Navigating financial aid is a rite of passage for incoming college students. The process gets easier each year, but it still requires careful planning. Part of that planning involves evaluating student loan lenders when scholarships and grants aren’t sufficient.

We’ve researched to take the guesswork out of finding student loans. Keep reading for the best loans available to students in California.

| Lender | Best for | Our rating |

| U.S. Dept. of Education | Federal student loans | Not rated |

| College Ave | Private student loans | 5/5 |

| Sallie Mae | Cosigners | 4.8/5 |

| Earnest | No fees | 4.7/5 |

| SoFi | Member benefits | 4.7/5 |

| ELFI | Personalized support | 4.5/5 |

Federal student loans in California

We recommend starting with federal loans if you’re considering borrowing money for school. Federal loans offer benefits not available through private lenders, such as fixed rates, more repayment options, including income-based, and loan forgiveness for eligible borrowers.

Types of federal loans

Several types of federal student loans are available to borrowers throughout the U.S., including those studying in California:

- Direct Subsidized Loans: These loans are available to undergraduates with financial need. The Department of Education pays interest on these loans while you’re in school, for six months after you leave school, and during deferment.

- Direct Unsubsidized Loans: These loans are available to undergraduate and graduate students regardless of financial need. You’re responsible for paying the interest on this loan during all periods.

- PLUS Loans: There are two types of PLUS Loans, the Parent PLUS Loan and the Grad PLUS Loan. The Parent PLUS Loan is for parents of dependent undergraduate students, while the Grad PLUS Loan is reserved for graduate and professional students.

Your cost of attendance determines how much you can borrow in federal loans. Your credit score doesn’t factor with Direct Subsidized and Unsubsidized Loans, but Direct PLUS Loans require a credit check for approval.

Private student loans in California

Due to borrowing limits on federal student loans, many borrowers need to borrow state private loans to augment their financial aid. To help you find funding faster, we’ve analyzed several lenders to bring you these top choices for student loans in California.

College Ave

Why we picked it

College Ave is our top-rated lender, offering private student loans to undergraduates, graduates, and parents. You can apply with or without a cosigner, depending on what suits you best.

College Ave also lets you choose between fixed and variable rates. That, combined with its multiple repayment options and six-month grace period, makes College Ave a wise choice for students learning to budget and launching their careers post-graduation.

- Apply and get a decision in 3 minutes

- 0.25% autopay discount

- Cosigner release after 24 on-time payments

Loan details

| Rates (APR) | 4.39% – 16.85% |

| Loan amounts | $1,000 – 100% of certified costs |

| Repayment terms | 5, 8, 10, or 15 Years |

| Repayment plans | Full, interest-only, $25 flat, or deferred |

| Grace period | 6 months, but can apply for up to 6 more months |

| States | All 50 states |

Sallie Mae

Why we picked it

When it comes to private student loans, Sallie Mae is an industry leader. This lender offers loans for all levels and programs of study, including professional and trade schools.

Sallie Mae is best suited for students with good credit or reliable cosigners. Applying takes just 10 minutes, and you only need to submit one application to get funded for the entire academic year.

- Loans disbursed in 10 business days

- 6-month grace period

- Cosigner release after 12 on-time payments

Loan details

| Rates (APR) | 4.39% – 16.85% |

| Loan amounts | $1,000 – 100% of certified costs |

| Repayment terms | 10 – 15 years |

| Repayment plans | Full, interest-only, $25 flat, or deferred |

| Grace period | 6 months |

| States | All 50 states |

Earnest

Why we picked it

Earnest offers California student loans to undergraduates, graduates, and parents. You can check your eligibility in two minutes without commitment or effect on your credit. Once repayment has started, borrowers can skip one payment per year.

Earnest lends to international and domestic applicants pursuing overseas study. The Golden State boasts the highest number of international students and the highest number of students going abroad, making Earnest a solid pick for California scholars.

- No late fees, origination fees, or disbursement fees

- 9-month grace period

- Rate match guarantee

Loan details

| Rates (APR) | 4.39% – 16.85% |

| Loan amounts | $1,000 – 100% of certified costs |

| Repayment terms | 5, 7, 10, 12, or 15 years |

| Repayment plans | Full, interest-only, $25 flat, or deferred |

| Grace period | 9 months |

| States | All states except Nevada |

Sofi

Why we picked it

SoFi offers student loans to undergraduates, graduates, and parents. You can borrow up to 100% of certified school costs, including room and board, which makes it a great pick for students in California with a high cost of living.

As a top lender in the Golden State, SoFi offers an easy application process, competitive rates, and no fees. But the lender stands out by offering unique perks. Borrowers can take advantage of free meetings with a financial planner and earn cashback rewards through the members-only app.

- No origination fees or late fees

- Unique members-only perks, like free financial planning

- Earn rewards to pay off your loan

Loan details

| Fixed Rates (APR) | 4.13% – 17.99% w/ autopay |

| Variable Rates (APR) | 4.13% – 17.99% w/ autopay |

| Loan amounts | $1,000 – 100% of certified costs |

| Repayment terms | 5, 7, 10, 15 or 20 years |

| Repayment plans | Full, interest-only, fixed, or deferred |

| Min. credit score | Not disclosed |

ELFI

Why we picked it

With loans for undergraduates, graduates, and parents, ELFI is a solid online lender for California students. It only takes a few minutes to apply online. Once you begin the process, you’ll work with a dedicated loan advisor who can answer questions and provide help.

ELFI has repayment terms for up to 20 years, much longer than most lenders. It’s a helpful option for California borrowers who need lower monthly payments. You can also request up to 12 months of forbearance due to job loss or other financial setbacks.

- Work one-on-one with a loan advisor

- Longer repayment terms

- Up to 12 months of forbearance due to hardship

Loan details

| Rates (APR) | 3.98% – 14.22% |

| Loan amounts | $1,000 – 100% of certified costs |

| Repayment terms | 5, 7, 10, 15, or 20 years |

| Repayment plans | Immediate, interest-only, $25 fixed, or deferred |

| Grace period | 6 months |

| States | All 50 states |

To compare other options, check out our guide to the best private student loans or learn more about state student loans.

California state financial aid

In addition to federal and private loans, California residents are eligible for state-sponsored grants and scholarships. Once you complete the FAFSA, the state automatically considers you for the following financial aid.

| Program | Eligibility | Award amount |

| Cal Grant | Undergraduate students with financial need | $1,094 – $15,400 |

| Middle Class Scholarship | Undergraduates or teaching credential students with family income under $226,000 | 10% – 40% of school costs |

| The California Chafee Grant for Foster Youth | Current or former foster youth under 26 years old | Up to $5,000 per year |

How to get student loans in California

Figuring out how to fund college usually requires multiple steps. Here’s the most effective way to tackle the process.

- Complete the FAFSA: All students should apply for federal student aid by filling out the Free Application for Federal Student Aid (FAFSA). The application allows you to access various financial aid options, including state-based aid like CalGrant.

- Accept financial aid: After completing the FAFSA, your school will use your Student Aid Index (SAI) to generate your financial aid award letter. This letter details your eligibility for scholarships, grants, and federal loans. Federal student loans usually have lower interest rates than private loans, so it makes sense to prioritize federal loans first.

- Calculate the gap: Once you know your federal aid amount, you can calculate how much more you need to afford school. For example, imagine it costs $30,000 to attend your school for one year. You get $20,000 in federal aid, so you need an additional $10,000 to make it work.

- Apply for private loans: Apply for private student loans to cover the remaining costs you must pay. Start with the lenders that have the best rates and repayment terms.

What to know about student loans in California

Student loan borrowers in California are protected by the state’s Student Borrower Bill of Rights. Introduced under Assembly Bill 376, the Student Borrower Bill of Rights affords you the following protections:

- Late fees are capped at 6% of your unpaid balance.

- Lenders can’t impose minimum flat-dollar-amount late fees.

- Payments made by 11:59 p.m. on the due date must be considered on-time payments.

- Overpayments must be applied in a way that benefits you financially.

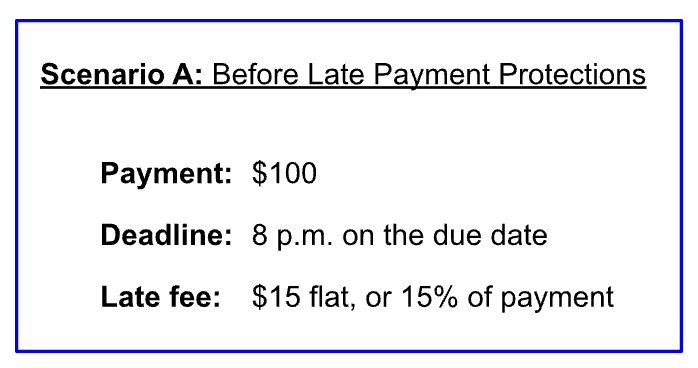

Many lenders set not just payment due dates but cutoff times: If you don’t make your payment by a specified time—say, 8 p.m. the day it’s due—it’s considered late. Your lender could assess a full late payment penalty if you pay just a few minutes after that time.

To better illustrate how this could affect you, imagine paying $100 toward your student loans. If your lender has a mandatory minimum $15 late fee, you’ll pay a 15% penalty for submitting your payment on or after 8:01 p.m.

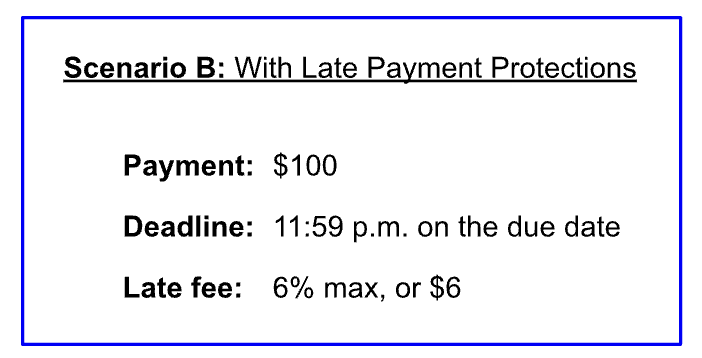

That’s no longer permissible in California, at least not for student loans. Instead, you’ll have until just before midnight to make your payment. If you submit after 11:59 p.m. on your due date, you won’t pay more than 6% in late fees—which, in this hypothetical case, would save you $7.

California’s Student Borrower Bill of Rights also requires lenders to ask borrowers how they want overpayments applied. Absent your input, your lender must act in your best interest.

In many states and with many lenders, overpayments are applied first to any fees, then to accrued interest, and finally to your principal balance. But in California, student loan lenders must use your overpayment to reduce the total cost of your loan.

As you can, take advantage of these protections to make extra payments toward your principal. Shrinking your principal balance will not only help you pay off your student debt faster, but it could also save you hundreds—maybe thousands—in interest over the life of your loan.

FAQ

What is the cost of college in California?

The average cost of college in California is $24,015 per year for in-state tuition at a public school, including tuition, fees, room, and board. But you can expect to pay an extra $10,383 per year if you have out-of-state tuition fees. Private colleges in California cost an average of $53,680 per year.

Can I switch my rate from variable to fixed (or vice versa) during my loan term?

Most lenders offer a choice between a fixed or variable rate when you first borrow. However, changing your rate after this point isn’t typically an option. Refinancing your student loan is likely the only possible solution if you want to change from a variable to a fixed rate or vice versa.

How do I qualify for a student loan?

Qualifying for a student loan usually involves basic eligibility criteria. You must be a U.S. citizen or a permanent resident. Some lenders may allow international students with a U.S. citizen cosigner. In many cases, you must be enrolled at least half-time in an eligible degree-granting program. Approval also often requires a good or excellent credit score or a creditworthy cosigner.

Can California residents refinance their student loans?

California residents can refinance private or federal student loans. You typically have to wait to do so until you graduate or withdraw from your program. But refinancing can help you save money on your California student loan if you get a lower interest rate or better repayment terms.

I would not recommend that these protections dictate where a student attends school unless there is a strong conviction that their financial condition or personal/family preference warrants repayment plans/benefits to guide their decision for their education. If this is important to you, I suggest narrowing down options to schools and lenders in the state of California and, of course, preparing a pros and cons list.

Erin Kinkade, CFP®

Recap of best private California student loans

| Lender | Best for | LendEDU rating |

| College Ave | Private student loans | 5/5 |

| Sallie Mae | Cosigners | 4.8/5 |

| Earnest | No fees | 4.7/5 |

| SoFi | Member benefits | 4.7/5 |

| ELFI | Personalized support | 4.5/5 |

About our contributors

-

Written by Taylor Milam-Samuel

Written by Taylor Milam-SamuelTaylor Milam-Samuel is a personal finance writer and credentialed educator who is passionate about helping people take control of their finances and create a life they love. When she's not researching financial terms and conditions, she can be found in the classroom teaching.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.