Declaring bankruptcy can damage your credit, but it can also be a pathway to getting your student loans forgiven. You can’t discharge student loans under the bankruptcy code if they are: backed by the federal government or a nonprofit; a scholarship, stipend, or educational benefit you are obligated to repay; or a “qualified education loan.”

You must prove undue hardship in court to cancel the debt in these cases. However, if you can prove that a private student loan is a nonqualified education loan, you may be able to get it discharged under ordinary bankruptcy proceedings.

Therefore, you must prove undue hardship to discharge federal student loans. The process starts with filing bankruptcy and then filing a lawsuit against your lender.

Table of Contents

What is undue hardship?

When a person files for student loan bankruptcy, undue hardship refers to a financial situation where continuing to make student loan payments will unfairly affect the borrower’s and their dependents’ well-being. In these cases, with proof of undue hardship, the court system can cancel some or all of the imposing student loan debt.

However, the relief options available to borrowers differ based on the loan type, as the requirements for bankruptcy discharge vary.

Borrowers can discharge nonqualified education loans in bankruptcy without proving undue hardship. These include loans:

- Paid directly to the debtor and that exceed the cost of attendance

- For students who attended school less than half-time

- For unaccredited colleges, trade schools, or foreign schools

- For living expenses and fees during a period of medical or dentistry residency, or while studying for the bar or other professional exams

The debtor must prove undue hardship for federal student loans and private student loans considered qualified education loans.

How to prove undue hardship for student loans under the Brunner test

Where you live can affect how courts consider your student loans for discharge in bankruptcy proceedings. Many bankruptcy courts in the U.S. defer to the “Brunner test” to determine undue hardship.

The Brunner test requires debtors to show they:

- Would not be able to maintain a minimal standard of living if forced to repay the loan

- Have made good-faith efforts to repay the loan before declaring bankruptcy

- Are experiencing a financial situation that is not temporary and which they expect to persist rather than improve

How to prove undue hardship for student loans under the totality of circumstances approach

The First and Eighth Circuit Court of Appeals courts have historically used a less stringent test that considers the “totality of circumstances.”

These include courts in the following states and territories:

- Arkansas

- Iowa

- Minnesota

- Maine

- Massachusetts

- Missouri

- Nebraska

- New Hampshire

- North Dakota

- Puerto Rico

- Rhode Island

- South Dakota

The totality of circumstances approach takes into account the debtor’s:

- Past, present, and future financial circumstances

- Reasonable and necessary living expenses

- Other circumstances and relevant facts

Considered more flexible than the Brunner test, this approach results in more student loan discharges.

Even among courts that apply the Brunner test to prove undue hardship, results can vary. The Fifth Circuit (Mississippi, Louisiana, and Texas) has a reputation for applying the Brunner test so strictly that proving undue hardship is almost impossible.

For example, in 2016, a debtor who lived in Maine had her loans discharged after the court considered the totality of her circumstances. Meanwhile, a debtor in a similar situation in Texas failed because the court determined she didn’t pass the Brunner test.

How hard is it to get approved for undue hardship?

Approval can be strenuous since it requires proof in a court of law. Whether you aim to have federal or private student loans discharged, the process is the same. Unless you can prove you have a nonqualified education loan, you must first file an adversary proceeding—a lawsuit against your creditor.

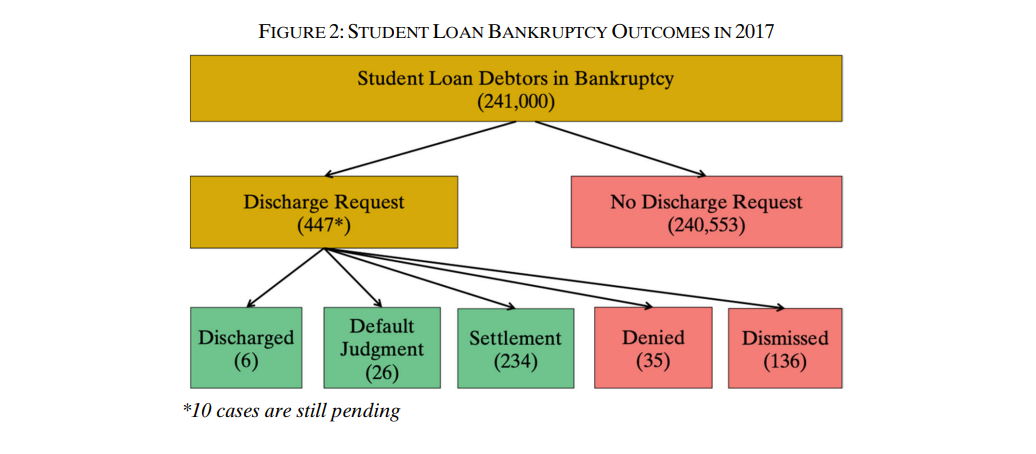

In 2020, almost a quarter of a million borrowers with student loans declared bankruptcy. Of that group, around 300 student loan borrowers—about one-tenth of a percent of those who filed for bankruptcy—had their debt discharged.

These statistics can seem disheartening. They contribute to the common belief that borrowers can never discharge student loan debt through bankruptcy.

But data supports that those who properly attempt to get approved for undue hardship are more likely to be approved.

Source: Iuliano, J. (2020) Duke Law Journal.

A researcher who published an article in the Duke Law Journal found that of the student loan debtors in bankruptcy in 2017, just 447 requested discharge.

Of those who requested a discharge, 60% had favorable outcomes of either full discharge, default judgment, or settlement.

The full 100% of the student loan debtors who did not request a discharge had the unfavorable outcome of retaining their student debt.

The only difference between these two groups is the former filed an adversary proceeding and attempted to prove undue hardship, and the latter did not.

What does filing an adversary proceeding do?

Filing an adversary proceeding allows the lender to contest the suit. The Consumer Bankruptcy Rights Center found that in 15 years (as of 2017), the Fifth Circuit had not discharged a single student loan debt in cases the lenders contested.

However, evidence suggests student loan lenders fight against discharge in the few cases they think they can win but choose to settle most cases. Settlement results in more favorable outcomes for the debtors, such as decreased balances, lower interest rates, and extended repayment periods.

Results of settlements

In 2021, one borrower was granted the discharge of $350,000 of student debt after proving undue hardship. She remained responsible for $7,200 of debt, which she must repay over 10 years.

In another case, a military veteran granted a student loan discharge for over $200,000 in 2020 had that discharge revoked. After his creditor challenged the initial ruling, another court determined he didn’t meet the requirements of the Brunner test.

Whether you can prove undue hardship and get a favorable outcome to reduce your student loan burden will depend on your situation and the state in which you live—and litigate.

Time and financial commitments are involved in making your legal case to have your student loans discharged, which can be a barrier for many.

Steps to prove undue hardship for student loans

While proving undue hardship can be lengthy, you may be able to do so by following five straightforward steps.

1. File bankruptcy

Before claiming undue hardship, you must first file for Chapter 7 (liquidation) or Chapter 13 (adjustment of debts) bankruptcy. The type of bankruptcy for which you file depends on your assets and income.

2. Document and gather evidence for your case

You must show you have no alternative means than bankruptcy to repay your student loans. This means documenting your living expenses, such as rent, food, and medical care.

Pay stubs and bank statements proving your income will also be useful. Moreover, you’ll want to collect documentation if you’re getting government aid, relying on a family member, or suffering from a disabling sickness or injury.

To prove undue hardship for student loans, it is essential to document your good-faith efforts to repay your lender. This includes correspondence with your lender regarding your repayment options, monthly statements, and records of payments.

3. File an adversary proceeding

You must initiate an adversary proceeding to assert an undue hardship claim after declaring bankruptcy. That means you’re starting a lawsuit to take legal action against your student loan lender, whether it’s the federal government or a private company.

To do this, file a complaint that describes the following:

- Your debt

- To whom you owe it

- Your case for undue hardship

4. Litigate the Lawsuit

After you file your proceeding, the lender or loan servicer can respond to the lawsuit. Having a skilled bankruptcy lawyer represent your case could help.

To ensure you’re prepared for your case while filing for bankruptcy or in an adversary proceeding, it can be helpful to enlist the help of an expert and prepare for the proceedings.

Your student loan lenders and other creditors may contest your bankruptcy filing, which might harm your chances of getting a loan discharge if you’re unprepared.

What are possible results if I try to prove undue hardship?

If you demonstrate undue hardship, you can get some or all of your student loan debt discharged via a full or partial discharge.

The amount discharged is not taxable at the federal level due to the American Rescue Act of 2021, but it is scheduled to resume in 2025. Certain states tax the amount of student loan forgiveness, so be aware of your state tax laws.

If the court denies a discharge, you may be able to settle for more favorable loan terms, such as deferment, an extended repayment period, or a lower interest rate.

However, if you’re unsuccessful in proving undue financial hardship, talk to your lender about your options. If you have federal student loans, various income-based repayment plans are available.

Alternatives if I can’t prove undue hardship for student loans

If you can’t prove undue hardship for student loans, you may have options to reduce the financial burden of your debt. Contact your lender’s customer support to determine your repayment options and modify your repayment plan.

Federal student loan repayment options

If you can’t prove undue hardship, a favorable alternative for repayment of federal student loans is an income-driven repayment (IDR) plan. Available to many federal student loan borrowers, IDR plans offer more manageable monthly payments based on a borrower’s income and family size.

Borrowers with loans under the Federal Family Education Loan Program, which expired in 2010, may use the Income-Sensitive Repayment plan. The lender chooses the amount you’ll pay each month, up to 25% of your gross income. This plan is only available for federal loans, not private student loans.

Options for federal and private student loan repayment

Other alternatives include deferment and forbearance, which may be available for federal and private student loans. These options allow you to temporarily pause payments or reduce your monthly payment amount, offering breathing room while you explore other repayment options.

Options exist for special cases. For example, you can look into Closed School Discharge if you can’t return to your school because it’s closed. The government may forgive your loans if this is the case. You must apply for this in most cases. There are regulations, but if you qualify, it can be an excellent way to rid yourself of student loan debt.

Borrowers with private lenders, PLUS loans, and other government loans are eligible if they cannot complete their education due to a closed institution. This choice applies to enrolled students and those granted an absence from school.

Private loan repayment options

Most private loans offer fewer options than federal loans, but be sure to contact your lender to see how it can help. Certain private lenders will allow interest-only repayment plans for as long as six months. Be sure to review the terms of these offers to ensure they will benefit you.

If you’re in a position where your debt hinders your quality of life and you’re filing for bankruptcy, you might consider filing for undue hardship to discharge your student loans. Remember, the process takes time, and you must be prepared to prove the undue hardship in court.

About our contributors

-

Written by Rebecca Neubauer

Written by Rebecca NeubauerRebecca Neubauer is a personal finance and science writer who specializes in writing about managing money, sustainability, entrepreneurship, and alternative living. She has a bachelor’s degree in environmental science, and she learned about personal finance on her journey to pay off $100,000 in student loans.