Some YouTube creators and online personalities promote using a home equity line of credit (HELOC) to pay off your mortgage early as a so-called “mortgage payoff hack.” But does it really work?

In reality, replacing a fixed-rate mortgage with a variable-rate HELOC can be risky. While you might lower your interest rate in the short term, you’re not eliminating debt; you’re just shifting it. Whether this strategy actually helps depends on your rate, timeline, and discipline.

This guide breaks down how using a HELOC to pay off a mortgage works, the pros and cons, and when you might be better off with options like mortgage refinancing or just making extra payments.

Table of Contents

Can you really use a HELOC to pay off your mortgage?

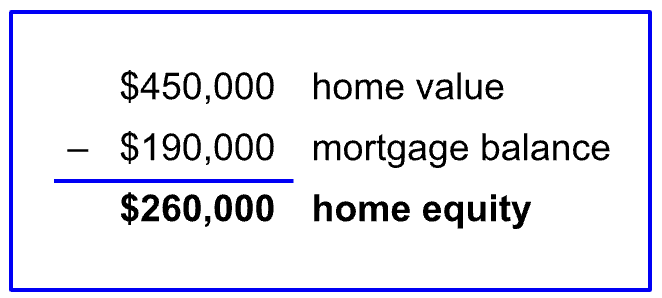

Yes. Many lenders allow you to borrow against your home equity through a HELOC and use the funds to pay off your remaining mortgage balance. In this scenario, you no longer owe your mortgage lender but are instead repaying the HELOC.

However, this isn’t technically “paying off” your home. You’re simply replacing one form of secured debt with another. And because HELOCs usually come with variable interest rates, the new loan could become more expensive over time.

So while this is possible, whether it’s smart is another matter entirely.

Is this actually a smart mortgage payoff strategy?

Many personal finance experts (and Reddit commenters) say no. The math only works if your HELOC rate stays lower than your mortgage rate and you stick to an aggressive repayment schedule.

Another important consideration: Interest on most HELOCs starts accruing immediately and daily, even if you don’t use the full line. If you’re using your HELOC for everyday expenses or holding a balance between paychecks, you could end up paying more in interest than on your original mortgage.

Ultimately, you risk trading a stable fixed-rate loan for a more volatile one that could cost more in the long run. You might also lose the mortgage interest tax deduction and pay thousands in fees.

In most cases, making extra payments on your mortgage or refinancing into a lower rate are simpler, safer ways to get debt-free faster.

Alternatives to using a HELOC to pay off your mortgage

If your goal is to pay off your mortgage faster or lower your interest rate, you have other options, some of which don’t require replacing one loan with another.

- Make extra payments: Even one extra payment per year toward your principal can shave years off your mortgage and save thousands in interest.

- Refinance your mortgage: If rates have dropped or your credit has improved, you may be able to lower your interest rate and monthly payment by refinancing—without the risk of variable HELOC rates.

- Use a mortgage recast: If your lender allows it, a lump-sum payment toward your mortgage balance could qualify for a recast, which recalculates your monthly payment without a full refinance.

Will a HELOC help me pay off my mortgage faster?

Many so-called “mortgage payoff hacks” promoted online rely on perfect timing, tight budgeting, and ideal market conditions. But without a fixed rate or firm repayment strategy, you’re exposed to rising costs and confusion. As several Redditors pointed out in the thread below, this strategy often replaces a stable mortgage with a riskier loan structure:

But in a few limited cases, it can help you pay off your mortgage faster—if your HELOC rate is lower than your mortgage rate and you keep making the same monthly payment. More of your payment will go toward principal, which could help you pay down the loan faster.

Just keep in mind: Most HELOCs accrue interest daily, not monthly. That makes repayment discipline even more important if you want to see real savings.

If rates rise or you reduce your payments, you may not save anything and could even end up paying more.

Refinancing your mortgage for a lower rate is likely the safer option to help you save money.

How much can I borrow with a HELOC to pay off my mortgage?

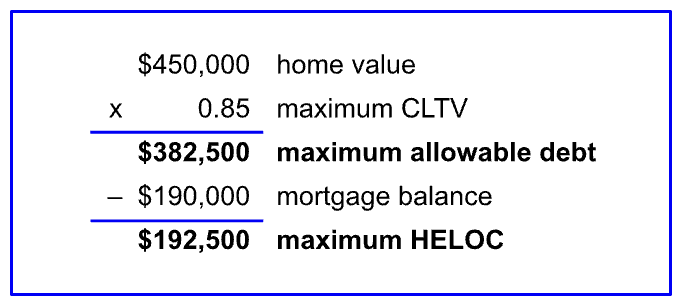

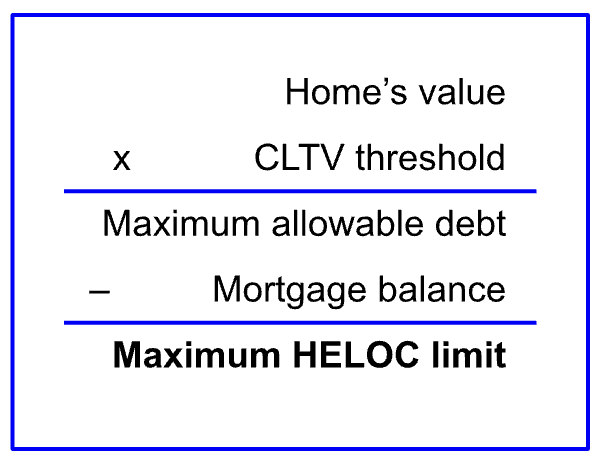

Lenders typically cap your combined loan-to-value ratio (CLTV) at 70% to 90%. That includes your existing mortgage and new HELOC.

Example:

- Home value: $450,000

- Mortgage balance: $190,000

- Max CLTV: 85%

- Max total debt: $382,500

- Max HELOC size: $192,500

Your credit score, income, and location can also affect your limit.

Pros and cons of using a HELOC

Using a HELOC to pay off a mortgage offers a few benefits, but be aware of the drawbacks as well.

Pros

-

Possibly lower interest rate than mortgage

-

Potentially lower monthly payments (during draw period)

-

Flexible borrowing for other expenses

-

Faster payoff if rate is lower and payments are steady

Cons

-

Doesn’t reduce your debt, just shifts it

-

Most HELOCs have variable rates

-

Interest may not be tax-deductible

-

Potential fees and closing costs

-

Interest on HELOCs accrues daily

How to use a HELOC to pay off a mortgage

Using a HELOC to pay off your mortgage involves replacing one form of home-secured debt with another. Here’s how the process typically works:

- Get a mortgage payoff quote from your lender so you know the exact amount needed.

- Estimate your home’s value to calculate your equity.

- Apply for a HELOC with a lender offering favorable terms (ideally fixed or rate-lock options).

- Get an appraisal, if required by the lender.

- Review and sign your HELOC agreement, then withdraw funds.

- Pay off your mortgage using the HELOC funds.

Heads up: This process can take several weeks and may involve closing costs or appraisal fees.

The relative benefits and drawbacks of using your HELOC to pay off your mortgage depend almost entirely on your HELOC rate and repayment habits. These strategies can help you combat any potential volatility:

Pick a HELOC with a fixed rate

Not all have variable interest rates. If you want to hedge your bets against a possible rate increase, choose a lender (like Figure) that offers fixed-rate HELOCs. Depending on the overall interest rate environment, your starting rate may be higher than a variable-rate HELOC, but you’ll have peace of mind.

Choose a HELOC that allows you to lock in rates

HELOCs with fixed-rate conversion options allow borrowers to “lock” their rate at specific points of the draw period. If you plan to borrow a large chunk to pay off your home mortgage balance, you may be able to secure your rate just after opening the line of credit.

Pay off your HELOC balance as soon as possible

Instead of paying interest during your draw period, pay as much as possible toward your monthly balance. The sooner you pay off your borrowed home equity, the less you’ll pay in interest, and the earlier you’ll get out of debt.

Does having a mortgage make it difficult to get a HELOC?

Having a mortgage won’t necessarily prevent you from getting approved for a HELOC, but it will reduce the size of your HELOC.

Lenders often won’t let you borrow 100% of your home’s equity through a HELOC, instead limiting your HELOC to 70% to 90% of your equity, minus any outstanding debt obligations.

In our earlier example, your lender set its CLTV threshold at 85%. In theory, you could borrow $382,500. But because you still owed $190,000 on your mortgage, you could only borrow the difference between that $382,500 limit and your unpaid mortgage balance:

Your CLTV considers all the liens against your property, not just your mortgage. For example, second mortgages and home equity loans will decrease what you can borrow with a HELOC.

Your income, credit score, and zip code can also affect your HELOC amount. Knowing and understanding these HELOC requirements can help you determine if you’re likely to qualify and for how much.

Lenders reserve their maximum CLTV for the most eligible borrowers, so if your credit score or income is lower, your debt-to-income ratio (DTI) is higher, or you’re located in certain states, your HELOC limit could be lower.

Where to get a HELOC to pay off a mortgage

Refinancing your mortgage is often the better strategy. You might be able to refinance even if you’ve done so before.

But in the rare event a HELOC is truly the preferred option, these two lenders offer unique benefits.

Note: If your credit score is below 720, it is unlikely that you will pass the prequalification stage for most HELOC lenders. If your score is higher than 580, see our highest-rated HELOCs for fair credit. Below 580, look into home equity agreements as an alternative.

Figure

HELOC details

| Rates (APR) | 8.35% – 16.55%ⓘ |

| Funding amount | $15,000 – $400,000 |

| Repayment terms | Draw: 2 – 5 years / Repayment: 5, 10, 15, or 30 years |

| Min. credit score | 640 |

| Prequalify | Get your estimate in under 5 minutes |

FourLeaf

HELOC details

| Rates (APR) | 12-month intro rate starting at 6.99% for qualifying borrowers, then variable starting at 8.50%ⓘ |

| Loan amounts | $10,000 – $1 million |

| Repayment terms | Draw: 10 years / Repayment: 20 years |

| Min. credit score | 670 |

FAQ

Can you refinance a mortgage with a HELOC?

Refinancing a mortgage and taking out a HELOC are two separate ways to tackle tough mortgage payments. However, you can use a home equity line of credit to pay off your mortgage.

How can I calculate the savings of using a HELOC to pay off my mortgage?

To calculate your savings from using a HELOC to pay off your mortgage, you must:

- Determine how much you have left to spend over the life of your mortgage, including principal and interest. You can refer to your loan amortization schedule to determine how much you’ll still spend over the remaining years.

- Determine what your total HELOC cost would be, including principal and interest.

- Subtract the HELOC total from the mortgage total to calculate the savings.

However, several elements could throw a wrench into this plan:

- HELOCs are traditionally variable-rate, meaning you cannot assume a steady interest rate over the life of the line of credit—and there’s no way to predict what interest rates will be in the future.

- HELOCs may have closing costs and annual fees that eat into any savings you may access from paying off your mortgage with one.

- You could potentially make larger payments toward your principal balance during the HELOC’s draw period to save a lot of money on interest and thus further maximize your savings.

About our contributors

-

Written by Timothy Moore, CFEI®

Written by Timothy Moore, CFEI®Timothy Moore is a Certified Financial Education Instructor (CFEI®) specializing in bank accounts, student loans, taxes, and insurance. His passion is helping readers navigate life on a tight budget.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.