Our take: Fig Loans offers a safer, more transparent alternative to payday loans, with fast funding and no credit check required. Its installment and credit builder loans can help borrowers with limited credit history access cash or build credit. But high APRs and small loan amounts mean it’s best suited for emergencies or short-term credit improvement.

Installment Loans

- No credit score required

- Quick funding

- Online banking requirement

- High APRs

- Small loan amounts

- Limited availability

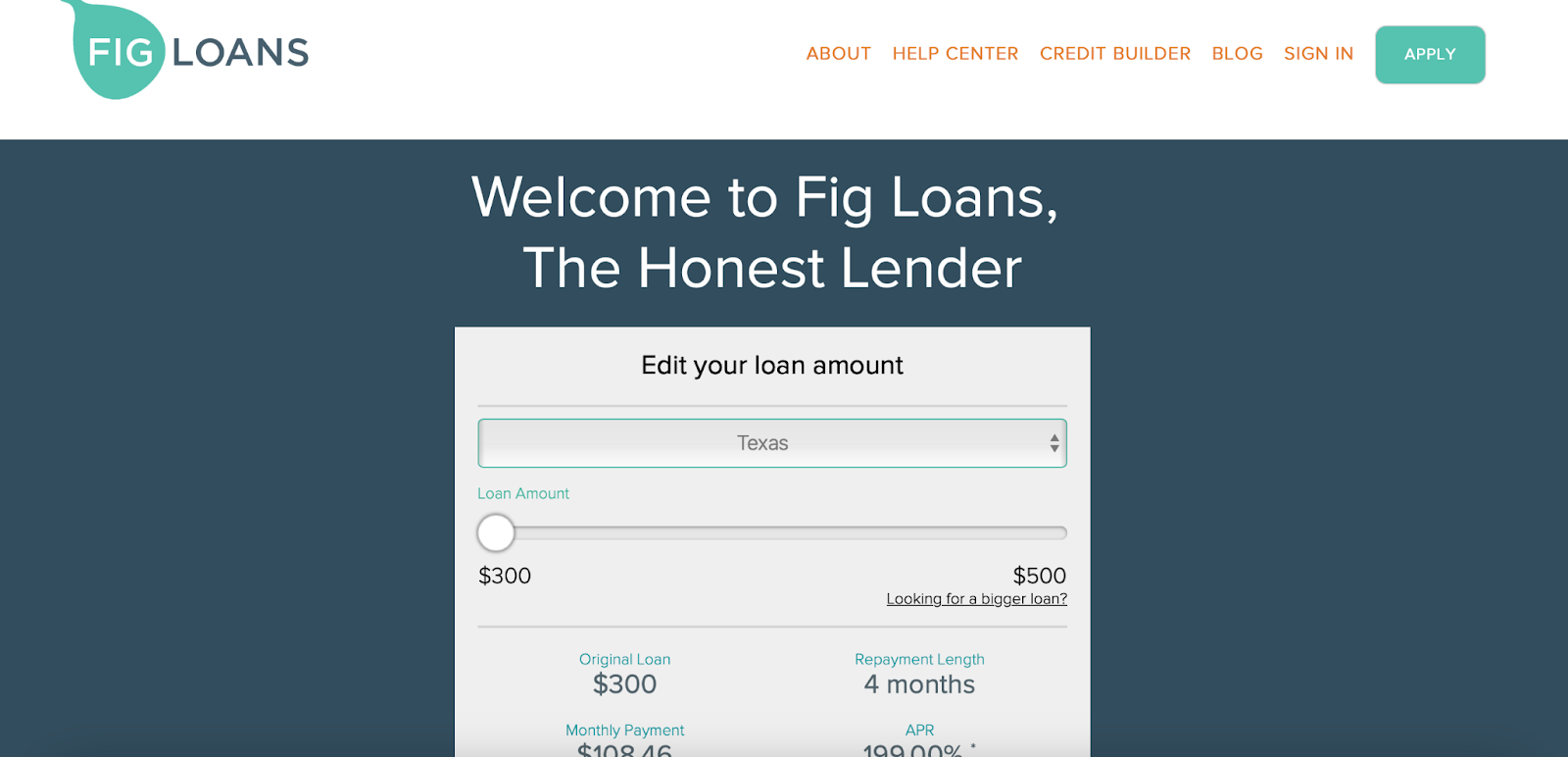

| Fixed rates (APR) | 199% – 211%, depending on state |

| Loan amounts | $50 – $500, depending on state |

| Repayment period | 1 month – 6 months, depending on state |

| Time to funding after approval | Decision in 1 day; Funds in 1-3 business days |

| Fees | Vary by state; One-time account opening fee |

Credit Builder Loans

| Amounts | $500 – $1,000 |

| Term length | 12 months |

| Rate | As low as 4% APR |

| Credit bureaus reported to | TransUnion, Equifax, and Experian |

| Unique features | Reverse loan: Instead of receiving money upfront, you make 12 manageable monthly payments into a savings account. If your payment is close to being 30 days late, Fig proactively closes the loan to protect your credit. |

Founded in 2015, Fig Loans is a mission-driven lender designed to support working-class Americans who may not qualify for traditional credit.

It began in Houston, Texas, as a partnership with United Way THRIVE to offer a safer, more transparent alternative to payday loans.

What is a Fig loan?

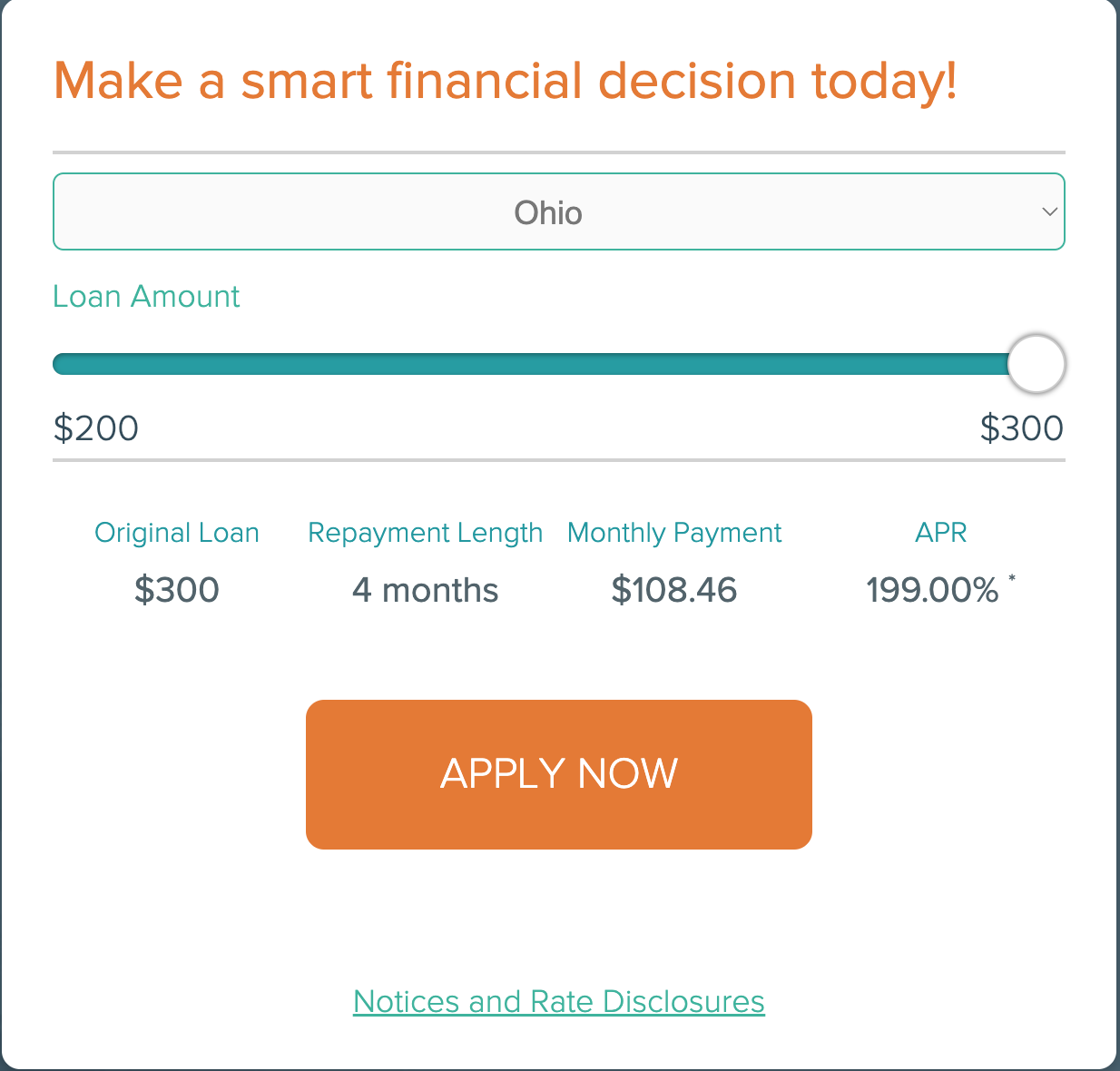

Fig Loans offers short-term installment loans and credit builder loans in six states: Texas, Missouri, Ohio, Utah, Florida, and California.

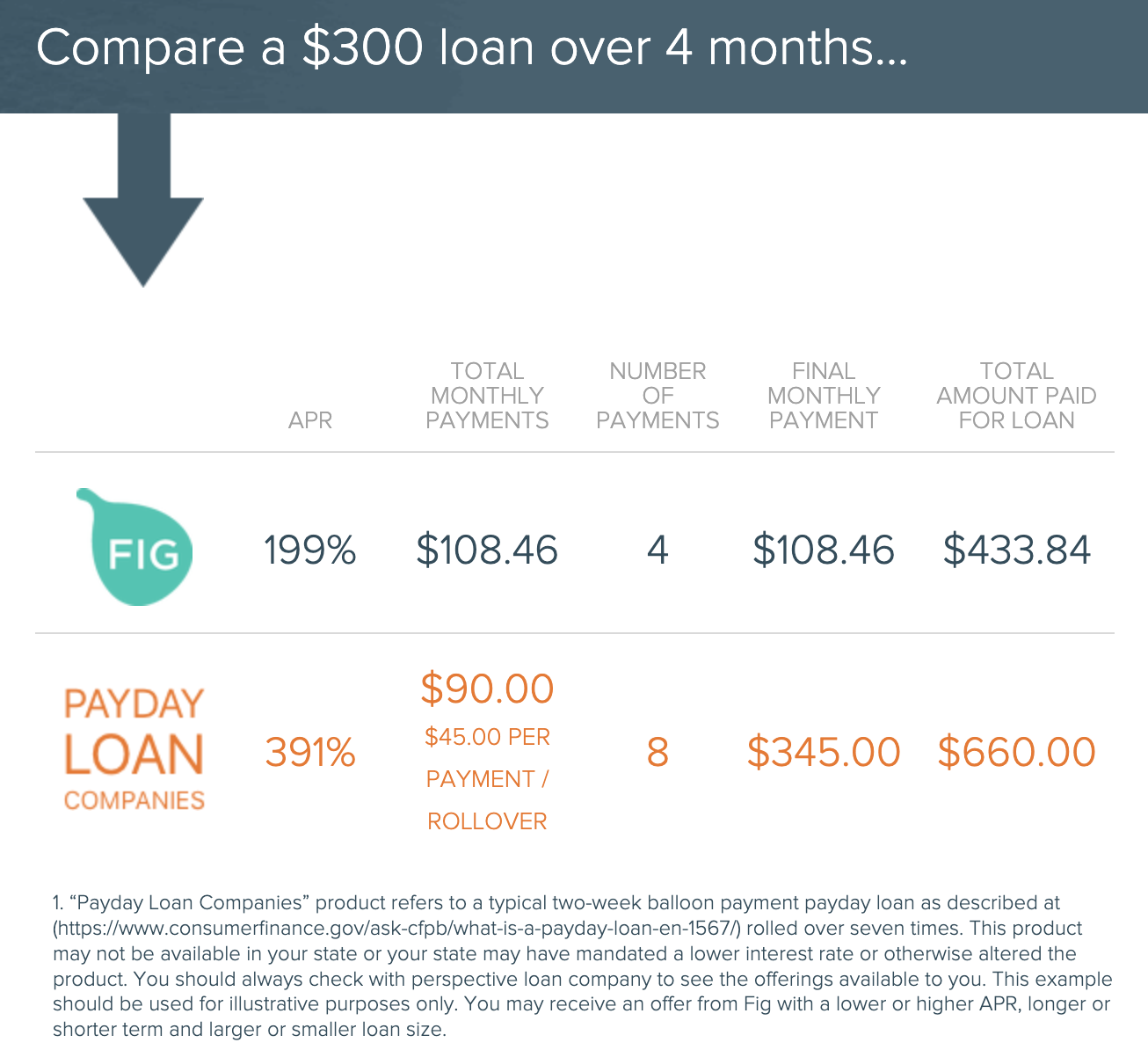

Though marketed as a payday loan alternative, Fig’s installment loans have high APRs (199% to 211%), far above those of traditional personal loans.

Fig’s credit builder loan allows borrowers to build credit by making monthly payments, which are reported to all three major credit bureaus. Borrowers get their funds back at the end of the term, minus interest and fees.

While Fig Loans provides access and credit-building opportunities, borrowers should compare costs with other lenders before applying.

Fig installment loans at a glance

Fig Loans offers small, short-term personal loans known as installment loans.

| Fixed rates (APR) | 199% – 211%, depending on state |

| Loan amounts | $50 – $500, depending on state |

| Repayment period | 1 month – 6 months, depending on state |

| Time to funding after approval | Decision in 1 day; Funds in 1-3 business days |

| Fees | Vary by state; One-time account opening fee |

Fig Loans designed its personal loan process to be straightforward and accessible, especially for those who may not qualify for traditional loans.

Eligibility requirements

Fig Loans personal loans cater to people who might struggle with traditional credit requirements. Fig Loans does not require a credit check, making it an accessible option for those with poor or no credit history.

Here’s the full breakdown of eligibility requirements for a Fig Loans personal loan:

| Requirement type | Details |

|---|---|

| Citizenship | Not specified, but U.S. bank account required |

| Employment status | 3 months of direct deposits required |

| State of residence | California, Missouri, Utah, Texas, Ohio, Florida |

| Credit score check | None required |

| Minimum income | Monthly deposits of at least $1,400 |

| Other requirements | Internet connection Online application capability Phone number Social Security number Government-issued photo ID Online banking |

Costs and fees

When you apply for a Fig Loan, your fixed APR varies by state, typically ranging between 199% to 211%. This rate is based on the loan amount and the state you reside in.

Fig Loans markets itself as a payday loan alternative, meaning it’s likely a better option than a traditional payday loan, which can have an APR of up to 400%. Still, Fig’s APR is much higher than a traditional personal loan. Our best personal loan selections have maximum APRs near 36%.

Other cost and fees include:

- Administrative fee: This varies based on the state and the amount borrowed. It’s an additional charge for account opening and loan processing.

- Other fees: Fig doesn’t disclose membership fees, but we recommend verifying whether additional fees apply during the application process.

Repayment

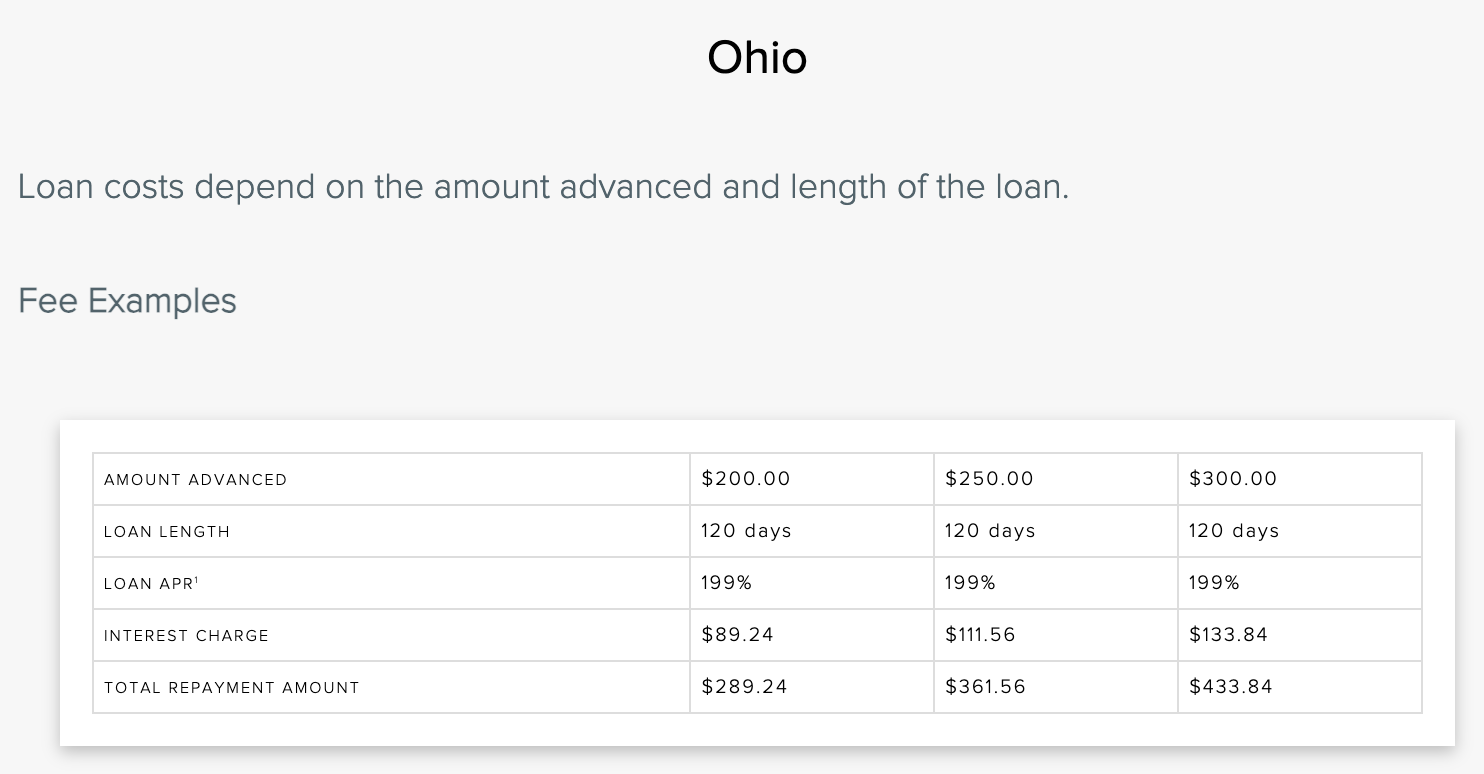

Repayment terms are specific to each state.

- In California, borrowers repay the loan and interest in a single installment one month after the loan is issued.

- Florida offers an 84-day repayment period with biweekly payments.

- Missouri, Ohio, and Texas have monthly repayment schedules spread over four months.

- In Utah, it’s spread over six months.

Payments are automatically deducted from the borrower’s bank account on the agreed-upon dates, and borrowers can track their payments and manage their accounts online.

Pros and cons

Pros

-

No credit score required

-

Quick funding

-

No early repayment penalty

Cons

-

Online banking requirement

-

High APRs

-

Limited availability

-

Small loan amounts

Alternatives

Paycheck advance apps

For quick advances of $1,000 or less, we recommend reputable cash advance apps as a more convenient and cost-effective solution.

For those who can qualify, and are interested in borrowing $1,000 or more, alternatives SoFi, PenFed, Upstart, Personify, and OppLoans might provide more favorable terms, such as lower APRs and broader loan options.

Personal loans

Fig Credit Builder Loan Review at a glance

| Deposit amounts | Not specified |

| Term length | 12 months |

| Rate | As low as 4% APR |

| Credit bureaus reported to | TransUnion, Equifax, and Experian |

| Time to funding after approval | Decision in 1 day; Funds in 1-3 business days |

| Fees | Vary by state; Administrative and debit card processing fees |

| Unique features | Reverse loan: Instead of receiving money upfront, you make 12 manageable monthly payments into a savings account. If your payment is close to being 30 days late, Fig proactively closes the loan to protect your credit. |

Fig Loans’ credit builder loan is aimed at individuals looking to build or improve their credit scores. Fig’s credit builder reports to the three major credit bureaus: TransUnion, Equifax, and Experian.

However, these loans are available in only six states.

How does it work?

Borrowers make regular payments over a set term, with payments reported to major credit bureaus.

The loan acts as a savings account. You get the funds back at the end of the term, minus interest and fees.

Eligibility requirements

| Requirement | Details |

| State of residence | California, Florida, Missouri, Ohio, Texas, and Utah |

| Minimum age | Not disclosed |

| Minimum credit score | None |

| Minimum income | Monthly deposits of at least $1,400 |

| Other requirements | Internet connection Online application capability Phone number Social Security number Government-issued photo ID Online banking |

Costs and fees

The interest rate for Fig Loans’ credit builder loans varies based on loan amount and state, but it can be as low as 4%. This rate influences the total amount you repay over the term of the loan.

Other cost and fees include:

- Administrative fee: This varies based on the state and the amount borrowed. It’s an additional charge for account opening and loan processing.

- Other fees: Fig doesn’t disclose membership fees, but we recommend verifying whether additional fees apply during the application process.

Repayment

Borrowers make 12, fixed payments over the course of a year, and then get their payments back, minus APR/fees, at the end of the 12-month period.

Pros and cons

Pros

-

Credit building

-

No credit score requirement

-

End-of-term fund distribution

Cons

-

Online banking and deposit requirements

-

Limited availability

Alternatives

We recommend considering the best credit builder apps from CreditStrong, MoneyLion, Self, and more:

*Sample loans: $25/mo, 24 mos, 15.92% APR; $35/mo, 24 mos, 15.69% APR; $48/mo, 24 mos, 15.51% APR; $150/mo, 24 mos, 15.82% APR. Variable admin fee of $1-$5 may apply. See self.inc/pricing.

Self is not a bank. Credit Builder Accounts & Certificates of Deposit made/held by Lead Bank, Sunrise Banks, N.A., or First Century Bank, N.A., each Member FDIC, see more at FDIC coverage. Credit Builder Accounts & Certificates of Deposit are subject to loan application and approval. See self.inc/credit-builder-loan for plans and pricing.

Secured Self Visa Credit Card issued/held by Lead Bank, Sunrise Banks, N.A., or First Century Bank, N.A., each Member FDIC. See self.inc/visa-secured-credit-card for details including important rate and fee information. Qualification for the secured Self Visa Credit Card is based on meeting eligibility, including income and expense requirements and establishment of minimum $100 security interest. Criteria subject to change.

Results may vary. You may not receive an improved credit score based on your financial behavior, including missed payments with Self credit products and activity with other creditors.

Other factors, including activity with other creditors, may impact results. Failure to make monthly minimum payments by due date may result in delinquent payment reporting to credit bureaus which may negatively impact your credit score. Self is not a Credit Repair Organization. Self does not remove negative credit history from credit reports. Self products are not intended to provide advice or assistance related to a consumer’s credit record or history.

All trademarks and brand names belong to their respective owners and do not represent endorsements of any kind.

*Sample loans: $25/mo, 24 mos, 15.92% APR; $35/mo, 24 mos, 15.69% APR; $48/mo, 24 mos, 15.51% APR; $150/mo, 24 mos, 15.82% APR. Variable admin fee of $1-$5 may apply. See self.inc/pricing.

Self is not a bank. Credit Builder Accounts & Certificates of Deposit made/held by Lead Bank, Sunrise Banks, N.A., or First Century Bank, N.A., each Member FDIC, see more at FDIC coverage. Credit Builder Accounts & Certificates of Deposit are subject to loan application and approval. See self.inc/credit-builder-loan for plans and pricing.

Secured Self Visa Credit Card issued/held by Lead Bank, Sunrise Banks, N.A., or First Century Bank, N.A., each Member FDIC. See self.inc/visa-secured-credit-card for details including important rate and fee information. Qualification for the secured Self Visa Credit Card is based on meeting eligibility, including income and expense requirements and establishment of minimum $100 security interest. Criteria subject to change.

Results may vary. You may not receive an improved credit score based on your financial behavior, including missed payments with Self credit products and activity with other creditors.

Other factors, including activity with other creditors, may impact results. Failure to make monthly minimum payments by due date may result in delinquent payment reporting to credit bureaus which may negatively impact your credit score. Self is not a Credit Repair Organization. Self does not remove negative credit history from credit reports. Self products are not intended to provide advice or assistance related to a consumer’s credit record or history.

All trademarks and brand names belong to their respective owners and do not represent endorsements of any kind.

*Sample loans: $25/mo, 24 mos, 15.92% APR; $35/mo, 24 mos, 15.69% APR; $48/mo, 24 mos, 15.51% APR; $150/mo, 24 mos, 15.82% APR. Variable admin fee of $1-$5 may apply. See self.inc/pricing.

Self is not a bank. Credit Builder Accounts & Certificates of Deposit made/held by Lead Bank, Sunrise Banks, N.A., or First Century Bank, N.A., each Member FDIC, see more at FDIC coverage. Credit Builder Accounts & Certificates of Deposit are subject to loan application and approval. See self.inc/credit-builder-loan for plans and pricing.

Secured Self Visa Credit Card issued/held by Lead Bank, Sunrise Banks, N.A., or First Century Bank, N.A., each Member FDIC. See self.inc/visa-secured-credit-card for details including important rate and fee information. Qualification for the secured Self Visa Credit Card is based on meeting eligibility, including income and expense requirements and establishment of minimum $100 security interest. Criteria subject to change.

Results may vary. You may not receive an improved credit score based on your financial behavior, including missed payments with Self credit products and activity with other creditors.

Other factors, including activity with other creditors, may impact results. Failure to make monthly minimum payments by due date may result in delinquent payment reporting to credit bureaus which may negatively impact your credit score. Self is not a Credit Repair Organization. Self does not remove negative credit history from credit reports. Self products are not intended to provide advice or assistance related to a consumer’s credit record or history.

All trademarks and brand names belong to their respective owners and do not represent endorsements of any kind.

Fig36

Fig36 is Fig Loans’ nonprofit lending program. It equips community organizations with the tools to offer affordable, credit-building loans.

Through Fig36, partners gain access to Fig’s risk models, loan management software, credit reporting, and compliance infrastructure, delivering the sophistication of a major financial institution with a local, community-first approach.

The program is currently in limited beta in Texas, with plans to expand.

Is Fig Loans legit? What customer reviews say

| Source | Customer rating | Number of reviews |

| Trustpilot | 4.9/5 | 8,612 |

| Better Business Bureau | 1.0/5 | 3 |

| 4.7/5 | 2,326 |

Fig Loans has a good reputation across various review platforms. Customers praise Fig Loans for working with individuals with bad credit, fast delivery of funds, and its ability to boost credit scores. However, some reviews point out high rates and issues with the application system.

Fig Loans is not BBB-accredited. Complaints here focus on inaccurate reporting to credit agencies, identity theft concerns, and loan denials.

Positive feedback on Google highlights the ease of obtaining a loan and manageable payments. Nevertheless, some reviewers express dissatisfaction with application issues and loan denials.

Customer service

Fig Loans’s customer service team can assist customers with inquiries and issues related to their loans. The team is based at the company’s headquarters in Sugar Land, Texas.

Ways to contact Fig Loans:

- Phone number: Toll-free at 833-335-0855

- Mailing address: 2245 Texas Drive, Suite 300, Sugar Land, TX 77479

- Chat box: Available on the website for quick inquiries

- Business hours: Monday – Friday, 8 a.m. – 4 p.m. Central time

How to apply

Applying for a Fig Loans personal or credit builder loan doesn’t affect your credit score.

Unlike other lenders that offer prequalification to gauge eligibility without affecting credit scores, Fig Loans’ approach simplifies the process, but its terms are less flexible than traditional personal loan lenders.

Here are the steps to apply:

- Select your state: Begin by choosing your state of residence. Loan terms and availability vary by state.

- Choose the loan amount: Determine your desired loan amount.

- Register and submit required documents: Create an account with Fig Loans and provide necessary documentation, including:

- Bank login information: Username and password for a compatible checking or savings account with three months of transaction history and income deposits of $1,400 per month.

- Two bank verification partners: These partners securely access and verify banking information.

- A positive bank balance: Required at the time of application.

- Social Security number: Necessary for identity verification.

- Photo ID: State-issued ID or passport.

The application process is straightforward.

Bottom line

Fig Loans fills an important gap for borrowers with limited credit options, offering fast funding and no credit check. However, its triple-digit APRs, low loan amounts, and limited availability mean it should only be a short-term solution.

If you qualify for a lower-rate personal loan or a more flexible credit builder program, those alternatives may be more cost-effective paths to improving your finances.

About our contributors

-

Written by Amanda Hankel

Written by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.