A college degree can fast-track you to a job with a higher salary, but like most things in life, you must spend money to make money. And when it comes to college, you might have to spend a lot of money. According to the Education Data Initiative’s report published in December 2024, the average cost of a single year of college in the United States is $38,270.

But that doesn’t mean you must give up hope on a college education.

In case you’ve exhausted your federal financial aid, school aid package, and scholarship opportunities, and are currently in need of funding for school, here’s our list of top-rated private student loan lenders: Best Private Student Loans: Reviewed and Ranked.

Below, we’ll explore how to pay for college with no money (and maybe without even taking on debt).

| Company | Fixed Rates (APR) | Variable Rates (APR) | Rating (0-5) |

|---|---|---|---|

|

Terms & Disclosures

Information advertised valid as of 07/20/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s). All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit. College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC |

5.59% – 16.99% | 3.99% – 15.89% |

Terms & Disclosures

Information advertised valid as of 07/20/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s). All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit. College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC |

|

Terms & Disclosures

Information advertised valid as of 7/24/2026 Borrow responsibly Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000. 1. Loan application must be submitted to see available rates. 2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal. 3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024. 4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment. 5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment. 6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered. 7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not. SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION. Sallie Mae loans are made by Sallie Mae Bank. |

5.59 – 16.99 | 3.87 – 16.50% |

Terms & Disclosures

Information advertised valid as of 7/24/2026 Borrow responsibly Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000. 1. Loan application must be submitted to see available rates. 2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal. 3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024. 4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment. 5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment. 6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered. 7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not. SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION. Sallie Mae loans are made by Sallie Mae Bank. |

Terms & Disclosures

Interest Rates Disclosure Actual rate and available repayment terms will vary based on your financial profile. Fixed annual percentage rates (APR) range from 2.69% to 16.74% (2.19% – 16.24% with Auto Pay and Loyalty discounts). Variable annual percentage rates (APR) range from 5.24% to 17.1% (4.74% – 16.6% with Auto Pay and Loyalty discounts). Earnest variable interest rate student loans are based on a publicly available index, the 30-day Average Secured Overnight Financing Rate (SOFR) published by the Federal Reserve Bank of New York. The variable rate is based on the rate published on the 25th day, or the next business day, of the preceding calendar month, rounded to the nearest hundredth of a percent plus a margin and will change on the 1st of each month. The rate will not increase more than once a month, but there is no limit on the amount that the rate could increase at one time. Our lowest rates are only available for our most credit qualified existing cosigned loan borrowers who receive the 0.25% Loyalty discount and requires selection of our shortest term offered, full principal and interest payment while in school, and enrollment in our 0.25% Auto Pay discount. Enrolling in Auto Pay is not required as a condition for approval. Interest rates are subject to change. Loyalty Discount To be eligible for the Loyalty Discount, applicants must have previously obtained an Earnest Private Student Loan and apply using the same email address associated with that loan. Only one Loyalty Discount may be applied per eligible Earnest Private Student Loan. Not all applicants may qualify. This offer cannot be combined with Earnest’s Rate Match program. Earnest may modify or discontinue this offer at any time and without notice, however, once a Loyalty Discount is earned, it will not be taken away. In-School Loans Disclosures

Earnest Private Student Loans are subject to credit approval. Before applying for private student loans, it’s best to maximize your other sources of financial aid first. It’s recommended to use a 3-step approach to assembling the funds you need: 1) Look for funds you don’t have to pay back, like scholarships, grants, and work-study opportunities. 2) Next, fill out a FAFSA® form to apply for federal student loans options. 3) Finally, consider a private student loan to cover any difference between your total cost of attendance and the amount not covered in steps 1 and 2. For more information, visit the Department of Education website at studentaid.gov.

Auto Pay Discount

You can take advantage of the Auto Pay interest rate reduction by setting up and maintaining active and automatic ACH withdrawal of your loan payment from a checking or savings account. The interest rate reduction for Auto Pay will be available only while your loan is enrolled in Auto Pay. Interest rate incentives for utilizing Auto Pay may not be combined with certain private student loan repayment programs that also offer an interest rate reduction. It is important to note that the 0.25% Auto Pay discount is not available when loan payments are deferred during the interim period as a result of selecting the deferred repayment option.

Cosigner Release

To qualify for automatic cosigner release, the outstanding principal balance of your loan must be paid down to 50% or less of the original principal balance. The primary borrower must have made 36 months of required payments after the end of the Interim Period. The primary borrower must meet our eligibility and minimum credit requirements. Additional terms and conditions may apply.

To request cosigner release, the primary borrower must have made 12 consecutive, monthly on-time principal and interest payments (or an amount equal thereto) immediately preceding the cosigner release application. The primary borrower must satisfy certain eligibility and credit criteria at the time of application. Additional terms and conditions may apply.

Grace Period

Nine-month grace period is not available for borrowers who choose our Principal and Interest Repayment plan while in school.

Loan Cost Examples

Available interest rates are subject to change. Interest rates as of 03/19/2026. Earnest’s Loan Cost Examples:

1.) These examples provide estimates based on principal and interest payments beginning immediately upon loan disbursement. Variable annual percentage rate (“”APR””): A $10,000 loan with a 15-year term (180 monthly payments of $152.84) and a 16.85% interest rate without Auto Pay (16.85% APR) would result in a total estimated payment amount of $27,511.20. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed APR: A $10,000 loan with a 15-year term (180 monthly payments of $150.30) and a 16.49% interest rate without Auto Pay (16.49% APR) would result in a total estimated payment amount of $27,054.10.

2.) These examples provide estimates based on interest-only payments while in school. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $152.84) and a 16.85% interest rate without Auto Pay (16.85% APR) would result in a total estimated payment amount of $35,515.14. For a variable loan, after your starting rate is set, your rate will then vary with the market. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $140.42 for 57 months. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $150.30) and a 16.49% interest rate without Auto Pay (16.49% APR) would result in a total estimated payment amount of $34,886.94. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $137.42 for 57 months.

3.) These examples provide estimates based on fixed $25 payments while in school. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $253.39) and a 16.85% interest rate without Auto Pay (14.92% APR) would result in a total estimated payment amount of $47,035.20. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $246.61) and a 16.49% interest rate without Auto Pay (14.65% APR) would result in a total estimated payment amount of $45,814.80. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $25.00.

4.) These examples provide estimates based on deferred payments. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $275.17) and a 16.85% interest rate without Auto Pay (14.67% APR) would result in a total estimated payment amount of $49,530.60. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $268.03) and a 16.49% interest rate without Auto Pay (14.39% APR) would result in a total estimated payment amount of $48,245.40. Your actual repayment terms may vary. Other repayment options are available. It is important to note that the 0.25% Auto Pay discount is not available when the deferred repayment option has been selected and the loan is in the interim period. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $0.

Loan Minimum

Residents of Hawaii must request a loan of at least $1,501.

Repayment Terms and Options

Repayment terms and repayment options available vary based on loan type.

Skip a Payment

Earnest clients may skip a payment through a single, one-month forbearance during a 12 month period. Your first request to skip a pay can be made once you’ve made at least 6 months of consecutive on-time full principal and interest payments, and your loan is in good standing. The interest accrued during the skipped month will result in an increase in your remaining minimum payment. The final payoff date on your loan will be extended by the length of the skipped payment periods. Any unpaid accrued interest may capitalize (added to the principal balance) at the end of the forbearance period by adding unpaid accrued interest to the outstanding principal as permitted by law and the terms of the loan agreement. Please note that skipping a payment is not guaranteed and is at Earnest’s discretion. Your monthly payment and total loan cost may increase as a result of postponing your payment and extending your term.

No Fees

Earnest does not charge fees for origination, late payments, returned check, or prepayments. Florida Stamp Tax: For Florida residents, Florida documentary stamp tax is required by law, calculated as $0.35 for each $100 (or portion thereof) of the principal loan amount, the amount of which is provided in the Final Disclosure. Lender will add the stamp tax to the principal loan amount. The full amount will be paid directly to the Florida Department of Revenue. Certificate of Registration No. 78-8016373916-1.

Earnest Private Student Loans are made by FinWise Bank, Member FDIC. FinWise Bank, 756 East Winchester, Suite 100, Murray, UT 84107. Earnest student loans are serviced by Earnest Operations LLC, 300 Frank H. Ogawa Plaza, Suite 340, Oakland, CA 94612. NMLS #1204917, with support from Higher Education Loan Authority of the State of Missouri (MOHELA) (NMLS# 1442770). FinWise Bank and Earnest LLC and its subsidiaries, including Earnest Operations LLC, are not sponsored by agencies of the United States of America. |

5.59% – 16.99% | 3.99% – 16.85% |

Terms & Disclosures

Interest Rates Disclosure Actual rate and available repayment terms will vary based on your financial profile. Fixed annual percentage rates (APR) range from 2.69% to 16.74% (2.19% – 16.24% with Auto Pay and Loyalty discounts). Variable annual percentage rates (APR) range from 5.24% to 17.1% (4.74% – 16.6% with Auto Pay and Loyalty discounts). Earnest variable interest rate student loans are based on a publicly available index, the 30-day Average Secured Overnight Financing Rate (SOFR) published by the Federal Reserve Bank of New York. The variable rate is based on the rate published on the 25th day, or the next business day, of the preceding calendar month, rounded to the nearest hundredth of a percent plus a margin and will change on the 1st of each month. The rate will not increase more than once a month, but there is no limit on the amount that the rate could increase at one time. Our lowest rates are only available for our most credit qualified existing cosigned loan borrowers who receive the 0.25% Loyalty discount and requires selection of our shortest term offered, full principal and interest payment while in school, and enrollment in our 0.25% Auto Pay discount. Enrolling in Auto Pay is not required as a condition for approval. Interest rates are subject to change. Loyalty Discount To be eligible for the Loyalty Discount, applicants must have previously obtained an Earnest Private Student Loan and apply using the same email address associated with that loan. Only one Loyalty Discount may be applied per eligible Earnest Private Student Loan. Not all applicants may qualify. This offer cannot be combined with Earnest’s Rate Match program. Earnest may modify or discontinue this offer at any time and without notice, however, once a Loyalty Discount is earned, it will not be taken away. In-School Loans Disclosures

Earnest Private Student Loans are subject to credit approval. Before applying for private student loans, it’s best to maximize your other sources of financial aid first. It’s recommended to use a 3-step approach to assembling the funds you need: 1) Look for funds you don’t have to pay back, like scholarships, grants, and work-study opportunities. 2) Next, fill out a FAFSA® form to apply for federal student loans options. 3) Finally, consider a private student loan to cover any difference between your total cost of attendance and the amount not covered in steps 1 and 2. For more information, visit the Department of Education website at studentaid.gov.

Auto Pay Discount

You can take advantage of the Auto Pay interest rate reduction by setting up and maintaining active and automatic ACH withdrawal of your loan payment from a checking or savings account. The interest rate reduction for Auto Pay will be available only while your loan is enrolled in Auto Pay. Interest rate incentives for utilizing Auto Pay may not be combined with certain private student loan repayment programs that also offer an interest rate reduction. It is important to note that the 0.25% Auto Pay discount is not available when loan payments are deferred during the interim period as a result of selecting the deferred repayment option.

Cosigner Release

To qualify for automatic cosigner release, the outstanding principal balance of your loan must be paid down to 50% or less of the original principal balance. The primary borrower must have made 36 months of required payments after the end of the Interim Period. The primary borrower must meet our eligibility and minimum credit requirements. Additional terms and conditions may apply.

To request cosigner release, the primary borrower must have made 12 consecutive, monthly on-time principal and interest payments (or an amount equal thereto) immediately preceding the cosigner release application. The primary borrower must satisfy certain eligibility and credit criteria at the time of application. Additional terms and conditions may apply.

Grace Period

Nine-month grace period is not available for borrowers who choose our Principal and Interest Repayment plan while in school.

Loan Cost Examples

Available interest rates are subject to change. Interest rates as of 03/19/2026. Earnest’s Loan Cost Examples:

1.) These examples provide estimates based on principal and interest payments beginning immediately upon loan disbursement. Variable annual percentage rate (“”APR””): A $10,000 loan with a 15-year term (180 monthly payments of $152.84) and a 16.85% interest rate without Auto Pay (16.85% APR) would result in a total estimated payment amount of $27,511.20. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed APR: A $10,000 loan with a 15-year term (180 monthly payments of $150.30) and a 16.49% interest rate without Auto Pay (16.49% APR) would result in a total estimated payment amount of $27,054.10.

2.) These examples provide estimates based on interest-only payments while in school. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $152.84) and a 16.85% interest rate without Auto Pay (16.85% APR) would result in a total estimated payment amount of $35,515.14. For a variable loan, after your starting rate is set, your rate will then vary with the market. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $140.42 for 57 months. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $150.30) and a 16.49% interest rate without Auto Pay (16.49% APR) would result in a total estimated payment amount of $34,886.94. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $137.42 for 57 months.

3.) These examples provide estimates based on fixed $25 payments while in school. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $253.39) and a 16.85% interest rate without Auto Pay (14.92% APR) would result in a total estimated payment amount of $47,035.20. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $246.61) and a 16.49% interest rate without Auto Pay (14.65% APR) would result in a total estimated payment amount of $45,814.80. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $25.00.

4.) These examples provide estimates based on deferred payments. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $275.17) and a 16.85% interest rate without Auto Pay (14.67% APR) would result in a total estimated payment amount of $49,530.60. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $268.03) and a 16.49% interest rate without Auto Pay (14.39% APR) would result in a total estimated payment amount of $48,245.40. Your actual repayment terms may vary. Other repayment options are available. It is important to note that the 0.25% Auto Pay discount is not available when the deferred repayment option has been selected and the loan is in the interim period. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $0.

Loan Minimum

Residents of Hawaii must request a loan of at least $1,501.

Repayment Terms and Options

Repayment terms and repayment options available vary based on loan type.

Skip a Payment

Earnest clients may skip a payment through a single, one-month forbearance during a 12 month period. Your first request to skip a pay can be made once you’ve made at least 6 months of consecutive on-time full principal and interest payments, and your loan is in good standing. The interest accrued during the skipped month will result in an increase in your remaining minimum payment. The final payoff date on your loan will be extended by the length of the skipped payment periods. Any unpaid accrued interest may capitalize (added to the principal balance) at the end of the forbearance period by adding unpaid accrued interest to the outstanding principal as permitted by law and the terms of the loan agreement. Please note that skipping a payment is not guaranteed and is at Earnest’s discretion. Your monthly payment and total loan cost may increase as a result of postponing your payment and extending your term.

No Fees

Earnest does not charge fees for origination, late payments, returned check, or prepayments. Florida Stamp Tax: For Florida residents, Florida documentary stamp tax is required by law, calculated as $0.35 for each $100 (or portion thereof) of the principal loan amount, the amount of which is provided in the Final Disclosure. Lender will add the stamp tax to the principal loan amount. The full amount will be paid directly to the Florida Department of Revenue. Certificate of Registration No. 78-8016373916-1.

Earnest Private Student Loans are made by FinWise Bank, Member FDIC. FinWise Bank, 756 East Winchester, Suite 100, Murray, UT 84107. Earnest student loans are serviced by Earnest Operations LLC, 300 Frank H. Ogawa Plaza, Suite 340, Oakland, CA 94612. NMLS #1204917, with support from Higher Education Loan Authority of the State of Missouri (MOHELA) (NMLS# 1442770). FinWise Bank and Earnest LLC and its subsidiaries, including Earnest Operations LLC, are not sponsored by agencies of the United States of America. |

Terms & Disclosures

SoFi Bank, N.A. and its lending products are not endorsed by or directly affiliated with any college or university unless otherwise disclosed. Please borrow responsibly. SoFi Private Student loans are not a substitute for federal loans, grants, and work-study programs. We encourage you to evaluate all your federal student aid options before you consider any private loans, including ours. Read our FAQs. Terms and Conditions Apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. SoFi Private Student loansare subject to program terms and restrictions, such as completion of a loan application and self-certification form, verification of application information, thestudent’s at least half-time enrollment in a degree program at a SoFi-participating school, and, if applicable, a co-signer. In addition, borrowers must be U.S. citizens or other eligible status, be residing in the U.S., Puerto Rico, U.S. Virgin Islands, or American Samoa, and must meet SoFi’s underwriting requirements, including verification of sufficient income to support your ability to repay. Not all repayment options may be available for all loans. Minimum loan amount is $1,000. See SoFi.com/eligibility for more information. View payment examples. Lowest rates reserved for the most creditworthy borrowers. SoFi reserves the right to modify eligibility criteria at any time. This information is current as of 3/4/2026 and is subject to change. SoFi Private Student loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891. (www.nmlsconsumeraccess.org). Good Grades Reward: If eligible, you may receive one cash reward to a SoFi Checking and Savings account. The cash reward offered is $100 for single-semester loans and $250 for full-year loans. Additional terms and conditions apply, see https://www.sofi.com/private-student-loans/rewards-for-good-grades/ for details. SoFi Cosigner Release Disclosure: SoFi does not offer a cosigner release program for In-School Student Loans disbursed prior to May 1, 2019. For In-School Student Loans disbursed on or after May 1, 2019 the borrower may apply for cosigner release after making 12 consecutive on-time full principal and interest payments or the equivalent thereof through a lump sum payment or payments, unless fewer payments are required in accordance with applicable law. Borrowers still must pass an underwriting review and meet all other requirements. Requirements subject to change. 0.125% Continuing Scholar Discount: Terms and conditions apply. Offer good for private student loan customers who have previously borrowed a private student loan from SoFi and are taking out a subsequent loan only, select a term and repayment type that is eligible for the discount, and is subject to lender approval. To receive the offer, you must: (1) complete a loan application with SoFi; and (2) meet SoFi’s underwriting criteria. Once conditions are met and the loan has been disbursed, the interest rate shown in the Final Disclosure Statement will include an additional 0.125% rate discount because you have borrowed a private student loan from SoFi in the past. Offer good for existing private student loan borrowers only. Offer cannot be combined with other rate discounts, with the exception of the 0.25% autopay rate discount and the 0.125% SoFi Plus Parent discount. SoFi reserves the right to change or terminate the Rate Discount Program to unenrolled participants at any time with or without notice. |

3.29% – 15.99% fixed-rate APR w/ autopay included | 4.64% – 16.73% variable-rate APR w/autopay included |

Terms & Disclosures

SoFi Bank, N.A. and its lending products are not endorsed by or directly affiliated with any college or university unless otherwise disclosed. Please borrow responsibly. SoFi Private Student loans are not a substitute for federal loans, grants, and work-study programs. We encourage you to evaluate all your federal student aid options before you consider any private loans, including ours. Read our FAQs. Terms and Conditions Apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. SoFi Private Student loansare subject to program terms and restrictions, such as completion of a loan application and self-certification form, verification of application information, thestudent’s at least half-time enrollment in a degree program at a SoFi-participating school, and, if applicable, a co-signer. In addition, borrowers must be U.S. citizens or other eligible status, be residing in the U.S., Puerto Rico, U.S. Virgin Islands, or American Samoa, and must meet SoFi’s underwriting requirements, including verification of sufficient income to support your ability to repay. Not all repayment options may be available for all loans. Minimum loan amount is $1,000. See SoFi.com/eligibility for more information. View payment examples. Lowest rates reserved for the most creditworthy borrowers. SoFi reserves the right to modify eligibility criteria at any time. This information is current as of 3/4/2026 and is subject to change. SoFi Private Student loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891. (www.nmlsconsumeraccess.org). Good Grades Reward: If eligible, you may receive one cash reward to a SoFi Checking and Savings account. The cash reward offered is $100 for single-semester loans and $250 for full-year loans. Additional terms and conditions apply, see https://www.sofi.com/private-student-loans/rewards-for-good-grades/ for details. SoFi Cosigner Release Disclosure: SoFi does not offer a cosigner release program for In-School Student Loans disbursed prior to May 1, 2019. For In-School Student Loans disbursed on or after May 1, 2019 the borrower may apply for cosigner release after making 12 consecutive on-time full principal and interest payments or the equivalent thereof through a lump sum payment or payments, unless fewer payments are required in accordance with applicable law. Borrowers still must pass an underwriting review and meet all other requirements. Requirements subject to change. 0.125% Continuing Scholar Discount: Terms and conditions apply. Offer good for private student loan customers who have previously borrowed a private student loan from SoFi and are taking out a subsequent loan only, select a term and repayment type that is eligible for the discount, and is subject to lender approval. To receive the offer, you must: (1) complete a loan application with SoFi; and (2) meet SoFi’s underwriting criteria. Once conditions are met and the loan has been disbursed, the interest rate shown in the Final Disclosure Statement will include an additional 0.125% rate discount because you have borrowed a private student loan from SoFi in the past. Offer good for existing private student loan borrowers only. Offer cannot be combined with other rate discounts, with the exception of the 0.25% autopay rate discount and the 0.125% SoFi Plus Parent discount. SoFi reserves the right to change or terminate the Rate Discount Program to unenrolled participants at any time with or without notice. |

|

|

5.59% – 16.99% | 3.99% – 17.99% |

|

|

|

5.59% – 16.99% | 6.75% – 17.99% |

|

Table of Contents

- 1. Apply for financial aid

- 2. Seek scholarships and grants

- 3. Consider work-study programs

- 4. Explore community college options

- 5. Leverage employer tuition assistance

- 6. Use military benefits

- 7. Examine income-share agreements (ISAs)

- 8. Consider online learning platforms

- 9. Investigate tuition-free colleges

- 10. Look into international study options

1. Apply for financial aid

The number one way to pay for college with no money is to apply for financial aid. While it’s not guaranteed you’ll get a full ride, it’s the official process for obtaining need-based aid. (Schools may supplement your need-based aid with merit-based scholarships, depending on your academic resume.)

Start by filling out the FAFSA (Free Application for Federal Student Aid), then wait to see what kind of aid you get offered by each school. And don’t wait too long—each year, there’s a FAFSA deadline you’ll need to meet to qualify for aid. Common types of financial aid from schools include:

- Grants

- Scholarships

- Work-study programs

- Federal Direct Loans

In addition to federal loans, you can apply for private student loans to fill the gap. This allows you to attend college without spending a dime now—and you’ll repay any loans once you graduate and, theoretically, have a job with income to cover the payment.

2. Seek scholarships and grants

One of the core components of your financial aid package is the Pell Grant—money you don’t have to pay back, awarded to you based on your family’s financial need. Similarly, colleges and universities may award specific scholarships to help reduce the cost of school for you, often based on your academic or athletic record.

But the financial aid letter is only the start. Outside organizations may also award scholarships and private grants, either based on your academic performance or affiliation with a specific group or community, including:

- Organizations in your field of study

- Religious organizations

- Community groups

- Ethnic-based organizations

- Your parents’ employer (or your employer, if you already have a job)

You can use websites such as CareerOneStop and Fastweb to search for scholarships online or contact your school’s financial aid office for further assistance. Here are some unique college scholarships to start your search.

3. Consider work-study programs

Your financial aid package might also include employment through a federal work-study program. These are part-time jobs available to undergraduate and graduate students with greater financial need.

Jobs could be on or off campus and ideally related to the major you declare—which can give you real-world experience in your chosen field well before you graduate. These jobs are also designed to be flexible with your class schedule.

Generally, you’ll earn the federal minimum wage in a work-study program, but this can vary depending on the type of job. The money goes to you, not directly to the school, to cover tuition—but the idea is that you’ll use this money to pay for college.

It’s possible you can find a better-paying job elsewhere, but it may be less flexible with your schedule. On top of that, you should tread lightly with any kind of work during school: You should prioritize your grades above all else. Working too much could impact your academics, socialization, and physical and mental health.

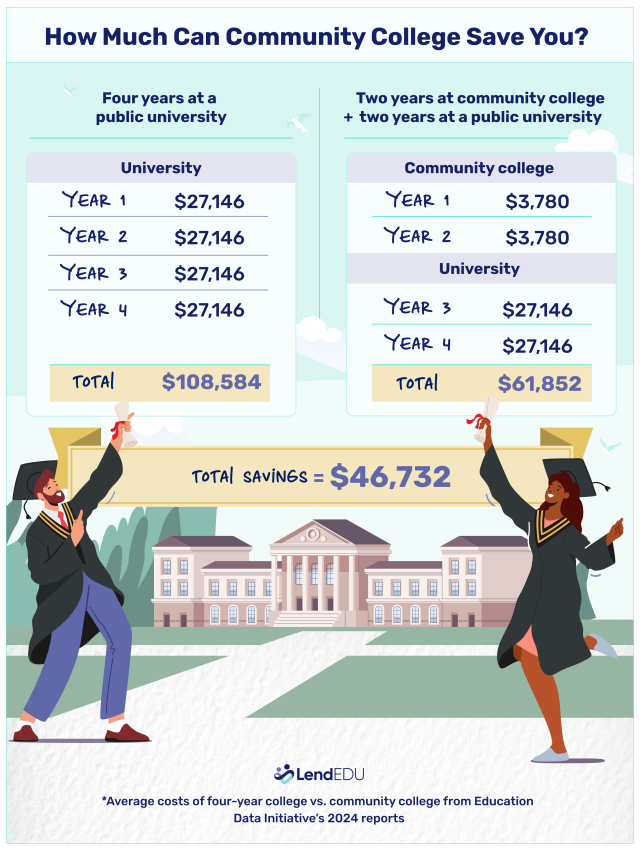

4. Explore community college options

Unfortunately, community college isn’t free, so you’ll technically need to spend money to attend. However, the average cost of community college in 2024 was roughly $1,890 per semester, according to the Education Data Initiative—dramatically lower than the average annual cost of college at a four-year institution, $27,146.

Many students opt to save money by knocking out their general education credits at a community college and then switching to a four-year school to finish their degree.

While attending community college for your general education credits isn’t a true strategy to pay for college with no money, the more flexible schedule could allow you to explore a part-time job while going to school, meaning you’ll potentially have the money to cover the cost of school—and then some.

You can still finance community college despite the lower price tag. Here are the best student loans for community college this year.

5. Leverage employer tuition assistance

Already have a job? See if your employer offers tuition assistance. This is a popular benefit; 46% of employers offer it, according to the Society for Human Resource Management’s 2024 Employee Benefits study.

How the programs work varies by employer: Some may bankroll your education upfront; others may reimburse you upon course completion. Companies may also only offer tuition assistance if you’re enrolled in a program relevant to your role; some may limit how much aid they offer per year, and some may require you to pay back the tuition if you leave the company within a stated time period.

Here are some companies that currently offer tuition assistance, many to both full- and part-time employees:

- Amazon

- AT&T

- Chipotle

- JetBlue

- Starbucks

- Target

- T-Mobile

- UPS

- Walmart

6. Use military benefits

You can also rely on the U.S. military to help pay for college, as long as you’re part of a military branch. How much the military covers depends on your branch and status:

- Active-duty members can get up to $4,500 a year.

- Eligible service members, veterans, and family members can get assistance through the GI Bill.

- Reservists can also get assistance, as well as students who participate in ROTC programs or attend a military academy.

7. Examine income-share agreements (ISAs)

Income-share agreements (ISAs) were once considered an innovative alternative to student loans, but they’ve become less common in recent years. The Consumer Financial Protection Bureau (CFPB) has scrutinized them for deceptive practices, such as misrepresenting the nature of the agreements and failing to provide required disclosures.

Consequently, fewer schools now offer ISAs, but some programs still exist. An income-share agreement is a contract in which a student receives funding from a university or private lender to pay for school. Instead of making fixed payments like a traditional student loan, the borrower agrees to repay a percentage of their future income for a set number of years after graduation. The repayment amount varies based on earnings—if you earn more, you pay more, and if you earn less, your payments decrease.

Unlike student loans, ISAs typically don’t require a credit check, making them an option for students who lack strong credit or a cosigner. Eligibility is often based on academic performance and field of study, with lenders prioritizing degrees expected to lead to higher salaries.

While ISAs can provide access to funding for those who don’t qualify for traditional loans, it’s important to carefully review the repayment terms—some agreements may result in higher overall costs compared to federal or private student loans.

8. Consider online learning platforms

Who says you have to go to college to go to college? Accredited online degree programs are a practical alternative to in-person education at traditional colleges and universities — and they’re cheaper, too. The Education Data Initiative found getting an online degree saves you $30,545 over four years.

And that doesn’t include other savings, such as gas, parking, and rent (if living with parents). While you’ll still technically need some money to pay for an online degree, it’s much more affordable—and you’ll have more free time to work a part-time job or side hustle during college to pay for your degree.

If you’re not seeking a degree but just want to expand your knowledge, you can also find free online courses in various subjects. Some of the country’s most famous schools offer such free courses, including:

- Harvard

- Massachusetts Institute of Technology (MIT)

- Brown University

9. Investigate tuition-free colleges

Across more than 30 states, there are several colleges and universities—some even Ivy League—offering tuition-free degrees, according to Best Colleges. Of course, tuition isn’t free for everyone. Often, these programs are available to students from low-income families; in fact, multiple Ivy League schools offer free tuition to students whose families make under a specific threshold (assuming you can get accepted into the school), including:

Depending on the school, there may also be free tuition opportunities for students pursuing a degree in a field currently experiencing a labor shortage, as well as Native American students.

10. Look into international study options

Some countries allow international students, including those from the United States, to study for free. Germany and Iceland are two of the most notable countries, though you may encounter other fees and a higher cost of living to attend—not to mention a language barrier.

Other countries may not offer free tuition to international students, but many in Europe, like the Nordic countries, do offer much more affordable education.

When helping someone with a very tight budget plan to attend college, we would likely do a few things:

- We would start by re-aligning assets to help improve need-based financial aid.

- Further, if we can work with a student early enough, we encourage them to participate in school activities and improve their grades so they have a better chance of getting scholarships and grants from colleges.

- It is also important to consider the cost of paying student loans so the student can decide if it makes sense to pursue.

About our contributors

-

Written by Timothy Moore, CFEI®

Written by Timothy Moore, CFEI®Timothy Moore is a Certified Financial Education Instructor (CFEI®) specializing in bank accounts, student loans, taxes, and insurance. His passion is helping readers navigate life on a tight budget.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Michael Menninger, CFP®

Reviewed by Michael Menninger, CFP®Michael Menninger, CFP®, is the founder and president of Menninger & Associates Financial Planning. He provides his clients with financial products and services, always keeping their individual needs foremost in mind.