An interest-only HELOC (home equity line of credit) lets you borrow against your home’s equity while paying only interest for a set time. These types of loans can be helpful if you’re flipping houses, planning to sell your home soon, or just want to keep your initial monthly payments low.

Most lenders offer interest-only payments during the draw period only, typically 10 years. However, some banks like First Fidelity and SouthState provide fully interest-only HELOCs for the entire loan term. Here are the draw periods for several top-rated lenders.

| Lender | Draw period |

| FourLeaf FCU | 10 years |

| Hitch | 10 years |

| Spring EQ | 10 years |

| First Fidelity Bank* | 7-10 years |

| SouthState* | 5 or 10 years |

| Unison** | None |

Table of Contents

What is an interest-only HELOC?

There are two common types of interest-only HELOCs — those where you make interest-only payments during the draw period and those where make interest-only payments the entire time with one large payment due at the end. Here’s a closer look.

Type 1: Interest-only payments during the draw period

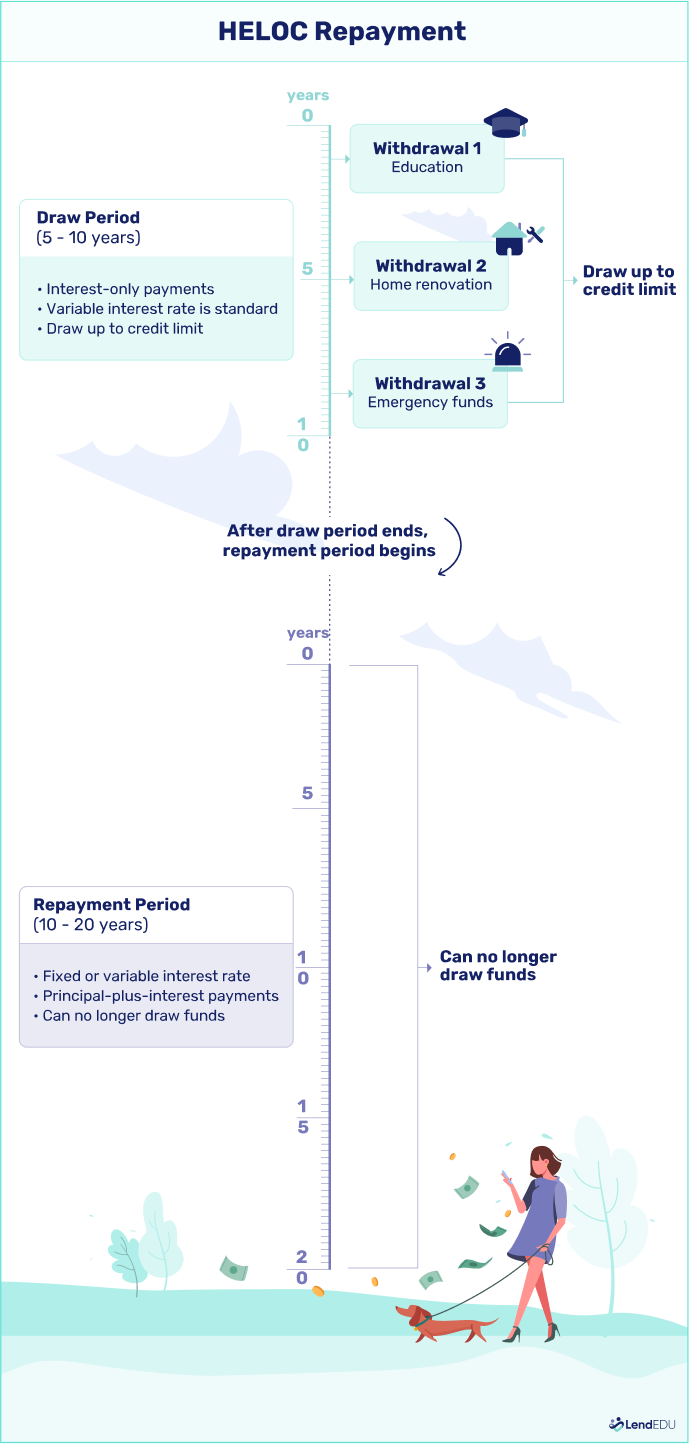

The first type of interest-only HELOC is what you find most often. You make interest-only payments during the draw period, which usually lasts five to 15 years.

Like a credit card, you can repay your outstanding HELOC balance at any time during the draw period and then borrow it again. Your monthly payment will vary, depending on how much you’ve borrowed. The HELOC interest rate is typically variable, which can also cause your payment to change.

After the draw period ends, you enter the repayment period, which is when you make traditional principal and interest payments. The repayment period may last 15 to 25 years. Once it ends, you will have fully paid off your loan.

While HELOCs and home equity loans both use your home as collateral, they work differently. A HELOC allows repeated borrowing, like a credit card. A home equity loan provides a lump sum upfront with fixed payments.

The following graphic illustrates how the draw and repayment period works for most HELOCs with interest-only draw periods:

Here’s an example to add perspective:

- You have a $100,000 HELOC with an outstanding balance of $50,000.

- You have an annual interest rate of 6%.

- Your monthly interest-only payment on this balance would be $250.

Your payment will also change as your balance increases or decreases or your variable interest rate changes. For example:

- You draw the full HELOC up to its $100,000 credit limit.

- Your monthly payment would be $500 at 6% interest.

- It would increase even more to $583 if the rate rose to 7%.

While the amount you owe each month varies based on the amount you borrow, you won’t need to worry about paying down the principal amount you’ve borrowed until later (unless you want to). This can be helpful if you face limited cash flow during the draw period.

However, when the draw period ends, your payment will be spread over the remaining term and include both principal and interest. For example:

- At the draw period’s end, let’s say your balance is $100,000.

- You have a fixed interest rate of 7%, and the term is 20 years.

- Your monthly payment would be about $775.

Type 2: interest-only payments the entire time

The second type of interest-only HELOC is less common. It’s where you make interest-only payments for the entire loan term, followed by one big balloon payment at the end.

You can draw from your line of credit as much as you want throughout your entire term, up to your line limit. There is no separate repayment period where borrowing is off-limits.

Here’s an example for context:

- You have a $100,000 HELOC with a 6% interest rate and a 10-year term.

- Your monthly payment would be $500 (interest only).

- It would increase even more to $583 if the rate rose to 7%.

- After 10 years, you’d owe a $100,000 balloon payment.

First Fidelity Bank and SouthState Bank both offer fully interest-only HELOCs.

This type of interest-only HELOC can be useful if you’re 100% positive you’ll have enough cash to fully cover your balloon payment when it comes due. But it’s also very, very risky. If you can’t make the balloon payment, you could lose your home.

Pros & cons of an interest-only home equity line of credit

An interest-only HELOC gives you lower payments initially, but it also comes with the risk of higher payments later on. Here’s a breakdown of the main advantages and disadvantages:

Pros

-

Flexible borrowing

You can borrow and repay funds repeatedly during the draw period (or during the entire term for interest-only HELOCs with a balloon payment).

-

Low initial payments

This keeps your initial costs low and frees up cash flow for other goals.

-

Lower rates than credit cards and personal loans

This is because your home secures the HELOC.

-

Interest can be tax-deductible

This is the case if you buy, build, or substantially improve your home and itemize the deductions.

Cons

-

Larger payments later

You’ll either have full principal and interest payments after the draw period or one final balloon payment for your remaining loan balance.

-

Your home is collateral

This puts your house at risk if you can’t repay.

-

Generally have variable interest rates

Rates can change over time and potentially increase your payments.

-

Higher total interest

You may pay more interest over time if you carry a balance long-term.

Is an interest-only HELOC right for you?

Interest-only HELOCs have their place, but they’re not a good fit for everyone. See below to find out when one of these loans may be best—and when they’re better off avoided.

| If you … | Consider an interest-only HELOC? |

| Want low payments now & can afford larger payments later. | Yes |

| Want to access your home equity on demand. | Yes |

| Want to use the funds for a higher-return investment & are comfortable putting your home at risk. | Yes |

| Flip houses & prefer to use home equity to fund it. | Yes |

| Are buying another home & want to use home equity to fund the down payment before you sell. | Yes |

| Want a lower rate than a credit card or personal loan offers. | Yes |

| Struggle with budgeting or financial planning. | No |

| Have a small amount of home equity. | No |

| Are financially unstable. | No |

| Want to reduce total financing costs. | No |

When an interest-only HELOC may make sense …

The flexibility of an interest-only HELOC may make sense in several situations:

- You prefer low payments now, with the ability to cover larger payments later: Don’t let the appeal of low monthly payments reel you in, though. You must have a plan for how you’ll make larger payments later.

- Want to access your home’s equity on demand: With a HELOC, you can get the funds immediately rather than potentially waiting weeks for approval on a home equity loan or other financing.

- Plan to use the funds for a higher-return investment: Interest-only HELOCs can be ideal if you have a lot of home equity and want to use the funds toward investments with higher interest earnings. But make sure you’re comfortable with the risks.

- Flip houses: HELOCs provide flexible financing for buying, repairing, and selling properties. But remember, your home is at risk if the flip doesn’t go as planned.

- Need to use your home’s equity for a down payment on another home: These loans can also be a good option if you need funds for a down payment or closing costs on a new property and plan to sell your old home shortly.

- Prefer a more affordable financing option than a credit card or personal loan: HELOCs typically offer lower rates and potentially higher credit limits (depending on how much equity you have in your home).

When an interest-only HELOC might not make sense …

You should avoid an interest-only HELOC if your income is unstable (and you’re not confident it will rise in a few years) or if you can afford to make more than interest payments now.

Interest-only HELOCs might also be unwise if:

- Budgeting or financial planning isn’t your strong suit: Since your monthly payment will vary with a HELOC, budgeting can be more difficult. If you’re not good at managing your budget, you should avoid using a HELOC.

- Cost-saving is your goal: The costs of a HELOC can quickly add up if you carry a balance, make interest-only payments, and don’t pay down the principal balance. The quicker you pay down the principal balance, the less you’ll pay in interest on the loan.

- Equity in your home is low: You typically need to maintain at least 80% to 85% home equity to get approved after factoring in your mortgage balance and the HELOC limit. A HELOC may not work if you haven’t yet built up much equity in your home.

- Financial stability is weak: Not only will your payments vary during the draw period as your interest rate changes and balance fluctuates, but the payment may significantly increase during the draw period. If your income and expenses are unstable, you may want to avoid a HELOC.

I’ve seen several examples where people will use a HELOC for home renovations to improve the value of their home with the intention of selling it later. Also, many will access their home equity to help pay for their children’s higher education needs because HELOCs can be more affordable than private student loans. It becomes problematic when people have a spending problem and no real strategy for how they will be using it. I’ve heard, ‘I can deduct the interest,’ which is only the case if you itemize deductions, and most people don’t have enough deductions to do so and can’t deduct anything extra.

Crystal Rau, CFP®

What to consider before your HELOC’s interest-only period ends

Regardless of how well you plan, it can be hard to make those increased payments once your HELOC’s term or draw period ends. You can use these strategies to ease the burden or even remove it.

Make more than the minimum payment

If you can, start making payments that are more than interest during your draw period. Making even a small dent in your principal balance can shave months off your repayment timeline and reduce the interest you’ll pay over time.

Ultimately, a home equity line of credit is intended to be used as a line of credit, meaning you should quickly repay the principal after you borrow it. Using the HELOC as intended will save you money in the long run.

Replace your HELOC with a home equity loan

Home equity loans let you tap your home equity for quick cash. They often come with fixed rates that might be lower than variable rates HELOC. For this reason, if you don’t need to access the funds more than once, a home equity loan is often the better option.

If you’re eligible, you can refinance your HELOC into a home equity loan. This would mean lower payments and less interest paid in the long haul.

Consider a cash-out refinance

Refinancing into a larger mortgage loan via a cash-out refinance can free up cash and help you pay off that HELOC balance. Depending on the interest rate environment, you may even get a lower rate than your current mortgage. That would mean lower mortgage payments and overall cost savings.

Downsize your home (or just sell it)

Once your term or draw period ends, you could sell your home and downsize to a smaller property (if the timing works). Once your home sells, you could use the proceeds to pay off your mortgage and HELOC, using any leftovers as a down payment on a smaller, less expensive property.

This is a terrific option if you’re nearing retirement or are an empty nester.

Renew your credit line

Depending on how much equity you have in your home, your lender may allow you to renew your home equity line of credit once the draw period ends.

This would let you keep that lower monthly payment and put off the higher-payment period until later. A warning, though: This means paying more interest in the long run (and spending more time in debt).

Also, lenders will typically want to see that you’ve been using the HELOC as intended – or have enough cash to do so – before agreeing to offer you a new interest-only draw period. If you can’t show that you can afford to do this, the lender probably won’t agree to the renewal.

Consider a reverse mortgage

If you’re 62 or older, you might consider a reverse mortgage to help you pay off your HELOC balance and fund your retirement. These mortgages pay you (either in a lump sum or monthly payment) to live in your home.

They’re a solid option if you’re on a fixed income and need to reduce your monthly costs. Once you vacate the property, the lender pays off the loan balance (plus interest) with the proceeds from the home sale.

Where to find HELOC lenders

Most major mortgage lenders offer home equity lines of credit with interest-only draw periods (though a few have balloon payment options). As with any mortgage loan, shopping around for a HELOC is important. Compare customer service, rates, and other factors before making your decision.

Need help choosing the right lender for your interest-only HELOC? Here are our top-rated HELOC lenders that offer an interest-only option.

Determine whether you are looking at HELOC options due to a want or a need. For example, say you dislike the floors in your home. A HELOC may be a solid option to replace them if you plan to update them then sell the property for a higher selling price. It may be unwise if you’re short on cash and just want new floors. Either way, ensure you go in with a proper strategy of using a HELOC responsibly and a way to pay it off ASAP.

Crystal Rau, CFP®

FAQ

Can I get an interest-only home equity loan?

No, most lenders do not offer interest-only home equity loans. However, if you have sufficient equity in your home—typically at least 15% to 20%—you may be able to get approved for an interest-only home equity line of credit (HELOC).

With most HELOCs, the initial draw period (often five to 15 years) will include interest-only payments followed by a repayment period with standard principal and interest payments (often 15 to 25 years). However, some lenders like First Fidelity Bank and SouthState Bank have interest-only HELOCs with one final balloon payment at the end.

Alternatively, Unison offers a unique home equity sharing agreement. Unlike loans or HELOCs, Unison’s product doesn’t require monthly payments. Instead, it invests in a portion of your home’s future value. You receive a lump sum now and settle the investment when you sell your home or after 30 years. This option doesn’t involve interest charges or affect your credit score like a HELOC would.

Do all HELOCs have an interest-only option for repayment?

Most HELOCs allow you to make interest-only payments during the initial draw period. The loan will enter a traditional repayment period requiring principal and interest payments after the draw period ends (usually no longer than 15 years).

However, some lenders offer fully interest-only HELOCs. With these, you make interest-only payments for the entire loan term, followed by a large lump sum payment (also called a balloon payment) at the end to repay the principal.

Can I make more than interest-only payments during my HELOC draw period if I want to?

Yes. A HELOC is a revolving line of credit that allows you to borrow and repay the funds during the draw period. You can always pay more than the required interest-only payments. If you’re using the HELOC as intended, your goal should be to repay the principal as fast as possible.

If I make interest-only payments during the draw period, will I still pay interest during the repayment period?

Yes. Interest is charged on a HELOC any time you have an outstanding balance. When you’re in the draw period, you’re often just required to make interest payments. Once you’ve entered the repayment period, you must pay for interest plus reduce the balance with principal payments.

About our contributors

-

Written by Cassidy Horton, MBA

Written by Cassidy Horton, MBACassidy Horton is a finance writer passionate about helping people find financial freedom. With an MBA and a bachelor's in public relations, her work has been published more than 1,000 times online.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Crystal Rau, CFP®, CRPC®, AAMS®

Reviewed by Crystal Rau, CFP®, CRPC®, AAMS®Crystal Rau, CFP®, CRPC®, AAMS®, is a Certified Financial Planner based in Midland, Texas. She is the founder of Beyond Balanced Financial Planning, a fee-only registered investment advisor that helps young professionals and families balance living their ideal lives with being good stewards of their finances.