Consolidating private student loans can have several benefits, such as combining multiple payments into one and securing a lower interest rate. Depending on your credit history, consolidating private loans can simplify your payments and save you money.

Remember that a federal Direct Consolidation Loan differs from a private student loan consolidation. We’ll help you understand the important distinction between the two. Then, we’ll talk to you about the process of consolidating your private student loans and list some top consolidation lenders.

Table of Contents

Can I consolidate private student loans?

If you have multiple private and/or federal student loans, it’s possible to combine these into a single private student loan, potentially with a lower interest rate than you’re currently paying. This may be possible if your credit score has improved since you first applied or if you have a cosigner with a strong credit history.

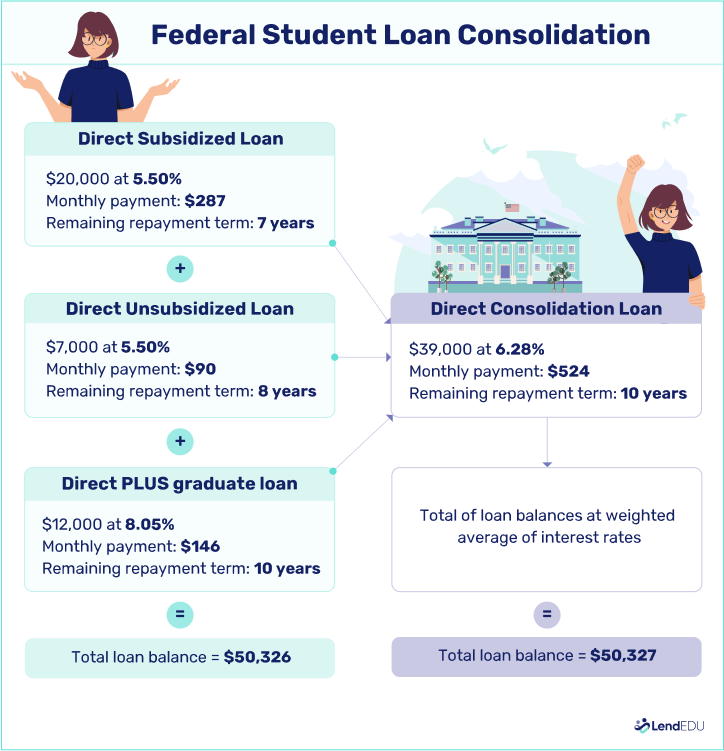

An important distinction is that student loan consolidation generally refers to the Department of Education’s federal Direct Consolidation Loans. These programs are only available for federal student loans, and their primary purpose is to combine your loans into a single payment. However, they don’t lower your interest rate.

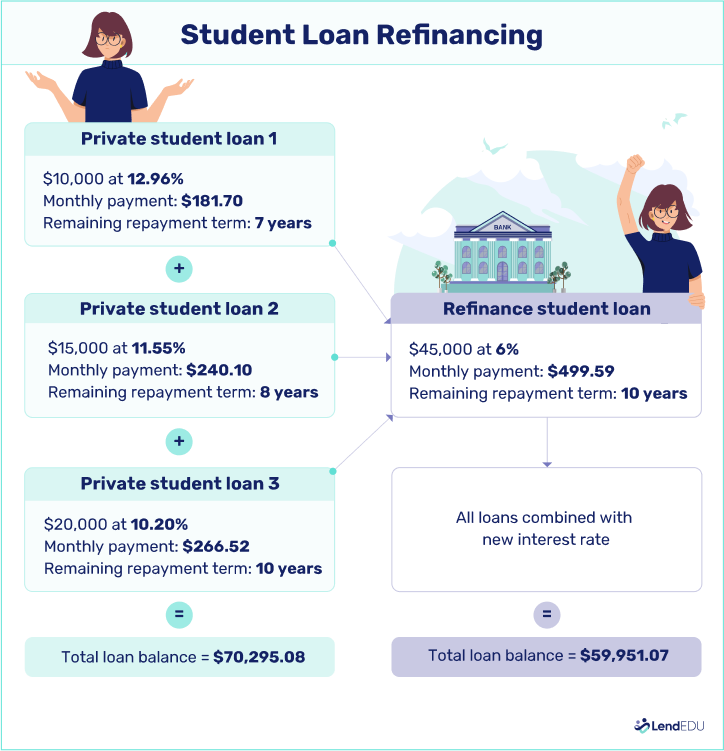

Consolidating private student loans, more commonly known as refinancing, lets you combine multiple federal or private student loans into a single payment. While you can refinance both federal and private student loans, only federal student loans are eligible for federal student loan consolidation.

One of the biggest advantages of student loan refinancing is that you may be able to qualify for a lower interest rate. However, applying only if you have good-to-excellent credit is best because that depends on your credit score. Also, remember that private student loans aren’t available for income-driven repayment or programs like Public Student Loan Forgiveness (PSLF) or deferment/forbearance.

If you are unsure where you have federal and/or private student loans, contact your school to clarify or check the student loan servicer you pay—MOHELA, Nelnet, and EdFinancial Services are examples of federal loan servicers. Meanwhile, you pay the lender for private student loans.

Investigate your loan documents for clues—federal student loans typically mention entities like the Department of Education.

How to consolidate private student loans

If you are ready to refinance your private student loans, here are some general steps to take:

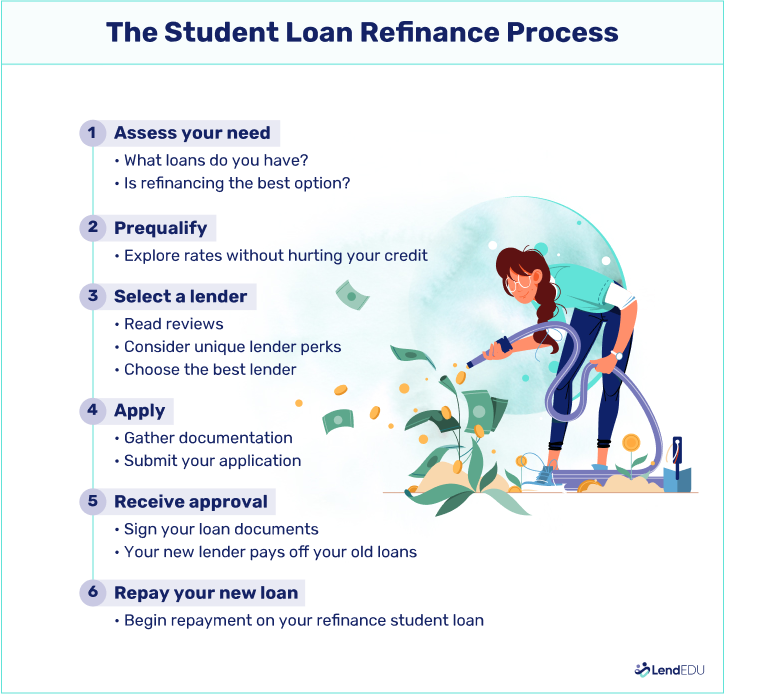

- Assess your needs. The first step in consolidating private student loans is ensuring it makes sense to do so. Understand the types of loans you have and if it makes financial sense to combine payments and apply for refinancing.

- Evaluate interest rates. Interest rates are crucial to student loan refinancing, as this rate determines whether the loan will save you money. Most student loan refinancing lenders will allow you to prequalify to check your rate and eligibility without affecting your credit score. In addition to the rate, check whether each lender offers fixed or variable rates, as this can greatly impact how much interest you will pay.

- Select a lender. Compare the refinancing offers you receive through prequalification to choose the right lender and refinance loan for you. In addition to interest rate, evaluate other loan terms like repayment length. Also consider things like customer reviews and if the lender has the customer service features you desire.

- Apply for a loan. Once you have found a few lenders that meet your needs, you must apply for loans with them. These are usually online and require basic information, such as your income, current student loans, and other financial details.

- Receive approval. After you apply and are approved, you’ll receive all of the information about the loan in the loan documents. Review the interest rates, loan terms, fees, and potential penalties. Once you sign the loan documents. The lender will pay off your existing student loans and combine them into a single payment.

- Start making payments. You will then begin making payments to your new lender. Often, the new lender will set you up with online access to make paying easier.

The timeframe for student loan refinancing can vary depending on several factors. For instance, the lender may need to run a credit check, which could take anywhere from a few days to a week.

In addition, the lender may need additional documentation, which could add a few more days. Loan disbursement can also take up to a week. The entire process typically takes two to four weeks, though it could be shorter in some cases.

Remember that while refinancing can lead to a lower interest rate, private student loans often have fewer protections and forgiveness options than federal student loans. In addition, you aren’t required to refinance all your student loans—you can refinance as many or as few as you prefer.

If you have private student loans, review other refinancing institutions annually to see if they could create a better pay-off plan. I rarely recommend clients refinance their federal student loans into private loans because programs such as deferment and forgiveness may be unavailable if you refinance. Some programs can be created that a private lender may not adhere to. We saw this during the pandemic with the COVID relief payment options.

Natalie Slagle, CFP®

Lenders to consolidate private student loans

When choosing a lender to consolidate private student loans, it’s important to consider factors such as interest rates, repayment terms, fees, and any additional benefits that may be offered. We’ve researched and compiled a list of some of the best lenders for consolidating student loans below.

| Lender | Rates (APR) | Terms |

| Credible | Varies by lender | Varies by lender |

| Earnest | Starting at 5.19% | 5 – 20 years |

| RISLA | Starting at 6.34% | 5, 10, or 15 years |

Credible: Best marketplace

LendEDU rating: 4.8 out of 5

- Easily compare multiple offers

- Quick online application

- No impact on your credit score

Credible operates as a marketplace for borrowers looking to consolidate their private student loans.

After submitting an online application, borrowers can compare real offers from lenders they were determined to be eligible with. This feature makes finding the best terms easier than applying with each lender individually.

Earnest: Best skip-a-payment benefit

LendEDU rating: 4.6 out of 5

- Customizable loan terms

- Skip one payment annually, if needed

- Check your rate without impacting your credit

Earnest can consolidate federal and private student loans into a new, highly customizable loan. Borrowers can choose a payment that fits their budget while selecting biweekly or monthly payments. There are no fees for making extra payments and the payment date can be adjusted if needed.

RISLA: Best hardship protections

LendEDU rating: 4.4 out of 5

- Focus on borrower protections

- Competitive interest rates

- Non-profit lender

RISLA (Rhode Island Student Loan Authority) is a non-profit lender that offers significant borrower protections, making it a reliable choice for those concerned about unexpected financial hardships.

Its sole focus is on educational loans meaning it understands the unique needs of borrowers, which allows it to offer terms and features that are uncommon with other private lenders, such as temporary income-based repayment and military benefits.

Pros and cons of private student loan consolidation

Private student loans can lead to lower interest rates and simplify your loan payments. However, remember that it can mean giving up certain borrower protections and generally requires at least a good credit score. Here are the pros and cons to keep in mind for private student loan consolidation.

Pros

-

Lower interest rates

Private student loan consolidation can help you secure a lower interest rate, potentially lowering your monthly payment and the total interest you pay.

-

Simplifies your payments

Instead of making multiple payments, you might have a single monthly payment.

-

Choose your loan term

You can potentially choose from multiple loan terms and find one that aligns with your needs.

-

Release a cosigner

If you had a cosigner on an older loan and your credit has since improved, refinancing may allow you to release the co-signer from their financial obligation.

Cons

-

Loss of federal protections

Private student loans don’t qualify for the same protections as federal student loans, such as income-driven repayment, deferment, and forgiveness programs.

-

Interest rate risk

Interest rates change frequently. You could have a higher monthly payment if your private student loan has a variable interest rate and rates increase.

-

Qualifying can be difficult

You generally need a good-to-excellent credit score to qualify for private student loans. And you may need an excellent score to qualify for the best rates.

Alternatives to private student loan consolidation

Private student loan refinancing is a great option for some, but it may not be right for you. For instance, consider these alternatives if your credit score isn’t the best or you are worried about losing federal borrower protections.

Negotiate a lower interest rate

How it works: Depending on your lender’s policies, you may be able to negotiate a lower interest rate on your existing loan. Let your lender know if your credit has improved since you first applied. Also, highlight that you have consistently made on-time payments and will continue to do so.

What you need to know: This can make your loan cheaper, and consistently on-time payments can boost your credit score. However, not all lenders will be willing to negotiate, and negotiation can lead to a loss of benefits like discounts or loyalty programs.

Make extra payments

How it works: If you have extra money available, you can make extra payments instead of just the minimum. This can lead to a big reduction in the amount of total interest you pay on your loan and a shortening of the term.

What you need to know: This alternative can lead to less money spent on interest payments and a shorter repayment timeline. It can also reduce financial stress since you will repay your debt sooner. But this will reduce the money you have available for other debt, which may have higher interest rates. Also, not all lenders allow you to make extra payments.

Look into Public Service Loan Forgiveness

How it works: Some careers offer public loan forgiveness programs for private student loans. If you qualify, working in the field for a certain period can lead to the forgiveness of your remaining loan balance.

What you need to know: Jobs that offer public service forgiveness are often rewarding professions that provide high job security. However, you typically must work in the field for 10 years to be eligible, and there can be income limitations. In addition, only certain types of loans are typically eligible, such as Direct Loans and Federal Family Education (FFEL) loans in consolidation.

About our contributors

-

Written by Bob Haegele

Written by Bob HaegeleBob Haegele has been a freelance personal finance writer since 2018. In January 2020, he turned this side hustle into a full-time job. He is passionate about helping people master topics such as investing, credit cards, and student loans.