If Great Lakes serviced your federal student loans, you’ve probably received letters or emails from Nelnet. You’re probably also wondering why you’re hearing from a new loan servicer—and understandably so.

Transferring to a new loan servicer isn’t uncommon, but it’s easier to make that transition when you know what to expect. Keep reading as we guide you through why Great Lakes borrowers switched to Nelnet and how this change impacts you.

Can I refinance or consolidate my former Great Lakes student loan?

Refinancing or consolidating your Great Lakes student loans is always an option, even if you aren’t facing challenges with your current servicer.

Both choices let you condense multiple loans into one, but that’s about where the similarities end. Take a look at the table below for a closer look at the differences between student loan refinancing and consolidation.

| Refinancing | Consolidation | |

| What it is | Take out a new loan to pay off existing loans | Combine existing loans into one |

| Eligible loans | Private, federal | Federal |

| Credit check required? | Yes ✔️ | No ✖️ |

| Apply through… | Private lender | ED |

| Lower monthly payment? | Sometimes | Sometimes |

| Lower interest rate? | Sometimes | No ✖️ |

| Keep federal benefits? | No ✖️ | Yes ✔️ |

Do you have private student loans too?

While Aidvantage manages your federal student debt, many borrowers also carry private student loans. If you are looking to lower your monthly payments or secure a better interest rate on your private loans, refinancing may be the smartest move, even if your loan is in default. Check out the comprehensive review of the top student loan refinance companies to see if you can save.

In general, refinancing is best for students who exclusively borrowed private student loans. Conversely, student loan consolidation is reserved for federal loans.

While you can technically refinance federal loans, this isn’t always the wisest decision. If you do, you’ll lose federal loan benefits, like student loan forgiveness and income-based repayment.

Here are a few other scenarios to help you choose between consolidation and refinancing:

| If you… | Then consider… |

| Want a new loan servicer | Consolidation |

| Hope to release your cosigner | Refinancing |

| Don’t want to run your credit | Consolidation |

| Can qualify for a better rate | Refinancing |

| Only have federal loans | Consolidation |

| Have private student loans | Refinancing |

If you opt to consolidate your federal loans, your next step is applying for a Direct Consolidation Loan. Alternatively, if you’re going the refinancing route, it’s time to research lenders, starting with our list of the best student loan refinance companies.

Should problems persist or worsen, you might consider changing your loan servicer by refinancing or consolidating your loans.

What if I was a Great Lakes borrower?

Back in June 2023, Great Lakes merged with Nelnet, another long-established loan servicer. As a result, Great Lakes stopped servicing student loans, and Nelnet took over its loan portfolio.

Despite shifting to a different company, there’ll be minimal impact on your student debt. Just like when you switch cell phone providers but keep the same device and phone number, all that’s changing is who processes your payments and who you contact for support.

Curious about how this works in practice? Here’s how to navigate the servicer swap seamlessly.

Who is servicing my Great Lakes student loan now?

According to the U.S. Department of Education (ED), Nelnet is the new servicer for Great Lakes student loans. All borrowers who were previously assigned to Great Lakes should be with Nelnet, but it never hurts to double-check.

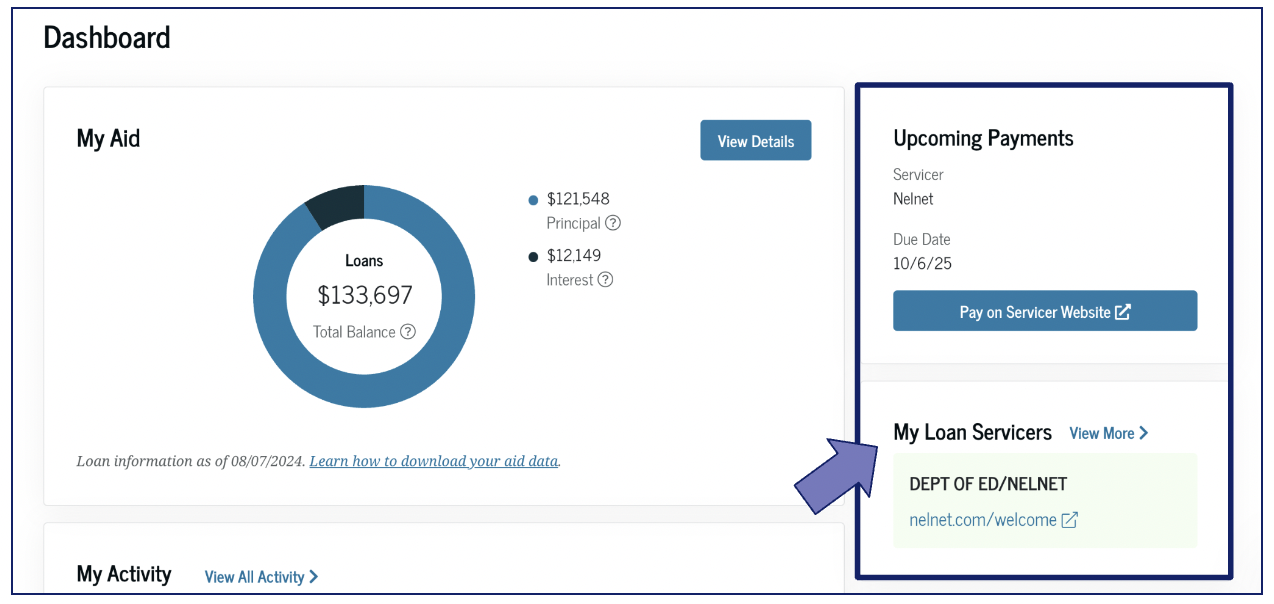

To confirm that Nelnet is your loan servicer, you can check your student loans on the Federal Student Aid website. When you log in, you’ll see an overview of your loan balance, including which company services your loans.

Use the link provided to visit your servicer’s website, or click “View More” for additional details about your loan servicer.

How can Great Lakes borrowers make payments on their loans now?

Making a payment with Nelnet works in much the same way as it did with Great Lakes. The primary difference is that you’ll now submit your loan payments through Nelnet instead of Great Lakes. Here’s how:

- Pay online through the Nelnet website.

- Enroll in autopay.

- Call to pay over the phone.

- Mail in a paper check.

- Set up bill pay through your bank.

Before you can utilize autopay or make online payments, you must create a new account with Nelnet. Since borrowers’ usernames and passwords don’t transfer alongside their student loans, your Great Lakes login credentials won’t work with Nelnet.

Nelnet refers to automatic payments as “auto debit.” It’ll reduce your student loan interest rate by 0.25% when you sign up.

Has my loan interest rate or terms changed after the transfer?

All that’s changed is which student loan companies service your loans. Your interest rate, loan terms, and outstanding balance should remain the same.

Your repayment status remains constant, too. For example, if you were in deferment with Great Lakes, you’d still be in deferment with Nelnet. This sounds straightforward, and in large part, it is. But where this can get confusing is on your credit report.

When your loans transfer to Nelnet, your Great Lakes account may say “closed” or “paid in full.” That account status suggests that your student debt is settled. In this case, however, it simply means that your account changed hands.

Longing for the day when your education debt becomes a thing of the past? Learn how to pay off student loans quickly with tips to adapt to any budget.

Can I still contact Great Lakes borrowing services with questions?

There’s currently no way to contact Great Lakes. Before shuttering its website and disconnecting its phone number, Great Lakes posted a message directing borrowers to contact Nelnet going forward.

While we didn’t find active contact information for the former loan servicer, we did come across a fictitious website cosplaying as Great Lakes. The site uses the Great Lakes name, logo, and even phone number.

It’s not an exact dupe of the now-defunct Great Lakes website, but that doesn’t make it any less dangerous. Rather than risking a run-in with an imposter, it’s best to heed Great Lakes’ advice and direct any questions to Nelnet.

How do I contact my new loan servicer?

Nelnet supplies borrowers with several ways to get in touch, including:

- Phone: Call Nelnet at 888-486-4722 from within the U.S. If you’re calling internationally, dial 303-696-3625. For military-specific questions, call 855-324-4027.

- Mail: Borrowers in most states can send general correspondence to P.O. Box 82561, Lincoln, NE, 68501-2561. California residents can contact Nelnet at P.O. Box 82578, Lincoln, NE, 68501-2578.

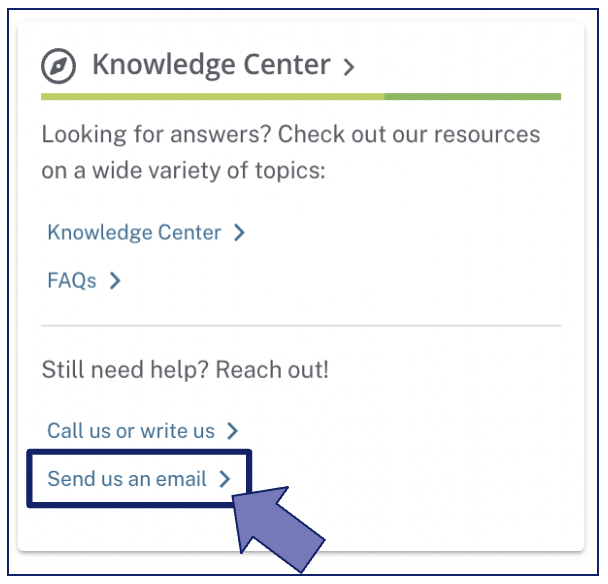

- Chat: For instant assistance, click the blue bubble in the bottom right corner of Nelnet’s website.

- Email: To send Nelnet a message, log in to your account. Scroll down until you see “Knowledge Center,” then select “Send us an email.”

While chat and email are available around the clock, Nelnet’s call center isn’t. Here’s when to call, in Eastern time, if you need to speak with a live human:

- Monday: 8 a.m. to 9 p.m.

- Tuesday and Wednesday: 8 a.m. to 8 p.m.

- Thursday and Friday: 8 a.m. to 6 p.m.

Furthermore, Nelnet lists additional addresses for payments, documents, and bankruptcy claims. If you’re sending mail to Nelnet for any of these purposes, visit Nelnet’s website or contact Great Lakes student loans customer service to ensure you’re sending your information to the right place.

What should I do if I’m having trouble with my new loan servicer?

If you’re unsatisfied with your new loan servicer and can’t reach a resolution with its representatives, you can file a complaint with ED.

When you submit a complaint, you’ll have the opportunity to share your grievances and describe your desired outcome. There’s no guarantee that you’ll get this result, but the formal complaint at least lets you escalate the issue and move closer to a solution.

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.