Personal loans allow you to borrow a fixed amount of cash for almost any purpose without providing collateral at lower rates than credit cards. This flexibility and affordability make them a popular lending option.

If you live in Illinois, there is an abundance of lenders to choose from. We’ve researched Illinois personal loans, both locally and online, to help you make the best choice. Here are our choices for the best online personal loans in Illinois:

Table of Contents

Online personal loans in Illinois

Getting a personal loan through an online lender makes it easy to apply and get your funds quickly, sometimes even on the same day.

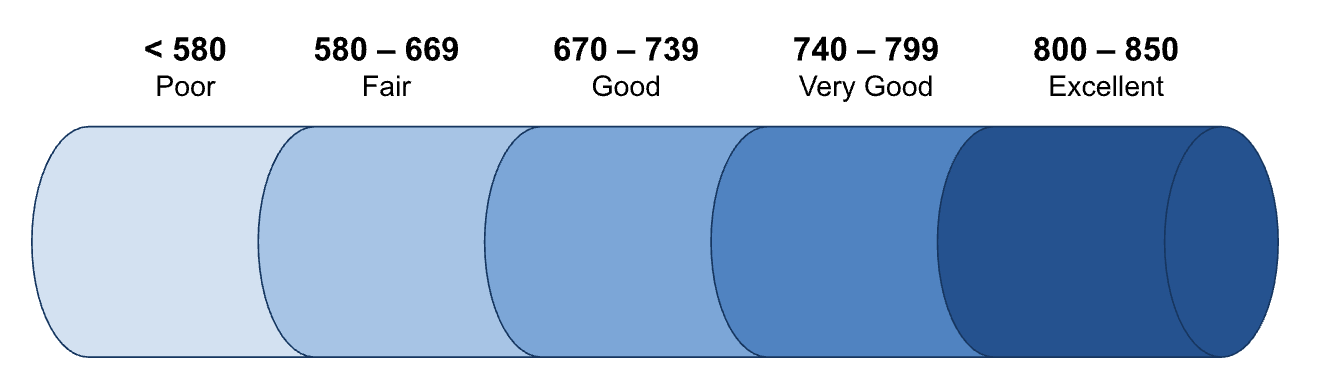

Because you don’t need to provide collateral, your credit score is the top consideration that affects personal loan approval and your rate. The good news is some lenders will offer personal loans to good, fair, and bad-credit borrowers. The credit score ranges are shown in the image below.

Based on where your credit score falls, here are our recommendations for online personal loans in Illinois:

Credible

Why Credible is the best marketplace

Credible is the best choice for personal loan marketplaces because it lets you compare rates and choose from lenders catering to all credit score levels. You can quickly compare offers from lenders like LightStream, Discover, Upstart, and SoFi all in one place.

Credible doesn’t charge fees, so the only cost is the fees each lender charges, like origination fees. You can prequalify for a loan to check your rates with no credit impact. Plus, close with a better rate than you prequalify for on Credible, and you’ll get a $200 gift card (Terms apply.)

In addition to personal loans, the company offers financial loan options such as student loan refinancing, mortgages, and home equity loans.

- Compare loans from multiple curated lenders

- Get prequalified loan offers in as little as 2 minutes

- Get funded within a few business days

- No option to apply for joint loans

| Rates (APR) | 6.99% – 35.99% |

| Loan amounts | $1,000 – $200,000 |

| Repayment terms | 1 – 10 years |

Eligibility requirements

- Soft credit check? Yes

- Minimum credit score: Varies

- Minimum income: Not disclosed

- States: Loan partners may not be available in all states

Repayment terms

Credible loans have repayment terms ranging from one to 10 years. Some lenders may charge a prepayment penalty if you pay your loan off early.

Upgrade

Why Upgrade is the best personal loan for fair credit

Upgrade is our top pick for borrowers with fair credit in Illinois. Its rates are competitive with most other lenders we considered.

If approved for a loan with Upgrade, you’ll receive multiple loan offers to choose from. Funds can be available before the next business day.

Upgrade also has a short-term hardship program. If you experience financial hardship, you can make reduced payments for a set period. For fair-credit borrowers needing financial flexibility, Upgrade is a great choice.

- Choose your monthly payment and loan term

- Joint applications accepted

- Loan funds may be available in as little as 1 day

- Smaller loan maximum limit

- 1.85% to 9.99% origination fee

| Rates (APR) | 8.49% – 35.99% |

| Loan amounts | $1,000 – $50,000 |

| Repayment terms | 2 – 7 years |

Eligibility requirements

- Soft credit check? Yes

- Minimum credit score: 580

- Minimum income: Not disclosed

- States: All 50 states and Washington, D.C.

Repayment terms

Upgrade loans have repayment terms from two to seven years, and your monthly due date is adjustable to fit your budget. A short-term financial hardship program is available if you’re temporarily unable to manage payments.

SoFi

Why SoFi is the best personal loan for good credit

SoFi® is our top pick for Illinois residents with good credit. No fees are required, and rates are competitive. The rates for SoFi personal loans are fixed, and the company also offers a rate discount for autopay if you bank with SoFi or have other financial products with the company.

You can check your rate in as little as 60 seconds. If approved, you can get funding as soon as the same day.

- No origination fees, late payment fees, or prepayment penalties

- Check rates in as little as 60 seconds

- Some borrowers may qualify for same-day funding

- Higher minimum loan amount

- Autopay discount is lower than what some lenders offer

| Fixed rates (APR) | 8.99% – 29.99% with all discounts |

| Loan amounts | $5,000 – $100,000 |

| Repayment terms | 2 – 7 years |

Eligibility requirements

- Soft credit check? Yes

- Minimum credit score: 660

- Minimum income: Not disclosed

- States: All 50 states and Washington, D.C.

Repayment terms

SoFi personal loans feature terms from two to seven years. If you enroll in autopay, you’ll get a 0.25% rate discount. There’s no penalty if you decide to pay your loan off early.

LightStream

Why LightStream is the best personal loan for excellent credit

LightStream is our top pick for excellent credit in Illinois. Its loans have competitive rates, no fees, and fast funding. The lender specifically works with those with good-to-excellent credit, and the best rates are reserved for borrowers with excellent credit.

LightStream doesn’t charge loan processing fees, late fees, or prepayment penalties. You’ll also get a 0.50% rate discount if you set up autopay.

It is important to note that LightStream does not offer preapproval with a soft credit check. Applying will affect your credit score, which is why having excellent credit is best when choosing Lightstream.

If you need flexibility in your loan term, LightStream offers terms of 24 to 240 months. Longer terms generally mean more overall interest costs but can also make payments more manageable, depending on your needs. Funds can be available as soon as the same day if you apply on a banking business day.

- Rate match guarantee ensures that you get the best rate possible

- Same-day funding may be available

- Take advantage of a longer repayment term if you need lower payments

- No option to prequalify or check rates with a soft credit pull

- Minimum loan amount is $5,000

| Rates (APR) | 7.49% – 25.49% |

| Loan amounts | $5,000 – $100,000 |

| Repayment terms | 2 – 12 years |

Eligibility requirements

- Soft credit check? No

- Minimum credit score: 660

- Minimum income: Not disclosed

- States: All 50 states and Washington, D.C.

Repayment terms

LightStream offers some of the longest repayment terms of any lender, giving you up to 12 years to repay your loan. You can pay your loan off early, without a prepayment penalty and rate discounts can help bring the cost of your loan down.

Local personal loan lenders in Illinois

You can also research local banks and credit unions if you want a personal loan. Because they’re local, they tend to be in tune with the needs of people in your area.

The downside of using a local lender is that you’re limiting your options. If there are only one or two banks within driving distance, you won’t be able to get many offers to compare. Some brick-and-mortar lenders can also be more conservative than online lenders, making it harder to qualify for a loan.

| Lender | Rates (APR) | Loan amounts |

| BMO Harris Bank | 9.89% – 22.14% | $5,000 – $35,000 |

| Old National Bank | Up to 25.00% | $2,500 – $25,000 |

| Central Credit Union of Illinois | Starting at 9.90% | Up to $30,000 |

Local lenders know your market and often your or your family history. I’ve seen larger, more generous mortgage loans sometimes offered by local lenders when they deem you creditworthy and are comfortable with the demographics and prospects of your neighborhood. That said, online lenders may offer quicker/easier underwriting options if you have a good credit score and borrow a small sum. If you have the time, check out both options before you choose.

Catherine Valega, CFP®

About personal loans in Illinois

Illinois has legislation limiting payday lenders to help protect consumers from predatory loans. This can help you avoid bad loans.

Keep the following in mind if you’re considering a payday loan in Illinois:

- Your monthly payment can’t exceed 22.5% of your monthly income

- Lenders can’t roll your loan into a new one if it will keep you in debt for longer than six months

- You’re entitled to an interest-free repayment plan if you’ve been in debt with a lender for over 35 days.

Read More Personal loans by state

How to apply for personal loans in Illinois

When you apply for a personal loan, you must provide identifying and financial information. This includes:

- Your name

- Your address

- Your Social Security number

- Your annual income

- Your monthly housing payment

- Information about other debts or liabilities you have

Many lenders will request proof, so be ready with a copy of your lease or a recent pay stub to prove your income and housing payments. Most loan applications outline what you must provide before final approval, so gather all the required documentation to speed up the process.

Recap: Best online personal loans in Illinois

About our contributors

-

Written by Bob Haegele

Written by Bob HaegeleBob Haegele has been a freelance personal finance writer since 2018. In January 2020, he turned this side hustle into a full-time job. He is passionate about helping people master topics such as investing, credit cards, and student loans.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Catherine Valega, CFP®, CAIA®

Reviewed by Catherine Valega, CFP®, CAIA®Catherine Valega, CFP®, CAIA®, founded Green Bee Advisory LLC to help women, philanthropists, investors, and small businesses build, manage, and preserve their financial resources. She's been practicing financial planning for more than 20 years.