The maturity date on a HELOC is when your draw period ends, and you must start repaying the principal plus interest—no more borrowing. It’s the official transition into repayment, sometimes called the reset date. Knowing this date is key to planning your finances, so you’re not caught off guard when payments increase.

If you’ve used a HELOC to tap your home equity, make sure you understand when and how repayment kicks in to avoid surprises.

Table of Contents

- Does the maturity date mean my HELOC is paid off?

- When will my HELOC reach its maturity date?

- Where can I find my HELOC maturity date?

- Will my lender notify me when my HELOC nears its maturity date?

- What should I do after I receive a HELOC maturity notification?

- How might my payments change after my HELOC maturity date?

- How long will it take to pay off my HELOC after the maturity date?

- What if I want to continue to borrow from my HELOC after its maturity date?

- Can I pay off my HELOC before the maturity date?

- FAQ

Does the maturity date mean my HELOC is paid off?

The maturity date doesn’t mean your HELOC is paid off. It’s when the outstanding balance on your loan—including principal, interest, and fees—becomes due. This is essentially the beginning of the repayment period.

Once a HELOC matures, you’ll pay off what you borrowed according to your lender’s repayment schedule. You may have been making interest-only payments during your draw period.

Depending on your HELOC’s structure, at the end of the draw period, you’ll repay the principal balance in full (called a balloon payment) or begin making principal and interest (P&I) payments. Some lenders, like Figure, require P&I payments through the draw period, in which case, your payment won’t change, but you will no longer be able to draw from the credit line.

The payoff date for a HELOC is the estimated date you’ll pay off your line of credit if you make your payments as scheduled. Your loan documents should outline your HELOC’s maturity and payoff dates. Your lender may charge a penalty if you pay off your HELOC balance before the final payoff date.

When will my HELOC reach its maturity date?

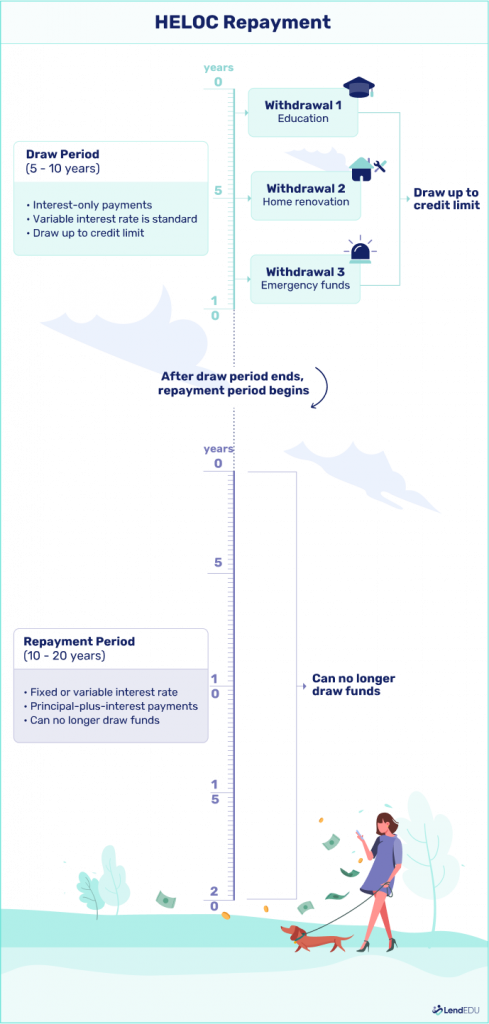

HELOCs have two phases: the draw period and the repayment period. Your HELOC will reach its maturity date at the end of the draw period—often after five to 10 years.

The draw period is the initial window to access your line of credit and withdraw. Your lender might require you to make interest-only payments toward your HELOC during this time.

A typical draw period for a HELOC lasts five to 10 years, and the line of credit matures when it ends. Some lenders might extend the draw period to 15 years. The end-of-draw date marks when your HELOC transitions from the withdrawal phase to the repayment phase.

HELOC repayment periods may last 10 to 20 years, depending on the lender. You pay down the balance, including interest and fees, during the repayment period. In the table below, you can see what the best HELOC lenders offer for repayment term length options.

Where can I find my HELOC maturity date?

If you have a HELOC, you have several options to determine your maturity date:

- Check your statement. Your HELOC statement includes important information about your line of credit, including your balance due, recent activity, and interest charges. You may also find your HELOC maturity date listed here.

- Log in to your account. Most HELOC lenders offer online access to your account. You can review statements and other information about your line of credit, including when your HELOC matures.

- Review loan documents. At closing, you should get a stack of paperwork that includes all the details of your HELOC, such as the maturity date.

- Contact the lender. To avoid sifting through loan paperwork or statements, you can contact your lender to check your HELOC’s maturity date. You may need to call rather than email or request live chat, as the lender will likely need to verify your identity before releasing details about your line of credit.

While checking your HELOC maturity date, you may also want to review your payment schedule, interest rate, and fees.

Will my lender notify me when my HELOC nears its maturity date?

You’ll often receive a HELOC reset or maturity notification in writing from your lender at least six months before it’s scheduled to reset or mature. Lenders send these notifications early, so you have time to prepare for the next phase (e.g., get ready to make P&I payments, refinance the HELOC, or pay it off).

How you’ll receive the HELOC reset or maturity notification depends on your lender and your selected communication preferences. You may get it by mail, or—if you’ve selected paperless communication—you might receive an electronic notification from your lender.

There’s also no standard form for how these notifications look. They can vary from lender to lender, but expect the notification to include the following information:

- When your HELOC is scheduled to mature or reset. The notice provides details about the specific date your HELOC will mature or reset.

- What will happen at the maturity or reset date. The letter explains what will happen on this date, such as if you must make a balloon payment or begin P&I payments.

- How much you’ll owe at the maturity or reset date. If you’re still in the draw period, your lender might not specify the amount you’ll need to pay because you can still draw from the HELOC. However, it should include an estimate of the most you may need to pay.

- Who to contact if you have questions or concerns. You may have questions about your upcoming HELOC maturity or reset. The letter should provide information about whom to contact with questions. It may also include information on resources you can use to get help (e.g., housing counselors).

Every lender’s process is different. To know what to expect at your HELOC’s reset or maturity date, reach out to your lender. It can provide details about what to expect and answer any questions about its process.

What should I do after I receive a HELOC maturity notification?

You shouldn’t need to do anything with the HELOC reset or maturity notification except start thinking about what it means for your finances and future actions you might need to take. What you’ll need to do will depend on the phase your HELOC is in, and your circumstances, such as:

- Start making P&I payments. Once you’ve reached the end of the draw period, you may need to begin making P&I payments, often amortized over 10 to 20 years. Ensure you have room in your budget before reaching this reset date.

- Make a balloon payment of the principal balance. Depending on how your HELOC is structured, you might need to repay the entire principal balance at the maturity date. If you don’t have enough cash to do this, you’ll need to find a way to get the funds or refinance the HELOC.

- Refinance the principal balance of your HELOC. If you can’t cover a balloon payment with cash or want better rates or terms, you may consider refinancing your HELOC. You can do this few different ways, such as getting a home equity loan or by combining your mortgage and HELOC.

- Extend your HELOC or get a new one. If you want to continue to use your HELOC as a line of credit and don’t have a significant principal balance, your lender may be willing to extend the draw period—or you can apply for a new HELOC.

You might be in a situation where you can’t afford the payment because your financial situation changed, or you can’t refinance the HELOC because your home’s value deteriorated. If so, talk to your lender. Your lender may agree to modify your HELOC to help you avoid default and foreclosure.

How might my payments change after my HELOC maturity date?

As you reach maturity on a HELOC, if you don’t make a balloon payment, you’ll prepare to begin paying back the principal and interest on your line of credit. So what does that mean for your payments? Here are a few scenarios that could play out.

| During draw period, you made | In maturity, your payment may |

| Interest-only payments… | ⬆️ …increase to account for principal, interest, and fees. |

| Principal and interest payments, and your interest rate hasn’t changed… | …remain unchanged. |

| Principal and interest payments, and your interest rate adjusts at maturity… | ↕️ …increase or decrease depending on how the rate adjusts. |

Keep in mind your payments may change again once your HELOC reaches maturity if you have a variable interest rate. Since variable rates are tied to an underlying benchmark rate, they can move up or down over time according to shifts in the benchmark.

If you’d rather avoid fluctuations in payments, you might want to shop around for a fixed-rate HELOC option.

How long will it take to pay off my HELOC after the maturity date?

As we mentioned, a typical repayment period for a HELOC is 20 years, but some lenders might shorten it. Aven, for example, allows borrowers to choose among 5, 10, 15, or 30 years terms.

If you’re making payments as scheduled and not paying extra, it could take up to 20 years to repay what you borrowed.

Can you pay off a HELOC early? Yes, in most cases—and it could make sense if you’d like to minimize what you pay in total interest charges. (More about this below.)

What if I want to continue to borrow from my HELOC after its maturity date?

Once your HELOC matures, you can’t withdraw additional money from your credit line. If you want to continue tapping into your home equity after your line of credit matures, you have a few options.

- Ask about a renewal or extension. Your lender may allow you to renew or extend a HELOC before maturity to continue making new draws while delaying repayment. Contact your lender to find out whether these are options.

- Refinance your credit line. Refinancing a HELOC means taking out a new line of credit to pay off an existing one. You could restart the clock on the draw and maturity periods and even get more favorable interest rates and fees.

- Take out a new HELOC or home equity loan. If your lender is unwilling to offer an extension, and you don’t want to refinance your HELOC, you might consider taking out a new line of credit or home equity loan. You’d need sufficient equity, and it would mean paying a second round of closing costs.

If none of these options work, you can weigh other possibilities. For example, you might be able to borrow a lump sum with an unsecured personal loan. The upside here is you don’t have to use your home to secure the loan.

Can I pay off my HELOC before the maturity date?

Yes, you can pay off a HELOC during the draw period before it reaches maturity. You might consider that option if you:

- Want to minimize the interest and fees you pay.

- Would like to eliminate your HELOC debt faster.

- No longer need access to your credit line.

You can pay off a HELOC early by making lump-sum payments or paying extra each month.

For example, imagine you owe $50,000, and your interest rate is 5%.

| Monthly payment | Time to pay off | Total interest paid |

| $375 | 196 months (over 16 years) | $23,125 |

| $630 | 8 years | $10,734 |

If you paid an additional $255 per month, you’d pay off your HELOC in half the time and save $12,401 in interest.

Before you pay off a HELOC early, it’s wise to read the fine print on your loan agreement. Lenders may apply prepayment penalties for paying off a HELOC early. Calculating the fee can help you decide whether paying off your line of credit in advance makes sense.

FAQ

Can the interest rate on my HELOC change after the maturity date, and how would it affect my payments?

Yes, the interest rate on your HELOC could change after the maturity date. If it does, it might raise your payment amounts. This can occur if you opt for a variable-rate HELOC. Variable-rate loans fluctuate according to the market interest rates. If the rates go up, so will your payments, and vice versa.

Are there alternatives to paying off a HELOC if I can’t afford the increased payments after maturity?

Yes, you have alternatives if you find it challenging to afford the payments after your HELOC matures. You might consider refinancing your HELOC. By doing so, you can potentially secure a lower interest rate or extend your repayment term to lower your monthly payments. Consulting a financial professional is a smart course of action to explore these alternatives.

What should I do if my financial situation changes and I can no longer afford my HELOC payments?

If your financial position changes and you can’t afford your HELOC payments, contact your lender immediately. It may be able to assist you with a hardship plan, modify the loan terms, or even accept a short sale of the property to avoid foreclosure.

How can I calculate the total interest I will pay on my HELOC by the end of the repayment period?

To calculate the total interest on your HELOC, multiply the outstanding balance by your annual interest rate, then divide by 12 to get the monthly interest charge. Repeat this for each month you plan to draw funds, and keep a running sum to estimate the total interest.

Are there any tax implications associated with paying off or refinancing a HELOC?

Yes, HELOCs can have tax implications. The interest you pay on your HELOC might be tax-deductible if used to buy, build, or significantly improve your home. However, refinancing may affect this. Consult a tax professional for clarity on these points.

Can I negotiate the terms of my HELOC with my lender as I approach the maturity date?

In some cases, it might be possible to negotiate terms with the lender as the maturity date nears. This depends on factors such as your financial situation, payment history, and the lender’s policies. It never hurts to reach out to the lender to discuss possible options.

Article sources

- Consumer Finance, Find a Housing Counselor

About our contributors

-

Written by Rebecca Lake, CEPF®

Written by Rebecca Lake, CEPF®Rebecca Lake is a certified educator in personal finance (CEPF®) and freelance writer specializing in finance.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.