Thanks to all the available choices, finding the right personal loan is a breeze for Utah residents. You might opt for a big-name online lender or keep it in the community and borrow from a local institution.

Among our recommendations are online lenders that serve Utah residents and banks and credit unions based in the Beehive State. We’ve found a lender for everyone. Keep reading to discover the best one for you.

Table of Contents

Online personal loans in Utah

We’ve researched online lenders more thoroughly than local ones, comparing them across rates, loan amounts, customer reviews, repayment details, and eligibility requirements.

We weighted, scored, and combined these factors to produce a final editorial rating. This rating is expressed on a scale from 1 to 5, with 5 being the highest possible score. Each online lender’s rating is included below. We’re confident Utah residents will have a terrific borrowing experience with these four lenders.

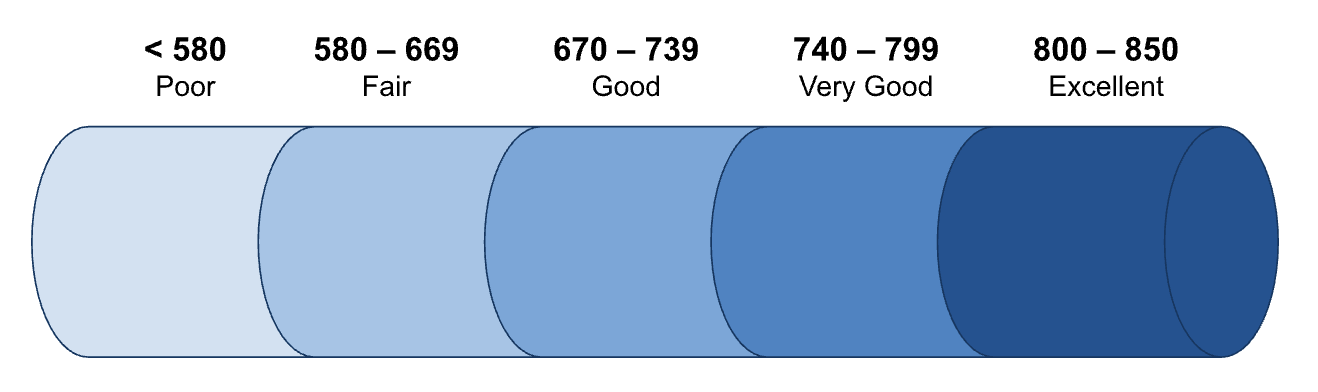

Your credit score is crucial in determining the interest rate and loan terms you qualify for. FICO credit scores are categorized as follows:

Lenders often specialize in serving borrowers within specific credit score ranges, providing options that best fit your financial situation and borrowing history. Whatever your credit score, a lender in Utah can meet your needs.

Here’s a look at the top-rated online lenders serving the state, each offering distinct advantages depending on your credit score.

Credible

Why Credible is the best marketplace

Credible is the leading online loan marketplace where you can compare personalized loan offers from multiple lenders without affecting your credit score.

It’s ideal if you want to explore various financial options in one place. Whether you need a loan for debt consolidation, home improvements, or unexpected expenses, Credible makes it easy to find the best rates tailored to your situation.

- Compare loans from multiple curated lenders

- Get prequalified loan offers in as little as 2 minutes

- Get funded within a few business days

- No option to apply for joint loans

| Rates (APR) | 6.99% – 35.99% |

| Loan amounts | $1,000 – $200,000 |

| Repayment terms | 1 – 10 years |

Eligibility requirements

- Soft credit check? Yes

- Minimum credit score: Varies

- Minimum income: Not disclosed

- States: Loan partners may not be available in all states

Repayment terms

Credible loans have repayment terms ranging from one to 10 years. Some lenders may charge a prepayment penalty if you pay your loan off early.

Upgrade

Why Upgrade is the best personal loan for fair credit

Upgrade is great if your credit isn’t perfect but you still need access to funds. It offers competitive rates for fair credit and allows you to customize your loan to your financial needs: Choose your monthly payment and term length, adjust your payment date during repayment if needed, and even apply with a well-qualified co-borrower.

- Choose your monthly payment and loan term

- Joint applications accepted

- Loan funds may be available in as little as 1 day

- Smaller loan maximum limit

- 1.85% to 9.99% origination fee

| Rates (APR) | 8.49% – 35.99% |

| Loan amounts | $1,000 – $50,000 |

| Repayment terms | 2 – 7 years |

Eligibility requirements

- Soft credit check? Yes

- Minimum credit score: 580

- Minimum income: Not disclosed

- States: All 50 states and Washington, D.C.

Repayment terms

Upgrade loans have repayment terms from two to seven years, and your monthly due date is adjustable to fit your budget. A short-term financial hardship program is available if you’re temporarily unable to manage payments.

SoFi

Why SoFi is the best personal loan for good credit

SoFi offers loans without required origination fees and no prepayment fees. However, you can opt to pay an origination fee in exchange for a lower rate, to select the rate terms that are best for you. With SoFi, you can check your rate without affecting your credit score.

- No origination fees, late payment fees, or prepayment penalties

- Check rates in as little as 60 seconds

- Some borrowers may qualify for same-day funding

- Higher minimum loan amount

- Autopay discount is lower than what some lenders offer

| Fixed rates (APR) | 8.99% – 29.99% with all discounts |

| Loan amounts | $5,000 – $100,000 |

| Repayment terms | 2 – 7 years |

Eligibility requirements

- Soft credit check? Yes

- Minimum credit score: 660

- Minimum income: Not disclosed

- States: All 50 states and Washington, D.C.

Repayment terms

SoFi personal loans feature terms from two to seven years. If you enroll in autopay, you’ll get a 0.25% rate discount. There’s no penalty if you decide to pay your loan off early.

LightStream

Why LightStream is the best personal loan for excellent credit

LightStream is a great option if you have excellent credit. It offers some of the lowest interest rates in the industry. With its Rate Beat program and Loan Experience Guarantee, LightStream provides a unique loan experience, ensuring you receive the best service and value.

However, LightStream doesn’t allow borrowers to prequalify without a soft credit check, meaning you must undergo a hard credit pull (which can lower your credit score) to view your potential rates. For this reason, we think the borrowers best suited for LightStream are those with excellent credit who are confident they’ll be approved.

- Rate match guarantee ensures that you get the best rate possible

- Same-day funding may be available

- Take advantage of a longer repayment term if you need lower payments

- No option to prequalify or check rates with a soft credit pull

- Minimum loan amount is $5,000

| Rates (APR) | 7.49% – 25.49% |

| Loan amounts | $5,000 – $100,000 |

| Repayment terms | 2 – 12 years |

Eligibility requirements

- Soft credit check? No

- Minimum credit score: 660

- Minimum income: Not disclosed

- States: All 50 states and Washington, D.C.

Repayment terms

LightStream offers some of the longest repayment terms of any lender, giving you up to 12 years to repay your loan. You can pay your loan off early, without a prepayment penalty and rate discounts can help bring the cost of your loan down.

Local personal loan lenders in Utah

Some borrowers prefer to work with institutions closer to home. Compared to national lenders, borrowing from local lenders offers several potential benefits:

- Rates are often more competitive.

- Underwriting requirements may be more flexible.

- You usually have the option to apply in person if you don’t want to apply online.

Furthermore, community banks and credit unions hold client relationships in high esteem. These lenders’ success depends on the residents around them. As a result, you’ll likely experience top-notch customer service with a neighborhood lender.

If you’re interested in getting a personal loan from a homegrown bank or credit union, we suggest starting with these:

| Lender | Rates (APR) | Loan amounts |

| Goldenwest Credit Union | 11.25% – 18.00 | Up to $20,000 |

| UFirst Credit Union | 12.74% – 18.00% | Up to $15,000 |

| Wasatch Peaks Credit Unions | 12.00% – 18.00% | $1,000 – $10,000 |

| Bank of Utah | 12.807% – 18.00% | $2,000 – $10,000 |

| Zions Bank | 11.26% – 18.00% | $2,500 – $100,000 |

About personal loans in Utah

In general, lending processes are similar no matter where you live. But you might find variations in personal loans by state, particularly when it comes to borrower protections.

In Utah, lenders aren’t subject to an interest rate ceiling as long as they have a contract with their borrowers. You’re unlikely to find a reputable lender extending you a personal loan without a contract, so your lender can assess whatever rate it chooses.

But your lender can’t take advantage of you. Utah has unconscionability provisions on the books. These don’t set a hard-and-fast rate threshold but prevent lenders from charging excessive interest rates.

Learn how to spot a good rate on a personal loan, and how to recognize a bad one, before you borrow.

“Excessive” is a relative term. You and your lender may have divergent ideas about what constitutes a too-high rate.

Higher APRs almost always guarantee a more expensive loan, so set your own maximum acceptable rate and stick to it. We also recommend prequalifying with several lenders for your best chance at the lowest rate possible.

Despite Utah’s minimal rate restrictions, the state looks out for consumers in other ways:

- Late fees are limited to $30 or 5% of the unpaid balance, whichever is greater.

- Lenders can’t charge prepayment penalties on personal loans.

No one enters into a loan anticipating a missed payment, but knowing your lender can’t levy exorbitant late charges may give you added peace of mind.

If you’re in a position to pay extra toward your loan, you won’t be subject to additional costs or fees. You can leverage this provision to your advantage—even if you can’t pay off the loan in full—to save money and reduce your interest expense.

How to apply for personal loans in Utah

You’ll likely apply online to get a personal loan in Utah, but you may be able to apply in person if you work with a local lender. Either way, you’ll follow similar steps. Here’s what to expect as you apply for your loan:

- Prep your documents. Your lender needs to see proof of income and identity. Gather these records before applying to save time. Scan these documents to your computer or snap photos with your phone if you’re applying online. Otherwise, hard copies should suffice.

- Check your rates. While not required, we suggest prequalifying with at least four lenders. Having multiple personalized offers to choose from helps ensure that you’re getting the best loan available.

- Submit an application. After selecting a loan offer with favorable terms, complete an application with that lender. During this step, you’ll consent to a hard credit pull and complete any additional verifications your lender requires.

- Review and accept your loan agreement. This agreement outlines your rate, monthly payment amount, and repayment schedule. Read it over, and if everything looks good, sign to accept your loan.

- Receive your loan funds. Most lenders send loan funds via electronic transfer within one to two business days of completing the application, passing verification, and signing your documents.

As you compare loan offers, use our personal loan calculator to estimate each one’s borrowing cost. Be sure to adjust your terms up or down to see how different repayment periods can impact your loan.

If this is your first time applying for a personal loan, you may be shocked at how fast you complete each step.

Checking your rates only takes about one minute per lender, and you may be able to finish the application itself in as little as five minutes. From prequalification to funding, expect the entire process to take just one to three business days.

Recap of the best online personal loans in Utah

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.