Falling behind on tuition payments is a common challenge for many students, with colleges and universities nationwide managing millions of dollars in past-due accounts. A recent ECSI and Higher Ed Dive Studio survey revealed that the majority of higher education institutions report an increase in past-due tuition and fees.

Unpaid tuition can lead enrollment holds, denied access to transcripts, and account collections. But several options are available to help you manage and resolve past-due tuition balances. This guide explores steps you can take, including federal and private student loan options, to address overdue tuition and continue your educational journey without interruption.

Keep going for everything you need to know on the steps to take if tuition is past due.

In case you’ve exhausted your federal financial aid, school aid package, and scholarship opportunities, and are currently in need of funding for school, here’s our list of top-rated private student loan lenders: Best Private Student Loans: Reviewed and Ranked.

Information advertised valid as of 08/10/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s).

All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit.

College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access

College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC

Information advertised valid as of 08/10/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s).

All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit.

College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access

College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC

Information advertised valid as of 08/10/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s).

All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit.

College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access

College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC

Information advertised valid as of 08/04/2026

Borrow responsibly

We encourage students and families to start with savings, grants, scholarships, and federal student loans to pay for college. Evaluate all anticipated monthly loan payments, and how much the student expects to earn in the future, before considering a private student loan.

Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000.

1. Loan application must be submitted to see available rates.

2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal.

3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024.

4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered.

7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not.

SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION.

Sallie Mae loans are made by Sallie Mae Bank.

Information advertised valid as of 08/04/2026

Borrow responsibly

We encourage students and families to start with savings, grants, scholarships, and federal student loans to pay for college. Evaluate all anticipated monthly loan payments, and how much the student expects to earn in the future, before considering a private student loan.

Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000.

1. Loan application must be submitted to see available rates.

2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal.

3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024.

4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered.

7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not.

SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION.

Sallie Mae loans are made by Sallie Mae Bank.

Information advertised valid as of 08/04/2026

Borrow responsibly

We encourage students and families to start with savings, grants, scholarships, and federal student loans to pay for college. Evaluate all anticipated monthly loan payments, and how much the student expects to earn in the future, before considering a private student loan.

Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000.

1. Loan application must be submitted to see available rates.

2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal.

3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024.

4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered.

7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not.

SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION.

Sallie Mae loans are made by Sallie Mae Bank.

Annual Percentage Rates (APRs) displayed are effective as of 08/01/2026 and reflect an Automatic Payment Discount (ACH). The ACH discount consists of 0.25% on credit-based college student loans submitted prior to 6/1/2025, a 0.5% discount for on credit-based college student loans submitted on or after 6/1/2025 and a 1.00% discount on outcomes-based loans when you enroll in automatic payments. Loans subject to individual approval, restrictions, and conditions apply. Loan features and information advertised are intended for college student loans and are subject to change at any time.

The final amount approved depends on the borrower’s credit history, verifiable cost of attendance as certified by an eligible school and is subject to credit approval and verification of application information. Lowest interest rates require full principal and interest (Immediate) payments, the shortest loan term, a cosigner, and are only available for our most creditworthy applicants and cosigners with the highest average credit scores. Actual APR offered may be higher or lower than the examples above, based on the amount of time you spend in school and any grace period you have before repayment begins. Variable rates may increase after consummation. 1% Cash Back Graduation Reward subject to terms and conditions. For details on Ascent borrower benefits, visit AscentFunding.com/

The following examples for a $10,000 loan show a 48-month in-school period plus 9 months of grace prior to a full repayment term for 60-months (variable rate), with examples of (i) Interest Only payments, (ii) $25 Minimum payments, (iii) Deferred repayment, and (iv) Immediate Repayment options.

* Interest Only Repayment: 5.89% APR, with 57 payments of $49.08 while in-school/grace, 60 payments of $192.84 during the repayment term, and a total cost of $14,368.54.

* $25 Minimum Payment: 6.52% APR, with 57 payments of $25.00 while in-school/grace, 60 payments of $233.97 during the repayment term, and a total cost of $15,463.01.

* Deferred Repayment: 6.71% APR, with no payment while in-school/grace, 60 payments of $269.84 during the repayment term, and a total cost of $16,175.28.

* Immediate Repayment: 3.64% APR, with 60 payments of $182.55, and a total cost of $10,953.09.

The following examples for a $10,000 loan show a 48-month in-school period plus 9 months of grace prior to a full repayment term for 180-months (highest variable rate), with examples of (i) Interest Only payments, (ii) $25 Minimum payments, (iii) Deferred repayment, and (iv) Immediate Repayment options.

* Interest Only Repayment: 16.30% APR, with 57 payments of $135.75 while in-school/grace, 180 payments of $148.94 during the repayment term, and a total cost of $34,546.75.

* $25 Minimum Payment: 15.07% APR, with 57 payments of $25.00 while in-school/grace, 180 payments of $256.92 during the repayment term, and a total cost of $47,672.31.

* Deferred Repayment: 15.25% APR, with no payment while in-school/grace, 180 payments of $291.22 during the repayment term, and a total cost of $51,619.42.

* Immediate Repayment: 16.05% APR, with 180 payments of $147.21, and a total cost of $26,495.61.

Annual Percentage Rates (APRs) displayed are effective as of 08/01/2026 and reflect an Automatic Payment Discount (ACH). The ACH discount consists of 0.25% on credit-based college student loans submitted prior to 6/1/2025, a 0.5% discount for on credit-based college student loans submitted on or after 6/1/2025 and a 1.00% discount on outcomes-based loans when you enroll in automatic payments. Loans subject to individual approval, restrictions, and conditions apply. Loan features and information advertised are intended for college student loans and are subject to change at any time.

The final amount approved depends on the borrower’s credit history, verifiable cost of attendance as certified by an eligible school and is subject to credit approval and verification of application information. Lowest interest rates require full principal and interest (Immediate) payments, the shortest loan term, a cosigner, and are only available for our most creditworthy applicants and cosigners with the highest average credit scores. Actual APR offered may be higher or lower than the examples above, based on the amount of time you spend in school and any grace period you have before repayment begins. Variable rates may increase after consummation. 1% Cash Back Graduation Reward subject to terms and conditions. For details on Ascent borrower benefits, visit AscentFunding.com/

The following examples for a $10,000 loan show a 48-month in-school period plus 9 months of grace prior to a full repayment term for 60-months (variable rate), with examples of (i) Interest Only payments, (ii) $25 Minimum payments, (iii) Deferred repayment, and (iv) Immediate Repayment options.

* Interest Only Repayment: 5.89% APR, with 57 payments of $49.08 while in-school/grace, 60 payments of $192.84 during the repayment term, and a total cost of $14,368.54.

* $25 Minimum Payment: 6.52% APR, with 57 payments of $25.00 while in-school/grace, 60 payments of $233.97 during the repayment term, and a total cost of $15,463.01.

* Deferred Repayment: 6.71% APR, with no payment while in-school/grace, 60 payments of $269.84 during the repayment term, and a total cost of $16,175.28.

* Immediate Repayment: 3.64% APR, with 60 payments of $182.55, and a total cost of $10,953.09.

The following examples for a $10,000 loan show a 48-month in-school period plus 9 months of grace prior to a full repayment term for 180-months (highest variable rate), with examples of (i) Interest Only payments, (ii) $25 Minimum payments, (iii) Deferred repayment, and (iv) Immediate Repayment options.

* Interest Only Repayment: 16.30% APR, with 57 payments of $135.75 while in-school/grace, 180 payments of $148.94 during the repayment term, and a total cost of $34,546.75.

* $25 Minimum Payment: 15.07% APR, with 57 payments of $25.00 while in-school/grace, 180 payments of $256.92 during the repayment term, and a total cost of $47,672.31.

* Deferred Repayment: 15.25% APR, with no payment while in-school/grace, 180 payments of $291.22 during the repayment term, and a total cost of $51,619.42.

* Immediate Repayment: 16.05% APR, with 180 payments of $147.21, and a total cost of $26,495.61.

Annual Percentage Rates (APRs) displayed are effective as of 08/01/2026 and reflect an Automatic Payment Discount (ACH). The ACH discount consists of 0.25% on credit-based college student loans submitted prior to 6/1/2025, a 0.5% discount for on credit-based college student loans submitted on or after 6/1/2025 and a 1.00% discount on outcomes-based loans when you enroll in automatic payments. Loans subject to individual approval, restrictions, and conditions apply. Loan features and information advertised are intended for college student loans and are subject to change at any time.

The final amount approved depends on the borrower’s credit history, verifiable cost of attendance as certified by an eligible school and is subject to credit approval and verification of application information. Lowest interest rates require full principal and interest (Immediate) payments, the shortest loan term, a cosigner, and are only available for our most creditworthy applicants and cosigners with the highest average credit scores. Actual APR offered may be higher or lower than the examples above, based on the amount of time you spend in school and any grace period you have before repayment begins. Variable rates may increase after consummation. 1% Cash Back Graduation Reward subject to terms and conditions. For details on Ascent borrower benefits, visit AscentFunding.com/

The following examples for a $10,000 loan show a 48-month in-school period plus 9 months of grace prior to a full repayment term for 60-months (variable rate), with examples of (i) Interest Only payments, (ii) $25 Minimum payments, (iii) Deferred repayment, and (iv) Immediate Repayment options.

* Interest Only Repayment: 5.89% APR, with 57 payments of $49.08 while in-school/grace, 60 payments of $192.84 during the repayment term, and a total cost of $14,368.54.

* $25 Minimum Payment: 6.52% APR, with 57 payments of $25.00 while in-school/grace, 60 payments of $233.97 during the repayment term, and a total cost of $15,463.01.

* Deferred Repayment: 6.71% APR, with no payment while in-school/grace, 60 payments of $269.84 during the repayment term, and a total cost of $16,175.28.

* Immediate Repayment: 3.64% APR, with 60 payments of $182.55, and a total cost of $10,953.09.

The following examples for a $10,000 loan show a 48-month in-school period plus 9 months of grace prior to a full repayment term for 180-months (highest variable rate), with examples of (i) Interest Only payments, (ii) $25 Minimum payments, (iii) Deferred repayment, and (iv) Immediate Repayment options.

* Interest Only Repayment: 16.30% APR, with 57 payments of $135.75 while in-school/grace, 180 payments of $148.94 during the repayment term, and a total cost of $34,546.75.

* $25 Minimum Payment: 15.07% APR, with 57 payments of $25.00 while in-school/grace, 180 payments of $256.92 during the repayment term, and a total cost of $47,672.31.

* Deferred Repayment: 15.25% APR, with no payment while in-school/grace, 180 payments of $291.22 during the repayment term, and a total cost of $51,619.42.

* Immediate Repayment: 16.05% APR, with 180 payments of $147.21, and a total cost of $26,495.61.

Interest Rates Disclosure

Actual rate and available repayment terms will vary based on your financial profile. Our lowest rates are only available for the most credit qualified existing cosigned loan borrowers who receive the 0.25% Loyalty discount and requires selection of our shortest term offered, full principal and interest payment while in school, and enrollment in our 0.25% Auto Pay discount. Enrolling in Auto Pay is not required as a condition for approval. Interest rates are subject to change.

Loyalty Discount

To be eligible for the Loyalty Discount, applicants must have previously obtained an Earnest Private Student Loan and apply using the same email address associated with that loan. Only one Loyalty Discount may be applied per eligible Earnest Private Student Loan. Not all applicants may qualify. This offer cannot be combined with Earnest’s Rate Match program. Earnest may modify or discontinue this offer at any time and without notice, however, once a Loyalty Discount is earned, it will not be taken away.

In-School Loans Disclosures

Earnest Private Student Loans are subject to credit approval. Before applying for private student loans, it’s best to maximize your other sources of financial aid first. It’s recommended to use a 3-step approach to assembling the funds you need: 1) Look for funds you don’t have to pay back, like scholarships, grants, and work-study opportunities. 2) Next, fill out a FAFSA® form to apply for federal student loans options. 3) Finally, consider a private student loan to cover any difference between your total cost of attendance and the amount not covered in steps 1 and 2. For more information, visit the Department of Education website at studentaid.gov.

Auto Pay Discount

You can take advantage of the Auto Pay interest rate reduction by setting up and maintaining active and automatic ACH withdrawal of your loan payment from a checking or savings account. The interest rate reduction for Auto Pay will be available only while your loan is enrolled in Auto Pay. Interest rate incentives for utilizing Auto Pay may not be combined with certain private student loan repayment programs that also offer an interest rate reduction. It is important to note that the 0.25% Auto Pay discount is not available when loan payments are deferred during the interim period as a result of selecting the deferred repayment option.

Cosigner Release

To qualify for automatic cosigner release, the outstanding principal balance of your loan must be paid down to 50% or less of the original principal balance. The primary borrower must have made 36 months of required payments after the end of the Interim Period. The primary borrower must meet our eligibility and minimum credit requirements. Additional terms and conditions may apply.

To request cosigner release, the primary borrower must have made 12 consecutive, monthly on-time principal and interest payments (or an amount equal thereto) immediately preceding the cosigner release application. The primary borrower must satisfy certain eligibility and credit criteria at the time of application. Additional terms and conditions may apply.

Grace Period

Nine-month grace period is not available for borrowers who choose our Principal and Interest Repayment plan while in school.

Loan Cost Examples

Available interest rates are subject to change. Interest rates as of 03/19/2026. Earnest’s Loan Cost Examples:

1.) These examples provide estimates based on principal and interest payments beginning immediately upon loan disbursement. Variable annual percentage rate (“”APR””): A $10,000 loan with a 15-year term (180 monthly payments of $152.84) and a 16.85% interest rate without Auto Pay (16.85% APR) would result in a total estimated payment amount of $27,511.20. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed APR: A $10,000 loan with a 15-year term (180 monthly payments of $150.30) and a 16.49% interest rate without Auto Pay (16.49% APR) would result in a total estimated payment amount of $27,054.10.

2.) These examples provide estimates based on interest-only payments while in school. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $152.84) and a 16.85% interest rate without Auto Pay (16.85% APR) would result in a total estimated payment amount of $35,515.14. For a variable loan, after your starting rate is set, your rate will then vary with the market. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $140.42 for 57 months. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $150.30) and a 16.49% interest rate without Auto Pay (16.49% APR) would result in a total estimated payment amount of $34,886.94. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $137.42 for 57 months.

3.) These examples provide estimates based on fixed $25 payments while in school. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $253.39) and a 16.85% interest rate without Auto Pay (14.92% APR) would result in a total estimated payment amount of $47,035.20. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $246.61) and a 16.49% interest rate without Auto Pay (14.65% APR) would result in a total estimated payment amount of $45,814.80. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $25.00.

4.) These examples provide estimates based on deferred payments. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $275.17) and a 16.85% interest rate without Auto Pay (14.67% APR) would result in a total estimated payment amount of $49,530.60. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $268.03) and a 16.49% interest rate without Auto Pay (14.39% APR) would result in a total estimated payment amount of $48,245.40. Your actual repayment terms may vary. Other repayment options are available. It is important to note that the 0.25% Auto Pay discount is not available when the deferred repayment option has been selected and the loan is in the interim period. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $0.

Loan Minimum

Residents of Hawaii must request a loan of at least $1,501.

Repayment Terms and Options

Repayment terms and repayment options available vary based on loan type.

Skip a Payment

Earnest clients may skip a payment through a single, one-month forbearance during a 12 month period. Your first request to skip a pay can be made once you’ve made at least 6 months of consecutive on-time full principal and interest payments, and your loan is in good standing. The interest accrued during the skipped month will result in an increase in your remaining minimum payment. The final payoff date on your loan will be extended by the length of the skipped payment periods. Any unpaid accrued interest may capitalize (added to the principal balance) at the end of the forbearance period by adding unpaid accrued interest to the outstanding principal as permitted by law and the terms of the loan agreement. Please note that skipping a payment is not guaranteed and is at Earnest’s discretion. Your monthly payment and total loan cost may increase as a result of postponing your payment and extending your term.

No Fees

Earnest does not charge fees for origination, late payments, returned check, or prepayments. Florida Stamp Tax: For Florida residents, Florida documentary stamp tax is required by law, calculated as $0.35 for each $100 (or portion thereof) of the principal loan amount, the amount of which is provided in the Final Disclosure. Lender will add the stamp tax to the principal loan amount. The full amount will be paid directly to the Florida Department of Revenue. Certificate of Registration No. 78-8016373916-1.

Earnest Private Student Loans are made by FinWise Bank, Member FDIC. FinWise Bank, 756 East Winchester, Suite 100, Murray, UT 84107. Earnest student loans are serviced by Earnest Operations LLC, 300 Frank H. Ogawa Plaza, Suite 340, Oakland, CA 94612. NMLS #1204917, with support from Higher Education Loan Authority of the State of Missouri (MOHELA) (NMLS# 1442770). FinWise Bank and Earnest LLC and its subsidiaries, including Earnest Operations LLC, are not sponsored by agencies of the United States of America.

Interest Rates Disclosure

Actual rate and available repayment terms will vary based on your financial profile. Our lowest rates are only available for the most credit qualified existing cosigned loan borrowers who receive the 0.25% Loyalty discount and requires selection of our shortest term offered, full principal and interest payment while in school, and enrollment in our 0.25% Auto Pay discount. Enrolling in Auto Pay is not required as a condition for approval. Interest rates are subject to change.

Loyalty Discount

To be eligible for the Loyalty Discount, applicants must have previously obtained an Earnest Private Student Loan and apply using the same email address associated with that loan. Only one Loyalty Discount may be applied per eligible Earnest Private Student Loan. Not all applicants may qualify. This offer cannot be combined with Earnest’s Rate Match program. Earnest may modify or discontinue this offer at any time and without notice, however, once a Loyalty Discount is earned, it will not be taken away.

In-School Loans Disclosures

Earnest Private Student Loans are subject to credit approval. Before applying for private student loans, it’s best to maximize your other sources of financial aid first. It’s recommended to use a 3-step approach to assembling the funds you need: 1) Look for funds you don’t have to pay back, like scholarships, grants, and work-study opportunities. 2) Next, fill out a FAFSA® form to apply for federal student loans options. 3) Finally, consider a private student loan to cover any difference between your total cost of attendance and the amount not covered in steps 1 and 2. For more information, visit the Department of Education website at studentaid.gov.

Auto Pay Discount

You can take advantage of the Auto Pay interest rate reduction by setting up and maintaining active and automatic ACH withdrawal of your loan payment from a checking or savings account. The interest rate reduction for Auto Pay will be available only while your loan is enrolled in Auto Pay. Interest rate incentives for utilizing Auto Pay may not be combined with certain private student loan repayment programs that also offer an interest rate reduction. It is important to note that the 0.25% Auto Pay discount is not available when loan payments are deferred during the interim period as a result of selecting the deferred repayment option.

Cosigner Release

To qualify for automatic cosigner release, the outstanding principal balance of your loan must be paid down to 50% or less of the original principal balance. The primary borrower must have made 36 months of required payments after the end of the Interim Period. The primary borrower must meet our eligibility and minimum credit requirements. Additional terms and conditions may apply.

To request cosigner release, the primary borrower must have made 12 consecutive, monthly on-time principal and interest payments (or an amount equal thereto) immediately preceding the cosigner release application. The primary borrower must satisfy certain eligibility and credit criteria at the time of application. Additional terms and conditions may apply.

Grace Period

Nine-month grace period is not available for borrowers who choose our Principal and Interest Repayment plan while in school.

Loan Cost Examples

Available interest rates are subject to change. Interest rates as of 03/19/2026. Earnest’s Loan Cost Examples:

1.) These examples provide estimates based on principal and interest payments beginning immediately upon loan disbursement. Variable annual percentage rate (“”APR””): A $10,000 loan with a 15-year term (180 monthly payments of $152.84) and a 16.85% interest rate without Auto Pay (16.85% APR) would result in a total estimated payment amount of $27,511.20. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed APR: A $10,000 loan with a 15-year term (180 monthly payments of $150.30) and a 16.49% interest rate without Auto Pay (16.49% APR) would result in a total estimated payment amount of $27,054.10.

2.) These examples provide estimates based on interest-only payments while in school. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $152.84) and a 16.85% interest rate without Auto Pay (16.85% APR) would result in a total estimated payment amount of $35,515.14. For a variable loan, after your starting rate is set, your rate will then vary with the market. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $140.42 for 57 months. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $150.30) and a 16.49% interest rate without Auto Pay (16.49% APR) would result in a total estimated payment amount of $34,886.94. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $137.42 for 57 months.

3.) These examples provide estimates based on fixed $25 payments while in school. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $253.39) and a 16.85% interest rate without Auto Pay (14.92% APR) would result in a total estimated payment amount of $47,035.20. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $246.61) and a 16.49% interest rate without Auto Pay (14.65% APR) would result in a total estimated payment amount of $45,814.80. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $25.00.

4.) These examples provide estimates based on deferred payments. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $275.17) and a 16.85% interest rate without Auto Pay (14.67% APR) would result in a total estimated payment amount of $49,530.60. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $268.03) and a 16.49% interest rate without Auto Pay (14.39% APR) would result in a total estimated payment amount of $48,245.40. Your actual repayment terms may vary. Other repayment options are available. It is important to note that the 0.25% Auto Pay discount is not available when the deferred repayment option has been selected and the loan is in the interim period. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $0.

Loan Minimum

Residents of Hawaii must request a loan of at least $1,501.

Repayment Terms and Options

Repayment terms and repayment options available vary based on loan type.

Skip a Payment

Earnest clients may skip a payment through a single, one-month forbearance during a 12 month period. Your first request to skip a pay can be made once you’ve made at least 6 months of consecutive on-time full principal and interest payments, and your loan is in good standing. The interest accrued during the skipped month will result in an increase in your remaining minimum payment. The final payoff date on your loan will be extended by the length of the skipped payment periods. Any unpaid accrued interest may capitalize (added to the principal balance) at the end of the forbearance period by adding unpaid accrued interest to the outstanding principal as permitted by law and the terms of the loan agreement. Please note that skipping a payment is not guaranteed and is at Earnest’s discretion. Your monthly payment and total loan cost may increase as a result of postponing your payment and extending your term.

No Fees

Earnest does not charge fees for origination, late payments, returned check, or prepayments. Florida Stamp Tax: For Florida residents, Florida documentary stamp tax is required by law, calculated as $0.35 for each $100 (or portion thereof) of the principal loan amount, the amount of which is provided in the Final Disclosure. Lender will add the stamp tax to the principal loan amount. The full amount will be paid directly to the Florida Department of Revenue. Certificate of Registration No. 78-8016373916-1.

Earnest Private Student Loans are made by FinWise Bank, Member FDIC. FinWise Bank, 756 East Winchester, Suite 100, Murray, UT 84107. Earnest student loans are serviced by Earnest Operations LLC, 300 Frank H. Ogawa Plaza, Suite 340, Oakland, CA 94612. NMLS #1204917, with support from Higher Education Loan Authority of the State of Missouri (MOHELA) (NMLS# 1442770). FinWise Bank and Earnest LLC and its subsidiaries, including Earnest Operations LLC, are not sponsored by agencies of the United States of America.

Interest Rates Disclosure

Actual rate and available repayment terms will vary based on your financial profile. Our lowest rates are only available for the most credit qualified existing cosigned loan borrowers who receive the 0.25% Loyalty discount and requires selection of our shortest term offered, full principal and interest payment while in school, and enrollment in our 0.25% Auto Pay discount. Enrolling in Auto Pay is not required as a condition for approval. Interest rates are subject to change.

Loyalty Discount

To be eligible for the Loyalty Discount, applicants must have previously obtained an Earnest Private Student Loan and apply using the same email address associated with that loan. Only one Loyalty Discount may be applied per eligible Earnest Private Student Loan. Not all applicants may qualify. This offer cannot be combined with Earnest’s Rate Match program. Earnest may modify or discontinue this offer at any time and without notice, however, once a Loyalty Discount is earned, it will not be taken away.

In-School Loans Disclosures

Earnest Private Student Loans are subject to credit approval. Before applying for private student loans, it’s best to maximize your other sources of financial aid first. It’s recommended to use a 3-step approach to assembling the funds you need: 1) Look for funds you don’t have to pay back, like scholarships, grants, and work-study opportunities. 2) Next, fill out a FAFSA® form to apply for federal student loans options. 3) Finally, consider a private student loan to cover any difference between your total cost of attendance and the amount not covered in steps 1 and 2. For more information, visit the Department of Education website at studentaid.gov.

Auto Pay Discount

You can take advantage of the Auto Pay interest rate reduction by setting up and maintaining active and automatic ACH withdrawal of your loan payment from a checking or savings account. The interest rate reduction for Auto Pay will be available only while your loan is enrolled in Auto Pay. Interest rate incentives for utilizing Auto Pay may not be combined with certain private student loan repayment programs that also offer an interest rate reduction. It is important to note that the 0.25% Auto Pay discount is not available when loan payments are deferred during the interim period as a result of selecting the deferred repayment option.

Cosigner Release

To qualify for automatic cosigner release, the outstanding principal balance of your loan must be paid down to 50% or less of the original principal balance. The primary borrower must have made 36 months of required payments after the end of the Interim Period. The primary borrower must meet our eligibility and minimum credit requirements. Additional terms and conditions may apply.

To request cosigner release, the primary borrower must have made 12 consecutive, monthly on-time principal and interest payments (or an amount equal thereto) immediately preceding the cosigner release application. The primary borrower must satisfy certain eligibility and credit criteria at the time of application. Additional terms and conditions may apply.

Grace Period

Nine-month grace period is not available for borrowers who choose our Principal and Interest Repayment plan while in school.

Loan Cost Examples

Available interest rates are subject to change. Interest rates as of 03/19/2026. Earnest’s Loan Cost Examples:

1.) These examples provide estimates based on principal and interest payments beginning immediately upon loan disbursement. Variable annual percentage rate (“”APR””): A $10,000 loan with a 15-year term (180 monthly payments of $152.84) and a 16.85% interest rate without Auto Pay (16.85% APR) would result in a total estimated payment amount of $27,511.20. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed APR: A $10,000 loan with a 15-year term (180 monthly payments of $150.30) and a 16.49% interest rate without Auto Pay (16.49% APR) would result in a total estimated payment amount of $27,054.10.

2.) These examples provide estimates based on interest-only payments while in school. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $152.84) and a 16.85% interest rate without Auto Pay (16.85% APR) would result in a total estimated payment amount of $35,515.14. For a variable loan, after your starting rate is set, your rate will then vary with the market. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $140.42 for 57 months. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $150.30) and a 16.49% interest rate without Auto Pay (16.49% APR) would result in a total estimated payment amount of $34,886.94. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $137.42 for 57 months.

3.) These examples provide estimates based on fixed $25 payments while in school. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $253.39) and a 16.85% interest rate without Auto Pay (14.92% APR) would result in a total estimated payment amount of $47,035.20. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $246.61) and a 16.49% interest rate without Auto Pay (14.65% APR) would result in a total estimated payment amount of $45,814.80. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $25.00.

4.) These examples provide estimates based on deferred payments. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $275.17) and a 16.85% interest rate without Auto Pay (14.67% APR) would result in a total estimated payment amount of $49,530.60. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $268.03) and a 16.49% interest rate without Auto Pay (14.39% APR) would result in a total estimated payment amount of $48,245.40. Your actual repayment terms may vary. Other repayment options are available. It is important to note that the 0.25% Auto Pay discount is not available when the deferred repayment option has been selected and the loan is in the interim period. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $0.

Loan Minimum

Residents of Hawaii must request a loan of at least $1,501.

Repayment Terms and Options

Repayment terms and repayment options available vary based on loan type.

Skip a Payment

Earnest clients may skip a payment through a single, one-month forbearance during a 12 month period. Your first request to skip a pay can be made once you’ve made at least 6 months of consecutive on-time full principal and interest payments, and your loan is in good standing. The interest accrued during the skipped month will result in an increase in your remaining minimum payment. The final payoff date on your loan will be extended by the length of the skipped payment periods. Any unpaid accrued interest may capitalize (added to the principal balance) at the end of the forbearance period by adding unpaid accrued interest to the outstanding principal as permitted by law and the terms of the loan agreement. Please note that skipping a payment is not guaranteed and is at Earnest’s discretion. Your monthly payment and total loan cost may increase as a result of postponing your payment and extending your term.

No Fees

Earnest does not charge fees for origination, late payments, returned check, or prepayments. Florida Stamp Tax: For Florida residents, Florida documentary stamp tax is required by law, calculated as $0.35 for each $100 (or portion thereof) of the principal loan amount, the amount of which is provided in the Final Disclosure. Lender will add the stamp tax to the principal loan amount. The full amount will be paid directly to the Florida Department of Revenue. Certificate of Registration No. 78-8016373916-1.

Earnest Private Student Loans are made by FinWise Bank, Member FDIC. FinWise Bank, 756 East Winchester, Suite 100, Murray, UT 84107. Earnest student loans are serviced by Earnest Operations LLC, 300 Frank H. Ogawa Plaza, Suite 340, Oakland, CA 94612. NMLS #1204917, with support from Higher Education Loan Authority of the State of Missouri (MOHELA) (NMLS# 1442770). FinWise Bank and Earnest LLC and its subsidiaries, including Earnest Operations LLC, are not sponsored by agencies of the United States of America.

SoFi Bank, N.A. and its lending products are not endorsed by or directly affiliated with any college or university unless otherwise disclosed.

Please borrow responsibly. SoFi Private Student loans are not a substitute for federal loans, grants, and work-study programs. We encourage you to evaluate all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

Terms and Conditions Apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. SoFi Private Student loansare subject to program terms and restrictions, such as completion of a loan application and self-certification form, verification of application information, thestudent’s at least half-time enrollment in a degree program at a SoFi-participating school, and, if applicable, a co-signer. In addition, borrowers must be U.S. citizens or other eligible status, be residing in the U.S., Puerto Rico, U.S. Virgin Islands, or American Samoa, and must meet SoFi’s underwriting requirements, including verification of sufficient income to support your ability to repay. Not all repayment options may be available for all loans. Minimum loan amount is $1,000. See SoFi.com/eligibility for more information. View payment examples. Lowest rates reserved for the most creditworthy borrowers. SoFi reserves the right to modify eligibility criteria at any time. This information is current as of 3/4/2026 and is subject to change. SoFi Private Student loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891. (www.nmlsconsumeraccess.org).

Good Grades Reward: If eligible, you may receive one cash reward to a SoFi Checking and Savings account. The cash reward offered is $100 for single-semester loans and $250 for full-year loans. Additional terms and conditions apply, see https://www.sofi.com/private-student-loans/rewards-for-good-grades/ for details.

SoFi Cosigner Release Disclosure: SoFi does not offer a cosigner release program for In-School Student Loans disbursed prior to May 1, 2019. For In-School Student Loans disbursed on or after May 1, 2019 the borrower may apply for cosigner release after making 12 consecutive on-time full principal and interest payments or the equivalent thereof through a lump sum payment or payments, unless fewer payments are required in accordance with applicable law. Borrowers still must pass an underwriting review and meet all other requirements. Requirements subject to change.

0.125% Continuing Scholar Discount: Terms and conditions apply. Offer good for private student loan customers who have previously borrowed a private student loan from SoFi and are taking out a subsequent loan only, select a term and repayment type that is eligible for the discount, and is subject to lender approval. To receive the offer, you must: (1) complete a loan application with SoFi; and (2) meet SoFi’s underwriting criteria. Once conditions are met and the loan has been disbursed, the interest rate shown in the Final Disclosure Statement will include an additional 0.125% rate discount because you have borrowed a private student loan from SoFi in the past. Offer good for existing private student loan borrowers only. Offer cannot be combined with other rate discounts, with the exception of the 0.25% autopay rate discount and the 0.125% SoFi Plus Parent discount. SoFi reserves the right to change or terminate the Rate Discount Program to unenrolled participants at any time with or without notice.

SoFi Bank, N.A. and its lending products are not endorsed by or directly affiliated with any college or university unless otherwise disclosed.

Please borrow responsibly. SoFi Private Student loans are not a substitute for federal loans, grants, and work-study programs. We encourage you to evaluate all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

Terms and Conditions Apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. SoFi Private Student loansare subject to program terms and restrictions, such as completion of a loan application and self-certification form, verification of application information, thestudent’s at least half-time enrollment in a degree program at a SoFi-participating school, and, if applicable, a co-signer. In addition, borrowers must be U.S. citizens or other eligible status, be residing in the U.S., Puerto Rico, U.S. Virgin Islands, or American Samoa, and must meet SoFi’s underwriting requirements, including verification of sufficient income to support your ability to repay. Not all repayment options may be available for all loans. Minimum loan amount is $1,000. See SoFi.com/eligibility for more information. View payment examples. Lowest rates reserved for the most creditworthy borrowers. SoFi reserves the right to modify eligibility criteria at any time. This information is current as of 3/4/2026 and is subject to change. SoFi Private Student loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891. (www.nmlsconsumeraccess.org).

Good Grades Reward: If eligible, you may receive one cash reward to a SoFi Checking and Savings account. The cash reward offered is $100 for single-semester loans and $250 for full-year loans. Additional terms and conditions apply, see https://www.sofi.com/private-student-loans/rewards-for-good-grades/ for details.

SoFi Cosigner Release Disclosure: SoFi does not offer a cosigner release program for In-School Student Loans disbursed prior to May 1, 2019. For In-School Student Loans disbursed on or after May 1, 2019 the borrower may apply for cosigner release after making 12 consecutive on-time full principal and interest payments or the equivalent thereof through a lump sum payment or payments, unless fewer payments are required in accordance with applicable law. Borrowers still must pass an underwriting review and meet all other requirements. Requirements subject to change.

0.125% Continuing Scholar Discount: Terms and conditions apply. Offer good for private student loan customers who have previously borrowed a private student loan from SoFi and are taking out a subsequent loan only, select a term and repayment type that is eligible for the discount, and is subject to lender approval. To receive the offer, you must: (1) complete a loan application with SoFi; and (2) meet SoFi’s underwriting criteria. Once conditions are met and the loan has been disbursed, the interest rate shown in the Final Disclosure Statement will include an additional 0.125% rate discount because you have borrowed a private student loan from SoFi in the past. Offer good for existing private student loan borrowers only. Offer cannot be combined with other rate discounts, with the exception of the 0.25% autopay rate discount and the 0.125% SoFi Plus Parent discount. SoFi reserves the right to change or terminate the Rate Discount Program to unenrolled participants at any time with or without notice.

SoFi Bank, N.A. and its lending products are not endorsed by or directly affiliated with any college or university unless otherwise disclosed.

Please borrow responsibly. SoFi Private Student loans are not a substitute for federal loans, grants, and work-study programs. We encourage you to evaluate all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

Terms and Conditions Apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. SoFi Private Student loansare subject to program terms and restrictions, such as completion of a loan application and self-certification form, verification of application information, thestudent’s at least half-time enrollment in a degree program at a SoFi-participating school, and, if applicable, a co-signer. In addition, borrowers must be U.S. citizens or other eligible status, be residing in the U.S., Puerto Rico, U.S. Virgin Islands, or American Samoa, and must meet SoFi’s underwriting requirements, including verification of sufficient income to support your ability to repay. Not all repayment options may be available for all loans. Minimum loan amount is $1,000. See SoFi.com/eligibility for more information. View payment examples. Lowest rates reserved for the most creditworthy borrowers. SoFi reserves the right to modify eligibility criteria at any time. This information is current as of 3/4/2026 and is subject to change. SoFi Private Student loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891. (www.nmlsconsumeraccess.org).

Good Grades Reward: If eligible, you may receive one cash reward to a SoFi Checking and Savings account. The cash reward offered is $100 for single-semester loans and $250 for full-year loans. Additional terms and conditions apply, see https://www.sofi.com/private-student-loans/rewards-for-good-grades/ for details.

SoFi Cosigner Release Disclosure: SoFi does not offer a cosigner release program for In-School Student Loans disbursed prior to May 1, 2019. For In-School Student Loans disbursed on or after May 1, 2019 the borrower may apply for cosigner release after making 12 consecutive on-time full principal and interest payments or the equivalent thereof through a lump sum payment or payments, unless fewer payments are required in accordance with applicable law. Borrowers still must pass an underwriting review and meet all other requirements. Requirements subject to change.

0.125% Continuing Scholar Discount: Terms and conditions apply. Offer good for private student loan customers who have previously borrowed a private student loan from SoFi and are taking out a subsequent loan only, select a term and repayment type that is eligible for the discount, and is subject to lender approval. To receive the offer, you must: (1) complete a loan application with SoFi; and (2) meet SoFi’s underwriting criteria. Once conditions are met and the loan has been disbursed, the interest rate shown in the Final Disclosure Statement will include an additional 0.125% rate discount because you have borrowed a private student loan from SoFi in the past. Offer good for existing private student loan borrowers only. Offer cannot be combined with other rate discounts, with the exception of the 0.25% autopay rate discount and the 0.125% SoFi Plus Parent discount. SoFi reserves the right to change or terminate the Rate Discount Program to unenrolled participants at any time with or without notice.

Table of Contents

Steps to take if your tuition is past due

Here are the steps to take if you need a student loan for past-due tuition.

- Talk to your school’s financial aid office

- Claim federal student loans

- Look into emergency student loan programs

- Apply for private student loans for past-due tuition

- Consider alternatives if you aren’t eligible for federal and private student loans

Step 1: Talk to your school’s financial aid office

Before taking out new loans, consult your college’s financial aid office. They can clarify your outstanding balance and discuss repayment options, such as payment plans or deferments. Depending on your situation and the school’s policies, this can be done in person, over the phone, or via email. Choose the method that best suits your needs and availability.

Step 2: Claim federal student loans

If you’ve completed the Free Application for Federal Student Aid (FAFSA), review your award letter on the StudentAid website.

Check for any unused federal student loans that can cover your past-due tuition, adhering to federal student loan limits.

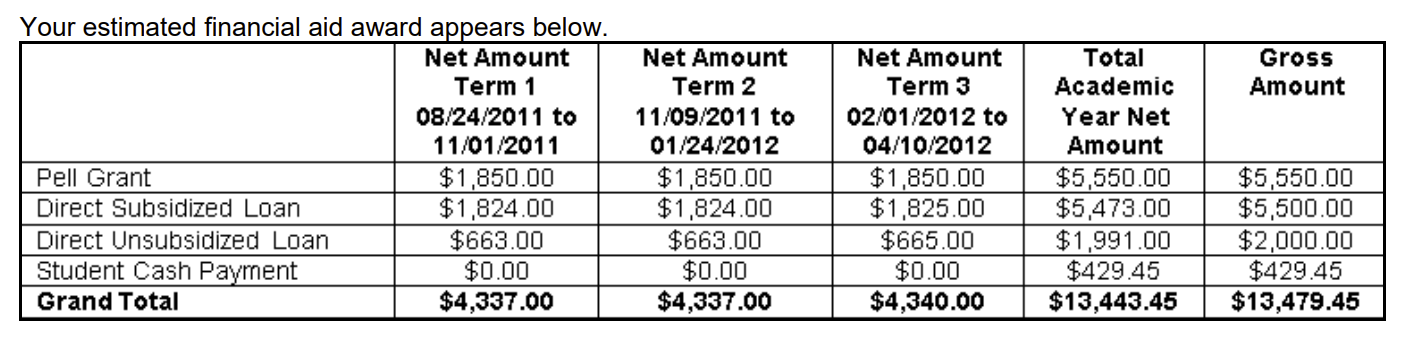

Prioritize Direct Subsidized Loans, followed by Direct Unsubsidized Loans. Graduate students should consider federal PLUS Loans as a final option.

Below is an example of what you would see in your letter that shows the loans and amounts you were awarded.

Be sure you’re clear on FAFSA deadlines, generally June 30 of the academic year (e.g., for 2025 – 2026, the deadline is June 30, 2026.) State and college deadlines may be earlier.

Submitting the FAFSA early increases your chances of receiving aid. Missing deadlines may limit your eligibility.

If you’re unable to secure federal aid for past-due tuition:

- Pause enrollment: Consider taking a break to address financial issues.

- Make payments: Work on settling your outstanding balance

- Re-enroll: Once resolved, re-enroll, ensuring compliance with your school’s specific deadlines.

Step 3: Look into emergency student loan programs

Many colleges offer emergency student aid programs to assist students facing financial hardships. These programs may include:

- Emergency loans: Short-term, often interest-free loans to cover immediate expenses.

- Grants: Funds that don’t require repayment, provided to students in need.

- Completion scholarships: Assistance to help students pay outstanding balances and complete their education.

Eligibility criteria, application processes, and available funds vary by institution. Contact your school’s financial aid office to learn about specific programs and determine your eligibility.

Organizations such as the United Negro College Fund (UNCF) offer emergency student aid programs to support students at risk of dropping out due to financial hardship.

Step 4: Apply for private student loans for past-due tuition

If federal or emergency loans aren’t viable, private student loans can help cover past-due tuition. These loans, from private lenders, are based on creditworthiness rather than financial need.

Considerations for private student loans:

- Eligibility: A good credit score is typically required. If your credit is limited or poor, a creditworthy cosigner may be necessary.

- School eligibility: Ensure your institution qualifies for private loans; some lenders have specific school criteria.

- Application timing: Unlike federal loans with strict deadlines, private student loans can be applied for at any time, making them a flexible option for addressing past-due balances.

- Lender policies on past-due balances: Some lenders allow loans to cover past-due tuition up to a certain time frame, often up to 12 months. For example, Earnest permits payment of past-due balances up to 365 days old.

Here are our highest-rated private student loans:

Information advertised valid as of 08/10/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s).

All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit.

College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access

College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC

Information advertised valid as of 08/10/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s).

All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit.

College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access

College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC

Information advertised valid as of 08/10/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s).

All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit.

College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access

College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC

Information advertised valid as of 08/04/2026

Borrow responsibly

We encourage students and families to start with savings, grants, scholarships, and federal student loans to pay for college. Evaluate all anticipated monthly loan payments, and how much the student expects to earn in the future, before considering a private student loan.

Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000.

1. Loan application must be submitted to see available rates.

2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal.

3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024.

4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered.

7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not.

SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION.

Sallie Mae loans are made by Sallie Mae Bank.

Information advertised valid as of 08/04/2026

Borrow responsibly

We encourage students and families to start with savings, grants, scholarships, and federal student loans to pay for college. Evaluate all anticipated monthly loan payments, and how much the student expects to earn in the future, before considering a private student loan.

Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000.

1. Loan application must be submitted to see available rates.

2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal.

3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024.

4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered.

7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not.

SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION.

Sallie Mae loans are made by Sallie Mae Bank.

Information advertised valid as of 08/04/2026

Borrow responsibly

We encourage students and families to start with savings, grants, scholarships, and federal student loans to pay for college. Evaluate all anticipated monthly loan payments, and how much the student expects to earn in the future, before considering a private student loan.

Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000.

1. Loan application must be submitted to see available rates.

2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal.

3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024.