. Then we’ll explain them in more detail below.

| Option | Federal or private loans? | Best for |

| Income-driven repayment (IDR) | Federal | Lowering payment amount |

| Consolidation | Federal | Combining loans into one payment |

| Refinance | Private | Good-credit borrowers |

Keep reading for more about federal loans, or jump to our section on private student loans.

If you have federal student loans

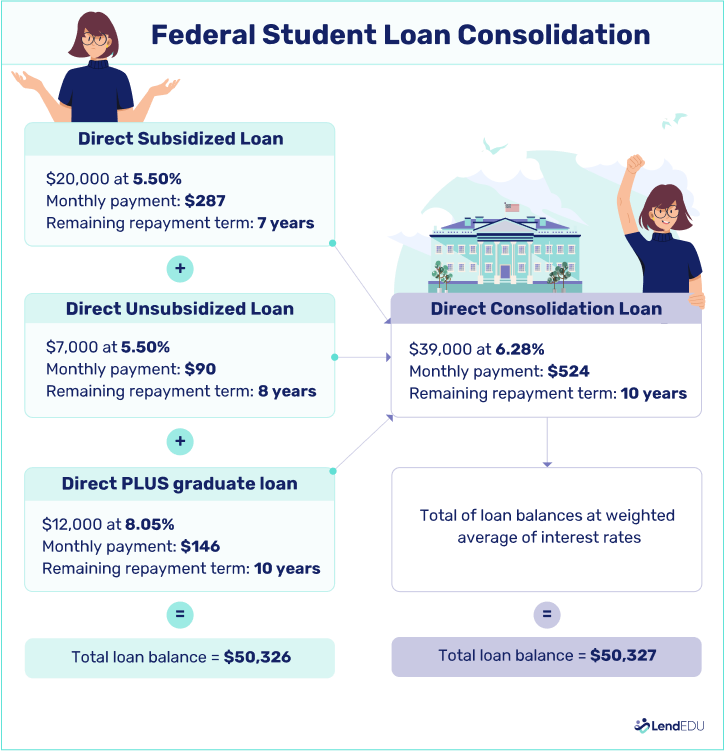

To get back on track with federal student loans, two popular solutions include IDR plans and loan consolidation.

IDR plans rework your payments around your disposable income, reducing the amount you owe each month. Consolidation merges multiple student loans into one Direct Consolidation Loan, like this:

You can enroll in either option with a quick online application. Applying doesn’t involve a credit check, but you must meet eligibility requirements. For example, if your loans are in default, you won’t qualify for an IDR plan on its own, but you could still take advantage of loan consolidation.

Along those lines, when you apply for loan consolidation, you can sign up for an IDR plan at the same time—even if your loans are in default. If you opt for an IDR plan, you can choose from one of four available arrangements:

- Saving on a Valuable Education (SAVE) Plan

- Pay as You Earn (PAYE) Repayment Plan

- Income-Based Repayment (IBR) Plan

- Income-Contingent Repayment (ICR) Plan

You can also elect to have your loan servicer enroll you in the plan with the lowest monthly payment.

Are IDR plans and loan consolidation not a good fit? Consider extended or graduated repayment instead. These plans aren’t always eligible for forgiveness, but they can still help you stay on top of your student debt.

If you have private student loans

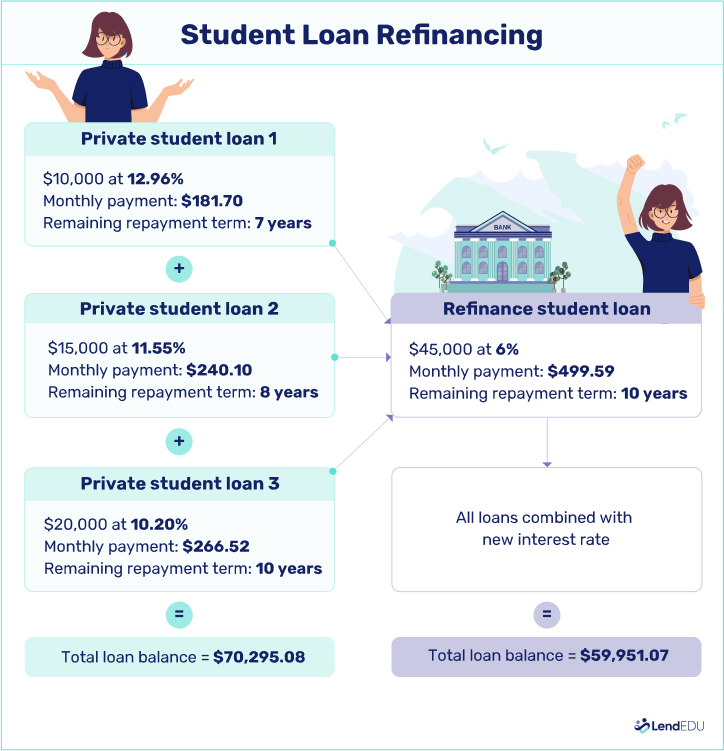

If you have private student loans, refinancing could be a smart solution. Like federal loan consolidation, refinancing lets you replace your student loans with one new loan:

You’ll sometimes hear “refinancing” and “consolidation” used interchangeably, but these are important differences between the two routes to repayment:

- Refinancing private loans requires a credit check.

- Refinanced loans don’t come with the same benefits and protections as consolidated federal loans.

Private student loans aren’t eligible for federal repayment or forgiveness programs anyway. If you only have private loans, you won’t necessarily lose anything by refinancing. These are the potential benefits:

- You could lower your interest rate.

- Your monthly payments could drop.

- You can choose a different lender if you’re dissatisfied with your current one.

- You can apply with or remove a cosigner, depending on your needs.

These advantages add up to an improved borrower experience—plus the opportunity for serious savings over time.

Keep in mind that refinancing essentially restarts your loan term. Refinancing may not be worth it if you can’t secure a lower rate.

Consider applying for forbearance if you can’t pay anything toward your loans. Most federal loans and some private lenders offer this temporary relief when borrowers face financial hardship.

If you have federal and private student loans

You may be one of many borrowers with a combination of federal and private student loans. If that’s the case, you can mix and match these repayment options to suit your situation.

You might, for example, refinance your private loans while enrolling in an IDR plan for your federal debt. Your student loan solution doesn’t have to be all or nothing—and oftentimes, it’s best if it’s not.

Say you decide to refinance your student loans. You’ll forfeit federal forgiveness and repayment options if you roll all your federal and private loans into one payment. There’s no way to undo that, so it’s usually best to keep your federal and private loans separate if you can.

How to avoid taking on too much student loan debt

If you’re still in school or haven’t yet started your degree, take action now so you can minimize how much you borrow later. Here are a few tips to help you stick to the rule of thumb:

- Fill out the FAFSA, and exhaust your free financial aid options first.

- Look for outside grants and scholarships.

- Choose—or transfer to—a college with more affordable tuition.

- Find a part-time job or paid internship.

- Compare on- and off-campus living costs, and opt for the least expensive choice.

- Make payments toward your accrued loan interest while in school.

- Start your degree at a community college.

- Take free dual enrollment and Advanced Placement courses.

- Split expenses with roommates or friends.

You can get as creative as you like here. Instead of going out to dinner, for instance, host a potluck in your dorm’s common area. Rather than commuting to campus individually, you and your friends can carpool to save on gas (and cut back on the time spent looking for parking).

Prioritize roles related to your field of study. You can put any extra income toward your loans—and gaining relevant experience before you graduate could translate to a higher salary when you do.

You could even study abroad in a country with a lower cost of living. It may sound extreme, but you’ll get school credit and experience a new culture, all while keeping more money in your pocket.

There’s also nothing wrong with taking a break from your studies. Giving yourself time to save isn’t the same as giving up. After all, no matter how you approach your student debt, every step you take toward responsible borrowing is a win.

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.