Student loan consolidation allows you to combine multiple loans into one, leaving you with a single monthly payment. It’s possible to consolidate private and federal student loans together, but the only way is by refinancing them with a private lender.

Consolidating private and federal student loans could make budgeting more manageable because you’d have just one monthly payment. But weigh the trade-offs of moving federal loans to a private lender.

We’ll explain how private and federal student loan consolidation works and what you should consider before making a move.

Table of Contents

Private vs. federal student loan consolidation

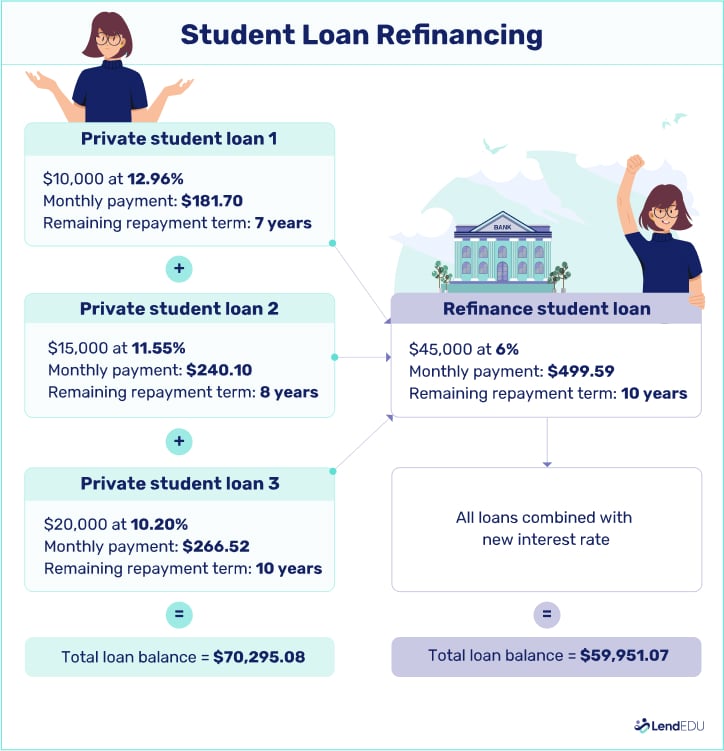

Private student loan consolidation is more often referred to as refinancing. When you refinance, you take out a new loan to pay off your student loans, which may be federal, private, or a mix of both. You then make payments to the new loan.

Refinancing private student loans can allow you to:

- Change your loan repayment term to make it shorter or longer than your previous loans

- Get a lower interest rate than what you were paying

- Switch from a variable rate to a fixed rate or vice versa

- Lower your monthly payment

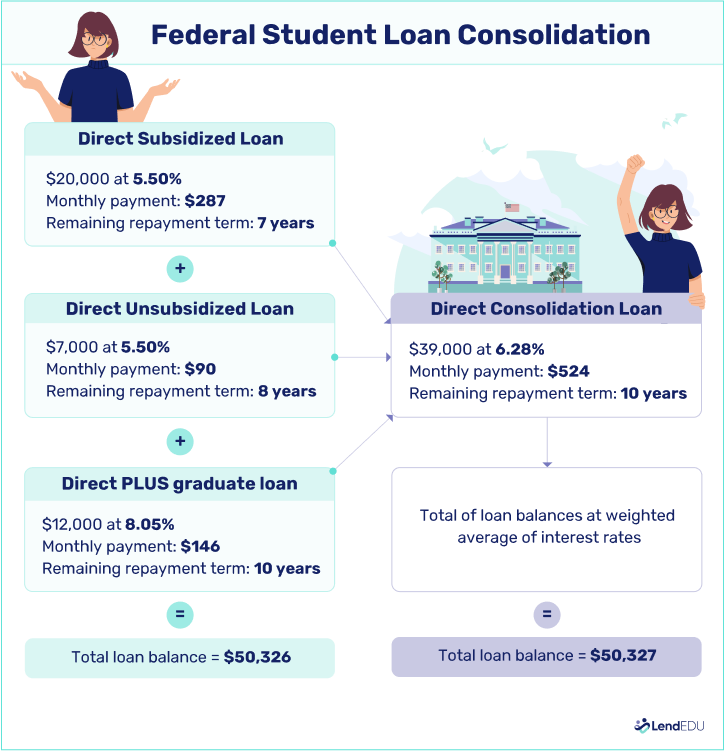

Federal student loan consolidation also allows you to combine multiple loans. What’s different is that you can only consolidate eligible federal loan balances, not private ones. Federal loan consolidation also doesn’t lower your interest rate; your consolidation loan rate is the weighted average of the rates you were paying.

You can see how federal consolidation and private refinancing work in the images below:

The Direct Consolidation Loan Program is open to borrowers with eligible federal loans. That means loans held by the U.S. government, which excludes loans from private lenders. The list of federal student loans eligible for Direct Consolidation includes:

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Direct PLUS Loans

- Subsidized Federal Stafford Loans from the Federal Family Education Loan (FFEL) Program

- Unsubsidized and Nonsubsidized Federal Stafford Loans

- FFEL PLUS Loans

- Federal Perkins Loans

- Supplemental Loans for Students

- Nursing Student Loans and Nursing Faculty Loans

- Health Education Assistance Loans

- Health Professions Student Loans

- FFEL Consolidation Loans and Direct Consolidation Loans (conditions apply)

- Federal Insured Student Loans

- Guaranteed Student Loans

- National Direct Student Loans

- National Defense Student Loans

- Parent Loans for Undergraduate Students

- Auxiliary Loans

Parent PLUS loans can’t be consolidated with federal loans the student received. Any loans you consolidate must be in repayment or the grace period. You can generally consolidate once you graduate, leave school, or drop below half-time enrollment.

| Refinance | Consolidation | |

| Can combine private and federal student loans | ✅ | ❌ |

| Lowers interest rate | ✅ | ❌ |

| Switch from variable to fixed rate | ✅ | ✅ |

| Reduce monthly payments | ✅ | ✅ |

| Loan forgiveness eligible | ❌ | ✅ |

| Repayment protection | ❌ | ✅ |

| Income-driven repayment eligibility | ❌ | ✅ |

Pros and cons of consolidating private and federal student loans

Consolidating private and federal loans together has advantages and disadvantages. Looking at both sides can give you a better sense of what you might get—and give up—with private and federal student loan consolidation.

Pros

-

Consolidating loans can make budgeting easier with just one payment each month.

-

If you choose a longer repayment term, your new monthly payment may be less than you were paying across your loans.

-

Refinancing could help you get a lower interest rate and save money over the life of the loan.

-

A lower rate could help you pay off student debt faster, leaving you free to work toward your other financial goals.

Cons

-

Qualifying for the best refinance rates may be challenging if you don’t meet the lender’s minimum requirements for credit scores, income, or other qualifications.

-

Moving federal loans to a private lender means giving up federal protections and benefits, including access to income-driven repayment plans and the opportunity to qualify for loan forgiveness.

That last con is important because private lenders aren’t obligated to extend deferment or forbearance options or offer income-driven repayment. Some lenders provide temporary assistance for borrowers experiencing financial hardship, but just as many don’t. And as mentioned, you’d no longer be eligible for Public Service Loan Forgiveness (PSLF).

Also, keep in mind that private loan refinancing approval isn’t guaranteed. Qualifying could be more challenging without a cosigner if you don’t have a strong credit profile or sufficient income. Asking a creditworthy person to cosign could help you get a refinance loan, but you risk straining the relationship if you can’t repay what you borrow.

Should you consolidate private and federal student loans?

Consolidating private and federal student loans isn’t something to take lightly because it means sacrificing federal loan benefits. Evaluating your financial situation can help you decide when to consolidate.

| Consolidate if… | Don’t consolidate if… |

| ✅ You want a better rate | ❌ Your rates are already low |

| ✅ Loan forgiveness is off the table | ❌ Loan forgiveness is a possibility |

| ✅ You want to pay off loans faster | ❌ Your income is uncertain |

When to consider private and federal student loan consolidation

You may benefit from consolidating private and federal loans together if:

- Your current loans have high rates, and you’re confident that you can get a better rate through a private lender based on your credit history and income.

- You’re not pursuing a career in public service or don’t qualify for income-driven repayment, which would allow you to have remaining federal loan balances paid off after 20 or 25 years.

- You’d like to fast-track your loan payoff by refinancing into a shorter loan term or a loan with a lower rate, allowing more of your payment to go to the principal.

To save for retirement, especially if your budget is tight, consolidating into a loan with better terms—such as a lower monthly payment—allows you to save toward retirement, an emergency fund, a down payment for a home or rental deposit, and other life goals. A provision is in place that allows employer-sponsored plans to “match” the amount the employee is paying toward their student loans into a retirement plan in the employee’s name, even if the employee can’t make a direct contribution. But this isn’t mandated, so it’s wise to check with your employer. It’s a question to ask during the interview process if you’re job searching. As far as additional financing goes, keep a pulse on your debt-to-income ratio to ensure it’s low enough to gain approval for additional funding, such as a mortgagor auto loan, if needed.

Erin Kinkade, CFP®

When not to consider private and federal student loan consolidation

You may want to pass on consolidating federal and private loans if:

- Your federal loan rates are lower than a private student loan lender’s best rates.

- You’re considering a public service job or may qualify for an income-driven repayment plan to make you eligible for loan forgiveness.

- You’re just starting your career and earning a lower income, or you’re self-employed and have an irregular monthly income.

Consolidating private and federal loans has short- and long-term impacts. It’s wise to consider the benefits you might reap now and in the future to decide whether it’s worth it.

If you’re debating between potentially lower interest rates via private refinancing and the loss of federal benefits, it depends on your unique circumstances: Consider your career, how steady the income is, whether the career is high-paying or lower-paying career, and the chances you could be laid off. These are just several items to think about. If you believe your income could be in jeopardy, it would be wise to stick with federal loans that offer options during financial hardships. If you’re in sound financial condition and have solid employment and an emergency fund, the lower-interest refinance with a private lender may be the best option. I recommend thinking about your current financial circumstances and what-ifs. And as always, if in doubt, consult with a financial professional.

Erin Kinkade, CFP®

How to consolidate private and federal student loans

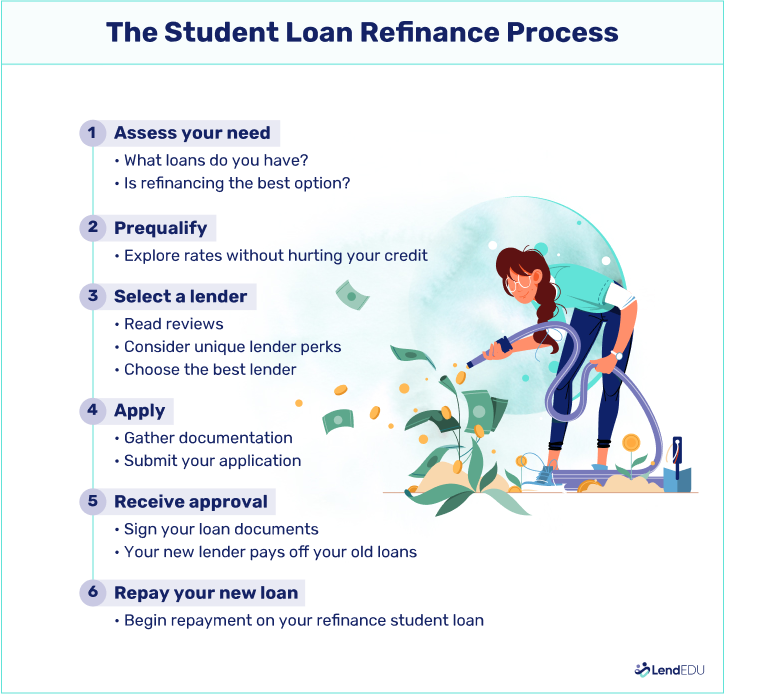

If you think private and federal student loan consolidation might be right for you, it helps to know what the process involves. The short version is: Find a lender, submit an application, and await approval.

But there’s more to it. So here’s a brief overview of how private and federal loan consolidation works.

- Assess your needs. The first step is deciding which loans to consolidate. Making a list of your loans with the balance, interest rate, and payment can save you time when you’re ready to apply for consolidation.

- Compare rates. Next, spend time researching lenders to compare rates and terms. It helps to get at least three rate quotes from different lenders so you know what you might be preapproved for. Look for lenders that offer quotes without requiring a hard pull of your credit.

- Choose a lender. Rates aren’t the only factor to consider when choosing a consolidation lender. It’s also important to look at a lender’s customer service, brand reputation, and the benefits extended to borrowers. Reading customer reviews can give you an idea of what people like or dislike about a particular lender.

- Apply for a loan. If you’ve chosen a lender, you can move on to applying for a loan. Here, you’ll need to share personal information and information about your loans, which you should have already gathered in step one. You’ll also need to prepare any financial documents the lender might need, such as tax returns, pay stubs, or bank statements.

- Wait for approval. Once the lender has your application, it will review it and make a decision. If you’re approved, you’ll have a chance to review the loan documents before you sign. You can check the rates, fees, and repayment terms to ensure you’re happy with everything before signing off.

- Pay off the old loans and begin repayment on the new one. Your lender should use the loan proceeds to pay off your old loans. It’s wise to continue making payments until you verify that the loans are paid off. Once your old loans are paid, you can start making payments to the new one.

Learn more about refinancing and explore the best student loan refinance companies.

Alternatives to student loan refinancing

If you have federal and private loans but don’t want to refinance them there are some other possibilities you might explore for making payments more manageable. Here are a few options to consider.

- Enroll in an IDR plan. If you have federal student loans, an income-driven repayment plan could make payments more affordable. It’s possible to reduce your payment to $0, depending on which plan you choose. After 20 or 25 years, any remaining loan balance would be forgiven.

- Consider a deferment or forbearance. Putting federal loans into deferment or forbearance can let you take a temporary break from making payments. That’s a benefit you might appreciate if you’re experiencing financial hardship. Keep in mind that if you have unsubsidized loans, pausing payments could leave you with a higher balance to repay once they resume.

- Consolidate loans separately. No rule says you have to add in federal loans when refinancing private loans. You could get a Direct Consolidation Loan for federal loans and refinance private loans separately. You’d still have two loan payments to make but you wouldn’t lose federal loan protections and you could still save money if your private loan has a lower rate.

If you’re having trouble with your loan payments or need advice on how to repay them, don’t be afraid to reach out to your lender or loan servicer. It can guide you on the best way to handle your loans based on your needs.

About our contributors

-

Written by Rebecca Lake, CEPF®

Written by Rebecca Lake, CEPF®Rebecca Lake is a certified educator in personal finance (CEPF®) and freelance writer specializing in finance.