Most private lenders want a credit score in the mid-600s, and most students aren’t there yet. Fortunately, federal student loans without a credit check exist. There is a small group of private lenders that approve borrowers based on alternative criteria like academic performance, career potential, or a qualified cosigner. Below, you’ll find the best no-credit-check student loan options for 2026 and what you need to qualify.

If you’ve exhausted your federal aid options, the private lenders below offer paths to approval that go beyond your credit score.

Ascent Funding, LLC products are made available through Bank of Lake Mills or DR Bank, each Member FDIC. Subject to credit approval. Loan products may not be available in certain jurisdictions. Certain restrictions, limitations, terms and conditions may apply for Ascent‘s Terms and Conditions please visit AscentFunding.com/Ts&Cs. Annual Percentage Rates (APRs) displayed above are effective as of 06/01/2026 and reflect an Automatic Payment Discount (ACH). The ACH discount consists of 0.25% on credit-based college student loans submitted prior to 6/1/2025, a 0.5% discount for on credit-based college student loans submitted on or after 6/1/2025 and a 1.00% discount on outcomes-based loans when you enroll in automatic payments. Loans subject to individual approval, restrictions and conditions apply. Loan features and information advertised are intended for college student loans and are subject to change at any time. For more information, see repayment examples or review the Ascent Student Loans Terms and Conditions. The final amount approved depends on the borrower’s credit history, verifiable cost of attendance as certified by an eligible school and is subject to credit approval and verification of application information. Lowest interest rates require full principal and interest (Immediate) payments, the shortest loan term, a cosigner, and are only available for our most creditworthy applicants and cosigners with the highest average credit scores. Actual APR offered may be higher or lower than the examples above, based on the amount of time you spend in school and any grace period you have before repayment begins. Variable rates may increase after consummation.1% Cash Back Graduation Reward subject to terms and conditions. For details on Ascent borrower benefits, visit AscentFunding.com/

Ascent Funding, LLC products are made available through Bank of Lake Mills or DR Bank, each Member FDIC. Subject to credit approval. Loan products may not be available in certain jurisdictions. Certain restrictions, limitations, terms and conditions may apply for Ascent‘s Terms and Conditions please visit AscentFunding.com/Ts&Cs. Annual Percentage Rates (APRs) displayed above are effective as of 06/01/2026 and reflect an Automatic Payment Discount (ACH). The ACH discount consists of 0.25% on credit-based college student loans submitted prior to 6/1/2025, a 0.5% discount for on credit-based college student loans submitted on or after 6/1/2025 and a 1.00% discount on outcomes-based loans when you enroll in automatic payments. Loans subject to individual approval, restrictions and conditions apply. Loan features and information advertised are intended for college student loans and are subject to change at any time. For more information, see repayment examples or review the Ascent Student Loans Terms and Conditions. The final amount approved depends on the borrower’s credit history, verifiable cost of attendance as certified by an eligible school and is subject to credit approval and verification of application information. Lowest interest rates require full principal and interest (Immediate) payments, the shortest loan term, a cosigner, and are only available for our most creditworthy applicants and cosigners with the highest average credit scores. Actual APR offered may be higher or lower than the examples above, based on the amount of time you spend in school and any grace period you have before repayment begins. Variable rates may increase after consummation.1% Cash Back Graduation Reward subject to terms and conditions. For details on Ascent borrower benefits, visit AscentFunding.com/

Ascent Funding, LLC products are made available through Bank of Lake Mills or DR Bank, each Member FDIC. Subject to credit approval. Loan products may not be available in certain jurisdictions. Certain restrictions, limitations, terms and conditions may apply for Ascent‘s Terms and Conditions please visit AscentFunding.com/Ts&Cs. Annual Percentage Rates (APRs) displayed above are effective as of 06/01/2026 and reflect an Automatic Payment Discount (ACH). The ACH discount consists of 0.25% on credit-based college student loans submitted prior to 6/1/2025, a 0.5% discount for on credit-based college student loans submitted on or after 6/1/2025 and a 1.00% discount on outcomes-based loans when you enroll in automatic payments. Loans subject to individual approval, restrictions and conditions apply. Loan features and information advertised are intended for college student loans and are subject to change at any time. For more information, see repayment examples or review the Ascent Student Loans Terms and Conditions. The final amount approved depends on the borrower’s credit history, verifiable cost of attendance as certified by an eligible school and is subject to credit approval and verification of application information. Lowest interest rates require full principal and interest (Immediate) payments, the shortest loan term, a cosigner, and are only available for our most creditworthy applicants and cosigners with the highest average credit scores. Actual APR offered may be higher or lower than the examples above, based on the amount of time you spend in school and any grace period you have before repayment begins. Variable rates may increase after consummation.1% Cash Back Graduation Reward subject to terms and conditions. For details on Ascent borrower benefits, visit AscentFunding.com/

Key Takeaways

- Federal Direct Subsidized and Unsubsidized Loans don’t require a credit check.

- Most private lenders want a credit score in the mid-600s, and borrowers who fall short typically need a qualifying cosigner.

- A handful of private lenders approve based on academic performance or future earning potential instead of credit.

- No-credit-check private loans typically carry 8% to 14%+ APR, while adding a creditworthy cosigner can drop rates to 3% to 5%.

Table of Contents

- Key Takeaways

- Federal student loans without a credit check

- 3 best bad credit private student loan providers (no cosigner)

- How to compare low-credit and no-credit student loans

- What counts as bad credit for student loans?

- Pros and cons of bad credit private student loans

- How to qualify for student loans with no credit

- How to get emergency student loans with no credit check

- Repayment tips to build credit with student loans

- Straight from the experts

- FAQ: No-credit and low-credit student loans

- How we chose the best low-credit student loans

Federal student loans without a credit check

If you have no credit, federal student loans should almost always be your first option.

The US Department of Education offers Direct Loans to eligible graduate and undergraduate students, regardless of credit history. These loans include:

- Subsidized Direct Loans: These are available to undergraduates with demonstrated financial need, regardless of proof of income or credit score. Interest is subsidized for students while they’re still in school, during the repayment grace period, and if loans are put into deferment after graduation.

- Unsubsidized Direct Loans: Available to undergraduates and graduate or professional students. Income and credit score do not matter, nor does financial need for this type of loan. Interest is not subsidized and continues to accrue while in school.

Another type of federal loan, the PLUS loan, is available to graduate students and parents of dependent undergraduates. It requires a credit check, but borrowers with an adverse credit history can still qualify if they meet other requirements.

This quick 30-second video breaks down how federal student loans handle approval without a credit check and how private student loans compare.

Compare federal student loan credit check requirements

Here’s a quick glance at the types of federal student loans, who’s eligible, and whether they require a credit score. Check out our complete federal student loans guide for more information.

| Loan type | Eligible students | Credit check required? |

|---|---|---|

| Direct Subsidized | Undergrads with financial need | No |

| Direct Unsubsidized | Undergrads, grads, and professional students | No |

| Parent PLUS | Parents of dependent undergrads | Yes |

| Grad PLUS | Grad and professional students | Yes |

Compare federal student loan interest rates

Federal student loan rates are fixed and set the same for every borrower, regardless of credit. Here’s how current rates and fees compare across loan types for the 2025-26 school year.

| Loan Type | Fixed Interest Rate | Loan Fee |

| Direct Subsidized & Unsubsidized Loans (undergraduate) | 6.39% | 1.057% |

| Direct Unsubsidized Loans (graduate) | 7.94% | 1.057% |

| Direct PLUS Loans | 8.94% | 4.228% |

Rates apply to loans first disbursed between July 1, 2025 and June 30, 2026. Federal student loan rates are set annually by Congress. Source: studentaid.gov.

3 best bad credit private student loan providers (no cosigner)

What “no credit check” means here: These lenders don’t require you to have an established credit score to qualify. Some may still run a credit inquiry for identity verification or fraud prevention, but approval is based mainly on academic factors, your school/program, or future earning potential.

If you were denied a federal Parent PLUS or Grad PLUS loan because of a credit issue, or you’ve already used all your federal loan eligibility, private student loans might be your next option. But most private lenders require either you or a cosigner to have good credit, often a score in the mid-600s or higher. That can be a hurdle if you’re just starting out financially or if your cosigner doesn’t meet those standards either.

Wondering if you can get a student loan on your own? The video below explains whether a cosigner is required and what your options look like without one.

A few private lenders take a different approach.

- Some evaluate academic factors like your school, major, GPA, and expected graduation date to determine whether you’re likely to repay.

- Others focus on your future earning potential, especially if you’re studying in a high-demand field, rather than your current income or credit history.

- A few structure their loans more like income-share agreements (ISAs) or flat-fee repayment plans, where you repay based on your earnings after graduation.

These options can give you more flexibility and access, even if you don’t have a credit score or a qualifying cosigner.

Below are our top picks for no-credit-check student loans. While none of these lenders require a strong credit history for approval, some may still run a soft or hard credit inquiry during the process for verification or fraud prevention.

Don’t have a cosigner, or your cosigner’s credit didn’t qualify? Our guide to student loans without a cosigner covers more options for students in both situations.

1. Best low-credit student loans for graduates: Ascent

Why we picked it

Ascent is best for juniors and seniors who are looking for non-cosigned loans with deferred payments. It lets you prequalify without affecting your credit score. However, if you apply, Ascent will run a credit check to gauge your eligibility.

Juniors and seniors who don’t qualify for the credit-based loan can apply for Ascent’s Outcomes-Based Loan. You don’t need credit to qualify for this loan, just a solid academic record and a minimum 3.0 GPA.

- Autopay discount of up to 1%

- 1% Cash Back Back Graduation Reward

- Grace periods from 9 to 36 months, depending on the program and level of study

Loan details

| Rates (APR) | Varies |

| Loan amounts | $2,001 – 100% of certified costs |

| Repayment terms | 5, 7, 10, 12, 15, or 20 years |

| In-school repayment plans | Progressive, full, interest-only, $25 flat, or deferred |

| Enrollment | At least half-time |

| States | All 50 states, Washington, D.C., and Puerto Rico |

| Credit score | None required for Ascent’s Outcomes-Based Loan |

| Income | None required for Ascent’s Outcomes-Based Loan |

2. Best student loans with no credit for undergrads: Funding U

Why we picked it

Funding U is ideal for undergraduates with no credit and no eligible cosigner. Instead of using credit scores, it looks at your GPA, major, class year, and graduation timeline to decide if you’re likely to repay. It’s a strong option if you were denied a private loan due to limited credit or your cosigner didn’t qualify.

- Approval based on academic track record

- No cosigner required

- No fees or prepayment penalties

Loan details

| Rates (APR) | Varies |

| Loan amounts | $3,001 – $20,000 |

| Repayment terms | 5 or 10 years |

| In-school repayment plans | Full, interest-only, $20 flat |

| Enrollment | Full time at a four-year college |

| States | All except Alaska, Idaho, Kentucky, Maine, Mississippi, Montana, Nevada, New Hampshire, Rhode Island, and Wyoming |

| Credit score | None required |

| Income | No minimum |

3. Best student loans without credit history needed for international students: MPOWER

Why we picked it

MPOWER loans are the best student loans without credit history needed for international students and DACA recipients, but U.S. citizens can apply. MPOWER checks your credit history if available, but one is not required to apply. Instead, the company focuses on your future earning potential.

The company accepts any currency during repayment because loans are available to students from over 190 countries. No prepayment penalties apply if you pay off your loan early.

- Schools in the U.S. and Canada are eligible

- 0.25% autopay discount

- Free visa support letter and job board access

Loan details

| Rates (APR) | Varies |

| Loan amounts | $2,001 – $100,000 |

| Repayment terms | 10 years |

| In-school repayment plans | Full or interest-only |

| Enrollment | Undergrad or grad student within 2 years of graduation or about to begin a 1- or 2-year program |

| States | All 50 states |

| Credit score | None required |

| Income | No minimum |

How to compare low-credit and no-credit student loans

If you have bad credit, college loans can vary significantly from one lender to the next. A few details have a much bigger impact on your total cost and flexibility than others. Knowing what to look for before signing a loan agreement can save you real money.

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and fees. Even a one- or two-point difference in annual percentage rates can add hundreds of dollars to your repayment total on a $10,000 loan. Compare APR side by side, not the advertised rate, since that’s the number that reflects what you’ll actually pay.

- Cosigner Release: If you’re applying with a creditworthy cosigner, find out how quickly they can be removed from the loan. Release timelines vary widely, ranging from 12 to 48 on-time monthly payments, depending on the lender. A shorter release window gives your cosigner peace of mind and frees them from the financial obligation sooner.

- Repayment Flexibility: Ask whether the lender offers deferment options, forbearance, or graduation grace periods before you start repaying. A lender that builds in breathing room can help you avoid missed payments if your income takes time to ramp up.

Run these three criteria across every lender you’re considering before you commit. What looks like the best offer upfront isn’t always the most affordable one over time.

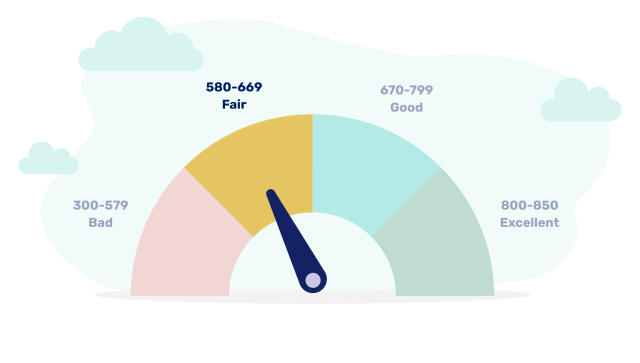

What counts as bad credit for student loans?

FICO credit scores range from 300 to 850. Anything below 670 is generally considered fair or poor. Most private student loan lenders want to see a score in the mid-600s or higher to approve an application without a cosigner. Many first-time borrowers have no credit history, which is different from bad credit but creates similar challenges with private lenders, since there’s no track record for them to evaluate.

| Credit Score Range | Category | What It Means for Student Loan Applicants |

| 300–579 | Poor | Most private lenders will decline the application or require a cosigner. |

| 580–669 | Fair | Some lenders may approve with a cosigner; rates will be higher. |

| 670+ | Good | Eligible for most private lenders; best rates available. |

What interest rates can you expect on student loans with bad credit?

Federal student loan rates are fixed and identical for all borrowers regardless of credit (see the rate table above). Private loan rates work differently:

- Without a cosigner: APRs typically range from 8% to 26%, depending on the lender and borrower profile.

- With a creditworthy cosigner: Rates can drop into the 3% to 5% range with some lenders.

- The cost gap: On a $20,000 loan, the difference between a cosigned and non-cosigned rate can add thousands of dollars to your total repayment.

Always prequalify with multiple lenders before applying. Most run a soft credit check that lets you see your actual rate without affecting your score.

Pros and cons of bad credit private student loans

Pros

- Access: Bad credit doesn’t automatically disqualify you from getting a private student loan.

- Approval flexibility: Some private lenders weigh academics or future earnings instead of credit.

- Credit building: On-time payments strengthen your credit profile over time.

- Gap coverage: Private loans can fill the shortfall when federal aid runs out.

Cons

- Cost: Private rates without a cosigner can reach 26% APR.

- Borrowing caps: Loan amounts are smaller without a creditworthy cosigner.

- Credit risk: Missed payments can damage your credit further.

- Fewer protections: Private loans lack income-driven repayment and PSLF.

How to qualify for student loans with no credit

If you’re applying for a student loan without strong credit, or without a cosigner, here’s what to expect and how to prepare:

- You may still need to verify identity and income. Even if lenders don’t use credit scores, they often request proof of enrollment, academic transcripts, or an estimated graduation date.

- Some lenders ask for your GPA or major. Academic standing or field of study may be used to evaluate your likelihood of repaying the loan.

- Be ready to share future plans. Lenders may ask for expected income after graduation or post-college employment goals.

- Expect limits on loan amounts. No-credit-check loans often come with lower borrowing caps than traditional loans with a cosigner.

- If you have a cosigner with low credit, proceed with caution. A weak cosigner may hurt your chances or result in worse loan terms. In many cases, applying on your own with a lender that doesn’t require a cosigner may be the better move.

- International or DACA students may need extra documentation. This could include a passport, visa, or proof of U.S. school enrollment.

How to get emergency student loans with no credit check

If you need fast funding and don’t have credit, start with options that move fastest, and don’t rely on private underwriting.

Here’s the smartest order of operations:

1. Contact your school’s financial aid office

Many colleges offer:

- Emergency grants

- Short-term institutional loans

- Tuition payment plans

- Hardship assistance programs

These options often require minimal documentation and may be faster than applying for a private loan.

2. Complete (or update) your FAFSA

Federal Direct Subsidized and Direct Unsubsidized Loans don’t require a credit check. If you haven’t used your full federal eligibility, this is typically the most affordable and reliable option.

3. Explore private lenders that don’t require established credit

If you’ve exhausted federal aid, lenders may approve you based on alternative factors.

Keep in mind that private student loans still require school certification, so they’re not designed for same-day cash emergencies.

If you need funds immediately for living expenses, your school’s emergency aid office is often your fastest path.

Repayment tips to build credit with student loans

No-credit-check student loans can help you pay for school, and they can help you build credit.

Most lenders report your payment history to the major credit bureaus. Making on-time payments consistently can strengthen your credit profile over time. Missing payments can hurt your score and make borrowing money in the future more expensive.

To maximize the benefit:

- Pay on time, every time. Payment history makes up 35% of your credit score.

- Use autopay if possible. Many lenders offer a small interest rate discount.

- Borrow only what you need. Keeping your balance manageable helps protect your credit and your budget.

- Know your cutoff times. Submit payments early so they post on time.

If you’re still building credit and learning how to improve your credit score, consider additional tools such as becoming an authorized user on a well-managed credit card or using a secured card responsibly.

Student loans affect your credit like any installment loan. Responsible repayment today can open the door to lower rates and better loan options in the future.

Straight from the experts

Federal student loan interest rates are the same for all borrowers and are set annually by Congress. This rate is fixed for the life of the loan. If you have a high credit score, you might qualify for the best interest rates with private loans. Sometimes, these rates can be lower than federal rates. Expect to pay a higher interest rate on a no-credit-check student loan.

If possible, look for ways to build credit early. Two easy ways to do this are to be added as an authorized user on a parent’s credit card (assuming they have good credit and make on-time payments) or to get a secured credit card. If you don’t have time to build your credit, consider federal student loans before no-credit-check private loans.

FAQ: No-credit and low-credit student loans

Can you get a student loan with a 500 credit score or no credit?

Yes. Federal Direct Subsidized and Direct Unsubsidized Loans do not require a credit check, making them accessible to students with no credit or a score as low as 500. Most private lenders want a FICO Score in the mid-600s, so qualifying with a 500 score typically requires a creditworthy cosigner. A few private lenders also approve borrowers based on academic performance or future earning potential instead of credit.

Do private student loans check your credit?

Most private student loan lenders perform a credit check during the application process. However, some lenders do not require a minimum credit score for approval. Instead, they evaluate factors such as GPA, major, graduation timeline, or projected earning potential. Even in these cases, a lender may run a soft or hard credit inquiry for identity verification.

Are there student loans for bad credit and no cosigner?

Yes, but your options are more limited. Federal student loans don’t require a cosigner or credit history. A small number of private lenders offer no-cosigner options and evaluate academic or career-related factors instead of traditional credit scores.

What is the lowest credit score for student loans?

Private student loan requirements vary by lender, but most want a score of at least 640, with mid-600s being the typical baseline for approval without a cosigner. Federal loans like Direct Subsidized and Unsubsidized are student loans no credit check is required for, so there’s effectively no minimum score floor.

Are “no credit check” student loans legit?

Yes, but it’s important to understand what that phrase means. Legitimate lenders may not require an established credit score for approval, but they still verify your identity, enrollment, and eligibility. Be cautious of lenders that promise guaranteed approval with no documentation, charge upfront fees, or pressure you to act immediately. Federal student loans and well-known private lenders are safe starting points.

What is the easiest student loan to get with bad credit?

Federal student loans are the easiest to qualify for with bad credit. Direct Subsidized and Unsubsidized Loans don’t require a credit check because they’re considered financial aid, making them accessible regardless of credit history. After exhausting federal options, some private lenders offer no-cosigner alternatives.

What’s the fastest way to get a student loan with no credit?

The fastest option is usually federal student loans through the FAFSA, provided you haven’t exhausted your eligibility. If you need immediate assistance, contact your school’s financial aid office about emergency grants or short-term institutional loans. Private lenders that don’t require established credit can be helpful, but they still require school certification and are not designed for same-day funding.

Can you be denied student loans because of bad credit?

Yes, but it depends on the loan type. Private lenders almost always run a credit check and can deny applications with poor credit or limited history. Federal Direct Subsidized and Unsubsidized Loans don’t require a credit check, so bad credit won’t disqualify you. PLUS loans are the exception, since they screen for adverse credit history.

Can a student loan help me build credit?

Yes, most student loan lenders report your payment history to the three major credit bureaus, so making every payment on time builds a positive credit record that can improve your score over time. Missing payments has the opposite effect and can pull your score down.

How we chose the best low-credit student loans

Our editorial team picks every lender featured here on its own merit. While partner compensation can affect where products appear on the page, it doesn’t shape our ratings or recommendations, and we refresh our lender reviews each year to keep the picks accurate.

LendEDU evaluates student loan lenders to help readers find the best student loans. Our latest analysis reviewed 725 data points from 25 lenders and financial institutions, with 29 data points collected from each. This information is gathered from company websites, online applications, public disclosures, customer reviews, and direct communication with company representatives.

These star ratings help us determine which companies are best for different situations. We don’t believe two companies can be the best for the same purpose, so we only show each best-for designation once.

Ascent Funding, LLC products are made available through Bank of Lake Mills or DR Bank, each Member FDIC. Subject to credit approval. Loan products may not be available in certain jurisdictions. Certain restrictions, limitations, terms and conditions may apply for Ascent‘s Terms and Conditions please visit AscentFunding.com/Ts&Cs. Annual Percentage Rates (APRs) displayed above are effective as of 06/01/2026 and reflect an Automatic Payment Discount (ACH). The ACH discount consists of 0.25% on credit-based college student loans submitted prior to 6/1/2025, a 0.5% discount for on credit-based college student loans submitted on or after 6/1/2025 and a 1.00% discount on outcomes-based loans when you enroll in automatic payments. Loans subject to individual approval, restrictions and conditions apply. Loan features and information advertised are intended for college student loans and are subject to change at any time. For more information, see repayment examples or review the Ascent Student Loans Terms and Conditions. The final amount approved depends on the borrower’s credit history, verifiable cost of attendance as certified by an eligible school and is subject to credit approval and verification of application information. Lowest interest rates require full principal and interest (Immediate) payments, the shortest loan term, a cosigner, and are only available for our most creditworthy applicants and cosigners with the highest average credit scores. Actual APR offered may be higher or lower than the examples above, based on the amount of time you spend in school and any grace period you have before repayment begins. Variable rates may increase after consummation.1% Cash Back Graduation Reward subject to terms and conditions. For details on Ascent borrower benefits, visit AscentFunding.com/

Ascent Funding, LLC products are made available through Bank of Lake Mills or DR Bank, each Member FDIC. Subject to credit approval. Loan products may not be available in certain jurisdictions. Certain restrictions, limitations, terms and conditions may apply for Ascent‘s Terms and Conditions please visit AscentFunding.com/Ts&Cs. Annual Percentage Rates (APRs) displayed above are effective as of 06/01/2026 and reflect an Automatic Payment Discount (ACH). The ACH discount consists of 0.25% on credit-based college student loans submitted prior to 6/1/2025, a 0.5% discount for on credit-based college student loans submitted on or after 6/1/2025 and a 1.00% discount on outcomes-based loans when you enroll in automatic payments. Loans subject to individual approval, restrictions and conditions apply. Loan features and information advertised are intended for college student loans and are subject to change at any time. For more information, see repayment examples or review the Ascent Student Loans Terms and Conditions. The final amount approved depends on the borrower’s credit history, verifiable cost of attendance as certified by an eligible school and is subject to credit approval and verification of application information. Lowest interest rates require full principal and interest (Immediate) payments, the shortest loan term, a cosigner, and are only available for our most creditworthy applicants and cosigners with the highest average credit scores. Actual APR offered may be higher or lower than the examples above, based on the amount of time you spend in school and any grace period you have before repayment begins. Variable rates may increase after consummation.1% Cash Back Graduation Reward subject to terms and conditions. For details on Ascent borrower benefits, visit AscentFunding.com/

Ascent Funding, LLC products are made available through Bank of Lake Mills or DR Bank, each Member FDIC. Subject to credit approval. Loan products may not be available in certain jurisdictions. Certain restrictions, limitations, terms and conditions may apply for Ascent‘s Terms and Conditions please visit AscentFunding.com/Ts&Cs. Annual Percentage Rates (APRs) displayed above are effective as of 06/01/2026 and reflect an Automatic Payment Discount (ACH). The ACH discount consists of 0.25% on credit-based college student loans submitted prior to 6/1/2025, a 0.5% discount for on credit-based college student loans submitted on or after 6/1/2025 and a 1.00% discount on outcomes-based loans when you enroll in automatic payments. Loans subject to individual approval, restrictions and conditions apply. Loan features and information advertised are intended for college student loans and are subject to change at any time. For more information, see repayment examples or review the Ascent Student Loans Terms and Conditions. The final amount approved depends on the borrower’s credit history, verifiable cost of attendance as certified by an eligible school and is subject to credit approval and verification of application information. Lowest interest rates require full principal and interest (Immediate) payments, the shortest loan term, a cosigner, and are only available for our most creditworthy applicants and cosigners with the highest average credit scores. Actual APR offered may be higher or lower than the examples above, based on the amount of time you spend in school and any grace period you have before repayment begins. Variable rates may increase after consummation.1% Cash Back Graduation Reward subject to terms and conditions. For details on Ascent borrower benefits, visit AscentFunding.com/

Related articles

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.