If your student loan payments are too high, you have options to lower or temporarily suspend them. Refinancing is often the best way to get a lower payment, but it’s not for everyone. If you need relief, here are seven ways to reduce your student loan payments, whether you have federal or private loans.

1. Refinance your student loans

- Loan types: Federal and private

- Impact: Lower monthly payments and potential savings on interest

- Best for: Borrowers with good credit and steady income

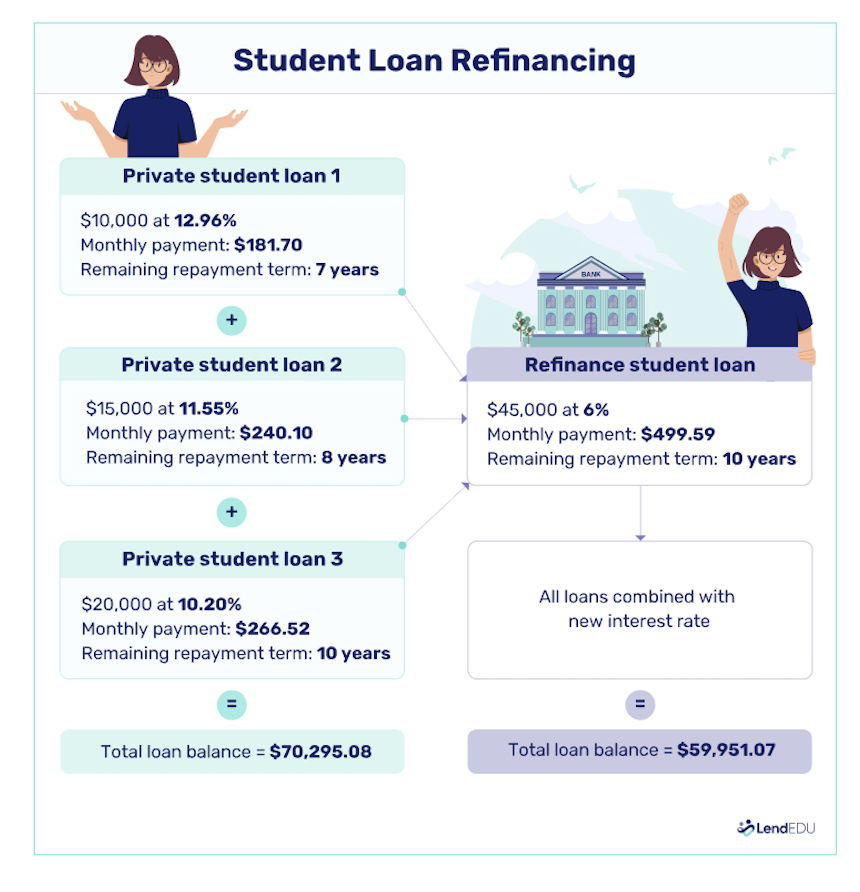

Refinancing replaces your current student loans with a new loan—ideally with a lower interest rate or longer repayment term. This can reduce your monthly payment and save you money over time.

Why refinancing is the best option for many borrowers:

- You can get a lower interest rate if you qualify.

- You may reduce your monthly payment by extending your loan term.

- You can consolidate multiple loans into one.

⚠️ Why refinancing might not be right for you:

- If you refinance federal loans, you lose access to income-driven repayment plans, deferment, and forgiveness programs.

- You need good credit (or a cosigner) and a stable income to qualify.

See more pros and cons of refinancing.

If you have a federal student loan but has strong credit and a good income, I recommend you evaluate refinancing to a private student loan because you might be able to significantly reduce your monthly payments via reduced interest rates or extended payment terms.

Check your rate with multiple lenders before committing. We recommend Credible as a convenient way to compare student loan refinancing offers.

2. Apply for an income-driven repayment (IDR) plan

- Loan types: Federal only

- Impact: Lower payments based on income

- Best for: Borrowers with low income or unstable employment

If you have federal loans, an IDR plan can cap your payments at 10% to 20% of your discretionary income and extend repayment to 20 to 25 years. Any remaining balance after that may be forgiven.

IDR plan options include:

- REPAYE: Best for low-income borrowers [Note: The SAVE Plan was formerly a replacement for REPAYE but has been challenged in court. See more here.]

- PAYE and IBR: Best if you expect income growth

- ICR: The only IDR plan available for Parent PLUS borrowers (must consolidate first)

Apply for IDR through StudentAid.gov and recertify your income annually.

3. Extend your repayment term

- Loan types: Federal and private

- Impact: Lower monthly payments, but more interest over time

- Best for: Borrowers who want predictable payments

Federal loans allow you to extend repayment up to 25 years through:

- Extended Repayment Plan (must owe $30,000+ in Direct Loans)

- Graduated Repayment Plan (payments start low and increase over time)

Some private lenders also allow longer repayment terms—often 15 to 25 years—if you refinance.

Only extend your loan term if necessary; you’ll pay more in interest overall.

4. Consolidate federal student loans

- Loan types: Federal only

- Impact: One payment, longer term, and access to more repayment options

- Best for: Borrowers with multiple federal loans

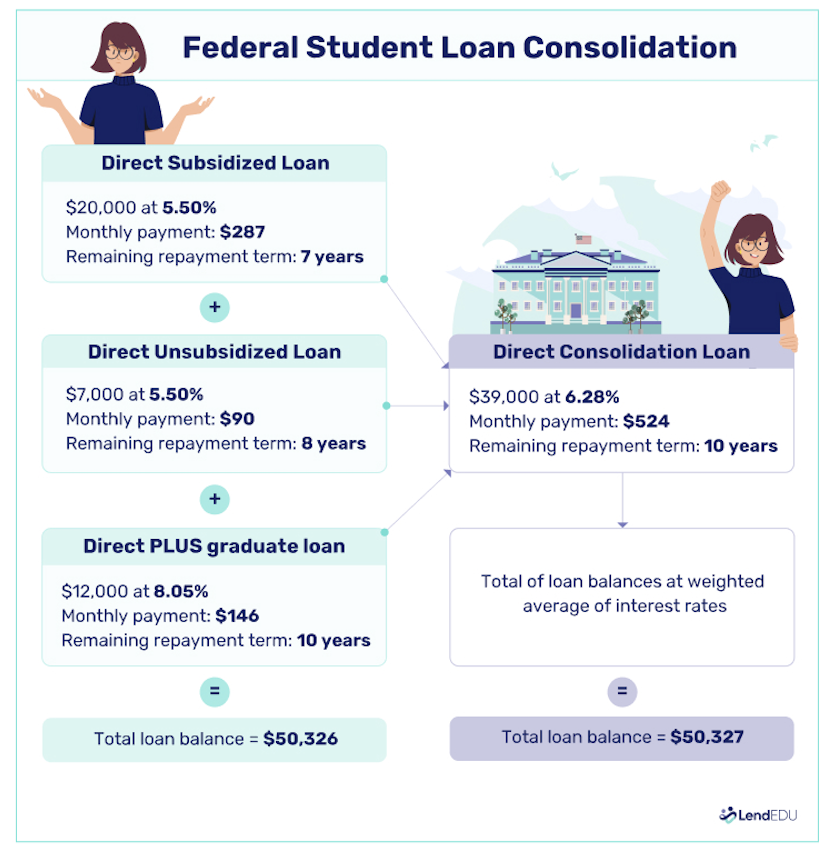

A Direct Consolidation Loan combines multiple federal loans into one, with a weighted average interest rate. This can make repayment simpler and help Parent PLUS borrowers qualify for Income-Contingent Repayment (ICR).

⚠️ What to watch out for:

- Your interest rate won’t decrease (unlike refinancing).

- You might reset progress toward PSLF or forgiveness programs.

If your goal is a lower rate, consider refinancing instead of consolidation.

5. Request deferment or forbearance

- Loan types: Federal and private

- Impact: Temporary suspension of payments

- Best for: Short-term financial hardship

If you’re unemployed, experiencing economic hardship, or in school, you may qualify for deferment (interest-free for Subsidized Loans) or forbearance (interest still accrues).

For private loans, contact your lender—some offer hardship forbearance, but terms vary.

Typically, we recommend that you start with refinancing federal student loans into private loans. This tends to be the biggest help for most clients to reduce interest payments.

If this isn’t an option or does not provide sufficient relief, we recommend evaluating all current expenses to see whether there are areas to cut out or reduce to free up additional cash flow.

Deferment or forbearance tends to be the last option because, while they may provide temporary relief, they tend to make things worse over the long term as interest continues to accrue and increases the overall amount of the loan and future monthly payments.

6. Seek employer loan assistance

- Loan types: Federal and private

- Impact: Employer helps with repayment

- Best for: Borrowers with jobs offering student loan benefits

Some employers offer student loan repayment assistance as part of their benefits package—typically $50 to $200 per month.

Ask your HR department about available programs. Some states also offer loan repayment grants for workers in high-need fields.

7. Consider student loan forgiveness programs

- Loan types: Federal only

- Impact: Potential loan cancellation

- Best for: Borrowers in public service or nonprofit work

If you work in public service, healthcare, or teaching, you may qualify for forgiveness programs:

- Public Service Loan Forgiveness (PSLF): Requires 10 years of qualifying payments while working for a government or nonprofit employer.

- Teacher Loan Forgiveness: Up to $17,500 for qualifying educators.

Parent PLUS Loans are not eligible for PSLF unless consolidated into a Direct Consolidation Loan.

Takeaway

If your student loan payments are too high, you have options—from refinancing for a lower rate to IDR plans, deferment, or forgiveness. The best solution depends on your loan type, credit score, and financial goals. Explore your options today to take control of your student debt.

About our contributors

-

Written by Megan Hanna, CFE, MBA, DBA

Written by Megan Hanna, CFE, MBA, DBADr. Megan Hanna is a finance writer with more than 20 years of experience in finance, accounting, and banking. She spent 13 years in commercial banking in roles of increasing responsibility related to lending. She also teaches college classes about finance and accounting.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.