Student loan consolidation involves paying off one or more student loans with a new one. Depending on your situation and objectives, consolidating your student loans can help you gain access to certain benefits, such as simplified payments and a lower payment amount.

However, federal and private student loan consolidation have significant differences. It’s important to understand what you can do with both and to consider the potential drawbacks. Here’s what you need to know to determine whether consolidation is right for you.

What is student loan consolidation?

Student loan consolidation refers to the process of combining multiple student loans into one. This results in a single monthly payment instead of juggling multiple due dates.

The main reasons people choose to consolidate student loans include:

- Making payments more manageable.

- Streamlining finances with just one monthly payment.

- Potentially securing a more affordable repayment term.

When you consolidate, you essentially use one new loan to pay off your loans. This process can offer you the peace of mind that comes with simplified financial management and student loan repayment.

However, you can’t reverse the process once you consolidate your loans. Understanding your situation and options is crucial to determine whether it’s right for you.

Private vs. federal student loan consolidation

Student loan consolidation can come in two forms: private or federal. Both offer the advantage of simplifying repayments, but they come with distinct features and considerations.

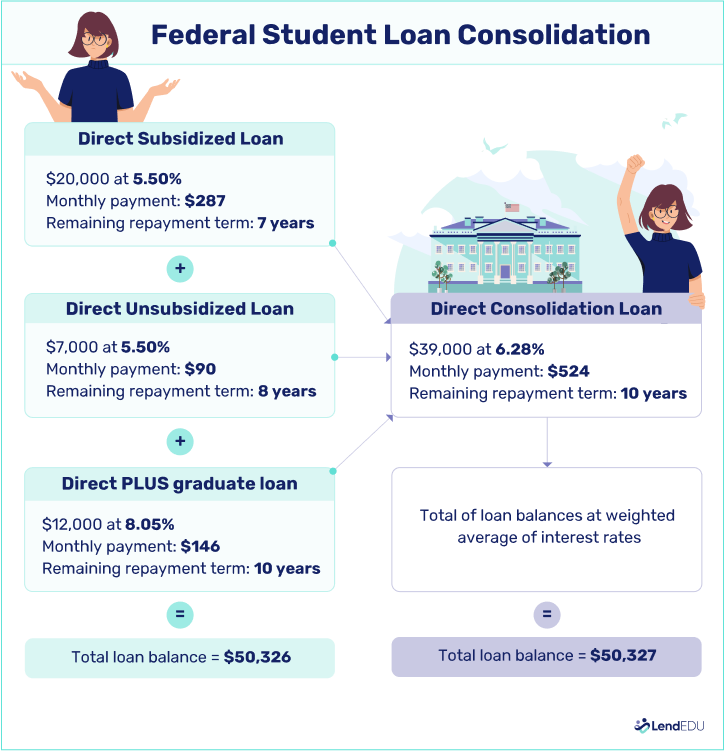

In most cases, student loan consolidation refers to the federal Direct Loan Consolidation program. It can help you simplify your monthly payments, and depending on the type of loans you have, it could also give you access to new benefits, such as income-driven repayment plans or student loan forgiveness programs. However, there’s no way to get a lower interest rate with this option.

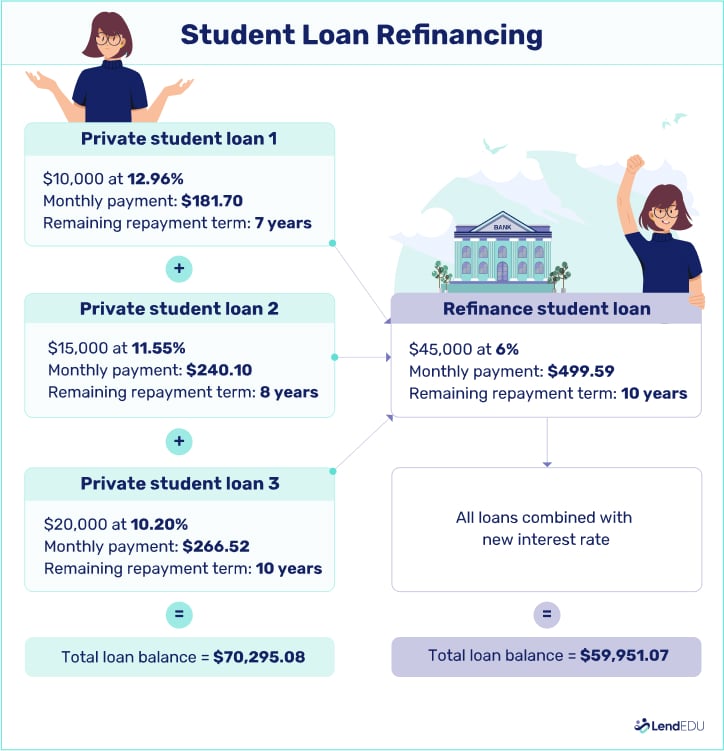

Private consolidation is typically known as student loan refinancing. This option can help you streamline monthly payments, reduce your interest rate, and save money. However, there’s no guarantee you’ll qualify, and refinancing federal loans with a private lender will cause you to lose access to federal benefits.

Here’s a breakdown of how federal and private student loan consolidation compare.

| Federal | Private | |

| Eligible loans | Federal | Federal and private |

| New interest rate | Weighted average of included loans | Vary based on credit |

| Lower monthly payment? | Yes | Yes |

| Interest savings? | No | Possibly |

| Maintain federal benefit eligibility? | Yes | No |

| Required to consolidate all student loans? | No | No |

Let’s examine how to go about consolidating each loan type and choose the right method.

How to consolidate federal student loans

The Direct Loan Consolidation program is only available to federal student loan borrowers. The program allows you to combine multiple loans into a single payment, simplifying your finances and potentially optimizing repayment terms.

However, it could even make sense to consolidate a single loan if it gives you access to certain relief options.

Eligibility requirements

You don’t need to meet credit or income requirements to get approved for a Direct Consolidation Loan. However, only certain types of loans are eligible, and your loan status is also a factor.

Loan types

Several types of federal student loans are eligible for federal consolidation. Some of the more popular loan programs include:

- Direct Loans (Subsidized, Unsubsidized, and PLUS)

- Federal Stafford Loans (Subsidized and Unsubsidized)

- Federal Perkins Loans

- Nursing Student and Faculty Loans

- Health Education Assistance Loans

Other types of federal loans might be eligible. Check the Federal Student Aid website for a comprehensive list.

Loan status

All your loans should be in their repayment phase or still within the grace period. If your loans are in default, you’ll need to meet one of two requirements to qualify:

- Make three consecutive monthly payments.

- Agree to repay your consolidation loan on an income-driven repayment plan, such as Saving on a Valuable Education (SAVE) or Pay As You Earn (PAYE).

How it works

The application process generally takes 30 minutes to complete, but knowing what to expect can help you save time. Here’s how the process works.

1. Gather necessary information

You’ll need the following information before you submit an application:

- Personal and financial details

- A verified Federal Student Aid (FSA) ID

- A list of the loans you want to consolidate and those you don’t

Your loan servicer’s website should provide the details about your loans. If you have multiple loan servicers, you can view all your federal loans in one place using the Federal Student Aid website.

2. Start the application process

To apply for a Direct Consolidation Loan, you’ll need to log in to your Federal Student Aid account. Submitting your application online will give you the fastest results, but you can also opt to print a paper application and mail it to your loan servicers.

Consolidating federal student loans could reset the clock on forgiveness programs, meaning it will take longer until you qualify for that benefit. Be sure to evaluate the pros and cons of consolidation before proceeding.

3. Choose a repayment plan

This is a pivotal decision in the process. Your options include:

- Standard repayment plan: You’ll have fixed monthly payments spread across 10 years.

- Graduated repayment plan: Payments start low and increase over time, with terms ranging from 10 to 30 years.

- Extended repayment plan: Offers fixed or graduated payments over 25 years; only available if you have more than $30,000 in debt.

- Income-driven repayment plans: Your minimum payment adjusts based on your income, with forgiveness available after 10 to 25 years, depending on the plan you choose and how much debt you have.

Get more details on federal loan repayment plans to determine which one is right for you. When choosing a plan, consider the short- and long-term impact. While a lower monthly payment can provide relief, it can make your loan more expensive over time.

Also, be sure to pick a plan based on your current income and future financial projections to ensure you can afford the payments.

How to consolidate private student loans

Consolidating private student loans and federal loans with a private lender can help you streamline your payments and lock in better interest rates.

However, the eligibility criteria and application process differ from federal consolidation. Here’s what you can expect, along with five lenders we recommend for student loan refinancing.

Eligibility requirements

Requirements for private student loan consolidation can vary depending on which lender you choose. Here are common criteria:

- Credit score: A score of 680 is a typical benchmark, but some lenders may go lower or higher than that. A higher score might yield a lower interest rate, and a lower one could limit your options.

- Income: Lenders calculate your debt-to-income ratio to determine how much of your monthly income goes toward debt payments. Some lenders also require a minimum income to get approved. For example, Citizens Bank has a minimum annual income of $24,000, while ELFI sets it at $35,000.

- Loan status: Loans should be in good standing with a history of on-time payments. Lenders may not approve you for refinancing if you’re behind on payments or in default.

- Loan amount: A minimum loan amount for refinancing is common. This is often around $10,000, but some lenders have a starting threshold of $5,000 or lower.

- Graduation status: Many lenders require at least a bachelor’s degree to refinance, but some may only require an associate degree or no degree at all. If you took out student loans but didn’t graduate, your options may be limited.

Many private lenders offer prequalification, which allows you to get an idea of your approval odds and potential loan terms without affecting your credit score.

How it works

Here are the steps you’ll take to refinance private or federal student loans with a private lender.

1. Gather your documents

You’ll typically need to provide the following documents during the application process:

- Government-issued photo ID

- Proof of income, such as a recent pay stub, or a tax return if you’re self-employed

- Current billing statement or payoff letter for each loan

Having all your paperwork on hand before you submit an application can help speed up the process.

2. Research lenders

Shopping around is the best way to ensure you get the best deal possible. Compare rates and terms from at least three lenders, focusing on financial institutions that offer no-commitment prequalification.

In addition to potential loan terms, look at eligibility requirements, repayment options, customer service, and other features that are important to you.

Private lenders may offer fixed and variable interest rates. Variable rates will fluctuate over the life of the loan, so your payments could be higher or lower over time. Fixed rates are set for the life of the loan, meaning you know exactly how much your loan will cost.

3. Choose a lender and apply

Once you’ve determined which lender is the best match, you can submit a full application through its website. Keep in mind that an official application will result in a hard credit inquiry, which can lower your credit score by a few points.

Make sure you submit any required documents on time to avoid delays.

4. Sign and wait

If the lender approves your application, you’ll get a loan agreement detailing the terms, which may be the same as your prequalification quote.

If you agree to the terms, sign the contract electronically, and the lender will pay off your loans. Keep making payments on your original loans until you’ve confirmed the payoff.

5. Begin repayments

Your lender will include your new payment date in your new loan agreement. Create an online account and set up automatic payments to ensure you don’t miss your first one.

Some lenders offer interest rate discounts when you set up autopay.

5 top lenders for private student loan consolidation

Choosing a lender means looking beyond the basics to understand each lender’s unique requirements and benefits. Here are five of our highest-rated recommendations.

Ensure your choice aligns with your unique financial situation and future plans. A lender that suits one individual may not be the best for another. Consider rates, terms, and unique benefits when making your decision.

| Lender | Best for |

| Earnest | Payment flexibility |

| SoFi® | Online lender |

| ELFI | Personalized support |

| Credible | Comparing multiple lenders |

| RISLA | Hardship protections |

Earnest: Best skip-a-payment benefit

LendEDU rating: 4.8 out of 5

- A wide range of loan amounts available

- Unique repayment flexibility, including skipping a payment once per year

- Competitive rates

Earnest offers competitive rates, wide-ranging loan amounts, and multiple term options, catering to borrowers with debt ranging from $5,000 to $500,000. Earnest also provides forbearance options, the chance to skip one payment annually, flexibility in repayment dates, and the ability to autopay on a biweekly basis to pay your loan off early.

SoFi: Best online refinancing lender

LendEDU rating: 4.9 out of 5

- Loans start at $5,000

- No minimum income threshold

- Borrowers can get a 0.25% autopay discountⓘ

With loans starting at $5,000, a range of terms, and no minimum income requirements, SoFi caters to a broad spectrum of borrowers.

You can refinance private or federal loans, undergraduate and graduate student loans, and specialized loans, such as Parent PLUS, MBA, law, and medical school loans, with SoFi. It also offers refinancing for medical residents.

ELFI: Best personalized support

LendEDU rating: 4.8 out of 5

- Every applicant gets a student loan advisor

- Options to consolidate parent and student loans

- Refinance your total outstanding balance

ELFI stands out for its stellar customer service. It assigns every applicant a dedicated student loan advisor to walk them through the process and answer questions. The lender offers competitive rates and flexible repayment term options, but its minimum loan amount is $10,000.

Its refinance loans also accommodate parents and students. Parents can transfer their federal Parent PLUS loans or private parent loans to their child, and the child can further consolidate private or federal loans using their parent as a cosigner if needed.

Credible: Best for comparing multiple offers

LendEDU rating: 4.8 out of 5

- Compare real offers with one application

- No impact on your credit to prequalify

Credible is an online marketplace where you can prequalify with multiple lenders at once, allowing you to compare offers side by side. Credible can help you save time and improve your odds of getting the best deal.

Because Credible works with several lenders, eligibility requirements and loan terms will vary depending on which lender you choose.

RISLA: Best hardship protections

LendEDU rating: 4.4 out of 5

- Immediate and deferred repayment options available

- Several hardship protections, including income-based repayment

- $40,000 income requirement

Though rooted in Rhode Island, RISLA caters to borrowers nationwide. Its standout feature is a specialized in-school refinance option, allowing students to defer payments until postgraduation. But for those eyeing lower rates, immediate repayment is an option.

RISLA is also unique among private lenders in that it offers an income-based repayment plan, allowing borrowers experiencing financial hardship to reduce their payments to just 15% of their discretionary income.

Which student loan consolidation option is best for you?

Deciding on the ideal student loan consolidation path is crucial for your financial well-being and peace of mind. The goal is to tailor the choice to your individual needs.

| When to consolidate (federal) | When to refinance (private) |

| 🏛️ You want to retain access to federal loan payment relief options | 🏦 You have private student loans and don’t qualify for federal consolidation |

| 🏛️ You’re eligible for student loan forgiveness | 🏦 You have federal loans but don’t anticipate needing access to relief options |

| 🏛️ Your credit score is in fair or poor shape | 🏦 You don’t qualify for federal loan forgiveness |

| 🏛️ You aren’t concerned if you get a slightly higher interest rate | 🏦 Your credit score and income can help you secure a lower interest rate |

When to consolidate your student loans through the government

Understanding whether to consolidate your loans with the government rather than a private lender is also crucial. When considering federal student loan consolidation, consider the following factors.

Consolidate federal loans only

Federal student loan consolidation is exclusive to federal loans. You cannot mix in private student loans with this option.

Maintain federal benefits

Federal borrowers can retain valuable benefits through the Direct Consolidation Loan program while simplifying their loan repayments into one monthly commitment. It’s about having the best of both worlds: protection and convenience.

Qualify for income-driven repayment

If you have Parent PLUS Loans, FFEL Program loans, or Perkins Loans, merging these through the Direct Consolidation Loan program can unlock doors to income-driven repayment plans that weren’t accessible before.

However, consolidating Perkins Loans will cause you to lose access to the Perkins Loan forgiveness option.

Overcome challenges with private consolidation

Federal loan consolidation sidesteps hurdles such as credit scores or employment history. If private lender consolidation isn’t feasible, this pathway offers a means to streamline repayments without these qualifiers.

Make payments more manageable, but not necessarily save money

If saving isn’t the primary goal, federal consolidation might be on the table. Your new interest rate post-consolidation mirrors the weighted average of your previous rates, rounded up to the nearest one-eighth of a percentage point.

An extended repayment span might inflate the interest over the loan’s duration, but it can be worth considering if it makes your monthly budget more manageable.

When to consolidate your student loans with a private lender

Private student loan consolidation is a solution for those with private loans, federal student loans, or a mix of both.

However, consolidating federal loans into a private one comes with specific considerations. We recommend you consider consolidating with a private lender if the following scenarios apply.

You’re eyeing a lower interest rate

A lower interest rate doesn’t just lead to manageable monthly installments—it can also mean you’ll pay less over the life of the new loan. But your credit track record and earnings will play pivotal roles in the interest rate and terms you can secure.

Private student loan consolidation can be advantageous if you have a solid credit score coupled with a stable income. Without these credentials, finding a favorable interest rate can be challenging.

Use our student loan refinance calculator to assess your potential savings through consolidation.

You’re ready to forgo federal benefits

Moving your federal loans to a private lender means you’ll relinquish unique benefits only available to federal borrowers. These include income-driven repayment plans, student loan forgiveness programs, and generous forbearance and deferment options.

If you’re already taking advantage of one of these programs or you don’t want to close the door on them in the future, think twice about refinancing.

You have a high income

Refinancing to a private lender can make sense if you have a high income and are sure you can handle the payments without the federal benefits mentioned above.

Consider refinancing if you earn more than you owe in student loan debt. For example, if you earn $100,000 per year and you owe $50,000 in student loan payments, refinancing with a private lender can make sense.

We don’t recommend moving loans out of the federal system if you owe more than you earn.

Be sure to keep abreast of student loan forgiveness programs, employer benefits (such as matching what a student pays toward their loan in an employer-sponsored retirement plan that goes into effect in 2025), and other benefits that help relieve the debt burden of education loans. And if you’re feeling overwhelmed, I recommend engaging a financial professional or counselor.

Erin Kinkade, CFP®

FAQ

Can parents consolidate the loans they took out to finance their child’s education, or is student loan consolidation only for students?

Parents and former students can take advantage of both federal and private consolidation options. Some private lenders even allow parents who took out loans to help their child to transfer that debt to the child if the child agrees to the refinance and meets the lender’s eligibility requirements.

How soon can you consolidate student loans after taking them out?

In most cases, student loan consolidation is an option as soon as your loans enter their repayment period or grace period. However, it’s wise to think about the timing. For instance, if you’re considering private refinancing, it may make sense to wait until your credit score and income are in good enough shape to qualify you for better terms.

Does it hurt your credit score to consolidate student loans?

The federal Direct Loan Consolidation program doesn’t require a credit check when you apply. If you’re considering private student loan refinancing, most lenders will let you prequalify with a soft credit inquiry, which won’t affect your credit.

However, submitting an official application will affect your credit score. Opening a new credit account can reduce your average age of accounts, which can also affect your score. But with on-time payments, your score should rebound.

Do I have to consolidate all my student loans?

Whether you’re considering federal or private student loan consolidation, you don’t need to consolidate all your loans. You can choose which loans to include based on their terms and objectives.

Should married couples consolidate student loans?

You cannot combine federal student loans with your spouse, but some private lenders allow spouses to consolidate student loans.

Consolidating joint student loans might simplify payments, but it can complicate the situation if the marriage ends or one partner dies because the other remains liable for the full loan amount. Always weigh the potential risks against the benefits.

About our contributors

-

Written by Ben Luthi

Written by Ben LuthiBen Luthi is a Salt Lake City-based freelance writer who specializes in a variety of personal finance and travel topics. He worked in banking, auto financing, insurance, and financial planning before becoming a full-time writer.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.