Stafford Loans, now known as Direct Subsidized Loans and Direct Unsubsidized Loans, are federal student loans available to undergraduate and graduate students enrolled at least half-time.

They can offer students a more affordable way to fund their education.

Stafford Loans don’t require a credit check or income verification, allowing many students to be eligible for funding for their higher education.

Table of Contents

Subsidized Stafford Loans vs. Unsubsidized Stafford Loans

Many students and their families are often confused by the two types of federal Direct Loans.

We’re breaking down the difference between Subsidized and Unsubsidized Stafford Loans.

With Direct Subsidized Loans, the federal government pays the interest while you’re in school or in deferment, but the interest on Direct Unsubsidized Loans accrues once funds are disbursed, even while you’re in school.

| Feature | Direct Subsidized | Direct Unsubsidized |

| Eligibility | Undergrads w/ financial need | Undergrad, grad students |

| Gov’t. pays interest? | ✅ (in school and deferment only) | ❌ |

| Repayment begins | 6 mos. after graduation or less than half-time enrollment | 6 mos. after graduation or less than half-time enrollment |

How much can you borrow with a Direct Stafford Loan?

Annual and aggregate borrowing limits apply to Direct Subsidized Loans and Direct Unsubsidized Loans. The tables below show the maximum you can take out based on your dependency status (dependent or independent) and year of attendance, including the amount that may be Subsidized.

| Year | Annual max for dependent students |

| 1st | $5,500 ($3,500 Subsidized) |

| 2nd | $6,500 ($4,500 Subsidized) |

| 3rd+ | $7,500 ($5,500 Subsidized) |

| Grad/prof. | N/A |

| Aggregate | $31,000 ($23,000 Subsidized) |

| Year | Annual max for independent students* |

| 1st | $9,500 ($3,500 Subsidized) |

| 2nd | $10,500 ($4,500 Subsidized) |

| 3rd+ | $12,500 ($5,500 Subsidized) |

| Grad/prof. | $20,500 ($0 Subsidized) |

| Aggregate | $57,500 undergrad ($23,000 Subsidized); $138,500 grad/prof. ($65,500 Subsidized) |

Already hit federal limits? Check out our list of the best private student loans to cover other school expenses.

What are the rates and fees on Stafford Loans?

Unlike private student loans, Stafford Loan rates are fixed and don’t change for the life of the loan. The government sets these rates, and they don’t influence your credit and income.

Because the interest rate on a private student loan generally depends on your credit history and income, the fixed or variable rates may range broadly. Even if a private lender advertises rates lower than or comparable to those of Stafford Loans, they’re often only available to borrowers with excellent credit scores and high incomes.

Some private lenders also charge higher origination fees than federal loans. The lender adds these fees to your loan, increasing the amount you’ll have to pay back.

Below are the interest rates and fees you can expect from federal and private student loans.

| Loan type | Interest rate | Origination fee |

| Stafford Loan | 5.50% (undergrad) 7.05% (grad/prof.) | 1.057% |

| Private loan | 4.00% – 17.00%+ | Varies* |

Overall cost of a Stafford Loan for an undergraduate

Based on rates, an undergrad’s $10,000 federal student loan balance over a 10-year term will have a monthly payment of $109. In total, the loan could cost $13,023.

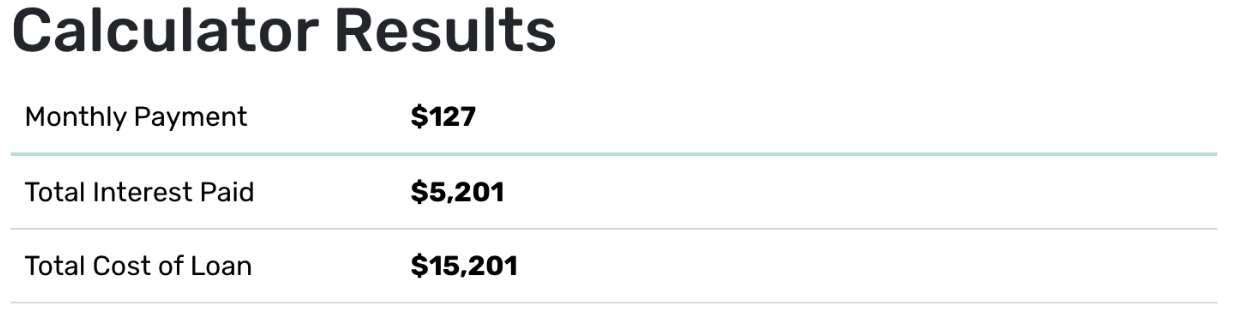

Overall cost of a private student loan:

Based on a fixed 9.00% interest rate, a $10,000 private student loan balance over a 10-year term will have a monthly payment of $127. In total, the loan could cost $15,201.

Source: Student Loan Payment Calculator

Understanding the interest rates and fees associated with federal and private student loans—and how they affect the overall cost of your loan—can help you make more well-informed decisions.

Applying for loans with lower or fixed interest rates and fees can save you thousands of dollars in the long run. Plus, fixed rates are easier to work around your budget and future financial planning.

What are the repayment options for a Stafford Loan?

Federal student loans, including Stafford Loans, offer various repayment plans to accommodate your financial situation.

| Repayment | Terms | Eligibility |

| Standard | 10 yrs. Fixed payments | All fed. borrowers |

| Extended | Up to 25 yrs. Fixed or graduated payments | 30,000+ in Direct Loans |

| Graduated | Payments rise every 2 yrs. 10 yr. term | All fed. borrowers |

| IDR | Based on income & family size (20 – 25 yrs.) | All fed. borrowers |

| PSLF | 10 years (120 pmts.), income-based Balance forgiven after | Qualifying public service employees |

| Deferment or forbearance | Term length varies, payments paused | Financial hardship, unemployment, etc. |

The four types of IDR plans are:

- Saving on a Valuable Education (SAVE)

- Pay As You Earn (PAYE)

- Income-Based Repayment (IBR)

- Income-Contingent Repayment (ICR)

These options are one of the major advantages federal loans can provide.

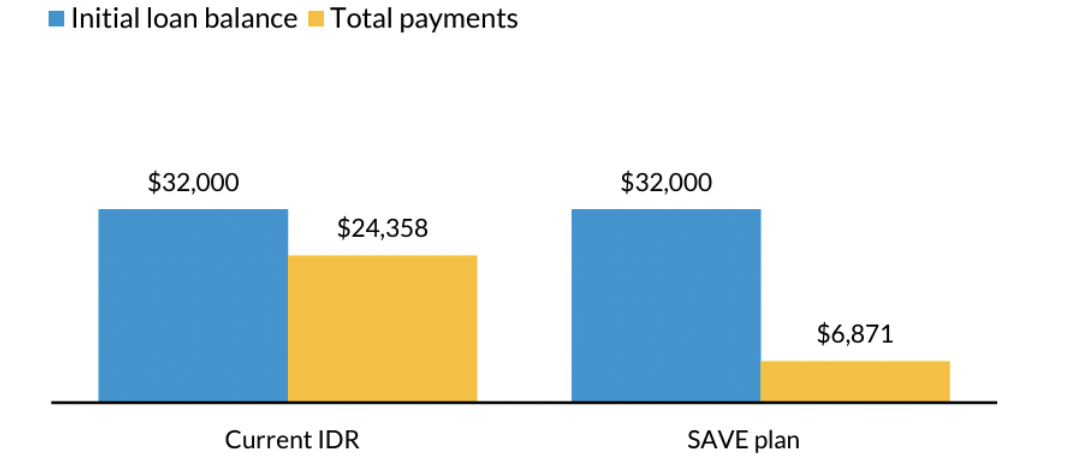

Take a look at how much the SAVE Plan could save a low-income borrower on a $32,000 student loan compared with the savings on other IDR plans:

These repayment plans could offer a life-changing solution for borrowers who are under financial strain or looking for a clearer path forward in their careers.

How to apply for a federal Direct Stafford Loan

Students who’d like to apply for a Stafford Loan must complete a Free Application for Federal Student Aid (FAFSA). Applying involves several important steps to ensure you receive the financial aid you need.

1. Set up a Federal Student Aid account online

To set up an account, you must provide personal information, such as your name, date of birth, and Social Security number. The entire process may take five to 10 minutes.

2. Complete the FAFSA

You have until June 30 to fill out and submit the FAFSA. But before you do, check your school’s and state’s unique deadlines.

You’ll need to provide detailed information, so completing the FAFSA the first time can take up to an hour. You must renew your FAFSA application every year for additional financial aid in the following school years.

As you fill out the FAFSA, you must choose at least one school to determine the types of student aid it will offer, and how much, but you can select up to 20 schools.

3. Review your FAFSA Submission Summary

Your FAFSA will be processed in a few days, up to a week if you submit it by mail. Once it’s processed, you’ll receive the FAFSA Submission Summary, which you must review. Be sure to correct any errors. This may take 10 to 15 minutes to review and revise.

The summary will list the financial aid you may be eligible for, information about the schools you selected when you completed the FAFSA, and the next steps.

4. Review your federal financial aid offers

The schools you selected will send you an offer of financial aid, often in the spring. The offer will include the cost to attend, the types of aid the school is offering, including Direct Stafford Loans you’re eligible for, and the deadline to accept.

The time it takes you to review your offers will depend on the number of schools you selected in your FAFSA and the types of financial aid you’re offered. Expect to spend at least five minutes reviewing the details of each school’s offer.

5. Accept your offer

Once you’ve decided where you’d like to enroll, you’ll follow the instructions to notify the school and accept any or all of the financial aid offers that work best for you.

If you’re offered different types of financial aid, we recommend accepting them in this order:

- Grants and scholarships

- Work-study program (if needed)

- Loans (if needed) in the following order: Subsidized, Unsubsidized, and PLUS

After accepting your loan offer, you’ll complete entrance counseling to demonstrate that you understand your loan terms, rights, and responsibilities.

The time it may take to get the funds can vary depending on the program, but they’re generally available or disbursed by the beginning of the fall semester. You can contact your financial aid office to find out more details.

Is a Stafford Loan right for you?

Stafford Loans’ fixed interest rates, flexible repayment options, and borrower protections, including potential loan forgiveness, place them among your best options for funding your education through a loan.

So it’s best to exhaust your options for Stafford Loans first before considering other loans, including PLUS Loans and private student loans.

Start by planning ahead. If you can, make it a point to go to school with no debt or as little as possible. Before applying for a Stafford Loan, explore all your alternatives—starting with ones that don’t involve borrowing at all, like work-study programs and scholarships.

About our contributors

-

Written by Melody Stampley, CEPF®

Written by Melody Stampley, CEPF®Melody Stampley is a personal finance writer and Certified Educator in Personal Finance® with 10-plus years of combined experience in writing, editing, and finance. She specializes in credit, loans, budgeting, saving, and insurance. Melody is a mother who enjoys helping others become free and empowered to show younger generations good stewardship practices.

-

Reviewed by Gail Urban, CFP®

Reviewed by Gail Urban, CFP®Gail Urban, CFP®, AAMS®, has been a licensed financial advisor since 2009, specializing in helping individuals. Before personal financial advising, she worked as a business financial manager in several industries for about 25 years.