Continuing education courses can help you change careers, increase income, or reenter the workforce. These courses are often a cost-effective way to enhance your career, but unless you can pay in cash, you must find a way to fund them.

Student loans can help. You might be eligible for federal, private, or both loans depending on your program and where you attend.

Information advertised valid as of 08/03/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s).

All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit.

College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access

College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC

Information advertised valid as of 08/03/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s).

All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit.

College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access

College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC

Information advertised valid as of 08/03/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s).

All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit.

College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access

College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC

Information advertised valid as of 08/04/2026

Borrow responsibly

We encourage students and families to start with savings, grants, scholarships, and federal student loans to pay for college. Evaluate all anticipated monthly loan payments, and how much the student expects to earn in the future, before considering a private student loan.

Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000.

1. Loan application must be submitted to see available rates.

2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal.

3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024.

4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered.

7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not.

SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION.

Sallie Mae loans are made by Sallie Mae Bank.

Information advertised valid as of 08/04/2026

Borrow responsibly

We encourage students and families to start with savings, grants, scholarships, and federal student loans to pay for college. Evaluate all anticipated monthly loan payments, and how much the student expects to earn in the future, before considering a private student loan.

Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000.

1. Loan application must be submitted to see available rates.

2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal.

3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024.

4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered.

7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not.

SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION.

Sallie Mae loans are made by Sallie Mae Bank.

Information advertised valid as of 08/04/2026

Borrow responsibly

We encourage students and families to start with savings, grants, scholarships, and federal student loans to pay for college. Evaluate all anticipated monthly loan payments, and how much the student expects to earn in the future, before considering a private student loan.

Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000.

1. Loan application must be submitted to see available rates.

2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal.

3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024.

4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment.

6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered.

7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not.

SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION.

Sallie Mae loans are made by Sallie Mae Bank.

Annual Percentage Rates (APRs) displayed are effective as of 08/01/2026 and reflect an Automatic Payment Discount (ACH). The ACH discount consists of 0.25% on credit-based college student loans submitted prior to 6/1/2025, a 0.5% discount for on credit-based college student loans submitted on or after 6/1/2025 and a 1.00% discount on outcomes-based loans when you enroll in automatic payments. Loans subject to individual approval, restrictions, and conditions apply. Loan features and information advertised are intended for college student loans and are subject to change at any time.

The final amount approved depends on the borrower’s credit history, verifiable cost of attendance as certified by an eligible school and is subject to credit approval and verification of application information. Lowest interest rates require full principal and interest (Immediate) payments, the shortest loan term, a cosigner, and are only available for our most creditworthy applicants and cosigners with the highest average credit scores. Actual APR offered may be higher or lower than the examples above, based on the amount of time you spend in school and any grace period you have before repayment begins. Variable rates may increase after consummation. 1% Cash Back Graduation Reward subject to terms and conditions. For details on Ascent borrower benefits, visit AscentFunding.com/

The following examples for a $10,000 loan show a 48-month in-school period plus 9 months of grace prior to a full repayment term for 60-months (variable rate), with examples of (i) Interest Only payments, (ii) $25 Minimum payments, (iii) Deferred repayment, and (iv) Immediate Repayment options.

* Interest Only Repayment: 5.89% APR, with 57 payments of $49.08 while in-school/grace, 60 payments of $192.84 during the repayment term, and a total cost of $14,368.54.

* $25 Minimum Payment: 6.52% APR, with 57 payments of $25.00 while in-school/grace, 60 payments of $233.97 during the repayment term, and a total cost of $15,463.01.

* Deferred Repayment: 6.71% APR, with no payment while in-school/grace, 60 payments of $269.84 during the repayment term, and a total cost of $16,175.28.

* Immediate Repayment: 3.64% APR, with 60 payments of $182.55, and a total cost of $10,953.09.

The following examples for a $10,000 loan show a 48-month in-school period plus 9 months of grace prior to a full repayment term for 180-months (highest variable rate), with examples of (i) Interest Only payments, (ii) $25 Minimum payments, (iii) Deferred repayment, and (iv) Immediate Repayment options.

* Interest Only Repayment: 16.30% APR, with 57 payments of $135.75 while in-school/grace, 180 payments of $148.94 during the repayment term, and a total cost of $34,546.75.

* $25 Minimum Payment: 15.07% APR, with 57 payments of $25.00 while in-school/grace, 180 payments of $256.92 during the repayment term, and a total cost of $47,672.31.

* Deferred Repayment: 15.25% APR, with no payment while in-school/grace, 180 payments of $291.22 during the repayment term, and a total cost of $51,619.42.

* Immediate Repayment: 16.05% APR, with 180 payments of $147.21, and a total cost of $26,495.61.

Annual Percentage Rates (APRs) displayed are effective as of 08/01/2026 and reflect an Automatic Payment Discount (ACH). The ACH discount consists of 0.25% on credit-based college student loans submitted prior to 6/1/2025, a 0.5% discount for on credit-based college student loans submitted on or after 6/1/2025 and a 1.00% discount on outcomes-based loans when you enroll in automatic payments. Loans subject to individual approval, restrictions, and conditions apply. Loan features and information advertised are intended for college student loans and are subject to change at any time.

The final amount approved depends on the borrower’s credit history, verifiable cost of attendance as certified by an eligible school and is subject to credit approval and verification of application information. Lowest interest rates require full principal and interest (Immediate) payments, the shortest loan term, a cosigner, and are only available for our most creditworthy applicants and cosigners with the highest average credit scores. Actual APR offered may be higher or lower than the examples above, based on the amount of time you spend in school and any grace period you have before repayment begins. Variable rates may increase after consummation. 1% Cash Back Graduation Reward subject to terms and conditions. For details on Ascent borrower benefits, visit AscentFunding.com/

The following examples for a $10,000 loan show a 48-month in-school period plus 9 months of grace prior to a full repayment term for 60-months (variable rate), with examples of (i) Interest Only payments, (ii) $25 Minimum payments, (iii) Deferred repayment, and (iv) Immediate Repayment options.

* Interest Only Repayment: 5.89% APR, with 57 payments of $49.08 while in-school/grace, 60 payments of $192.84 during the repayment term, and a total cost of $14,368.54.

* $25 Minimum Payment: 6.52% APR, with 57 payments of $25.00 while in-school/grace, 60 payments of $233.97 during the repayment term, and a total cost of $15,463.01.

* Deferred Repayment: 6.71% APR, with no payment while in-school/grace, 60 payments of $269.84 during the repayment term, and a total cost of $16,175.28.

* Immediate Repayment: 3.64% APR, with 60 payments of $182.55, and a total cost of $10,953.09.

The following examples for a $10,000 loan show a 48-month in-school period plus 9 months of grace prior to a full repayment term for 180-months (highest variable rate), with examples of (i) Interest Only payments, (ii) $25 Minimum payments, (iii) Deferred repayment, and (iv) Immediate Repayment options.

* Interest Only Repayment: 16.30% APR, with 57 payments of $135.75 while in-school/grace, 180 payments of $148.94 during the repayment term, and a total cost of $34,546.75.

* $25 Minimum Payment: 15.07% APR, with 57 payments of $25.00 while in-school/grace, 180 payments of $256.92 during the repayment term, and a total cost of $47,672.31.

* Deferred Repayment: 15.25% APR, with no payment while in-school/grace, 180 payments of $291.22 during the repayment term, and a total cost of $51,619.42.

* Immediate Repayment: 16.05% APR, with 180 payments of $147.21, and a total cost of $26,495.61.

Annual Percentage Rates (APRs) displayed are effective as of 08/01/2026 and reflect an Automatic Payment Discount (ACH). The ACH discount consists of 0.25% on credit-based college student loans submitted prior to 6/1/2025, a 0.5% discount for on credit-based college student loans submitted on or after 6/1/2025 and a 1.00% discount on outcomes-based loans when you enroll in automatic payments. Loans subject to individual approval, restrictions, and conditions apply. Loan features and information advertised are intended for college student loans and are subject to change at any time.

The final amount approved depends on the borrower’s credit history, verifiable cost of attendance as certified by an eligible school and is subject to credit approval and verification of application information. Lowest interest rates require full principal and interest (Immediate) payments, the shortest loan term, a cosigner, and are only available for our most creditworthy applicants and cosigners with the highest average credit scores. Actual APR offered may be higher or lower than the examples above, based on the amount of time you spend in school and any grace period you have before repayment begins. Variable rates may increase after consummation. 1% Cash Back Graduation Reward subject to terms and conditions. For details on Ascent borrower benefits, visit AscentFunding.com/

The following examples for a $10,000 loan show a 48-month in-school period plus 9 months of grace prior to a full repayment term for 60-months (variable rate), with examples of (i) Interest Only payments, (ii) $25 Minimum payments, (iii) Deferred repayment, and (iv) Immediate Repayment options.

* Interest Only Repayment: 5.89% APR, with 57 payments of $49.08 while in-school/grace, 60 payments of $192.84 during the repayment term, and a total cost of $14,368.54.

* $25 Minimum Payment: 6.52% APR, with 57 payments of $25.00 while in-school/grace, 60 payments of $233.97 during the repayment term, and a total cost of $15,463.01.

* Deferred Repayment: 6.71% APR, with no payment while in-school/grace, 60 payments of $269.84 during the repayment term, and a total cost of $16,175.28.

* Immediate Repayment: 3.64% APR, with 60 payments of $182.55, and a total cost of $10,953.09.

The following examples for a $10,000 loan show a 48-month in-school period plus 9 months of grace prior to a full repayment term for 180-months (highest variable rate), with examples of (i) Interest Only payments, (ii) $25 Minimum payments, (iii) Deferred repayment, and (iv) Immediate Repayment options.

* Interest Only Repayment: 16.30% APR, with 57 payments of $135.75 while in-school/grace, 180 payments of $148.94 during the repayment term, and a total cost of $34,546.75.

* $25 Minimum Payment: 15.07% APR, with 57 payments of $25.00 while in-school/grace, 180 payments of $256.92 during the repayment term, and a total cost of $47,672.31.

* Deferred Repayment: 15.25% APR, with no payment while in-school/grace, 180 payments of $291.22 during the repayment term, and a total cost of $51,619.42.

* Immediate Repayment: 16.05% APR, with 180 payments of $147.21, and a total cost of $26,495.61.

Federal student loans for continuing education

As a continuing education student, you may be eligible for various federal loans but must meet the following eligibility requirements.

- Enroll at least half-time: To qualify for federal student loans, you must enroll at least half-time, which may vary by school.

- Attend an eligible program: You must also participate in an eligible degree or certification program. You can find potential programs and confirm eligibility using the National Center of Education Statistics’ College Navigator tool.

You must complete the Free Application for Federal Student Aid (FAFSA) to check your eligibility for federal loans. Completing the application means you might be eligible for a federal loan, including Direct Subsidized Loans, Direct Unsubsidized Loans, and PLUS Loans.

| Loan | Interest rate | Annual limit |

| Subsidized Loan | 6.53% | Undergrad: $3,500–$5,500 (varies by academic year) |

| Unsubsidized Loan | 6.53% (undergrads), 8.08% (grads & professionals) | Undergrad: $5,500–$12,500; Grad: $20,500 |

| Direct PLUS Loan | 9.08% | Cost of attendance minus any financial aid |

First-year students may be eligible to borrow up to $3,500 and $5,500 for Subsidized and Unsubsidized Loans, respectively; the limit increases up to your third academic year.

Unsubsidized Loans have an exception for independent students and dependent undergrads whose parents don’t qualify for the Parent PLUS Loan: Their limits start at $9,500 versus $5,500 for dependents.

The aggregate, or combined total, limit for undergrads, graduates, and professionals are:

- Undergraduate students

- Subsidized: $23,000

- Unsubsidized: $57,500

- Graduate and professional students

- Subsidized: $65,500

- Unsubsidized: $138,500

As you search for federal student loans, ask your institution for advice. Most continuing education programs have a financial aid office or counselor who can provide guidance.

Private student loans for continuing education

Private student loans can also help with the costs of your education. Unlike federal loans, some private lenders don’t require half-time enrollment.

You usually need a good credit score to qualify for a private student loan. If you don’t have a solid credit score, you may need a cosigner to help you qualify.

Although the top private student loan lenders offer low starting rates, borrowers with poor-to-average credit scores often get approved at much higher rates than federal loans. With excellent credit, you or a cosigner may be able to take advantage of these starting rates.

Here are the top private student loan lenders for continuing education costs.

College Ave

Why we picked it

College Ave offers a Career Loan for students pursuing associate’s, bachelor’s, graduate, and graduate health degree programs. The application process is simple, and you can apply with or without a cosigner. You can also score periodic cash-back bonuses applied to your loan balance.

You can borrow enough to cover the school’s attendance cost, including funds for living expenses and school bills. You must attend at least half-time to take advantage of College Ave’s six-month grace period. This period starts when you leave school and ends when your first full payment is due.

- Get cash-back rewards for completing your program

- Borrow up to 100% of school costs

- Can attend less than half-time (but must begin immediate repayment if attending less than half-time)

| Fixed rates (APR) | 4.17% – 17.99% |

| Variable rates (APR) | 4.13% – 17.99% |

| Loan amounts | $1,000 – 100% of attendance costs |

Sallie Mae

Why we picked it

With undergraduate loans, certificate loans, and specialized graduate student loans for various professions, Sallie Mae offers the most options for continuing education. Students can attend less than half-time, which provides additional flexibility. But you or your cosigner must meet the lending requirements, including a solid credit score.

The Smart Option Student Loan feature for Career Training means you’ll apply once for a year of trade school or professional training costs. Plus, you can release a cosigner after 12 months of on-time payments—faster than most lenders.

- Quick cosigner release after 12 months of consecutive on-time payments

- Covers up to 100% of certified costs

- Get a decision between 10 and 15 minutes

| Fixed rates (APR) | 4.13% – 17.99% |

| Variable rates (APR) | 4.13% – 17.99% |

| Loan amounts | $1,000 – 100% of attendance costs |

Ascent

Why we picked it

If you’re looking for student loans for continuing education, Ascent has two options: boot camp and career loans. These loan options are for students attending professional training and certification programs at select schools. Students can also earn 1% cash back after graduating, which reduces their loan balance.

Ascent doesn’t disclose a minimum credit score, but the company states that student borrowers without cosigners must have at least two years of credit history. The minimum loan amount is $2,001; the maximum is $200,000 for undergrads and $400,000 for graduates.

- Can cover up to 100% of total costs

- Check your rate without affecting your credit

- Loans for boot camps in several career tracks

| Fixed rates (APR) | 2.89% – 14.41% |

| Variable rates (APR) | 4.34% – 14.75% |

| Loan amounts | $2,001 ($6,001 for MA) – $400,000 for graduates for credit-based loans $20,000 per school year for non-cosigned Outcomes-Based Loans ( juniors/seniors) |

Read More Best private student loans

How much could continuing education student loans cost?

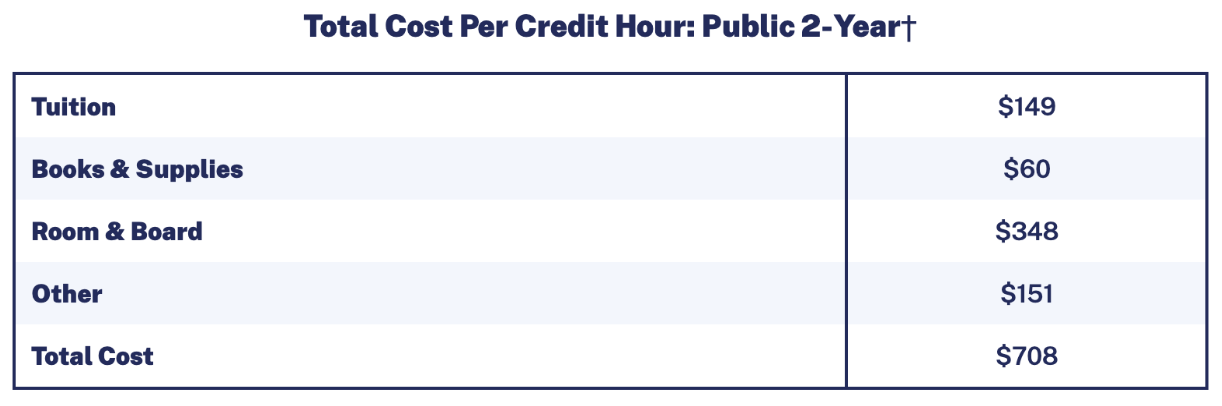

On average, your total cost to go to a two-year postsecondary institution in state would cost you $708 for each credit, according to the Education Data Initiative. That’s almost $4,300 per semester for a part-time student and $8,500 for full-timers.

When you take out student loans for continuing education, you invest in your future. Be sure you understand the long-term effects of this commitment.

The total cost of your loan goes far beyond the amount you borrowed and includes interest and fees. If we just focus on interest, we can see the implications. Interest can increase how much you pay over the life of your loan.

The two main types of interest rates are:

- Fixed: This rate and your monthly payment will remain the same throughout the life of your loan.

- Variable: This rate type can fluctuate with the markets, which means your monthly payment will also fluctuate.

If a $10,000 loan with a fixed interest rate of 5% has a standard 10-year repayment term, the total amount you repay by the end of the term includes your principal amount plus the interest accrued over the 10 years—according to our student loan calculator, it could cost an additional $2,728.

Additional loans on top of current debt

Don’t be hasty if you’re considering taking out additional student loans. The more you borrow, the more your overall debt will be, which could make paying it back more difficult.

For example, if you have a federal loan with a $15,000 balance at a 6.00% interest rate, you’re looking at a $167 monthly payment. Add another $10,000 loan at a 5.00% interest rate, and you assume another $106 monthly payment––$273 in combined monthly payments.

The average student loan borrower owes more than $40,000 in federal and private debt. So before you take on more debt:

- Use the Federal Loan Simulator or a calculator. These tools help you predict your monthly payments if you borrow. Our student loan payment calculator will tell you your monthly payment if you plug in the loan amount, interest rate, and term.

- Set a budget: Can you afford the additional monthly payments? Look for a job or career where you can earn enough to make the payments when you start repaying or set up a plan now.

- Seek alternatives: Can scholarships, grants, or employer-sponsored or work-study programs help fund your education without borrowing? Can you work through school or get a part-time job to save up?

- Understand the terms: For example, if you choose a variable-rate loan, what would your monthly payment be if you ended up paying the maximum rate at some point? Would you be able to manage?

- Explore your options: Research traditional, boot camp, or trade schools before you decide on the path you want to take.

This all comes down to cash flow and opportunity cost. The first thing to ask oneself is, “Why am I seeking continuing education?” If the answer is a higher income, look at your cash flow and continuing education costs to see whether you can afford it.

Kyle Ryan, CFP®

If you need loans, it requires balancing out what that increased income may be versus the additional cost of the education. Not all fields have a positive return on the cost of education. Deferment of loans is another important consideration. If going to school allows you to defer your loans, will you be able to get a higher-paying job once payments resume that can help you afford the cost of the additional loans?

Should you take out student loans for continuing education?

Whether you should take out student loans for continuing education depends on your situation.

Whichever decision you make, ensure that you can pay off your loans without unnecessary stress and continue to make progress in other areas of your life

| Consider continuing education loans if… | Consider an alternative if… |

| Your program shows a high earning potential. | The financial strain overshadows the benefits. |

| You’ve mapped out a repayment plan that won’t stretch you too thin. | You have cheaper options, such as online courses, scholarships, or employer-sponsored programs. |

| You qualify for favorable loan terms, such as low interest rates and practical terms you can take advantage of to pay the loan off quickly | You’re unsure about your career path, or you’re better off saving up for a few years and starting later |

How to apply for federal student loans for continuing education

Follow these steps to apply for a federal student loan.

1. Create your Federal Student Aid account

To set up an online account, enter your personal information.

2. Complete the Free Application for Federal Student Aid (FAFSA)

Fill out and submit the FAFSA by June 30 for the current school year. Your school and state deadlines vary, so check those too.

Select as many as 20 schools to find out what student aid each may offer. (You can confirm whether the U.S. Department of Education considers your school an eligible institution using the Database of Accredited Postsecondary Institutions and Programs or the Federal School Code Search.)

3. Review your FAFSA Submission Summary

It may take up to a week to process your application. Afterward, you’ll receive the FAFSA Submission Summary of financial aid you may be eligible for. Review the summary and make sure there are no mistakes.

4. Review your federal financial aid offers

The schools you chose will send you financial aid offers detailing the cost of attendance and your deadline to accept.

5. Accept your offer

Once you know where you’d like to attend, notify the school by following its instructions and accept the financial aid offers you’d need. Accept your financial aid in this order:

- Grants and scholarships

- Work-study programs

- Loans

How to apply for private student loans

Once you’ve exhausted funding through federal student loans, grants, and scholarships, if you need more funding for your continued education, you can take the following steps to apply for private student loans:

1. Provide your personal information and request a loan amount

The lender will attempt to verify your identity once you enter your personal information and details about your school or program, including when you’ll attend, attendance costs, and the loan amount you need.

2. Apply individually or with a cosigner

Many borrowers are more likely to get approved with a cosigner. The lender will allow you to apply with or without one. If you apply with a cosigner, they must fill out a separate part of the application.

Be sure your cosigner understands they’re committing to paying for your loan if you don’t.

3. Share employment information

Enter your employment status and annual income.

4. Submit the application

You can view the interest rates you prequalify for after submitting your application.

5. Accept the loan

If you’re approved, the lender will let you know when to expect funding.

Your school should get the funds on your behalf within the first few weeks of the start of the semester.

Other student loan resources for continuing education

We have more resources to assist you if you’re looking for additional help financing your continuing education.

See below for a variety of program-specific loans and financing products:

- Student loans for certificate programs: Head here if you’re enrolling in a one- or two-year program, such as an anatomical sciences education program for community college instructors.

- Student loans for non-degree programs: Check this list if you want to acquire certain skills or gain knowledge in a field but don’t intend to earn a degree or certification.

- Student loans for trade school and career training: Exploring a specific path, such as culinary school? These resources can help.

- Student loans for acting school: If you’re enrolled in a professional acting program or academy, these loan options could help cover the costs.

- Student loans for cosmetology school: Studying to become a hairstylist or makeup artist? These cosmetology program loans might be helpful.

- Student loans for coding boot camp: Coding is one of the most in-demand career paths. Use these resources to help pay for your program.

Alternatives to student loans for continuing education

You have options if you’re not sold on student loans or need additional funds. But before considering loans or alternatives, research scholarships and grants that offer free money. You might be able to find a scholarship or grant specific to your chosen career path.

Once you’ve exhausted your free options, consider the following alternatives to student loans for continuing education.

- Check with your employer: Ask whether you qualify for educational benefits. Many companies will cover all or some of the costs of continuing education courses related to your job.

- Consider other loan options: If you need additional funding, you might be able to use a personal loan, a home equity loan, a home equity line of credit (HELOC), or even a 401(k) loan. These loans might have higher interest rates than student loans and don’t have a deferment period, making them more challenging to handle while in school.

- Work a side gig: Depending on your course load and other commitments, consider whether you can work a part-time job or side gig while in school. Earning extra money each month can help offset the cost of tuition.

- Gift or loan from a family member: If this might be available to you, consider asking for assistance from friends or family through a monetary gift or a loan agreement.

Your employer is the best place to start! If the continuing education is for your current job, your workplace may be incentivized to help support your career growth.

Kyle Ryan, CFP®

FAQ

Can I use FAFSA to pay for a certificate program?

Yes, you can use the FAFSA to pay for a certificate program from an accredited institution participating in federal student aid programs. Eligible students can get federal grants, loans, and work-study funds to help cover the cost of their certificate programs. It’s important to verify the institution and program’s accreditation and federal aid eligibility before applying.

Can I get a student loan for more than my tuition?

Yes, you can get a student loan for more than your tuition. Federal and many private student loans can cover tuition and other education-related expenses, such as room and board, books, supplies, transportation, and personal expenses. The total amount you can borrow is typically capped by the cost of attendance determined by your school minus any other financial aid you receive.

How many years can you get federal student loans?

The number of years you’re eligible for federal student loans depends on the type of loan and your academic program. Federal Direct Subsidized and Unsubsidized Loans have annual and aggregate limits for undergraduate students. You may be able to take out up to 150% of the published length of your program (e.g., six years for a four-year degree). Graduate and professional student loans have annual and aggregate loan limits but no fixed number of years. Eligibility continues if you meet the requirements and haven’t exceeded the aggregate loan limits.

Does financial aid cover a second bachelor’s degree?

Financial aid can cover a second bachelor’s degree, but eligibility for certain types of aid may be limited. Federal Pell Grants, for example, are available only for the first bachelor’s degree. However, you may still be eligible for Direct Loans, federal work-study, and other federal, state, or institutional aid for a second bachelor’s degree. Check with your school’s financial aid office to understand your options and limitations.

How we chose the best student loans for continuing education

LendEDU evaluates student loan lenders to help readers find the best student loans. Our latest analysis reviewed 725 data points from 25 lenders and financial institutions, with 29 data points collected. This information is gathered from company websites, online applications, public disclosures, customer reviews, and direct communication with company representatives.

These star ratings help us determine which companies are best for different situations. We don’t believe two companies can be the best for the same purpose, so we only show each best-for designation once.

About our contributors

-

Written by Melody Stampley, CEPF®

Written by Melody Stampley, CEPF®Melody Stampley is a personal finance writer and Certified Educator in Personal Finance® with 10-plus years of combined experience in writing, editing, and finance. She specializes in credit, loans, budgeting, saving, and insurance. Melody is a mother who enjoys helping others become free and empowered to show younger generations good stewardship practices.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Reviewed by Kyle Ryan, CFP®

Reviewed by Kyle Ryan, CFP®Kyle Ryan, CFP®, ChFC®, is a co-owner and financial planner at Menninger & Associates Financial Planning. He provides his clients with financial products and services, always with his clients' individual needs foremost in his mind.