If you borrow a home equity line of credit (HELOC), you might not need to pay back the total amount right away. Like credit cards, HELOCs offer a revolving line of credit to access during your draw period, which often spans 10 years.

Many lenders let you make monthly interest-only payments during this time. After your draw period ends, you can expect to start making full principal and interest payments on the amount you borrowed over a repayment term of up to 20 years.

HELOCs often come with variable rates, so your monthly payment could change if your rate increases or decreases. In an environment with increasing interest rates, this is crucial to remember when determining what you can afford.

Table of Contents

HELOC payment formula

Understanding how your monthly HELOC payments are calculated is crucial for effective financial management. These payments can vary based on the amount you borrow, what phase of repayment you’re in, and whether you have a variable interest rate.

Amount borrowed

Your initial payment is determined by how much you draw from your HELOC. The more you borrow, the higher your interest charges, which leads to higher monthly payments.

Draw period vs. repayment period

- During the draw period: You are often allowed to make interest-only payments. This period typically lasts about 10 years.

- Repayment period: After the draw period ends, you will start to repay the principal and interest over a set term, which could extend up to 20 years.

Interest rate variability

Many HELOCs feature variable interest rates. This means the rate applied to your borrowed amount can change, affecting your monthly payments. An increase in rates leads to higher payments, and a decrease reduces your payment amount.

If only interest payments are required during the draw period, your monthly payment will be calculated as follows:

This formula helps you grasp the basic structure of your payments during the draw and repayment periods.

How is HELOC interest calculated?

Interest on a HELOC is often calculated using a simple interest formula, applied to the outstanding balance of the line of credit. The formula for calculating your monthly interest payment is straightforward:

This calculation is performed monthly because the interest rate on a HELOC is variable and can shift over time based on market conditions. For example:

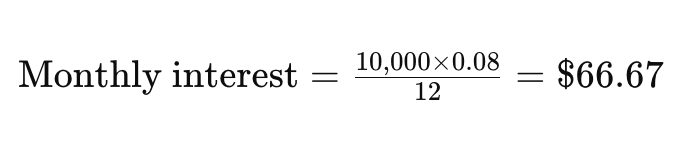

- During the draw period: If you have an outstanding balance of $10,000 with an annual interest rate of 8%, your monthly interest payment would be:

- Rate adjustments: If the interest rate increases to 9%, the new monthly interest payment on the same balance would increase:

This method ensures your payments adjust with fluctuations in the interest rate, which affects the total amount you pay over the life of your HELOC.

By understanding these fundamental calculations, you can better anticipate changes in your monthly payments and plan accordingly for the draw and repayment phases of your HELOC.

You can opt to pay off your HELOC sooner. Paying back the amount you borrowed means it becomes available to take out again if your draw period is still active. Lenders may charge a prepayment penalty for paying off your HELOC ahead of schedule, so check with your lender first.

FAQ

Why is my HELOC payment $0?

If you haven’t made any withdrawals from your HELOC, your monthly payment will be $0. You haven’t borrowed from your line of credit, so you don’t have to pay anything back from month to month.

If you’ve borrowed from your HELOC, there might have been a delay in processing the amount you owe. Contact your lender if you think there’s been a mistake, and keep an eye out for next month’s bill to see whether you owe interest on your withdrawal.

What if my HELOC payment due looks wrong?

If your HELOC payment looks wrong, contact your lender to discuss the issue. Calling customer service is often best, but some lenders may assist through web chat, email, or a secure message via your online account.

What is the minimum monthly payment on a HELOC?

Some lenders require you to make a minimum monthly payment on your HELOC. The amounts will vary by lender. For example, your lender might require monthly payments of the greater of 1% of your outstanding balance or $50.

During your repayment period, your minimum HELOC monthly payment is often the principal and interest amount necessary to pay off your HELOC in full by the end of your term, similar to a mortgage.

What if I can’t afford my HELOC payment?

If you can’t afford your HELOC payment, contact your lender to discuss your options. It may be able to adjust your repayment term to give you a more affordable monthly payment.

You can also explore options for refinancing your HELOC into a new mortgage or home equity loan. However, you’ll still need to make monthly payments on your new loan.

About our contributors

-

Written by Rebecca Safier

Written by Rebecca SafierRebecca Safier is a personal finance writer with years of experience writing about student loans, personal loans, budgeting, and related topics. She is certified as a student loan counselor through the National Association of Certified Credit Counselors.

-

Edited by Kristen Barrett, MAT

Edited by Kristen Barrett, MATKristen Barrett is a managing editor at LendEDU. She lives in Cincinnati, Ohio, with her wife and their pack of senior rescue dogs. She has edited and written personal finance content since 2015.