Student Loans

- Competitive rates

- Many term-length options

- Excellent transparency and openness

- Available to Texas students and residents, and non-Texas applicants attending an approved Texas school

- Can’t be used at for-profit schools or most community colleges

- Noticeable lack of reviews from actual customers

- Restricted to Texas students, residents, and schools

| Fixed rates (APR) | 2.96% – 7.63% with autopay discount |

| Variable rates (APR) | Starting from 4.60% with autopay discount (Texas residents only) |

| Loan amounts | $1,000* – 100% of school-certified costs |

| Repayment terms | 5, 7, 10, 15, or 20 years |

Everything’s bigger in Texas, except for the interest rates on Brazos student loans. If you’re looking for an affordable private student loan and you’re a Texas resident—or studying at a Texas school—it’s worth adding Brazos to your list of possible loan options.

In addition to low-interest student loans, Brazos offers a wider range of term length options than most other lenders, allowing you to align your monthly payment and overall loan cost with your post-graduation goals. It also provides multiple loan types for undergrads, grads, and parents alike.

It’s worth noting that loans to Texas residents are made by Brazos Education Lending Corporation and loans to non-Texas residents studying in Texas are made by Bank of Lake Mills, member FDIC, so some loan terms will vary depending on which entity is the lender. Still, here is our full review and what you need to know about Brazos student loans as you decide if this is the right lender for you

What types of student loans does Brazos offer?

Brazos offers a wide range of student loans to fit just about all borrower needs, including:

- Parent loans (only available for Texas residents)

- Graduate loans

- Undergraduate loans

- Student loan refinance

If you’re interested in more advanced degrees, you’ll also find Brazos student loans for certain fields, such as healthcare, law, and MBAs. But don’t be fooled: These are all the same loan type as its graduate loans, just with their own pages for marketing purposes.

The only substantial difference between “medical school loans” and Brazos student loans for graduate students in general is that doctors can continue deferring payment while they’re completing a residency or fellowship.

Brazos student loan rates and terms

Low interest rates are the primary standout feature of Brazos student loans. They’re much lower than most other private student loan companies:

| Term | Detail |

| Fixed rates (APR) | 2.96% – 7.63% with autopay discount |

| Variable rates (APR) | Starting from 4.60% with autopay discount (Texas residents only) |

| Loan amounts | $1,000 ($2,001 for non-TX residents attending a TX school) – 100% of school-certified costs |

| Repayment period | 5, 7, 10, 15, or 20 years |

| Fees | None, except for late payment fees (For Texas residents, 5% of the late payment or $35, whichever is less. For non-Texas residents, 5% of the unpaid amount of the monthly payment due or $10, whichever is less) |

Eligibility requirements

Brazos offers a soft credit pull option, like Credible, Earnest, and some other lenders

If you don’t meet the eligibility requirements yourself, it allows you to apply with a cosigner. When you apply, it will conduct a thorough investigation of your credit, education, and financial details, including a hard credit check.

| Requirement | Details |

| Citizenship | U.S. citizen or permanent resident; non-citizens with a work or student visa and DACA recipients can qualify with an eligible cosigner |

| State of residence | Texas resident or studying at a school in Texas |

| Min. age | 18 |

| Enrollment status | Be enrolled with at least half-time status at an accredited Title IV school that is a state or private not-for-profit four-year institution within the United States |

| Min. credit score | 680 (borrower or cosigner) |

| Min. income | $35,000 (borrower or cosigner) |

How does repayment work?

You’ll choose a combination of loan term length and repayment option when you apply for your loan. Choose carefully; you can’t modify these selections after the fact if your post-college plans change.

| Terms | Details |

| Repayment options | Immediate, interest-only, or deferred |

| Repayment terms | 5, 7, 10, 15, or 20 years |

| Grace period | 6 months |

| Cosigner release? | Yes, after you make 12 on-time payments (or prepaid by 12 months) and pass a credit check |

How do Brazos student loans compare to alternatives?

SoFi® is a worthy competitor for Brazos student loans, but when it comes to interest rates, it still can’t quite beat Brazos. SoFi is available nationwide, and it offers benefits that include free access to financial planners, cash for good gradesⓘ, and rewards.

If you don’t have a cosigner but are otherwise positioned to earn a strong income after graduation, Ascent may be a better option. It offers an option for non-cosigned loans for upperclassmen, and its features include discounts and cashback rewards for graduating and signing up for autopay.

College Ave is one of our top picks for best private student loan lender overall due to its more expansive approval criteria. You can get approved if you’re studying at less than half-time status, for example, and once approved, it will be easier to get future loans if you need them.

What do Brazos customers say?

We couldn’t find any examples of actual Brazos customers discussing their experiences on any online review platforms. Brazos is a small regional lender, but even so, a total lack of reviews is unusual.

That doesn’t necessarily mean Brazos is a bad lender. It just means people who have worked with Brazos haven’t been swayed enough by their experiences—good or bad—to go out of their way to talk about it.

Given that graduates are often stymied and frustrated by private student loans, that could be a positive sign. If Brazos were a terrible lender to work with, we’d likely have heard about it from someone—anyone—by now.

Does Brazos have a customer service team?

Yes, it’s possible to get ahold of someone before applying for Brazos student loans, albeit in a bit of a clunky way. Brazos doesn’t offer a live chat option or even a mobile app, leaving only three ways to contact the lender with questions:

- Phone: 1-800-453-0841

- Email: [email protected]

- Mailing address: Brazos Education Lending, 5609 Crosslake Parkway, Waco, TX, 76712

If you already have Brazos student loans, you won’t contact Brazos with questions—you’ll contact the company Brazos hired to service your loan instead:

- AES-PHEAA: 1-800-233-0557

How do you get a Brazos student loan?

Before completing the full loan application, Brazos offers the option to do a soft credit pull for you to check potential rates. This doesn’t affect your credit score, and it’s the best way to shop around and explore different lenders to find the best loan for you.

Once you do complete the full Brazos loan application, you’re not obligated to take the loan offer, but the full application will result in a hard credit pull on your report.

Here’s how to apply for Brazos student loans:

Step 1: Go to the application page

Look for the green “APPLY NOW” buttons, which are abundant on Brazos’s website. Click on one to begin your application.

Step 2: Check your Texas eligibility

The first page of the application will ask the most important question: Are you a Texas resident? And if not, are you applying as an out-of-state resident studying at a Texas school? If you are eligible based on state residency rules, you’ll proceed to the next page of the application.

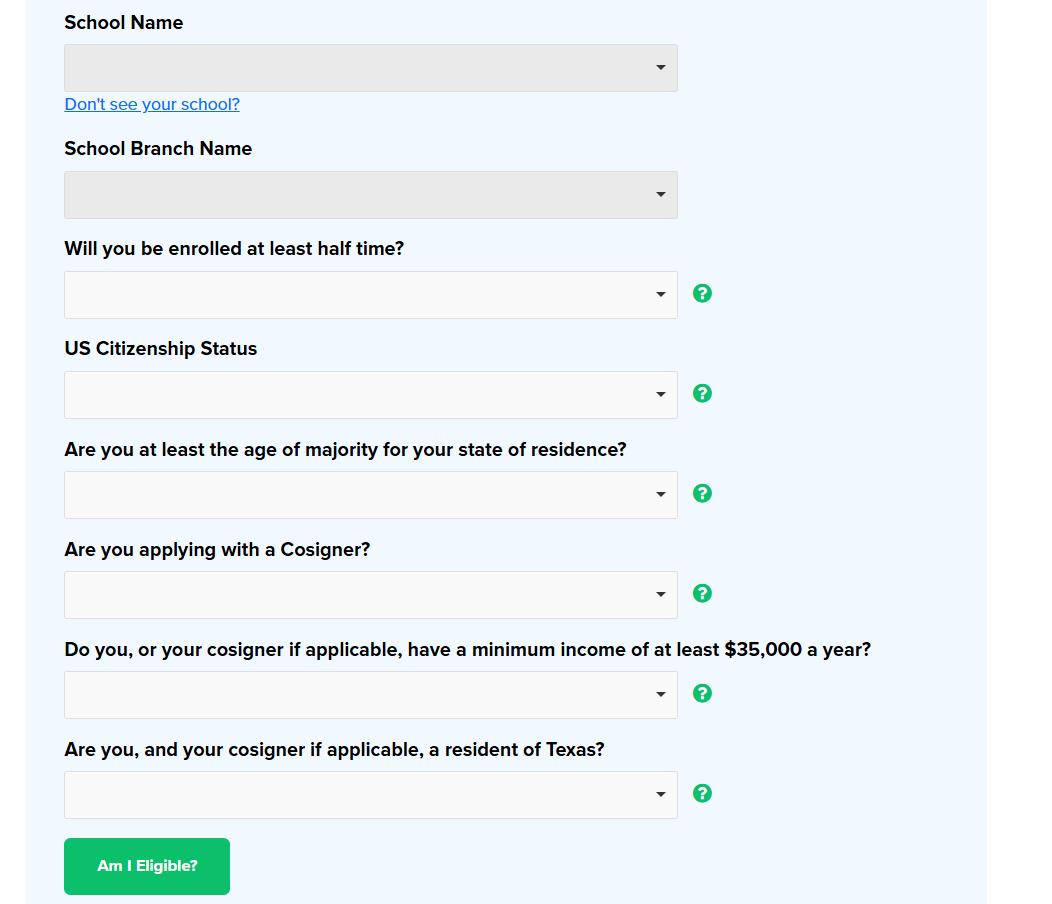

Step 3: Check your other qualifications

The third page of the application will ask for more granular details about your specific school, your study plans, your cosigner, and more. When you’re done, hit the green “Am I Eligible?” button at the bottom.

Step 4: Review your preapproval decision

After this point, you’ll need to provide a few more details, including your and your cosigner’s Social Security numbers, addresses, and school-certified cost of attendance, along with any other financial aid, which you can find in your financial award letter.

Brazos will do a quick credit check and may offer an instant preapproval at this point, contingent on a few more details.

Step 5: Receive a decision and get the loan funds

If necessary, Brazos will request additional documentation of your and your cosigner’s income, such as prior tax returns or pay stubs, and check with your school. Once everything is verified, Brazos will send the loan funds to your school, which typically happens just before the school year starts.

About our contributors

-

Written by Lindsay VanSomeren

Written by Lindsay VanSomerenLindsay VanSomeren is a personal finance writer living in Suquamish, Washington. She's passionate about helping people manage their money better so that they can live the life they want. In her spare time, she enjoys outdoor adventures, reading, and learning new languages and hobbies.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.