Student loan funds can cover living expenses included in your school’s cost of attendance (COA), such as food, utilities, transportation, and more. We’ll walk you through eligible living costs and how to find lenders that offer flexible support for day-to-day costs.

Table of Contents

- Can I get student loans for living expenses?

- What’s the average cost of student living expenses

- How to use federal student loans for living expenses

- The best private student loans for living expenses

- How to use living expense loans for students

- Student loans for living expenses off campus [Example budget]

- Tips for using student loan funds for living expenses

- FAQ

- Are there grants for living expenses while in college?

- Can you use a Pell Grant for your cost of living?

- Can you get student loans for living expenses with bad credit?

- What if my student loans don’t cover my living expenses—can I take out more student loans just for these costs?

- Can you take out personal loans for college students for living expenses?

- Are there grad school loans for living expenses?

- Do medical school loans cover living expenses?

- Recap of student loans for living expenses

Can I get student loans for living expenses?

You can use student loans for any expense that supports your ability to attend school and earn your degree. These generally fall under the umbrella of “educational expenses.”

The biggest expense outside of tuition is likely your housing expenses. You can find our full guide to using student loans to pay for housing here. Beyond housing, qualifying living costs include:

- Utilities (electric, gas, water, internet, and cellphone)

- Groceries and personal supplies (e.g., toiletries, medications)

- Transportation (e.g., parking passes, public transit, gas)

- School-related items (e.g., laptop, books, supplies)

- Dependent care (e.g., child care so you can attend class)

You may not use student loans for vacations, luxury items, or nonessential purchases.

Since housing is often the biggest line item on a student’s budget, we’ve created a separate, in-depth guide just for that. If you’re looking for help specifically with room and board, be sure to check out our complete guide to how to pay for college housing.

What’s the average cost of student living expenses

While housing tends to dominate the cost of college attendance, non-housing living expenses can still add up quickly. On average, students can expect to spend between $7,000 and $9,000 per year on essential living costs outside of rent. These include groceries, transportation, school supplies, and more.

Here’s a breakdown of typical annual costs based on data from the College Board and student budget reports:

| Category | Estimated annual cost |

| Utilities (electric, gas, water, internet, phone) | $1,200 – $1,800 |

| Groceries and personal supplies | $3,000 – $4,500 |

| Transportation (gas, transit, parking) | $1,000 – $1,500 |

| School-related items (books, laptop, supplies) | $900 – $1,200 |

| Dependent care (if applicable) | $1,000 – $3,000+ |

Total estimated cost: $7,100 – $12,000 per year

These numbers can vary widely depending on your location, whether you’re attending school full-time or part-time, and if you have dependents. For example, students in rural areas might spend less on public transportation, while those with young children may have significantly higher dependent care costs.

Tip: Use your school’s COA worksheet or talk with the financial aid office to get a more personalized estimate of your non-housing expenses.

How to use federal student loans for living expenses

Federal student loans can be a lifeline for covering living expenses while you’re in school. They’re designed to help with not just tuition and fees but also day-to-day costs. Here’s how it works:

- Disbursement to your school first: Your federal loan funds are sent directly to your school.

- School covers tuition, fees, and room/board (if you live in a dorm): The school deducts these expenses from your loan amount.

- Leftover funds are refunded to you: Once the school has taken its share, the remaining balance is sent to you via check or direct deposit. This can take 3 – 4 weeks to arrive, so be prepared to wait a bit before the money is in your hands.

Federal loans should be your first choice because of their built-in protections, like income-driven repayment plans and forgiveness options. But sometimes, your federal loans might not cover your COA. In that case, private student loans can step in to help—but keep in mind they don’t come with the same safety nets.

If you have hit your federal limits, private loans might be worth considering. Just be sure to compare your options and borrow only what you truly need.

The best private student loans for living expenses

Private student loans can help cover your living expenses when federal loans don’t go far enough. Unlike federal loans, private loans typically require a good credit score or a cosigner.

Here are the top-rated private lenders that allow funds to be used for housing and other living costs. In our reviews, we’ve noted which living expenses each lender specifically lists as covered on its website.

College Ave

Why we picked it

- Approves loan amounts up to 100% of certified COA, including living expenses.

- Funds are first sent to the school; excess refunded to student.

- No enrollment restrictions (full- or part-time OK).

Undergraduates, graduates, and parents can use College Ave loans to cover housing and other living expenses, such as rent, books, transportation, and groceries.

College Ave uses your cost of attendance to determine the total funding you receive. The approved amount is first sent to your school to be applied toward your tuition bill, with excess funds delivered to you for other expenses.

Loan Details

| Fixed Rates (APR) | 4.39% – 16.85% |

| Variable Rates (APR) | 4.13% – 17.99% |

| Loan amounts | $1,000 – 100% of certified costs |

| Repayment terms | 5, 8, 10, or 15 years |

| Repayment plans | Full, interest-only, $25 flat, or deferred |

| Enrollment | No restrictions |

| States | 50 states |

| Credit score | Mid-600s and above |

| Annual income | $35,000 |

Sallie Mae

Why we picked it

- Loan can cover full year’s COA, including room and board, transportation, and personal expenses.

- You can cancel future disbursements without penalty—useful if living expenses change.

Sallie Mae is the industry’s most well-known private lender. You can use its loans for tuition, room and board, off-campus housing, transportation, sheets and towels, meals, books, and more. Rather than applying multiple times, you can cover an entire year’s worth of housing and living expenses with one application.

Loan Details

| Fixed Rates (APR) | 4.50% – 16.70% |

| Variable Rates (APR) | 4.13% – 17.99% |

| Loan amounts | $1,000 – 100% of certified costs |

| Repayment terms | 10 – 15 years |

| Repayment plans | Interest-only, $25 flat, or deferred |

| Enrollment | No restrictions |

| States | 50 states, D.C., and Puerto Rico |

| Credit score | Mid-600s and above |

| Annual income | Not disclosed |

Earnest

Why we picked it

- Covers full COA including off-campus rent, groceries, transportation, and even dependent care.

- Known for no fees, and unique features like a 9-month grace period and skip-a-payment option once per year.

Earnest is an online lender that offers several unique benefits, such as no fees on any of its loans, a nine-month grace period, and the ability to skip one payment per year.

Earnest loans can cover tuition, room and board, books, laptops, study abroad, kitchen supplies, transportation, dependent care, and more.

Loan Details

| Fixed Rates (APR) | 4.13% – 17.99% |

| Variable Rates (APR) | 4.13% – 17.99% |

| Loan amounts | $1,000 – 100% of certified costs |

| Repayment terms | 5, 7, 10, 12, or 15 years |

| Repayment plans | Full, interest-only, $25 flat, or deferred |

| Enrollment | At least half-time |

| States | 49 states and D.C. (Nevada excluded) |

| Credit score | 650+ |

| Annual income | $35,000 |

SoFi

Why we picked it

- Allows use of funds for school-certified expenses, which can include rent, utilities, groceries, and other off-campus living costs.

- Also offers perks like financial planning access and app-based loan management.

SoFi® offers fee-free student loans that cover school-certified living expenses, including rent, utilities, groceries, and transportation.

Borrowers gain access to financial planning services and can manage their loans through the SoFi mobile app. SoFi members earn reward points by using the app, which they can use to pay down the balance on their student loans.

Loan Details

| Fixed APR | 4.13% – 17.99% w/ autopay |

| Variable APR | 4.13% – 17.99% w/ autopay |

| Loan amounts | $1,000 – 100% of certified costs |

| Repayment terms | 5, 7, 10, or 15 years |

| Repayment plans | Full, interest-only, flat, or deferred |

| Enrollment | At least half-time |

| States | 50 states |

| Credit score | Not disclosed |

| Annual income | None |

ELFI

Why we picked it

- Covers up to 100% of certified COA, including housing and living expenses.

- Personalized service via a dedicated student loan advisor, which can be especially helpful when budgeting for off-campus expenses.

ELFI student loans offer competitive interest rates and personalized customer service through a dedicated student loan advisor. This advisor can help you through the application process. Over 2,100 borrowers rate ELFI as “Excellent” on Trustpilot.

Loan Details

| Fixed Rates (APR) | 2.99% – 14.22% |

| Variable Rates (APR) | 5.00% – 14.22% |

| Loan amounts | $1,000 – 100% of certified costs |

| Repayment terms | 5, 7, 10, or 15 years |

| Repayment plans | Full, interest-only, $25 flat, or deferred |

| Enrollment | At least half-time |

| States | 50 states, D.C., Puerto Rico |

| Credit score | 680+ |

| Annual income | $35,000 |

How to use living expense loans for students

Whether you use federal or private student loans, any funds left after your tuition and fees are paid can be used to cover your living expenses. Our recent survey showed nearly half of students living on a college campus used these funds for personal expenses.

Your COA is the key factor lenders use to determine how much you can borrow for living expenses. Your school calculates your COA based on tuition, fees, and estimated living expenses.

Once your school determines your COA, it subtracts any financial aid you’ve already received (like grants and federal loans). The remaining amount is the maximum you can borrow through a combination of federal and private loans.

If you receive both federal and private loans, the federal funds are usually applied first. Here’s how it typically works:

- Federal loan disbursement: Your school uses federal loan funds to cover tuition, fees, and on-campus housing first. Any leftover amount is refunded to you for living expenses.

- Receiving private loan funds: Once approved, private loans typically follow a similar disbursement process—going to the school first, with any remaining balance refunded to you. Some private lenders may send funds directly to you, which can give you quicker access to cash for rent and bills.

Since both your school and your lenders are involved, it can take a few weeks to get your money, especially if you’re relying on a combination of federal and private loans. Make sure to plan ahead so you’re not caught short when bills are due.

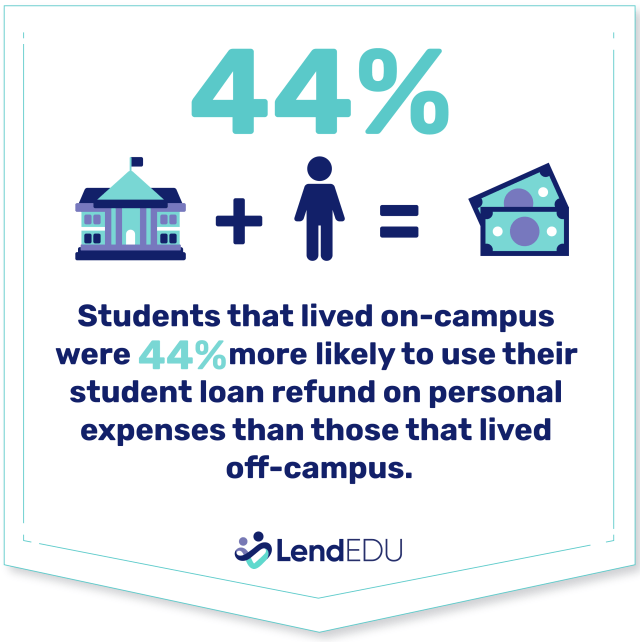

Student loans for living expenses off campus [Example budget]

When you’re living off-campus, your financial aid refund can help cover essential bills like groceries, utilities, transportation, and personal expenses. While rent is typically the biggest expense (learn more about how to plan for that in our housing guide), planning for all living costs is crucial to make your funds last throughout the academic year.

Interestingly, our latest survey found students living on campus are 44% more likely to use their student loans for personal expenses compared to those living off campus. This means that regardless of where you live, it’s important to plan ahead and budget carefully when you’re using student loan funds for living expenses.

Here’s a hypothetical monthly budget that focuses on non-rent living expenses:

| Expense | Monthly cost |

| Utilities (electric, gas, water) | $150 |

| Internet and phone | $80 |

| Groceries | $300 |

| Transportation (gas/public transit) | $100 |

| Personal expenses (toiletries, laundry, etc.) | $50 |

| Emergency savings | $50 |

| Total | $730 |

Of your financial aid refund, you could expect to dedicate about $6,750, or $750 per month, to cover living expenses for a 9-month academic year. With the budget above, you’ll have a little buffer each month for unexpected costs.

Tips for using student loan funds for living expenses

Managing your funds wisely can help you avoid running out of money mid-semester. Here are some practical tips:

- Create a monthly budget before school starts: Estimate your non-rent living expenses and break them down by month to see how much you can reasonably spend.

- Prioritize essential expenses: Focus on necessary costs, like groceries, utilities, transportation, and personal supplies.

- Save for recurring bills: Set aside money for things that come up every month, like your utility bills or internet.

- Avoid impulse spending: Since you may receive a lump sum at the start of the year, it’s tempting to splurge. Stay disciplined to make your money last.

- Automate bill payments: This helps you avoid late fees and keeps your budget consistent.

- Track your expenses: Use a budgeting app to keep an eye on your spending and make adjustments as needed.

- Keep a small emergency fund: Unexpected expenses can come up, so it’s wise to set aside a little extra.

By planning ahead and focusing on essential expenses, you can make your student loan refund last without stressing about running out of money.

Get a full list of do’s and don’ts when using your student loan funds, and the full rundown on student loan uses in this guide.

Bottom line: Yes, student loans can cover living expenses.

Student loans are meant to support your education—and that includes groceries, transportation, and basic personal expenses. Whether you use federal or private loans, be strategic with how you spend. Borrow only what you need, avoid misusing funds, and consider all your financial aid options first.

If private loans are part of your plan, compare lenders carefully. Each offers different benefits, limits, and flexibility when it comes to using funds for living expenses.

FAQ

Are there grants for living expenses while in college?

Yes, some grants can be used to cover living expenses while you’re in college. Federal grants, like the Pell Grant, can help pay for housing, utilities, groceries, and other day-to-day costs if there’s money left after covering tuition and fees. Similarly, some state grants and scholarships can also be used for living expenses, depending on the program’s guidelines.

Since grants don’t need to be repaid, they’re an ideal form of financial aid. To maximize your chances, complete the FAFSA early and check for additional grants through your school or state government.

Can you use a Pell Grant for your cost of living?

Yes, Pell Grants can be used for living expenses if there’s money left after your tuition and fees are covered. Since Pell Grants are need-based and don’t have to be repaid, they’re one of the best ways to help cover essential costs like rent, groceries, and transportation. Once your school applies the grant to your direct educational expenses, any leftover amount can be used for your day-to-day living needs.

Can you get student loans for living expenses with bad credit?

Yes, it’s possible to get student loans for living expenses even with bad credit, but your options may be limited. Federal student loans, like Direct Subsidized and Unsubsidized Loans, don’t require a credit check, making them a good choice for students with poor credit. These loans are typically the first option to consider since they offer flexible repayment plans and protections.

If you’ve exhausted your federal loan options, private student loans are another possibility, but they usually require good credit or a cosigner. Some lenders specialize in working with borrowers who have bad credit or offer options if you have a cosigner with strong credit. Be aware that private loans may come with higher interest rates and less flexible repayment options, so compare offers carefully.

What if my student loans don’t cover my living expenses—can I take out more student loans just for these costs?

Yes, but only within certain limits. Federal and private student loans are capped by your school’s COA, which includes both direct costs (like tuition and fees) and indirect costs (like housing, food, and transportation).

If your current student loans don’t cover everything, you may still be eligible to borrow additional funds up to the COA—typically through a Direct PLUS Loan (for parents or grad students) or a private student loan. You’ll need to work with your school’s financial aid office to confirm your eligibility and update your financial aid package.

Can you take out personal loans for college students for living expenses?

Yes, but it comes with trade-offs. You can take out personal loans to help pay for living expenses while you’re in college, especially if you’ve hit federal borrowing limits or don’t qualify for more student loans. However, personal loans:

- Aren’t designed specifically for students and may have higher interest rates than student loans

- May require a strong credit history or a cosigner

- Do not offer income-driven repayment plans, deferment, or forbearance like federal loans do

Only consider personal loans after exhausting federal student aid options and carefully weighing the risks. Learn more about personal loans for students here.

Are there grad school loans for living expenses?

Yes. Graduate student loans—both federal and private—include living expenses as part of the total cost of attendance. That means you can use your loan funds not just for tuition and fees, but also for rent, food, utilities, transportation, and other basic needs.

Federal loans available for graduate students include Direct Unsubsidized Loans and Grad PLUS Loans. Learn more about student loans for graduate school here.

Do medical school loans cover living expenses?

Yes, medical school student loans also cover living expenses as part of your cost of attendance. Both federal and private lenders allow you to borrow enough to pay for not only tuition, books, and lab fees, but also day-to-day costs like rent, food, and transportation. Because medical school is so intensive, most students rely on loans to cover full-time living expenses. You can learn more about medical school loans here.

How we selected the best student loans for living expenses

LendEDU evaluates student loan lenders to help readers find the best student loans. Our latest analysis reviewed 725 data points from 25 lenders and financial institutions, with 29 data points collected from each. This information is gathered from company websites, online applications, public disclosures, customer reviews, and direct communication with company representatives.

These star ratings help us determine which companies are best for different situations. We don’t believe two companies can be the best for the same purpose, so we only show each best-for designation once.

Recap of student loans for living expenses

| Company | Best for… | Rating (0-5) |

|---|---|---|

|

|

Best Overall |

|

|

|

Best for Cosigners |

|

|

|

Best for Large Loans |

|

|

|

Best for Member Benefits |

|

|

|

Best Advisors |

|

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.