Are you ready to manage your student loans? Graduate student loan borrowers, especially those with medicine, law, or business degrees, often have more loans than undergraduates, making the debt more difficult to manage.

Refinancing these loans helps simplify your finances so you can enjoy greater flexibility and freedom. In this comprehensive guide, we’ll show you how to refinance your loans, evaluate potential lenders, and address key questions about the refinancing process.

| Company | Best for… | Rating (0-5) |

|---|---|---|

|

|

Best for comparison shopping |

|

|

Best online lender |

|

|

|

Best personalized support |

|

Terms & Disclosures

Student Loan Refinance Loans Disclosures Actual rate will vary based on your financial profile. Fixed annual percentage rates (APR) range from 4.20% APR to 10.24% APR (3.95% – 9.99% with .25% auto pay discount). Variable annual percentage rates (APR) range from 6.13% APR to 10.24% APR (5.88% – 9.99% with .25% auto pay discount). Earnest variable interest rate student loan refinance loans are based on a publicly available index, the 30-day Average Secured Overnight Financing Rate (SOFR) published by the Federal Reserve Bank of New York. The variable rate is based on the rate published on the 25th day, or the next business day, of the preceding calendar month, rounded to the nearest hundredth of a percent. The rate will not increase more than once a month, but there is no limit on the amount that the rate could increase at one time. Please note, we are not able to offer variable rate loans in AK, IL, MN, MS, NH, OH, TN, and TX. Our lowest rates are only available for our most credit qualified borrowers and requires selection of our shortest term offered and enrollment in our .25% auto pay discount from a checking or savings account. Enrolling in autopay is not required as a condition for approval.

Earnest Loans are made by Earnest Operations LLC. Earnest Operations LLC, NMLS #1204917. 300 Frank H. Ogawa Plaza, Suite 340, Oakland 94612. California Financing Law License 6054788. Visit www.earnest.com/licenses for a full list of licensed states. For California residents: Loans will be arranged or made pursuant to a California Financing Law License. Skip a payment disclosure: Earnest clients may skip a payment through a one, one-month forbearance during a 12 month period. Your first request to skip a payment can be made once you’ve made at least 6 months of consecutive on-time full principal and interest payments, and your loan is in good standing. The interest accrued during the skipped month will result in an increase in your remaining minimum payment. The final payoff date on your loan will be extended by the length of the skipped payment periods. Any unpaid accrued interest may capitalize (added to the principal balance) at the end of the forbearance period by adding unpaid accrued interest to the outstanding principal as permitted by law and the terms of the loan agreement. Interest will not be capitalized on loans originated to Michigan residents under the Regulatory Loan Act of 1963. Please be aware that a skipped payment does count toward the forbearance limits. Please note that skipping a payment is not guaranteed and is at Earnest’s discretion. Your monthly payment and total loan cost may increase as a result of postponing your payment and extending your term. |

Best skip-a-payment benefit |

Terms & Disclosures

Student Loan Refinance Loans Disclosures Actual rate will vary based on your financial profile. Fixed annual percentage rates (APR) range from 4.20% APR to 10.24% APR (3.95% – 9.99% with .25% auto pay discount). Variable annual percentage rates (APR) range from 6.13% APR to 10.24% APR (5.88% – 9.99% with .25% auto pay discount). Earnest variable interest rate student loan refinance loans are based on a publicly available index, the 30-day Average Secured Overnight Financing Rate (SOFR) published by the Federal Reserve Bank of New York. The variable rate is based on the rate published on the 25th day, or the next business day, of the preceding calendar month, rounded to the nearest hundredth of a percent. The rate will not increase more than once a month, but there is no limit on the amount that the rate could increase at one time. Please note, we are not able to offer variable rate loans in AK, IL, MN, MS, NH, OH, TN, and TX. Our lowest rates are only available for our most credit qualified borrowers and requires selection of our shortest term offered and enrollment in our .25% auto pay discount from a checking or savings account. Enrolling in autopay is not required as a condition for approval.

Earnest Loans are made by Earnest Operations LLC. Earnest Operations LLC, NMLS #1204917. 300 Frank H. Ogawa Plaza, Suite 340, Oakland 94612. California Financing Law License 6054788. Visit www.earnest.com/licenses for a full list of licensed states. For California residents: Loans will be arranged or made pursuant to a California Financing Law License. Skip a payment disclosure: Earnest clients may skip a payment through a one, one-month forbearance during a 12 month period. Your first request to skip a payment can be made once you’ve made at least 6 months of consecutive on-time full principal and interest payments, and your loan is in good standing. The interest accrued during the skipped month will result in an increase in your remaining minimum payment. The final payoff date on your loan will be extended by the length of the skipped payment periods. Any unpaid accrued interest may capitalize (added to the principal balance) at the end of the forbearance period by adding unpaid accrued interest to the outstanding principal as permitted by law and the terms of the loan agreement. Interest will not be capitalized on loans originated to Michigan residents under the Regulatory Loan Act of 1963. Please be aware that a skipped payment does count toward the forbearance limits. Please note that skipping a payment is not guaranteed and is at Earnest’s discretion. Your monthly payment and total loan cost may increase as a result of postponing your payment and extending your term. |

4 top lenders to refinance graduate student loans

Graduate student loan borrowers have distinct needs. For example, those with an advanced degree typically have more student loan debt than undergraduates.

Studying longer also means entering the workforce later, especially in specialized fields with residency, licensing, and fellowship requirements. Considering these unique circumstances, we’ve found the top lenders for graduate student loan refinancing.

Credible

Why it’s one of the best

Credible stands out as a convenient marketplace where you can research various lenders with just a soft credit check. This is particularly beneficial for graduate borrowers with limited time, helping them evaluate multiple options at once without damaging their credit.

The process with Credible is straightforward. Once you prequalify, you get personalized rate quotes from up to nine lenders simultaneously. The online tool then helps you compare their rates and terms in one place, guiding you to the lender that best suits your needs.

- Rates, terms, and eligibility requirements vary by lender. Credible does not underwrite or service loan products

- Prequalify without affecting your credit

- Get personalized rate quotes from several lenders at once

- Free online comparison tool helps you select the best lender

SoFi

Why it’s one of the best

SoFi® is our top-rated online lender, particularly for graduate student loans. High loan limits allow borrowers to refinance 100% of their remaining student loan debt.

SoFi’s repayment terms range from five to 20 years; this flexibility allows graduate borrowers to tailor loans to their specific financial situation. Additional benefits, including autopay discounts and referral rewards, make this a competitive option, all with no fees attached.

- Potential to earn referral bonusesⓘ

- Rate savings of 0.25% for automatic paymentsⓘ

- Competitive rates

Loan details

| Fixed rates (APR) | !sofi-refi-2-fixlow! – !sofi-refi-2-fixhigh! w/ all discounts |

| Variable rates (APR) | !sofi-refi-2-varlow! – !sofi-refi-2-varhigh! w/ all discounts |

| Loan amounts | !sofi-refi-2-amtrange! |

| Repayment terms | !sofi-refi-2-termlengthrange_y! |

ELFI

Why it’s one of the best

ELFI is set apart by its personalized support. Recognizing the complexities and significant debt loads associated with advanced degrees, ELFI assigns applicants a dedicated Student Loan Advisor to provide guidance and answer questions during the refinancing process.

ELFI’s reputation is reinforced by its impressive rating of 4.9 out of 5 stars on Trustpilot, based on over 2,100 reviews. Customers highlight the seamless application and loan servicing process, often crediting the assigned loan advisor for their exceptional support.

- Assigns each applicant a dedicated Student Loan Advisor to walk you through the process

- Customer reviews praise the personalized support of the Student Loan Advisor

- More stringent credit and income criteria than other lenders.

Loan details

| Rates (APR) | 4.50% – 14.22% |

| Loan amounts | $1,000 – cost of attendance |

| Repayment terms | 5 – 15 years |

Earnest

Why it’s one of the best

Earnest offers flexibility and customization for those looking to refinance graduate student loans. It allows one skipped payment per year, which is particularly useful for new professionals facing irregular income or unexpected expenses as they start their careers.

Earnest also provides exceptional control over loan terms. You can select a loan term between five and 20 years and adjust it down to the exact day. This customization helps borrowers find the perfect monthly payment to get their post-graduation budget and schedule.

- Option to skip one payment per year without penalty

- Customizable loan terms from 5 – 20 years, allowing you to adjust the term down to the day

- Rate-match guarantee: Earnest will match a lower rate and include a $100 bonus

Loan details

| Rates (APR) | 4.17% – 16.85% |

| Loan amounts | $1,000 – cost of attendance |

| Repayment terms | 5, 7, 10, 12, or 15 years |

The most common mistake people make when refinancing graduate student loans is not shopping around for preferable rates or companies they enjoy working with. Often, people seek out a friend or get a referral (which is a great start), but not getting at least three quotes is a mistake that can cost you in the long run.

Pros and cons of refinancing graduate student loans

Refinancing graduate student loans comes with both advantages and disadvantages. Understanding these pros and cons can help you decide if refinancing is the right option for you.

Pros

-

Single payment

Refinancing makes it possible to merge multiple loans into one, simplifying payments.

-

Pay less interest

You may be able to lock in lower rates, which can greatly reduce the amount of interest paid over the life of the loan.

-

Adjust monthly payments

When refinancing graduate student loans, you can choose repayment terms between five to 20 years; this allows you to adjust monthly payments up or down depending on your preference.

Cons

-

Loss of federal benefits

If you refinance federal student loans, you could lose benefits such as forbearance, loan forgiveness, and income-based repayment plans.

-

Strict credit requirements

Refinancing student loans typically requires that you have a good credit score plus a steady income, which may be a challenge for recent graduates.

-

Hard credit check

While you may be able to view initial loan terms with just a soft credit check, lenders will require a hard credit check to apply, which could temporarily lower your credit score.

Am I eligible to refinance my graduate student loans?

To refinance loans, borrowers must have already completed their graduate degree from an accredited school. Payments on already existing student loans must be current; loans that are in default cannot be refinanced. Most lenders require borrowers to be U.S. citizens or permanent residents, but exceptions do exist.

Borrowers must provide evidence of being creditworthy to refinance their loans. Lenders look for stable employment with recurring, verifiable income and a debt-to-income ratio below 50%. You’ll also need a credit score of 650 or higher, though some lenders may make an exception if you have a high income or a cosigner.

Refinancing graduate student loans isn’t for everyone; you need to check and make sure you meet the eligibility requirements before seriously considering this option.

What to look for in a graduate student loan refinancing lender

Refinancing graduate student loans requires careful consideration of various factors tailored to your situation. Here’s what to look for when assessing refinancing lenders:

- Interest rates: Look for interest rates that are lower than what your current loans offer. Reduced rates lower monthly payments and overall interest paid on the loan, which is especially beneficial for graduate borrowers with large debt loads.

- Fixed vs. variable rates: Choosing between fixed and variable interest rates is crucial. Fixed rates offer stability, while variable rates fluctuate. Recent grads who are just starting their careers may prefer having fixed rates which make budgeting easier.

- Loan amounts: As a graduate student, you might carry a higher debt burden. Look for a lender that will refinance larger amounts to align with your needs.

- Loan terms: As a recent graduate, you may want a longer term to make monthly payments more manageable. However, your high earning potential might allow for a shorter repayment term. Look for lenders who offer terms that align with your budget and financial goals.

- Specialty refinancing: Unique needs call for specialized products. Some lenders cater to specific borrowers, such as medical residents or dentists, providing options to reduce payments during residency.

Make a short list of some of the most important criteria for you using this article as a guide. Translate this criteria into one or two pointed interview questions when you’re shopping lenders. Trust your intuition when you’re talking to lenders. If something doesn’t feel right or if they’re overly pushy, move on.

Can you refinance Grad PLUS loans?

Refinancing federal graduate loans, such as Grad PLUS loans, is possible. As long as you meet the lender’s criteria, most will allow you to refinance Grad PLUS loans into a private student loan.

However, weigh the following before taking this step:

- You’ll lose federal protections: When you convert federal loans into private loans through refinancing, you forfeit borrower protections unique to federal loans. This includes access to loan forgiveness programs and income-based repayment plans.

- You need stable income: Only pursue refinancing federal loans into private loans if you have a reliable income and feel certain you won’t need federal benefits.

- Consider alternatives to refinancing: If you’re uncertain about the decision to refinance federal graduate loans, federal student loan consolidation may be a more prudent alternative. Student loan consolidation allows you to merge multiple federal loans into one, with an interest rate that is the weighted average of all of the loans you’ve consolidated. It’s similar to refinancing, but you may not achieve the same interest savings level.

While refinancing Grad PLUS loans is an option, it requires examining your personal financial stability and long-term needs. Losing federal benefits may not be suitable for every borrower, and exploring other paths, including federal consolidation, could be more fitting.

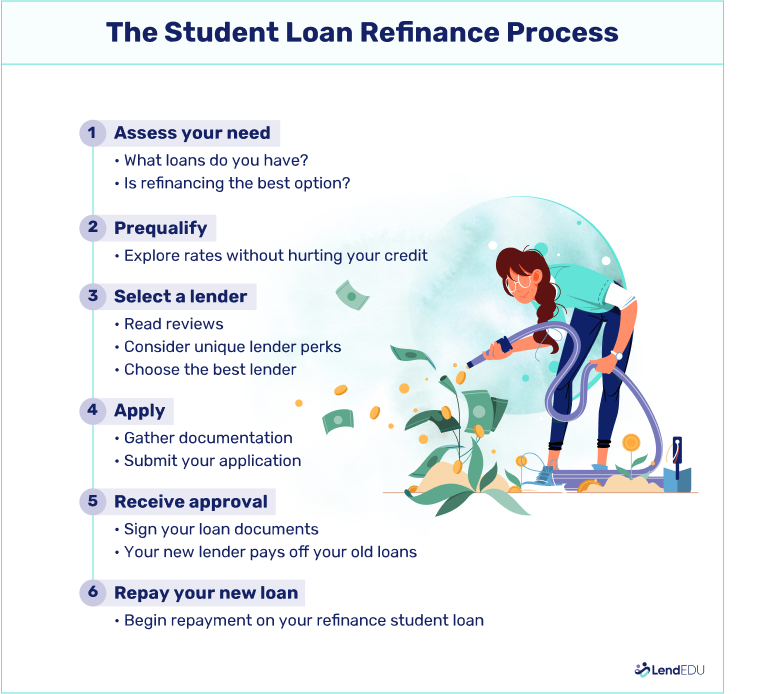

How to refinance graduate school student loans

Refinancing graduate school student loans can provide financial benefits and flexibility but requires a careful approach. Knowing the process and considering your unique situation as a graduate student borrower ensures that refinancing aligns with your financial goals.

Here’s a step-by-step guide.

By following these steps and focusing on the unique elements of graduate school student loans, you can tailor your refinancing experience and even save a significant amount over the life of your loan.

FAQ

Will refinancing hurt my credit score?

Prequalifying with lenders using a soft credit pull won’t hurt your credit score. A hard credit inquiry during the application process may lower your score by a few points, but responsibly managing the new loan can raise your credit score over time.

What factors determine my refinancing rate?

Your interest rate depends on factors such as your credit score, income, debt-to-income ratio, and the lender’s terms. It’s wise to compare offers from different lenders to find the best rate for your graduate student loan refinancing.

Can I refinance my loans more than once?

Yes, you can refinance graduate student loans multiple times if it benefits your financial situation. Consider changes in interest rates and potential costs to determine whether multiple refinances are advantageous.

What happens if I have trouble repaying my refinanced loan?

Some lenders offer forbearance or other temporary hardship options. Always communicate with your lender if you experience difficulty repaying, and understand the lender’s policies before refinancing.

Should I consolidate or refinance my graduate student loans?

Consolidation combines federal loans into one, possibly with a lower payment but not necessarily a lower interest rate. Refinancing can consolidate federal and private loans with the potential for a lower interest rate but may involve losing federal protections.

Do I need a cosigner to refinance my graduate student loans?

A cosigner is not always required. However, one might improve your chances if you have a lower credit score. Each lender has different criteria, so exploring your options and understanding each lender’s requirements is wise.

How we chose the best companies to refinance graduate student loans

LendEDU evaluates student loan companies to help readers find the best options for refinancing student loans. Our latest analysis reviewed 696 data points from 24 lenders and financial institutions, with 29 data points collected from each. This information is gathered from company websites, online applications, public disclosures, customer reviews, and direct communication with company representatives.

These star ratings help us determine which companies are best for different situations. We don’t believe two companies can be the best for the same purpose, so we only show each best-for designation once.

Recap of the best lenders to refinance graduate student loans

| Company | Best for… | Rating (0-5) |

|---|---|---|

|

|

Best for comparison shopping |

|

|

|

Best online lender |

|

|

|

Best personalized support |

|

|

Terms & Disclosures

Student Loan Refinance Loans Disclosures Actual rate will vary based on your financial profile. Fixed annual percentage rates (APR) range from 4.20% APR to 10.24% APR (3.95% – 9.99% with .25% auto pay discount). Variable annual percentage rates (APR) range from 6.13% APR to 10.24% APR (5.88% – 9.99% with .25% auto pay discount). Earnest variable interest rate student loan refinance loans are based on a publicly available index, the 30-day Average Secured Overnight Financing Rate (SOFR) published by the Federal Reserve Bank of New York. The variable rate is based on the rate published on the 25th day, or the next business day, of the preceding calendar month, rounded to the nearest hundredth of a percent. The rate will not increase more than once a month, but there is no limit on the amount that the rate could increase at one time. Please note, we are not able to offer variable rate loans in AK, IL, MN, MS, NH, OH, TN, and TX. Our lowest rates are only available for our most credit qualified borrowers and requires selection of our shortest term offered and enrollment in our .25% auto pay discount from a checking or savings account. Enrolling in autopay is not required as a condition for approval.

Earnest Loans are made by Earnest Operations LLC. Earnest Operations LLC, NMLS #1204917. 300 Frank H. Ogawa Plaza, Suite 340, Oakland 94612. California Financing Law License 6054788. Visit www.earnest.com/licenses for a full list of licensed states. For California residents: Loans will be arranged or made pursuant to a California Financing Law License. Skip a payment disclosure: Earnest clients may skip a payment through a one, one-month forbearance during a 12 month period. Your first request to skip a payment can be made once you’ve made at least 6 months of consecutive on-time full principal and interest payments, and your loan is in good standing. The interest accrued during the skipped month will result in an increase in your remaining minimum payment. The final payoff date on your loan will be extended by the length of the skipped payment periods. Any unpaid accrued interest may capitalize (added to the principal balance) at the end of the forbearance period by adding unpaid accrued interest to the outstanding principal as permitted by law and the terms of the loan agreement. Interest will not be capitalized on loans originated to Michigan residents under the Regulatory Loan Act of 1963. Please be aware that a skipped payment does count toward the forbearance limits. Please note that skipping a payment is not guaranteed and is at Earnest’s discretion. Your monthly payment and total loan cost may increase as a result of postponing your payment and extending your term. |

Best skip-a-payment benefit |

Terms & Disclosures

Student Loan Refinance Loans Disclosures Actual rate will vary based on your financial profile. Fixed annual percentage rates (APR) range from 4.20% APR to 10.24% APR (3.95% – 9.99% with .25% auto pay discount). Variable annual percentage rates (APR) range from 6.13% APR to 10.24% APR (5.88% – 9.99% with .25% auto pay discount). Earnest variable interest rate student loan refinance loans are based on a publicly available index, the 30-day Average Secured Overnight Financing Rate (SOFR) published by the Federal Reserve Bank of New York. The variable rate is based on the rate published on the 25th day, or the next business day, of the preceding calendar month, rounded to the nearest hundredth of a percent. The rate will not increase more than once a month, but there is no limit on the amount that the rate could increase at one time. Please note, we are not able to offer variable rate loans in AK, IL, MN, MS, NH, OH, TN, and TX. Our lowest rates are only available for our most credit qualified borrowers and requires selection of our shortest term offered and enrollment in our .25% auto pay discount from a checking or savings account. Enrolling in autopay is not required as a condition for approval.

Earnest Loans are made by Earnest Operations LLC. Earnest Operations LLC, NMLS #1204917. 300 Frank H. Ogawa Plaza, Suite 340, Oakland 94612. California Financing Law License 6054788. Visit www.earnest.com/licenses for a full list of licensed states. For California residents: Loans will be arranged or made pursuant to a California Financing Law License. Skip a payment disclosure: Earnest clients may skip a payment through a one, one-month forbearance during a 12 month period. Your first request to skip a payment can be made once you’ve made at least 6 months of consecutive on-time full principal and interest payments, and your loan is in good standing. The interest accrued during the skipped month will result in an increase in your remaining minimum payment. The final payoff date on your loan will be extended by the length of the skipped payment periods. Any unpaid accrued interest may capitalize (added to the principal balance) at the end of the forbearance period by adding unpaid accrued interest to the outstanding principal as permitted by law and the terms of the loan agreement. Interest will not be capitalized on loans originated to Michigan residents under the Regulatory Loan Act of 1963. Please be aware that a skipped payment does count toward the forbearance limits. Please note that skipping a payment is not guaranteed and is at Earnest’s discretion. Your monthly payment and total loan cost may increase as a result of postponing your payment and extending your term. |

About our contributors

-

Written by Christi Gorbett

Written by Christi GorbettChristi Gorbett is a finance writer with a master’s degree in English and years of experience. She specializes in creating financial content that simplifies complex topics, making them easier for a wide audience to understand.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.