Think your family earns too much to get financial aid? You’re not alone—but chances are, you’re not out of options either.

One of the biggest myths in college planning is that families with higher incomes won’t qualify for anything. But the truth is, there’s no strict income cutoff for most federal aid. And even if need-based grants aren’t on the table, you still have plenty of options.

In case you’ve exhausted your federal financial aid, school aid package, and scholarship opportunities, and are currently in need of funding for school, here’s our list of top-rated private student loan lenders: Best Private Student Loans in 2026: Reviewed and Ranked.

This guide will walk you through how your parents’ income affects your eligibility—and how to pay for college even if you don’t qualify for traditional financial aid.

| Company | Fixed Rates (APR) | Variable Rates (APR) | Rating (0-5) |

|---|---|---|---|

|

|

5.59% – 16.99% | 3.99% – 15.89% |

|

|

|

5.59% – 16.99% | 3.87% – 16.50%% |

|

|

5.59% – 16.99% | 3.99% – 16.85% |

|

|

3.29% – 15.99% fixed-rate APR w/ autopay included | 4.64% – 16.73% variable-rate APR w/autopay included |

|

|

|

5.59% – 16.99% | 3.99% – 17.99% |

|

|

|

5.59% – 16.99% | 6.75% – 17.99% |

|

Table of Contents

Income thresholds for financial aid eligibility

Even though there’s no official income cap for FAFSA eligibility, certain types of aid—especially grants and need-based loans—are generally awarded to students from lower-income households. The table below breaks down which financial aid programs are most likely to be available at different income levels.

| Aid type | Is income a factor? | More likely to qualify if household income is… |

| Pell Grant | Yes | Under $60K (most likely under $40K) |

| Federal Supplemental Educational Opportunity Grant (FSEOG) | Yes | Under $40K |

| Work-study | Yes | Typically under $60K |

| Direct Subsidized Loans | Yes | Under $70K |

| Direct Unsubsidized Loans | No | Available to all incomes |

| Direct PLUS Loans | No, but credit check required | Available to all incomes (with no adverse credit) |

| State-based aid | Often | Varies by state; many cap eligibility at ~$100,000 |

| Institutional aid (college-specific) | Often | Varies; may consider income and merit |

What this means

If your parents earn over $75,000 or even $100,000 per year, you might not qualify for need-based aid like Pell Grants or Subsidized Loans—especially if you’re an only child. But higher-income families can still get federal Unsubsidized Loans, PLUS Loans, and school-specific merit aid or tuition discounts.

Income protection allowances and household size also matter. For instance, having multiple kids in college or high medical bills can lower your Student Aid Index (SAI) and make need-based aid more accessible than you’d expect.

Bottom line

Don’t assume you’re ineligible just because your family’s income seems high. There’s no harm in applying, and many families with incomes over six figures still qualify for aid, especially from their school or state.

How your parents’ income affects your eligibility for federal aid

If you’re a dependent student, your parents’ income is factored into the financial resources you have at your disposal to pay for school. If you’re an independent student, your parents’ income isn’t considered, but your spouse’s income might be if you’re married.

You won’t know how your parents’ income affects your financial aid eligibility until you complete the Free Application for Federal Student Aid (FAFSA). This application gathers information about your family’s financial situation and uses it to calculate your Student Aid Index (SAI).

You’re considered a dependent student if you’re pursuing an associate or bachelor’s degree, are under 24, are unmarried, are not in the military, and don’t have dependents of your own.

The SAI is a measure, introduced for the 2024 – 2025 school year, that replaced the Expected Family Contribution (EFC) of years past.

Like the EFC, your individual SAI doesn’t indicate how much money you or your parents can put toward your education. Instead, it helps colleges gauge your financial aid eligibility and compare financial need among students.

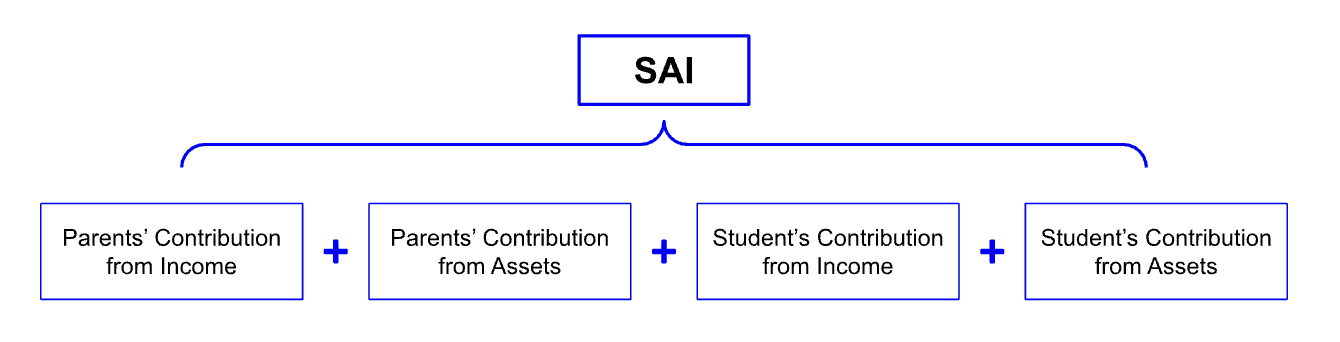

To calculate the SAI for dependent students, the FAFSA uses this formula:

In addition to looking at your income and assets, the SAI formula also counts:

- Your parents’ available income: This includes earned wages and certain tax deductions, minus income taxes paid and cost-of-living adjustments.

- Your parents’ assets: This includes bank account balances, investments, and child support received. Only 12% of your parents’ net assets are used to determine your SAI.

The greater your and your parents’ incomes and assets, the higher your SAI. The higher your SAI, the less outside help you need for school—theoretically, anyway.

But remember: A high income on paper doesn’t always mean a high SAI. The adjustments and allowances built into SAI calculations are proportional to your parents’ income and household size.

In other words, the FAFSA considers that only a portion of your family’s resources can be used to pay for college and adjusts your SAI accordingly.

What is the income cutoff for financial aid?

There’s no official income cutoff for federal student aid—but income does affect your eligibility for need-based programs like Pell Grants and Subsidized Loans.

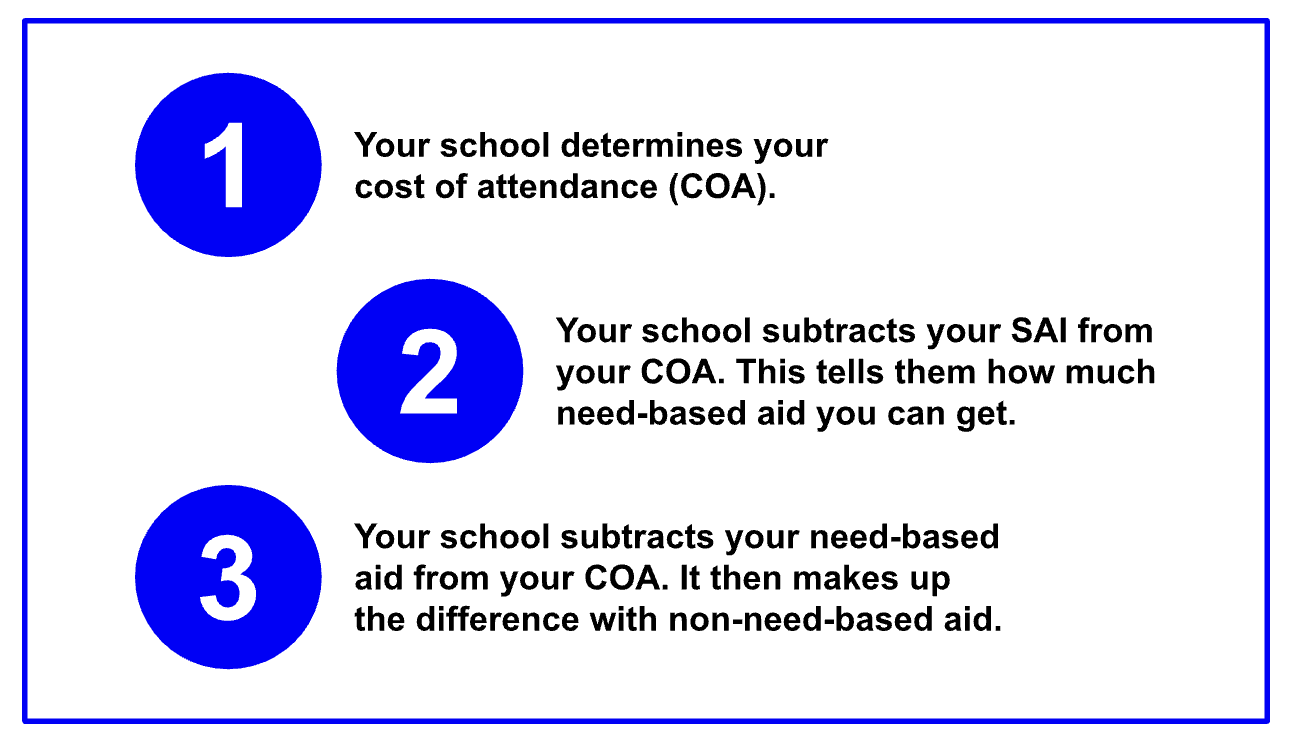

To determine how much of each aid type (need-based vs. non-need-based) you’re eligible for, colleges follow this process:

Rather than using a single number, the FAFSA looks at your household income after allowances and adjustments for taxes, family size, and more. These adjustments can bring a seemingly high income down to a level that still qualifies for aid.

For example, if your total cost of attendance is $15,000, and you get $5,000 in need-based aid, you’d be eligible for the remaining $10,000 in non-need-based aid.

And even if your family doesn’t qualify for need-based aid, you may still be eligible for non-need-based options like Unsubsidized Loans, PLUS Loans, or TEACH grants.

How much financial aid can you expect based on your parents’ income?

| Income | Federal aid | State or school aid | Private loans |

| $75K+ | ✅ Possible | 🟡 Likely | 🟡 Likely |

| $100K+ | 🔴 Rare | 🟡 Likely | 🟡 Likely |

| $200K+ | 🔴 Rare | ✅ Possible (merit-based) | 🟡 Likely |

| $400K+ | 🔴 Rare | 🔴 Rare (merit-only at elite schools) | 🟢 Very likely |

What to expect if your family earns over $75,000

| Aid type | Availability |

| Pell Grant | Unlikely unless large household or multiple kids in college |

| FSEOG Grant | Very unlikely |

| Work-study | Sometimes available |

| Direct Subsidized Loans | Possibly, depending on SAI |

| Direct Unsubsidized Loans | ✅ Available to all incomes |

| PLUS Loans | ✅ Available with credit check |

| Institutional/State Aid | Merit-based or limited need-based aid |

| Private Loans Needed? | Possibly |

| Notes | Family size and tax factors may still reduce your SAI |

This tier begins to edge out Pell Grants unless your family has multiple dependents or a high cost of living. But it’s still well within range for some need-based aid—especially from your state or school.

Key takeaways

- Subsidized loans may still be available

- Your SAI could qualify you for school-based grants

- FAFSA still highly recommended

Can you get financial aid if your parents make over $100,000?

| Aid Type | Availability |

| Pell Grant | ❌ Not available |

| FSEOG Grant | ❌ Not available |

| Work-study | Rare, but possible |

| Direct Subsidized Loans | Rare, unless unusual financial circumstances |

| Direct Unsubsidized Loans | ✅ Always available |

| PLUS Loans | ✅ Available with credit check |

| Institutional/State Aid | Merit-based awards more likely than need-based |

| Private Loans Needed? | Likely |

| Notes | Apply early for merit aid; FAFSA still recommended |

Yes—particularly non-need-based aid like Unsubsidized Loans and Parent PLUS Loans. School-specific merit scholarships or tuition discounts also play a major role at this income level.

If you’re attending a high-cost private college, even $100K may not stretch as far, which could make aid more likely.

Will I qualify if my parents make $200,000 or more?

| Aid type | Availability |

| Pell Grant | ❌ Not available |

| FSEOG Grant | ❌ Not available |

| Work-study | Very rare |

| Direct Subsidized Loans | ❌ Not available |

| Direct Unsubsidized Loans | ✅ Available |

| PLUS Loans | ✅ Available |

| Institutional/State Aid | Still possible—especially merit-based |

| Private Loans Needed? | Very likely |

| Notes | Some high-cost colleges may still offer merit-based tuition discounts |

Families earning $200K+ often assume they’re fully ineligible, but that’s not always the case.

You may still qualify for:

- Unsubsidized Loans

- Parent PLUS Loans (if credit-approved)

- Merit-based or department-specific scholarships

If your household has multiple children in college or high medical expenses, your calculated SAI may still reflect some financial need.

What if my parents make $400,000?

| Aid type | Availability |

| Pell Grant | ❌ Not available |

| FSEOG Grant | ❌ Not available |

| Work-study | ❌ Not available |

| Direct Subsidized Loans | ❌ Not available |

| Direct Unsubsidized Loans | ✅ Available |

| PLUS Loans | ✅ Available |

| Institutional/State Aid | Merit aid possible, but rare at this level |

| Private Loans Needed? | Almost certainly |

| Notes | FAFSA still required for some scholarships; don’t skip it |

At this tier, you’re generally looking at merit-based aid, employer tuition assistance, or private student loans.

But don’t skip FAFSA. Some colleges require it even for merit scholarships or work-study eligibility.

How to get financial aid without your parents’ help

There are ways to get financial aid despite your parents being high earners. Here are six tips on how to pay for college if you don’t qualify for financial aid or you think your parents’ income might be an obstacle:

- Fill out the FAFSA. Even if you think you won’t qualify for aid, don’t skip this step.

- Appeal your financial aid decision.

- Look for scholarships and grants.

- Use non-need-based federal financial aid.

- Consider private student loans.

- Readjust, regroup, and adapt.

Let’s explore each potential solution in more detail.

1. Fill out the FAFSA

Should I complete the FAFSA if my parents are rich? It’s a legitimate question, and the answer is a resounding yes.

You should complete the FAFSA every academic year, wealthy parents or not. You might be surprised and find out you’re eligible for aid you didn’t think you could get.

Besides, you can always update your FAFSA should your financial situation change. For example, if you or a parent loses a job after submission, you can amend your FAFSA and get a modified SAI.

2. Appeal your financial aid

You can also appeal your financial aid decision and request that your college reconsider your financial aid package.

After submitting your FAFSA, your college will send you a financial aid award letter. This letter outlines the institutional scholarships, federal grants, and federal loans it’ll give you. The letter should also include appeal instructions if you think your initial aid is inadequate.

You’re not guaranteed to receive more aid after an appeal, but you could leave money on the table if you don’t.

3. Look for scholarships and grants

Another option for obtaining financial aid for college when parents make too much is to consider scholarships and grant funding. A misconception about scholarships and grants is that these funds are only available to low earners, but that isn’t the case.

While some scholarships and grants are need-based, others are awarded for academic achievement, community service, artistic or athletic ability, or pursuing a particular career.

Deadlines vary, so get a head start by beginning to search for scholarships and grants at least a year before you plan to start school. Many major scholarship applications open up during the summer and early fall, so this period is crucial for researching and gathering all the necessary information.

A significant number of scholarships have deadlines in the fall, particularly between October and December. Make sure you have everything prepared well in advance for these deadlines, including letters of recommendation, essays, and transcripts.

4. Use non-need-based federal aid

You could still qualify for non-need-based aid, regardless of your income or SAI. Non-need-based aid includes the following types of federal student loans:

- Direct Unsubsidized Loans: Federal loan limits are based on the year of school the student is completing and the total cost of attendance. Although payment is not due on these loans until you leave school, interest accrues while loan payments are deferred.

- Direct PLUS Loans: Direct Grad PLUS Loans and Parent PLUS Loans work similarly to Direct Unsubsidized Loans in terms of deferment and interest accrual, but they have higher rates and no loan limits.

Federal student loans can be a viable way to cover the costs of college since they have low interest rates and favorable repayment terms. Keep in mind that while Direct Unsubsidized Loans don’t require a credit check, Direct PLUS Loans do.

5. Consider private student loans

Private student loans may be your next-best option if you don’t qualify for federal financial aid or have exhausted federal and state funding options.

Private student loans are available from banks, credit unions, and online lenders. They usually require a strong credit history or a cosigner with one (but student loans without a cosigner are available).

Having a high-income parent act as a cosigner could work in your favor. If your cosigning parent has a steady income and good credit history, that could make it easier to get approved and secure lower interest rates.

One solid option to consider is College Ave, our pick for the best overall private student loan. It offers flexible repayment terms, competitive rates, and cosigner release after consistent on-time payments. You can also check your eligibility with a soft credit pull, so there’s no risk to your score.

Rates, repayment terms, and benefits vary, so compare rates and loan offers with multiple lenders before accepting a private student loan.

6. Readjust, regroup, and adapt

Say you’ve explored your financial aid options and haven’t found realistic solutions. In that case, it may be time to think outside the box.

If you’re not set on one particular school, consider one with a lower COA. You might also look for schools in areas with a lower cost of living. You could also start your degree at a community college or take free or low-cost dual-enrollment courses through your high school.

If you’ve already started your program, you could transfer to a more affordable school or take a gap year to save up. Studying abroad in a country with lower tuition could also be an option.

Try to get a paid internship or entry-level job in your field. You’ll earn money you can use for school, and you might also earn course credit. Your employer may even help cover some or all of your tuition.

When it comes down to it, remember that your educational journey is exactly that: yours. You can likely qualify for aid even if your parents earn a high income, but even if you don’t, you aren’t out of options. Weigh each one, adjust as you go, and know it’s all part of the process.

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.