Jet skis aren’t just exhilarating when you’re out on the water—their price tags can get your heart racing, too. That’s where personal watercraft (PWC) financing comes in.

With the right jet ski loan, you can pay for your jet ski over time instead of all at once. Depending on your PWC of choice, you could even use dealer financing or credit cards to fund your purchase. Keep reading to find the best jet ski loans and PWC financing options for you.

Table of Contents

How to get PWC financing

As you research ways to finance your jet ski, consider these methods:

| Financing option | Rates (APR) | Best for |

| Unsecured personal loan | 6% – 36% | Good or excellent credit |

| Secured personal loan | 6% – 36% | Fair credit |

| Dealer financing | Varies, but may come with introductory 0% APR | Fair credit |

| Credit card | 21.59% average | 0% introductory offers |

Unsecured personal loan

An unsecured personal loan is one way to finance your jet ski. This loan type doesn’t require any collateral. Instead, lenders look at your credit, income, and debt-to-income ratio (DTI) when evaluating your loan application.

You’ll repay your loan in fixed monthly payments, with terms usually ranging from one to seven years. How much you’ll pay each month depends on how much you borrow and the interest rate you qualify for.

Borrowers with the strongest credit often qualify for the best rates. Before you apply for a personal loan, take steps to improve your credit for the best shot at a low rate.

Personal loan lenders abound, but we recommend the following due to their borrower benefits and minimal fees:

Best jet ski loans

If you decide a personal loan makes the most sense for your jet ski purchase, we have you covered with recommendations for the best personal loans for vehicles like PWCs.

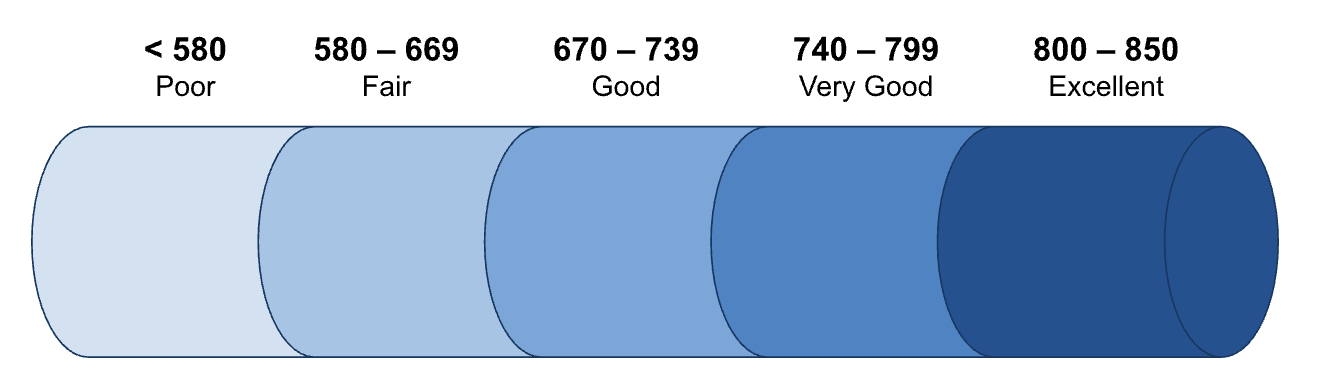

We’ve organized our choices by credit score, so take a second to see which credit category you’re in based on the FICO scoring model:

Now that you know where your credit stands, you’ll have a better idea which of these lenders to prioritize as you pursue jet ski financing.

Best for good credit: SoFi

LendEDU rating: 5.0 out of 5

- Repayment terms up to 84 months

- No late fees or prepayment penalties

- Exclusive member perks

Online lender SoFi offers unsecured personal loans from $5,000 to $100,000. It accepts fair credit scores, but good-credit borrowers will have an easier time accessing SoFi’s lowest rates.

Future jet ski owners will appreciate SoFi’s multiple rate discounts: SoFi will reduce your APR by 0.25% when you sign up for autopay, plus another 0.25% if you enroll in direct deposit with a SoFi bank account. That means more money in your pocket and less spent on interest.

Best for fair credit: Upgrade

LendEDU rating: 4.9 out of 5

- Get funds within a day of applying

- Check your rates through prequalification

- Small loan amounts starting at $1,000

Fair-credit borrowers may have an easier time qualifying with Upgrade, which accepts credit scores starting at 580. Upgrade will also let you submit a joint application to boost your odds of getting approved at a lower rate or for a higher loan amount.

The downside of an Upgrade personal loan is that it comes with origination fees up to 9.99% of your loan amount. Upgrade’s origination fees are deducted from your loan proceeds. While this reduces the amount you receive from Upgrade, it won’t add to your principal balance.

Best for thin credit: Upstart

LendEDU rating: 4.8 out of 5

- Accepts all credit scores

- Uses an alternative lending model

- Next-day funding

Upstart is a solid choice for borrowers with little to no credit who may have trouble qualifying for a personal loan elsewhere. This online lender uses an artificial intelligence-powered lending model that looks beyond your credit score when evaluating your loan application.

It also lets you check your rates online through prequalification. If you borrow a personal loan from Upstart, the lender will let you set up bi-monthly payments. This could make your loan payments easier to manage if you’re paid biweekly instead of once a month.

Should you consider personal watercraft financing?

Whether you should consider PWC financing depends on three factors:

- Your ability to repay the debt

- Your other financial goals

- How much use you’ll get out of your jet ski

In the financial sense, jet skis are liabilities, not assets. Your jet ski won’t make you money, so there’s no real return on investment when you buy a jet ski for personal use. That doesn’t mean it’s not a worthwhile purchase, though.

Here are a few scenarios where you could justify financing your jet ski—and a few scenarios where it makes better sense to pay cash or rent:

| Consider financing if you … | Reconsider if you … |

| Will spend more on jet ski rentals than you will to finance | Plan to buy a home or finance another large purchase in the next two years |

| Have a vehicle and trailer for towing the jet ski | Can buy outright without depleting your savings |

| Have free or low-cost storage | Can’t afford ongoing fuel and maintenance costs |

If you’re already spending several hundred dollars each summer to rent a jet ski, buying your own could save you money in the long run.

On the other hand, if purchasing a PWC means you’ll need to buy a larger vehicle or trailer and pay for storage, it may not be worth it—especially if you’ll only ride your jet ski once or twice a year.

Use our personal loan calculator to estimate your PWC borrowing cost. Divide that amount by what you pay each year in jet ski rental fees. This will tell you how many years it’ll take to recoup your jet ski investment.

As you decide whether to finance your jet ski, know that there’s no harm in waiting until you’ve boosted your credit, shored up your savings, or met other money milestones.

Whatever you do, don’t rush into a loan agreement. Financing will always be an option, even if it’s not the best option right now.

How to apply for personal watercraft loans

If you decide to borrow a personal loan for a jet ski, here’s how to apply:

- Check your credit. Review your credit score and credit report so you know what you’re working with before applying for loans. If your credit is subpar and you don’t mind waiting, consider improving it before applying for your loan.

- Prequalify with multiple lenders. Many personal loan lenders let you check your rates with no impact on your credit score, allowing you to compare loan offers before you commit.

- Look for the most affordable loan. As you compare offers, look for the lowest APR, low (or no) fees, and flexible repayment terms that work with your budget. Finding low jet ski loan rates will help you reduce your borrowing costs.

- Submit a complete application. If you find a loan offer that works for you, you can apply with your personal information and any required documentation, such as pay stubs or bank statements. The lender may run a hard credit inquiry to review your credit profile. This will lower your credit score by a few points, but it should rebound after six to 12 months as you make on-time payments.

- Get your funds and start repaying your loan. Once your application is approved, you’ll receive your jet ski loan as a lump sum in your bank account. Then, you’ll start paying back the loan monthly on the agreed-upon term.

Alternatives to personal watercraft loans

If you’re not sure whether an unsecured personal loan is the best way to buy your jet ski, consider the following options instead.

Secured personal loan

You might opt for a secured personal loan to finance your PWC. These loans may also be called jet ski loans, personal watercraft loans, or boat loans.

Since secured PWC loans will use your jet ski as collateral, they may have more lenient credit requirements and may come with more competitive rates. The risk, however, is that your lender could repossess your jet ski if you fall behind on payments.

Manufacturer or dealer financing

Some jet ski manufacturers or dealers offer financing to qualifying consumers. Deals vary, and you’ll likely have to pass a credit and income check to borrow. You’ll also be limited to that manufacturer’s inventory, so make sure it has the exact jet ski model you want before applying.

Some dealers offer 0% APR financing during your loan’s introductory period, saving you money on interest. When this promotional period ends, though, your APR could skyrocket.

Check your dealer’s offer terms carefully. In some cases, you’ll owe interest on the entire borrowed amount if you don’t pay off your balance in full before your introductory period ends.

Credit card

Purchasing your PWC with a credit card could make sense if you qualify for a credit card with a 0% APR promotional period—and a high enough credit limit.

Some credit cards also offer rewards, so you could earn points back on your jet ski purchase. Plus, if you can pay off your balance before the promotional period ends, you won’t have to pay interest. If you can’t, however, your balance may be subject to hefty interest charges.

FAQ

How much more expensive is financing a jet ski than paying cash?

Financing a jet ski is more expensive than paying cash due to interest and fees. The long-term costs of financing will vary depending on your loan amount, APR, and loan term.

Here’s an example of how much more a loan with a five-year repayment term would cost compared to paying cash for a $10,000 jet ski.

| Cash | 5-yr. loan | |

| Amount | $10,000 | $10,000 |

| Rate | 0% | 12% |

| Interest paid | $0 | $3,347 |

| Total cost | $10,000 | $13,347 |

A shorter loan term will save you money on interest but will come with higher monthly payments. A longer term will have more affordable monthly payments but will increase your interest costs.

What are the best jet ski loans?

What constitutes the best jet ski loan is a bit subjective and depends on the borrower. The best jet ski loan gives you enough financing to cover your purchase while also offering competitive rates and minimal fees.

To determine whether you’ve found the right jet ski loan, prequalify with four to five lenders. Compare each lender’s APR, fee structure, and features to decide which is the best for you.

Are there bad-credit jet ski loans?

Bad credit can make qualifying for a jet ski loan challenging, but you still have options. Upgrade, for example, accepts credit scores starting at 580, while Upstart will consider credit scores down to 300 (the lowest possible).

If you qualify for a loan with bad credit, ensure you’re comfortable with the terms. Bad-credit borrowers may pay higher rates and origination fees, making your loan more expensive.

What jet ski loan rates can you expect?

The rates you’ll get on a jet ski loan will vary depending on the type of loan and your credit profile. Here are a few rate ranges you can expect:

| Lender or financing type | Fixed rates (APR) |

| SoFi | 8.99% – 29.49% with all discounts |

| Upgrade | 8.49% – 35.99% |

| Upstart | 7.80% – 35.99% |

| Secured personal loans | Vary, but may be lower than unsecured rates |

| Manufacturer or dealer financing | Vary, but may come with 0% APR for 12 months |

| Credit cards | 21.59% average (as of May 2024) |

How long are jet ski loans?

Repayment terms on jet ski loans will vary by lender and loan amount, but most fall between one and seven years. Here’s what our recommended lenders offer, plus the loan terms for other jet ski financing options:

| Lender or financing type | Repayment terms |

| SoFi | 2 – 7 years |

| Upgrade | 2 – 7 years |

| Upstart | 3 or 5 years |

| Secured personal loans | 1 – 7 years or more |

| Manufacturer or dealer financing | Varies |

| Credit cards | Revolving basis |

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.