Americans have roughly $1.75 trillion in outstanding student loan debt. While that figure has plateaued over the past couple of years, it remains one of the largest financial obligations behind only mortgage and auto loans.

As a result, the financial burden can be significant, both for individual borrowers and the nation’s economy. Here’s a closer look at how student debt can affect your life—and what you can do to limit that impact.

Table of Contents

What is the impact of student loan debt on the economy and borrowers?

Student loan borrowers often face significant financial challenges due to their student loan debt.

The total amount Americans owe has nearly tripled since the start of the Great Recession in 2007, the student loan debt crisis has also swept the country’s economy. Here’s a quick summary of what you need to know.

Student loan debt economic impact

Economists generally view student loan programs as an investment in American workers and a necessity for remaining competitive in the global economy.

However, college costs have outpaced general inflation over the past two decades. During that same period, the wage premium—the difference in earnings between bachelor’s degree recipients and high school graduates—has stagnated. Here are some of the results.

Reduced consumer spending

Consumer spending drives more than two-thirds of the nation’s gross domestic product, making it by far the largest driver of economic growth.

As student loan payments continue to increase, consumers have less collective disposable income, which could result in sagging profits for corporations and small businesses, as well as less sales tax revenue for states.

Fewer small businesses

Small businesses are considered the backbone of the U.S. economy, making up 99.9% of all American businesses, according to the U.S. Small Business Administration.

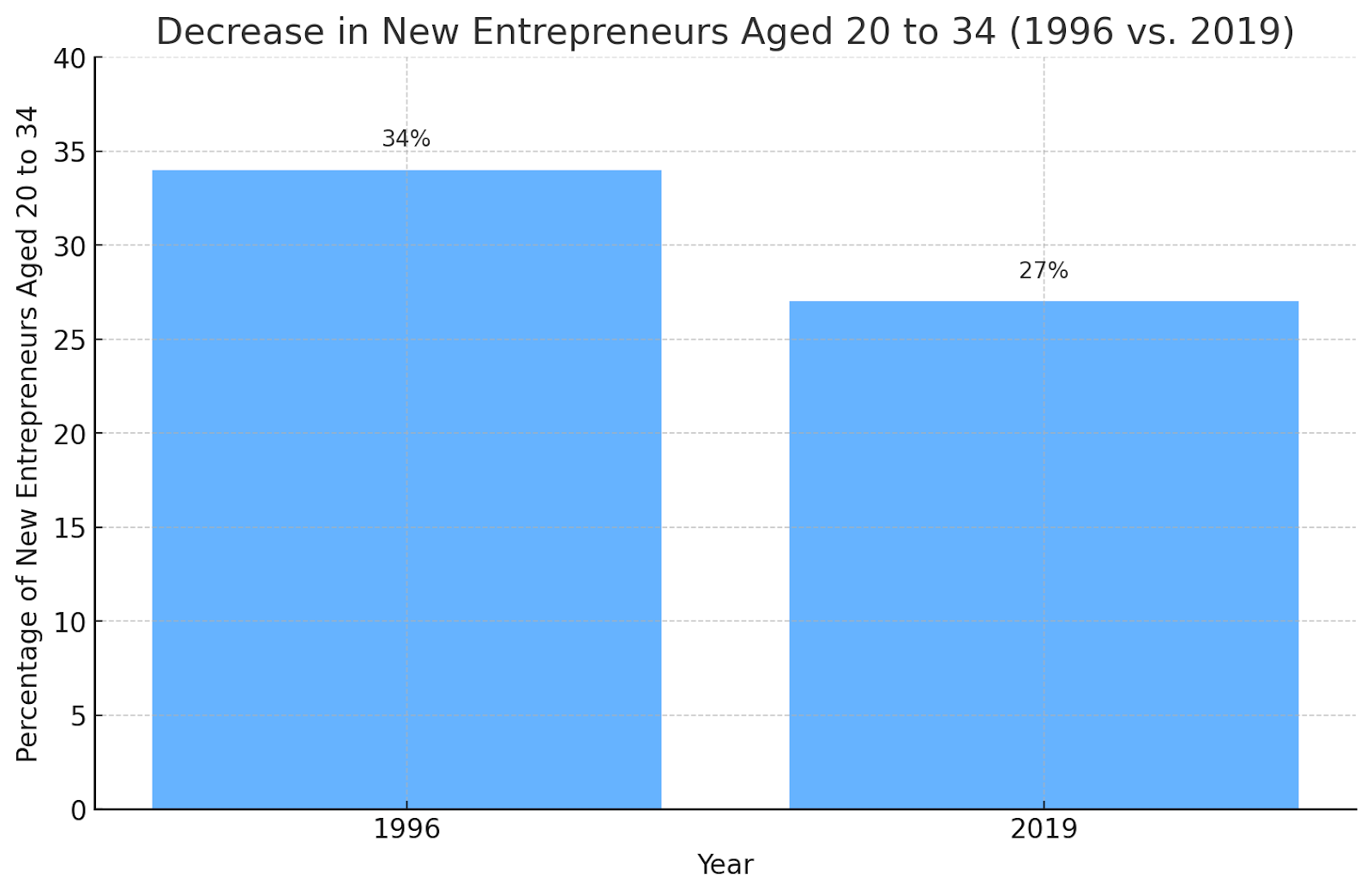

However, the burden of student loan debt has resulted in fewer young entrepreneurs, ultimately because the risk of failure is higher for student loan borrowers. In a 2020 study, the Ewing Marion Kauffman Foundation found that the share of new entrepreneurs aged 20 to 34 dropped from 34% to 27% between 1996 and 2019.

Lower rates of homeownership

The homeownership rate in the U.S. reached 69.2% in 2004 and currently sits at 65.6%, according to the Federal Reserve Bank of St. Louis. In particular, student loan borrowers struggle to buy a home.

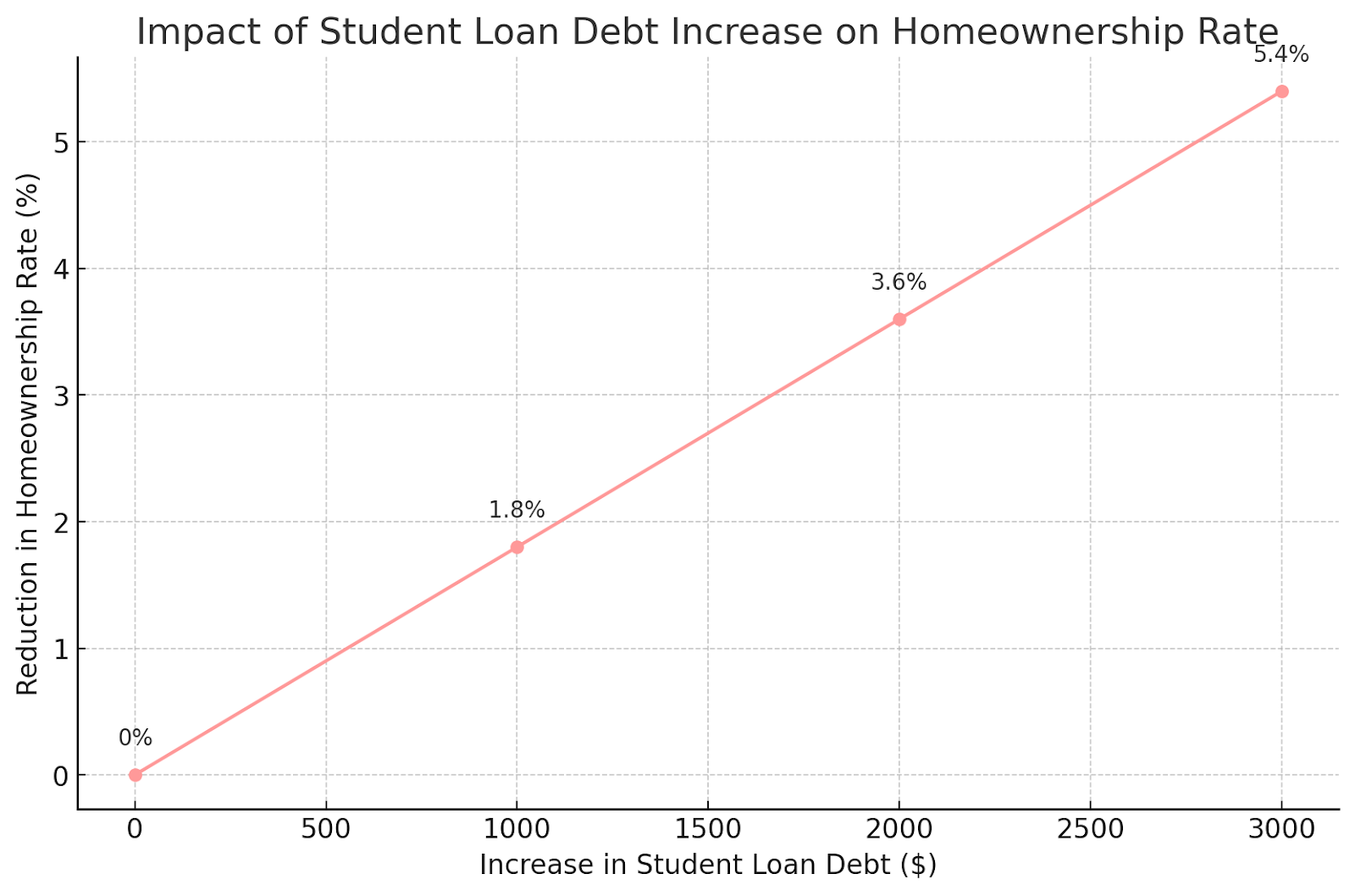

In fact, one study found that a $1,000 increase in student loan debt reduces the homeownership rate by 1.8% for borrowers in their mid-20s.

With less competition, real estate investors have aggressively pursued single-family homes, driving home and rent prices to record levels and making homeownership even more unattainable for some.

The student loan payment pause boosted the economy

According to researchers at the University of Chicago Booth School of Business, the student loan payment moratorium that lasted three-and-a-half years during the COVID-19 pandemic bolstered the economy by increasing short-term consumer spending.

Borrowers who benefited from the pause saved an average of $138 monthly. While they ultimately took on more of other types of consumer debt (primarily mortgage loans), that only resulted in an extra $20 in monthly payments.

What are the negative effects of student loan debt on students?

Individual borrowers have faced financial and mental challenges related to their student loan balances, much of which trickles up to the broader economy. What’s more, low-wage workers and disadvantaged communities are disproportionately affected by the burden of student debt.

Less savings

Student loan payments can impact your ability to set aside money for emergency expenses, a down payment for a home or car and other financial goals.

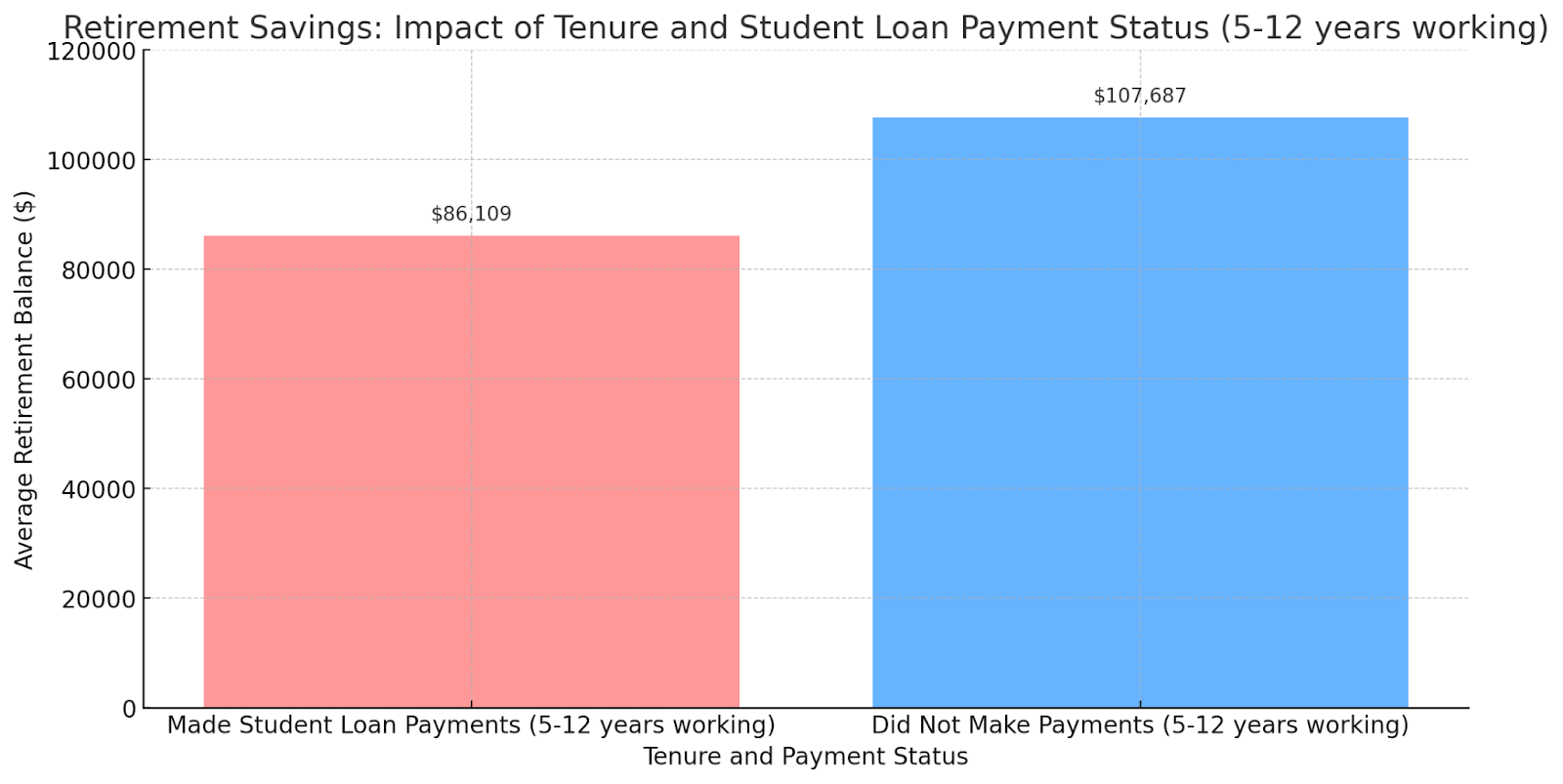

Most prominently, student loan debt can significantly impact retirement savings. In a recent study by the Employee Benefit Research Institute, the organization found that retirement account balances of student loan borrowers are as much as 26% lower compared to workers without student loan payments.

Less flexibility with career choices

Like many college graduates, student loan debt can significantly impact your career choices.

In a survey of Class of 2024 students, online recruiting platform Handshake found that 70% of graduates with student debt expect their debt to influence the jobs they consider. They’re also more likely to pursue gig work in addition to their full-time job to cover their payments.

Lower credit scores

Student loan borrowers are at a higher risk of delinquency on their debt and, as a result, tend to have a lower average credit score than non-borrowers.

According to data from FICO, student loan borrowers had an average credit score of 663 in January 2020, compared to 716 for consumers without student debt. During the Covid student loan payment pause, affected borrowers saw their FICO scores increase by 26 points compared to 9 points for other consumers.

Mental health challenges

Using social media posts, researchers at the University of Georgia found that student loan borrowers have high levels of depression, stress, fear, and other mental health issues as a result of their debt.

How does college debt affect the future life choices of students?

In a 2024 report by Lumina Foundation and Gallup, researchers found that 71% of student loan borrowers have delayed major life decisions due to their student debt, including returning to school, large purchases, marriage, and more.

Here’s a quick look at the results:

| Life event | Percentage delayed |

| Going back to school to finish a credential or degree | 35% |

| Buying a home | 29% |

| Buying a car | 28% |

| Moving out of your parents’ home | 22% |

| Starting your own business | 20% |

| Having children | 15% |

| Getting married | 13% |

The percentage of borrowers who have delayed a life event increases with student loan balances. Among those with less than $10,000 or less in debt, 63% delayed at least one major life event, but virtually all borrowers with $60,000 or more have been hindered.

Observations I have made regarding the long-term effects of student loan debt are clients transferring their student loan debt from provider to provider in search of the best rate (which is not a bad idea), but ideally, the focus should be on the pay-off plan. I have experienced individuals displaying guilty feelings trying to explain why their student loan amount is high and that it has been difficult to pay it off (thus leading them to get help to prepare a financial plan).

Erin Kinkade, CFP®

The younger individuals have chosen to forgo home buying and rent instead, which can lead to feelings of instability. Given these observations, I think a high student loan balance ultimately results in a loss of freedom.

How to limit the impact of student loan debt on your life

If you have student loans or plan to borrow for college, several strategies can help you minimize the impact of student debt. If you’re still in school, reduce your education costs by applying for more scholarships, choosing a less expensive program, or working during school to help pay tuition.

If you already have student debt, creating a budget is crucial. Tracking your spending can help you allocate more money toward paying off your loans, and setting up automatic payments ensures you never miss a due date. If you have federal student loans, explore repayment options such as income-driven plans or loan forgiveness, which can ease your financial burden.

If you’re struggling to manage your student loan debt, don’t hesitate to contact your loan servicer for assistance, and consider seeking support from friends or family.

Article sources

- Federal Reserve Bank of St. Louis, Student Loans Owned and Securitized (DISCONTINUED)

- U.S. Bank, How Does Consumer Spending Impact Economic Growth?

- U.S. Small Business Administration Office of Advocacy, FAQs

- Ewing Marion Kauffman Foundation, Student Loans and Entrepreneurship: An Overview

- Federal Reserve Bank of St. Louis, Homeownership Rate in the United States

- University of Chicago Press Journals, Student Loans and Homeownership

- Chicago Booth Review, Pausing Student-Loan Payments Boosted the Economy

- WorkRise, The Impact of Student Debt on the Low-Wage Workforce

- EBRI, Student Loans and Retirement Preparedness

- Handshake, The Class of 2024 Sets Their Sights on the Future

- FICO, Student Loan Borrowers at Risk of Delinquency When Payments Resume

- UGA Today, Student Loan Debt May Make Mental Health Issues Worse

- Lumina Foundation, Cost of College

About our contributors

-

Written by Ben Luthi

Written by Ben LuthiBen Luthi is a Salt Lake City-based freelance writer who specializes in a variety of personal finance and travel topics. He worked in banking, auto financing, insurance, and financial planning before becoming a full-time writer.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.