Getting a zero-interest student loan might sound like a fairytale or flat-out scam, but it’s not as far-fetched as student borrowers may think.

Zero-interest student loans aren’t very common, but they’re out there, and they’re typically available to U.S. citizens or permanent residents who have exceptional academic history, and can demonstrate financial need.

In case you’ve exhausted your federal financial aid, school aid package, and scholarship opportunities, and are currently in need of funding for school, here’s our list of top-rated private student loan lenders: Best Private Student Loans: Reviewed and Ranked.

Below, you’ll learn how zero-interest student loans work, where to find them, and how to apply.

| Company | Fixed Rates (APR) | Variable Rates (APR) | Rating (0-5) |

|---|---|---|---|

|

Terms & Disclosures

Information advertised valid as of 08/03/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s). All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit. College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC |

5.59% – 16.99% | 3.99% – 15.89% |

Terms & Disclosures

Information advertised valid as of 08/03/2026. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s). All rates shown include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit. College Ave Student Loan Servicing, LLC, NMLS#1263410 NMLS Consumer Access College Ave’s student loan products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or BTG Pactual Bank, N.A., member FDIC |

|

Terms & Disclosures

Information advertised valid as of 08/04/2026 Borrow responsibly Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000. 1. Loan application must be submitted to see available rates. 2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal. 3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024. 4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment. 5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment. 6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered. 7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not. SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION. Sallie Mae loans are made by Sallie Mae Bank. |

5.59 – 16.99 | 3.87 – 16.50% |

Terms & Disclosures

Information advertised valid as of 08/04/2026 Borrow responsibly Loans for Undergraduate & Career Training Students are not intended for graduate students and are subject to credit approval, identity verification, signed loan documents, and school certification. Student must attend a participating school. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., and apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident). Requested loan amount must be at least $1,000. 1. Loan application must be submitted to see available rates. 2. Although we do not charge you a penalty or fee if you prepay your loan, any prepayment will be applied as provided in your promissory note — first to Unpaid Fees and costs, then to Unpaid Interest, and then to Current Principal. 3. Based on a comparison of the percentage of students who were approved with a cosigner to the percentage of students who were approved without a cosigner from October 1, 2023 to September 30, 2024. 4. The borrower or cosigner must enroll in auto debit through Sallie Mae to receive a 0.25 percentage point interest rate reduction benefit. This benefit applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment. 5. Advertised APRs for undergraduate students assume a $10,000 loan with a 4-year in-school period, a 6-month grace, and the longest loan term offered. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment. 6. Savings comparison assumes a freshman student receives a $10,000 Smart Option Student Loan with the most common variable rate as of January 2025 and the longest loan term offered. 7. Examples of typical transactions for a $10,000 Smart Option Student Loan with the most common fixed rate, Fixed Repayment Option, two disbursements, a 4-year in-school period, and a 6-month grace: For a borrower with the shortest loan term, it works out to 16.16% fixed APR, 51 payments of $25.00, 119 payments of $296.32 and one payment of $41.82, for a total loan cost of $36,578.90. For a borrower with the longest loan term, it works out to 16.38% fixed APR, 51 payments of $25.00, 177 payments of $265.54 and one payment of $173.00, for a total loan cost of $48,448.58. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not. SALLIE MAE RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS, SERVICES, AND BENEFITS AT ANY TIME WITHOUT NOTICE. CHECK SALLIEMAE.COM FOR THE MOST UP-TO-DATE PRODUCT INFORMATION. Sallie Mae loans are made by Sallie Mae Bank. |

Terms & Disclosures

Interest Rates Disclosure Actual rate and available repayment terms will vary based on your financial profile. Fixed annual percentage rates (APR) range from 2.69% to 16.74% (2.19% – 16.24% with Auto Pay and Loyalty discounts). Variable annual percentage rates (APR) range from 5.24% to 17.1% (4.74% – 16.6% with Auto Pay and Loyalty discounts). Earnest variable interest rate student loans are based on a publicly available index, the 30-day Average Secured Overnight Financing Rate (SOFR) published by the Federal Reserve Bank of New York. The variable rate is based on the rate published on the 25th day, or the next business day, of the preceding calendar month, rounded to the nearest hundredth of a percent plus a margin and will change on the 1st of each month. The rate will not increase more than once a month, but there is no limit on the amount that the rate could increase at one time. Our lowest rates are only available for our most credit qualified existing cosigned loan borrowers who receive the 0.25% Loyalty discount and requires selection of our shortest term offered, full principal and interest payment while in school, and enrollment in our 0.25% Auto Pay discount. Enrolling in Auto Pay is not required as a condition for approval. Interest rates are subject to change. Loyalty Discount To be eligible for the Loyalty Discount, applicants must have previously obtained an Earnest Private Student Loan and apply using the same email address associated with that loan. Only one Loyalty Discount may be applied per eligible Earnest Private Student Loan. Not all applicants may qualify. This offer cannot be combined with Earnest’s Rate Match program. Earnest may modify or discontinue this offer at any time and without notice, however, once a Loyalty Discount is earned, it will not be taken away. In-School Loans Disclosures

Earnest Private Student Loans are subject to credit approval. Before applying for private student loans, it’s best to maximize your other sources of financial aid first. It’s recommended to use a 3-step approach to assembling the funds you need: 1) Look for funds you don’t have to pay back, like scholarships, grants, and work-study opportunities. 2) Next, fill out a FAFSA® form to apply for federal student loans options. 3) Finally, consider a private student loan to cover any difference between your total cost of attendance and the amount not covered in steps 1 and 2. For more information, visit the Department of Education website at studentaid.gov.

Auto Pay Discount

You can take advantage of the Auto Pay interest rate reduction by setting up and maintaining active and automatic ACH withdrawal of your loan payment from a checking or savings account. The interest rate reduction for Auto Pay will be available only while your loan is enrolled in Auto Pay. Interest rate incentives for utilizing Auto Pay may not be combined with certain private student loan repayment programs that also offer an interest rate reduction. It is important to note that the 0.25% Auto Pay discount is not available when loan payments are deferred during the interim period as a result of selecting the deferred repayment option.

Cosigner Release

To qualify for automatic cosigner release, the outstanding principal balance of your loan must be paid down to 50% or less of the original principal balance. The primary borrower must have made 36 months of required payments after the end of the Interim Period. The primary borrower must meet our eligibility and minimum credit requirements. Additional terms and conditions may apply.

To request cosigner release, the primary borrower must have made 12 consecutive, monthly on-time principal and interest payments (or an amount equal thereto) immediately preceding the cosigner release application. The primary borrower must satisfy certain eligibility and credit criteria at the time of application. Additional terms and conditions may apply.

Grace Period

Nine-month grace period is not available for borrowers who choose our Principal and Interest Repayment plan while in school.

Loan Cost Examples

Available interest rates are subject to change. Interest rates as of 03/19/2026. Earnest’s Loan Cost Examples:

1.) These examples provide estimates based on principal and interest payments beginning immediately upon loan disbursement. Variable annual percentage rate (“”APR””): A $10,000 loan with a 15-year term (180 monthly payments of $152.84) and a 16.85% interest rate without Auto Pay (16.85% APR) would result in a total estimated payment amount of $27,511.20. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed APR: A $10,000 loan with a 15-year term (180 monthly payments of $150.30) and a 16.49% interest rate without Auto Pay (16.49% APR) would result in a total estimated payment amount of $27,054.10.

2.) These examples provide estimates based on interest-only payments while in school. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $152.84) and a 16.85% interest rate without Auto Pay (16.85% APR) would result in a total estimated payment amount of $35,515.14. For a variable loan, after your starting rate is set, your rate will then vary with the market. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $140.42 for 57 months. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $150.30) and a 16.49% interest rate without Auto Pay (16.49% APR) would result in a total estimated payment amount of $34,886.94. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $137.42 for 57 months.

3.) These examples provide estimates based on fixed $25 payments while in school. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $253.39) and a 16.85% interest rate without Auto Pay (14.92% APR) would result in a total estimated payment amount of $47,035.20. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $246.61) and a 16.49% interest rate without Auto Pay (14.65% APR) would result in a total estimated payment amount of $45,814.80. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $25.00.

4.) These examples provide estimates based on deferred payments. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $275.17) and a 16.85% interest rate without Auto Pay (14.67% APR) would result in a total estimated payment amount of $49,530.60. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $268.03) and a 16.49% interest rate without Auto Pay (14.39% APR) would result in a total estimated payment amount of $48,245.40. Your actual repayment terms may vary. Other repayment options are available. It is important to note that the 0.25% Auto Pay discount is not available when the deferred repayment option has been selected and the loan is in the interim period. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $0.

Loan Minimum

Residents of Hawaii must request a loan of at least $1,501.

Repayment Terms and Options

Repayment terms and repayment options available vary based on loan type.

Skip a Payment

Earnest clients may skip a payment through a single, one-month forbearance during a 12 month period. Your first request to skip a pay can be made once you’ve made at least 6 months of consecutive on-time full principal and interest payments, and your loan is in good standing. The interest accrued during the skipped month will result in an increase in your remaining minimum payment. The final payoff date on your loan will be extended by the length of the skipped payment periods. Any unpaid accrued interest may capitalize (added to the principal balance) at the end of the forbearance period by adding unpaid accrued interest to the outstanding principal as permitted by law and the terms of the loan agreement. Please note that skipping a payment is not guaranteed and is at Earnest’s discretion. Your monthly payment and total loan cost may increase as a result of postponing your payment and extending your term.

No Fees

Earnest does not charge fees for origination, late payments, returned check, or prepayments. Florida Stamp Tax: For Florida residents, Florida documentary stamp tax is required by law, calculated as $0.35 for each $100 (or portion thereof) of the principal loan amount, the amount of which is provided in the Final Disclosure. Lender will add the stamp tax to the principal loan amount. The full amount will be paid directly to the Florida Department of Revenue. Certificate of Registration No. 78-8016373916-1.

Earnest Private Student Loans are made by FinWise Bank, Member FDIC. FinWise Bank, 756 East Winchester, Suite 100, Murray, UT 84107. Earnest student loans are serviced by Earnest Operations LLC, 300 Frank H. Ogawa Plaza, Suite 340, Oakland, CA 94612. NMLS #1204917, with support from Higher Education Loan Authority of the State of Missouri (MOHELA) (NMLS# 1442770). FinWise Bank and Earnest LLC and its subsidiaries, including Earnest Operations LLC, are not sponsored by agencies of the United States of America. |

5.59% – 16.99% | 3.99% – 16.85% |

Terms & Disclosures

Interest Rates Disclosure Actual rate and available repayment terms will vary based on your financial profile. Fixed annual percentage rates (APR) range from 2.69% to 16.74% (2.19% – 16.24% with Auto Pay and Loyalty discounts). Variable annual percentage rates (APR) range from 5.24% to 17.1% (4.74% – 16.6% with Auto Pay and Loyalty discounts). Earnest variable interest rate student loans are based on a publicly available index, the 30-day Average Secured Overnight Financing Rate (SOFR) published by the Federal Reserve Bank of New York. The variable rate is based on the rate published on the 25th day, or the next business day, of the preceding calendar month, rounded to the nearest hundredth of a percent plus a margin and will change on the 1st of each month. The rate will not increase more than once a month, but there is no limit on the amount that the rate could increase at one time. Our lowest rates are only available for our most credit qualified existing cosigned loan borrowers who receive the 0.25% Loyalty discount and requires selection of our shortest term offered, full principal and interest payment while in school, and enrollment in our 0.25% Auto Pay discount. Enrolling in Auto Pay is not required as a condition for approval. Interest rates are subject to change. Loyalty Discount To be eligible for the Loyalty Discount, applicants must have previously obtained an Earnest Private Student Loan and apply using the same email address associated with that loan. Only one Loyalty Discount may be applied per eligible Earnest Private Student Loan. Not all applicants may qualify. This offer cannot be combined with Earnest’s Rate Match program. Earnest may modify or discontinue this offer at any time and without notice, however, once a Loyalty Discount is earned, it will not be taken away. In-School Loans Disclosures

Earnest Private Student Loans are subject to credit approval. Before applying for private student loans, it’s best to maximize your other sources of financial aid first. It’s recommended to use a 3-step approach to assembling the funds you need: 1) Look for funds you don’t have to pay back, like scholarships, grants, and work-study opportunities. 2) Next, fill out a FAFSA® form to apply for federal student loans options. 3) Finally, consider a private student loan to cover any difference between your total cost of attendance and the amount not covered in steps 1 and 2. For more information, visit the Department of Education website at studentaid.gov.

Auto Pay Discount

You can take advantage of the Auto Pay interest rate reduction by setting up and maintaining active and automatic ACH withdrawal of your loan payment from a checking or savings account. The interest rate reduction for Auto Pay will be available only while your loan is enrolled in Auto Pay. Interest rate incentives for utilizing Auto Pay may not be combined with certain private student loan repayment programs that also offer an interest rate reduction. It is important to note that the 0.25% Auto Pay discount is not available when loan payments are deferred during the interim period as a result of selecting the deferred repayment option.

Cosigner Release

To qualify for automatic cosigner release, the outstanding principal balance of your loan must be paid down to 50% or less of the original principal balance. The primary borrower must have made 36 months of required payments after the end of the Interim Period. The primary borrower must meet our eligibility and minimum credit requirements. Additional terms and conditions may apply.

To request cosigner release, the primary borrower must have made 12 consecutive, monthly on-time principal and interest payments (or an amount equal thereto) immediately preceding the cosigner release application. The primary borrower must satisfy certain eligibility and credit criteria at the time of application. Additional terms and conditions may apply.

Grace Period

Nine-month grace period is not available for borrowers who choose our Principal and Interest Repayment plan while in school.

Loan Cost Examples

Available interest rates are subject to change. Interest rates as of 03/19/2026. Earnest’s Loan Cost Examples:

1.) These examples provide estimates based on principal and interest payments beginning immediately upon loan disbursement. Variable annual percentage rate (“”APR””): A $10,000 loan with a 15-year term (180 monthly payments of $152.84) and a 16.85% interest rate without Auto Pay (16.85% APR) would result in a total estimated payment amount of $27,511.20. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed APR: A $10,000 loan with a 15-year term (180 monthly payments of $150.30) and a 16.49% interest rate without Auto Pay (16.49% APR) would result in a total estimated payment amount of $27,054.10.

2.) These examples provide estimates based on interest-only payments while in school. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $152.84) and a 16.85% interest rate without Auto Pay (16.85% APR) would result in a total estimated payment amount of $35,515.14. For a variable loan, after your starting rate is set, your rate will then vary with the market. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $140.42 for 57 months. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $150.30) and a 16.49% interest rate without Auto Pay (16.49% APR) would result in a total estimated payment amount of $34,886.94. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $137.42 for 57 months.

3.) These examples provide estimates based on fixed $25 payments while in school. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $253.39) and a 16.85% interest rate without Auto Pay (14.92% APR) would result in a total estimated payment amount of $47,035.20. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $246.61) and a 16.49% interest rate without Auto Pay (14.65% APR) would result in a total estimated payment amount of $45,814.80. Your actual repayment terms may vary. Other repayment options are available. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $25.00.

4.) These examples provide estimates based on deferred payments. Variable interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $275.17) and a 16.85% interest rate without Auto Pay (14.67% APR) would result in a total estimated payment amount of $49,530.60. For a variable loan, after your starting rate is set, your rate will then vary with the market. Fixed interest rate: A $10,000 loan with a 15-year term (180 monthly payments of $268.03) and a 16.49% interest rate without Auto Pay (14.39% APR) would result in a total estimated payment amount of $48,245.40. Your actual repayment terms may vary. Other repayment options are available. It is important to note that the 0.25% Auto Pay discount is not available when the deferred repayment option has been selected and the loan is in the interim period. The calculation assumes that the “in-school” period is 4 years (48 months) and includes our 9 month grace period, during which the monthly payment will be $0.

Loan Minimum

Residents of Hawaii must request a loan of at least $1,501.

Repayment Terms and Options

Repayment terms and repayment options available vary based on loan type.

Skip a Payment

Earnest clients may skip a payment through a single, one-month forbearance during a 12 month period. Your first request to skip a pay can be made once you’ve made at least 6 months of consecutive on-time full principal and interest payments, and your loan is in good standing. The interest accrued during the skipped month will result in an increase in your remaining minimum payment. The final payoff date on your loan will be extended by the length of the skipped payment periods. Any unpaid accrued interest may capitalize (added to the principal balance) at the end of the forbearance period by adding unpaid accrued interest to the outstanding principal as permitted by law and the terms of the loan agreement. Please note that skipping a payment is not guaranteed and is at Earnest’s discretion. Your monthly payment and total loan cost may increase as a result of postponing your payment and extending your term.

No Fees

Earnest does not charge fees for origination, late payments, returned check, or prepayments. Florida Stamp Tax: For Florida residents, Florida documentary stamp tax is required by law, calculated as $0.35 for each $100 (or portion thereof) of the principal loan amount, the amount of which is provided in the Final Disclosure. Lender will add the stamp tax to the principal loan amount. The full amount will be paid directly to the Florida Department of Revenue. Certificate of Registration No. 78-8016373916-1.

Earnest Private Student Loans are made by FinWise Bank, Member FDIC. FinWise Bank, 756 East Winchester, Suite 100, Murray, UT 84107. Earnest student loans are serviced by Earnest Operations LLC, 300 Frank H. Ogawa Plaza, Suite 340, Oakland, CA 94612. NMLS #1204917, with support from Higher Education Loan Authority of the State of Missouri (MOHELA) (NMLS# 1442770). FinWise Bank and Earnest LLC and its subsidiaries, including Earnest Operations LLC, are not sponsored by agencies of the United States of America. |

Terms & Disclosures

SoFi Bank, N.A. and its lending products are not endorsed by or directly affiliated with any college or university unless otherwise disclosed. Please borrow responsibly. SoFi Private Student loans are not a substitute for federal loans, grants, and work-study programs. We encourage you to evaluate all your federal student aid options before you consider any private loans, including ours. Read our FAQs. Terms and Conditions Apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. SoFi Private Student loansare subject to program terms and restrictions, such as completion of a loan application and self-certification form, verification of application information, thestudent’s at least half-time enrollment in a degree program at a SoFi-participating school, and, if applicable, a co-signer. In addition, borrowers must be U.S. citizens or other eligible status, be residing in the U.S., Puerto Rico, U.S. Virgin Islands, or American Samoa, and must meet SoFi’s underwriting requirements, including verification of sufficient income to support your ability to repay. Not all repayment options may be available for all loans. Minimum loan amount is $1,000. See SoFi.com/eligibility for more information. View payment examples. Lowest rates reserved for the most creditworthy borrowers. SoFi reserves the right to modify eligibility criteria at any time. This information is current as of 3/4/2026 and is subject to change. SoFi Private Student loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891. (www.nmlsconsumeraccess.org). Good Grades Reward: If eligible, you may receive one cash reward to a SoFi Checking and Savings account. The cash reward offered is $100 for single-semester loans and $250 for full-year loans. Additional terms and conditions apply, see https://www.sofi.com/private-student-loans/rewards-for-good-grades/ for details. SoFi Cosigner Release Disclosure: SoFi does not offer a cosigner release program for In-School Student Loans disbursed prior to May 1, 2019. For In-School Student Loans disbursed on or after May 1, 2019 the borrower may apply for cosigner release after making 12 consecutive on-time full principal and interest payments or the equivalent thereof through a lump sum payment or payments, unless fewer payments are required in accordance with applicable law. Borrowers still must pass an underwriting review and meet all other requirements. Requirements subject to change. 0.125% Continuing Scholar Discount: Terms and conditions apply. Offer good for private student loan customers who have previously borrowed a private student loan from SoFi and are taking out a subsequent loan only, select a term and repayment type that is eligible for the discount, and is subject to lender approval. To receive the offer, you must: (1) complete a loan application with SoFi; and (2) meet SoFi’s underwriting criteria. Once conditions are met and the loan has been disbursed, the interest rate shown in the Final Disclosure Statement will include an additional 0.125% rate discount because you have borrowed a private student loan from SoFi in the past. Offer good for existing private student loan borrowers only. Offer cannot be combined with other rate discounts, with the exception of the 0.25% autopay rate discount and the 0.125% SoFi Plus Parent discount. SoFi reserves the right to change or terminate the Rate Discount Program to unenrolled participants at any time with or without notice. |

3.29% – 15.99% fixed-rate APR w/ autopay included | 4.64% – 16.73% variable-rate APR w/autopay included |

Terms & Disclosures

SoFi Bank, N.A. and its lending products are not endorsed by or directly affiliated with any college or university unless otherwise disclosed. Please borrow responsibly. SoFi Private Student loans are not a substitute for federal loans, grants, and work-study programs. We encourage you to evaluate all your federal student aid options before you consider any private loans, including ours. Read our FAQs. Terms and Conditions Apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. SoFi Private Student loansare subject to program terms and restrictions, such as completion of a loan application and self-certification form, verification of application information, thestudent’s at least half-time enrollment in a degree program at a SoFi-participating school, and, if applicable, a co-signer. In addition, borrowers must be U.S. citizens or other eligible status, be residing in the U.S., Puerto Rico, U.S. Virgin Islands, or American Samoa, and must meet SoFi’s underwriting requirements, including verification of sufficient income to support your ability to repay. Not all repayment options may be available for all loans. Minimum loan amount is $1,000. See SoFi.com/eligibility for more information. View payment examples. Lowest rates reserved for the most creditworthy borrowers. SoFi reserves the right to modify eligibility criteria at any time. This information is current as of 3/4/2026 and is subject to change. SoFi Private Student loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891. (www.nmlsconsumeraccess.org). Good Grades Reward: If eligible, you may receive one cash reward to a SoFi Checking and Savings account. The cash reward offered is $100 for single-semester loans and $250 for full-year loans. Additional terms and conditions apply, see https://www.sofi.com/private-student-loans/rewards-for-good-grades/ for details. SoFi Cosigner Release Disclosure: SoFi does not offer a cosigner release program for In-School Student Loans disbursed prior to May 1, 2019. For In-School Student Loans disbursed on or after May 1, 2019 the borrower may apply for cosigner release after making 12 consecutive on-time full principal and interest payments or the equivalent thereof through a lump sum payment or payments, unless fewer payments are required in accordance with applicable law. Borrowers still must pass an underwriting review and meet all other requirements. Requirements subject to change. 0.125% Continuing Scholar Discount: Terms and conditions apply. Offer good for private student loan customers who have previously borrowed a private student loan from SoFi and are taking out a subsequent loan only, select a term and repayment type that is eligible for the discount, and is subject to lender approval. To receive the offer, you must: (1) complete a loan application with SoFi; and (2) meet SoFi’s underwriting criteria. Once conditions are met and the loan has been disbursed, the interest rate shown in the Final Disclosure Statement will include an additional 0.125% rate discount because you have borrowed a private student loan from SoFi in the past. Offer good for existing private student loan borrowers only. Offer cannot be combined with other rate discounts, with the exception of the 0.25% autopay rate discount and the 0.125% SoFi Plus Parent discount. SoFi reserves the right to change or terminate the Rate Discount Program to unenrolled participants at any time with or without notice. |

|

|

5.59% – 16.99% | 3.99% – 17.99% |

|

|

|

5.59% – 16.99% | 6.75% – 17.99% |

|

Did you know? 96% of private undergraduate student loans have a cosigner.

What are zero-interest student loans?

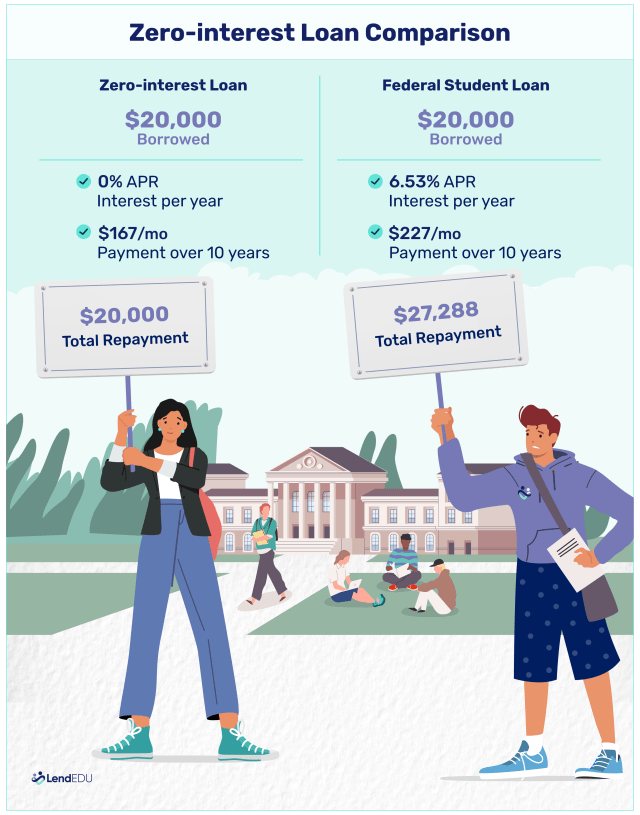

Zero-interest student loans do not charge interest—and they’re few and far between. Because this money is borrowed as an interest-free loan, the amount a student borrows is the same amount they will repay. As you might imagine, these loans are in high demand.

Although federal student loans are some of the most popular ways students finance post-secondary education, the interest on these loans can be expensive, often because of the decade-plus repayment periods. But a no-interest student loan can save a student borrower thousands over the life of the loan.

Take a look at current student loan interest rates and how much they’re costing student borrowers. As of January 2025, a college student would pay 6.53% interest for a federal Unsubsidized Loan.

With a zero-interest student loan that has a 10-year repayment term, you could save more than $7,200.

How do interest-free student loans work?

When a lender provides student borrowers with an interest-free student loan, no interest—or extra fee—accrues over the life of the loan. So whether the repayment term is five, 10, or 20 years or more, the amount originally borrowed is evenly divided over the term.

Nonprofit organizations, foundations, and institutions, such as state-run programs, often offer interest-free student loans in an effort to make higher education more accessible and affordable, encourage diversity, or boost their philanthropic footprint, image, or reputation.

Students hoping to get interest-free student loans typically must meet certain criteria, such as graduating high school, enrolling in a post-secondary program full-time, and being in good academic standing at the institution they’re attending.

Some lenders may also require potential borrowers to:

- Complete the Free Application for Federal Student Aid (FAFSA)

- Provide financial statements

- Obtain letters of recommendation

- Reside in the issuing lender’s state

- Not be in default on other student loans

- Apply with a cosigner

The process of applying for interest-free student loans is often more like an application process for a grant or scholarship. These loans may require more time, such as showing proof of residency, enrolling in a specific program—e.g., nursing or medical—submitting an essay and participating in an interview.

Since some interest-free student loans rely on information from the FAFSA, it’s usually best to seek financial aid by first completing the FAFSA, even if you don’t intend to get traditional student loans.

Once you’re approved for the zero-interest student loan, prepare to review an agreement letter from your lender explaining the repayment terms and other important information. After your loan is disbursed, you can use the funds you receive to pay for your education-related costs.

Where to find zero-interest student loans

If you want to find zero-interest student loans, start by researching “interest-free loans” and “scholarship loans.” You should also tap into your high school or college guidance counselors or financial aid office advisors, as well as local nonprofit organizations, fraternities and sororities, religious groups, and state government.

2 nonprofit organizations and charities

1. Central Scholarship

Important dates and requirements:

- Apply by the FAFSA deadline

- Be a Maryland resident

- Have a 2.8 GPA or higher

- Attend an accredited college, university, or community college

- Be a U.S. citizen or permanent resident

2. Lancaster Dollars for Higher Learning

Important dates & requirements:

- Application period is February 1 – April 30, 2025

- Must be a legal resident of Lancaster County, PA

- Must be enrolled in an eligible program at a selected institution

- A co-borrower must sign the loan agreement

2 state-sponsored programs

1. Massachusetts No Interest Loan Program

Important dates and requirements:

- Application period depends on financial aid office

- Must live in Massachusetts for at least one year and plan to remain in state

- Apply for financial aid through the FAFSA or an equivalent application

2. Abe and Annie Seibel Foundation [Texas]

Important dates and requirements:

- Application period is January 1 – February 28

- Must be a Texas resident who graduated from a Texas high school

- Enroll full-time at a Texas college or university accredited by the Southern Association of Colleges and Schools

- Top 10% of high school class, a minimum SAT score of 1100, or a minimum ACT score of 23

- Enroll full-time and maintain a 3.0 college GPA

3 religious organizations

1. Jewish Educational Loan Fund

Important dates and requirements:

- Application period is January 1 – April 30

- Must identify as Jewish

- U.S.-based cosigner

- Must be a U.S. citizen or have lawful status

- Apply for aid through FAFSA

- Legal resident of Florida, Georgia, North Carolina, South Carolina, or Virginia (not metro D.C.)

2. Riba-Free (interest-free) Educational Loans

Important dates and requirements:

- Application period is January 15 – February 28

- Must be a U.S. citizen, permanent resident, or DACA recipient

- Maintain satisfactory academic progress in college or career school

3. JFLA Zero-Interest, Zero-Fee Loan

Important dates and requirements:

- Application is currently open (for nursing and medical students); opens April 1, 2025 for all other students

- Must be at least 18 years old with a state-issued California ID

- Live in Los Angeles, Ventura, or Santa Barbara County

- Steady source of income or full-time student

- At least one qualified guarantor

How to apply for no-interest student loans

In general, here are the steps you should take when applying for no-interest student loans:

- Complete the FAFSA online: Even if you don’t want federal student loans, several lenders—including some listed above—rely on the information collected from the FAFSA to award funds. Be sure to apply for the FAFSA each year you need the loan or other financial aid.

- Research zero-interest student loans: Use state, local, and nonprofit databases, such as College Board and the Department of Education’s state webpage.

- Once you locate and decide on the interest-free loan program, check the eligibility requirements.

- If you qualify, follow the instructions to apply before the deadline.

If you don’t qualify for a zero-interest student loan, I always recommend filling out the FAFSA to see what kind of financial aid you may qualify for outside federal student loans. Schools have different scholarships or grants available—either based on merit or need-based—and you never know what you may qualify for.

Additionally, when you receive federal aid, do your best to keep spending at a minimum. Instead, look into work-study programs or even working part-time so you can use those funds to contribute to the cost of school. Search for outside scholarship opportunities through local businesses and foundations. There are several scholarships out there that are out there that people never pursue.

Alternatives to zero-interest student loans

If you don’t get anywhere in your search for zero-interest student loans, or if you don’t receive funds from any of the programs you applied to, all is not lost. You can still get financial aid via other means:

Scholarships and grants

Look up scholarships and grants, which serve as funds you don’t need to repay. Some are program-specific or based on merit. Others require you to submit an essay or run on a first-come, first-served basis.

Employer-funded continuing education

Ask your employer whether it will pay for you to go to school. Many companies cover their employees’ education, especially if it relates to their current role within the company.

Work-study programs

You can check with your college or university about working a part-time job while you attend school. If you demonstrate financial need, work-study can help you earn money to help pay for your education.

Tuition installment plans

Some colleges and universities allow their students to pay the cost of tuition and other education-related expenses during a semester in equal installments.

Tuition installment plans are typically interest-free but may include fees for setup and enrollment. Nevertheless, this can be a significant money-saving alternative to interest-bearing loans.

Federal student loans

Apply for federal loans through Federal Student Aid for four-year college, graduate, trade, career or technical school, or community college.

You could qualify for:

- Direct Subsidized Loans: Interest is covered while you’re attending school and up to six months afterward

- Direct Unsubsidized Loans: Interest accrues from the moment you get the loan.

Apply for Direct Subsidized Loans over Direct Unsubsidized Loans whenever possible, so you pay less interest over time.

Private student loans

Several private lenders offer private student loans if you’re in need of more funding. However, private student loans can come with higher interest rates, especially if you have less-than-perfect credit—and even if you qualify for competitive rates, private loans don’t come with the benefit of potential loan forgiveness.

So make sure you exhaust all other practical options before applying for any private student loans. Should you decide to explore these loans, we recommend starting with Credible. It’s our go-to marketplace when shopping for private student loans. You can get rate quotes from several lenders without affecting your credit—at no cost to you.

Funding

You can ask family and friends for help—or even strangers. Peer-to-peer (P2P) lending is one way to raise funds for school. Basically, a group of investors pools money on crowdfunding platforms to loan you the money you need, and you then pay the loan back over time with interest.

Crowdfunding or similar ways to borrow money are relatively new, and some platforms may be better than others. Should you choose to go down this route, do your due diligence by verifying the legitimacy of the platform you’re interested in with the Securities and Exchange Commission and state regulators.

FAQ

Do student loans have interest?

Yes, most student loans, including federal and private options, accrue interest. Interest is the cost of borrowing and is added to the loan balance over time, increasing the total amount you’ll repay.

Can I get student loans with no interest until after graduation?

Yes, certain loans, such as federal Direct Subsidized Loans, don’t accrue interest while you’re enrolled at least half-time, during the grace period after graduation, or while in deferment.

However, private loans typically start accruing interest immediately, even if you defer payments. Zero-interest student loans never accrue interest, but these programs are less common and often have strict eligibility criteria, such as financial need or institutional ties.

Are zero-interest student loans better than scholarships?

Interest-free student loans are a solid way to minimize debt costs because they allow you to borrow without the added expense of interest. However, scholarships are generally a better option because they don’t require repayment at all.

While zero-interest loans are helpful for covering gaps in funding, scholarships, and grants should be your first choice to reduce your overall financial burden. Combining both options can help you manage education costs.

About our contributors

-

Written by Melody Stampley, CEPF®

Written by Melody Stampley, CEPF®Melody Stampley is a personal finance writer and Certified Educator in Personal Finance® with 10-plus years of combined experience in writing, editing, and finance. She specializes in credit, loans, budgeting, saving, and insurance. Melody is a mother who enjoys helping others become free and empowered to show younger generations good stewardship practices.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Crystal Rau, CFP®, CRPC®, AAMS®

Reviewed by Crystal Rau, CFP®, CRPC®, AAMS®Crystal Rau, CFP®, CRPC®, AAMS®, is a Certified Financial Planner based in Midland, Texas. She is the founder of Beyond Balanced Financial Planning, a fee-only registered investment advisor that helps young professionals and families balance living their ideal lives with being good stewards of their finances.