It may seem counterintuitive that more debt could result in better credit, but getting a loan could boost your credit score. Here’s the catch: How it affects your credit will depend on multiple factors, including your credit history and payment habits.

If you’re considering a loan, personal loans are popular because you can get fast funds and use them for almost any purpose. Here’s how personal loans work, including how they can help or hurt your credit.

Table of Contents

What is a personal loan?

Personal loans are installment loans that often have fixed rates and relatively short repayment terms, often up to seven years. Because of the fixed rate, your monthly payments don’t change over time.

Secured personal loans exist, but most are unsecured, meaning they’re not backed by underlying collateral such as your car or home. Thus, you’ll generally need good credit and stable employment to get approved for the best personal loans.

How does a personal loan affect your credit score?

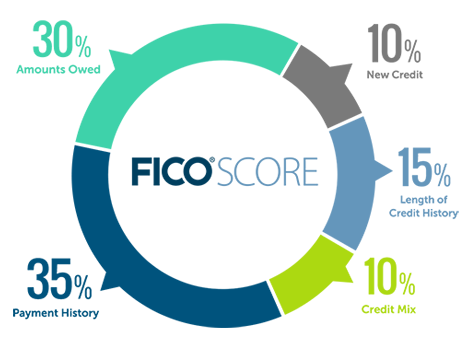

Lenders rely on the FICO credit scoring model when determining whether borrowers qualify for new credit. Your FICO score includes five factors, weighted according to their importance:

- Payment history (35%)

- Credit utilization ratio (30%)

- Length of credit history (15%)

- New credit (10%)

- Credit mix (10%)

A new personal loan may influence your credit utilization ratio, new credit, and credit mix right away. It will also affect the length of your credit history and payment history. The overall impact on your score depends on your credit history and how you manage your loan.

>> Read more: What credit score is needed for a personal loan?

How a personal loan can improve your credit score

A personal loan could help your credit score in several ways. Here’s how.

Payment history

Your payment history is weighted as a hefty 35% of your FICO score. Making your personal loan payments on time and in full each month should have a positive impact on your credit score over time.

Credit utilization ratio

Your credit utilization ratio is weighted as 30% of your credit score, and it’s based on how much revolving credit you use relative to your available revolving credit. Credit cards are revolving accounts, so they affect credit utilization. But personal loans are installment loans, not revolving accounts, so they don’t count toward your credit utilization.

For example, if your total credit card limit is $10,000, and you have an outstanding balance of $7,000, your credit utilization ratio is 70%. If you use a personal loan to pay off your credit cards, your credit utilization ratio would drop to 0%

As a general rule, it’s smart to keep your credit utilization ratio under 30%. In this case, using your personal loan to consolidate credit card debt could boost your credit score.

Credit mix

Credit mix is weighted as 10% of your FICO credit score, and a mix of accounts is generally positive. If you only have credit card accounts, for example, adding an installment loan to your credit profile could help your credit score.

How a personal loan can harm your credit score

A personal loan can help your credit, but it could also ding your credit score. Here’s what to know.

New credit

New credit accounts for a small portion of your FICO score—just 10%. When you apply for a personal loan, your lender will do a hard credit inquiry, which often shows up on your credit report within 30 days. This new inquiry can harm your credit score by a few points.

One new hard inquiry won’t have a significant negative impact, but too many new credit inquiries can be more detrimental. Keep this in mind if you’re considering applying for multiple loans or credit lines in a short time frame.

Length of credit history

Your credit history has a 15% weighting on your FICO score. In general, a longer credit history is better. A new account can affect the length of your credit history, which may lower your score by a few points. But it will likely be less harmful to your credit than closing an older account.

Payment history

Making on-time, full payments is good for your credit score, but late or missing payments is harmful. Prioritize making your monthly personal loan payments in a timely fashion to avoid hurting your score.

Should you take out a personal loan to improve your credit score?

Whether you should take out a personal loan to boost your credit score depends on your situation. If you’re using the proceeds to consolidate high-interest debt or can manage another monthly payment, a personal loan could make sense.

But before you apply for a new personal loan, account for potential costs, including origination fees, which can be as high as 10%. These fees vary by lender and are often deducted from your loan proceeds. For instance, if you borrow $10,000 with a 10% origination fee, you’d get just $9,000.

Weighing the pros and cons will help you determine whether a new personal loan is right for you.

Alternatives to consider for credit building

If a personal loan doesn’t seem like the right choice,you have other ways to build and improve your credit. Here are three approaches.

Credit builder loans

Credit builder loans are small, short-term loans available from banks, credit unions, and online lenders. You can often get approved for a credit builder loan with a thin credit file or poor credit. As their name suggests, these loans can help borrowers build credit, but they’re different from traditional loans.

Instead of disbursing funds immediately, your lender will hold your loan balance in a secured account. You make payments toward that balance, and your lender shares your payment history with the three major credit agencies: Equifax, Experian, and TransUnion. Once you’ve paid off the full balance, the lender releases your loan proceeds to you.

Ensure you make payments on time and in full to reap the benefits of a credit builder loan. Missing payments could harm your credit score.

Credit cards

You could use credit cards to build credit, but you may need to start with a secured credit card if you have a thin file or poor credit. Secured credit cards require a small deposit, often equal to your credit limit. That deposit serves as collateral for the credit card issuer in case you default.

When you use a secured credit card and make monthly payments, the lender reports your payments to the credit bureaus. Managing payments responsibly will result in a positive payment history, which could boost your credit score.

Improve your score with your current credit accounts

You could work toward improving your credit score without opening a new account. If you have credit card balances or outstanding loans, make a plan to pay them down as much as possible. Reworking your budget, negotiating with your creditors, picking up a part-time gig, and setting up automatic payments could ease this process.

A personal loan could boost your credit score. But do it with a deliberate plan to continue paying down your debt, or the additional debt may compound your problem and do more damage to your score.

If you’re considering this approach, be sure you understand how personal loans work.

FAQ

Do personal loans have a lesser impact on credit scores than credit cards?

One doesn’t always have more impact than the other. Making full on-time payments on your personal loan or credit cards could help improve your credit, but partial or missed payments can be detrimental.

Does the loan amount matter in terms of credit score impact?

The size of your loan can affect your credit score. Your total debt factors into the FICO and VantageScore credit scoring models. A larger loan could have a bigger impact than a smaller loan because of the more substantial increase in your debt.

But overall, your loan amount will have less of an impact than how you manage payments. Focus on making your monthly personal loan payments on time and in full to minimize any negative impact to your credit score.

How long does it take for a personal loan to help your credit score?

It will take around a month for a new account to appear on your credit report. But the time it takes for a personal loan to raise your credit will vary depending on your situation and how you manage your payments.

What happens to your credit score if you pay off the personal loan early?

Paying off a personal loan early—or at the end of your repayment term—could have a temporary detrimental impact on your credit score because that loan factors into your overall credit mix.

For instance, if you have a personal loan, auto loan, and two credit cards, your credit mix won’t be as varied when you pay off your personal loan. But credit mix is a more minor factor in popular credit scoring models, so the impact of an early payoff should be fairly small.

Can shopping around for personal loans hurt your credit score?

Shopping around for a personal loan may hurt your credit score, depending on the time frame in which you compare loans. Applying for multiple loans often results in multiple hard inquiries, which can harm your credit score more than a single hard inquiry.

But the FICO model accounts for rate shopping when you apply for an installment loan. Multiple hard inquiries within a 14-day window may count as a single inquiry, minimizing any negative impact on your credit score.

Does refinancing a personal loan affect your credit score?

Refinancing a personal loan may affect your credit score. Obtaining a new loan will result in a hard credit pull, and refinancing a loan will also influence the age of your accounts because you’re paying off an older loan with a new one. The hard pull and new account can lower your credit score.

About our contributors

-

Written by Jess Ullrich

Written by Jess UllrichJess is a personal finance writer who's been creating online content since 2009. She specializes in banking, investing, tax relief, and loans. She is a former financial editor at two popular online publications.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.