If your FICO score is between 740 and 850, give yourself a pat on the back: You have excellent credit. This tells lenders you manage your money—and your debts—responsibly. Because you’re deemed a more reliable borrower, lenders will let you borrow more for less.

You’ll enjoy higher loan limits, lower interest rates, and even more flexible repayment terms. Those favorable loan offers are especially helpful when you apply for a home equity line of credit (HELOC). We researched multiple HELOC lenders to find the best choices for excellent-credit borrowers like you. Read on for our top recommendations.

| Company | Best for… | Rates (APR) | Rating (0-5) |

|---|---|---|---|

|

|

Best Overall | 8.60% – 17.25% fixed |

|

|

|

Best Customer Reviews | 8.00% – 16.00% fixed |

|

|

|

Best Credit Union | 12-month intro rate of 6.99% for VantageScores of 720+, then a variable rate |

|

3 best HELOCs for excellent credit

We compared several choices to bring you the best HELOC lenders for excellent credit, evaluating their rate ranges, funding speeds, and overall borrowing experiences. These four beat out the competition.

Figure – Best overall

LendEDU rating: 4.9 out of 5

- No in-person appraisal required

- Repayment terms from 5 to 30 years

- Not available in Hawaii, Kentucky, New York, or West Virginia

Figure stands out for many reasons, but most notably for its rate structure. Where most HELOCs come with variable rates, Figure offers fixed-rate HELOCs. That stability means your monthly budget stays intact—an important feature for credit-conscious borrowers.

While you’ll enjoy consistent payments with Figure, you’ll need to withdraw 100% of your credit limit upon opening your HELOC. You’ll also only have two to five years to make any additional draws. Keep that in mind if you choose to apply.

Aven – Best customer reviews

LendEDU rating: 4.8 out of 5

- Lowest rate guarantee

- Optional debt protection program through Securian

- Approval in as little as 15 minutes

- Excellent Trustpilot customer reviews from more than 3,800 customers (in September 2024)

Aven is a standout HELOC provider for borrowers with excellent credit, offering a minimum loan amount of just $5,000. Aven’s unique HELOC structure allows borrowers to tap into their home equity with competitive fixed rates, flexible repayment terms, and no hidden fees, which can appeal to homeowners looking to leverage their excellent credit for lower costs.

With Aven, the application process is fast and user-friendly, often providing instant approval decisions for qualified borrowers. The platform’s transparent terms and excellent customer service add to its appeal, ensuring that borrowers understand their HELOC terms and can access their funds right away. This combination of low minimums, flexible borrowing options, and excellent service makes Aven a top choice for those with excellent credit looking for a reliable HELOC solution.

FourLeaf FCU – Best credit union

LendEDU rating: 4.7 out of 5

- No closing costs or origination fees

- May get approved without appraisal

- Not available in Texas

FourLeaf Federal Credit Union is the only lender on our list that offers online and in-person service options. If you live in New York, you can visit a branch to apply or find support for your HELOC. FourLeaf HELOCs are only open to credit union members, but joining costs just $5.

FourLeaf’s funding times are much longer than others on this list. From application to access, FourLeaf’s HELOC process can take up to 10 weeks. Provide as much upfront documentation as possible to give your loan the best chance of expediting.

What are the eligibility requirements for a HELOC?

Excellent credit is a near-guaranteed way to get approved for a HELOC, but creditworthiness isn’t the only requirement.

To qualify for a HELOC—especially one with favorable rates—you also need:

- Proof of consistent income

- A low debt-to-income ratio (DTI)

- Sufficient home equity

- A low loan-to-value ratio (LTV)

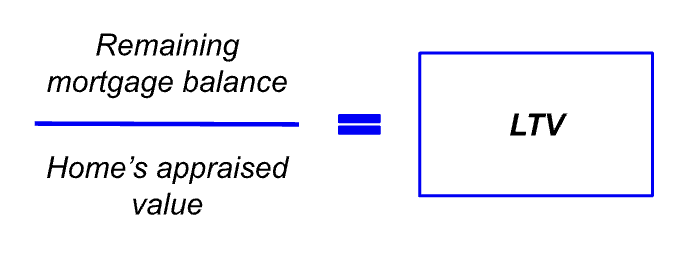

Equity is the difference between your home’s value and your outstanding mortgage balance. To calculate your home equity, use this formula:

Say, for instance, your home is worth $300,000. If you owe $170,000 on your mortgage, you’d have $130,000 in equity:

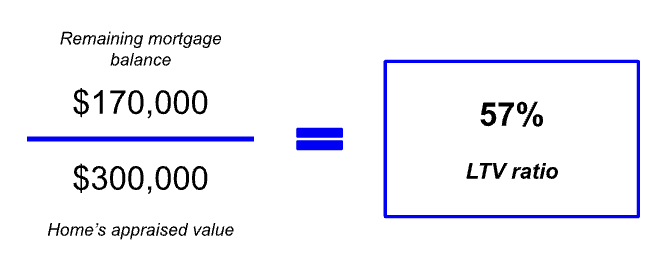

Your LTV, on the other hand, is a measure of how much your home is worth compared to what you owe. To find your LTV, you’ll divide your mortgage balance by your home’s value:

Continuing with the same example, if you owe $170,000 on a $130,000 home, your LTV would be 57%:

These figures—your home equity and your LTV—are linked to your HELOC eligibility. Even if you’re approved, these numbers determine how large a HELOC you can get.

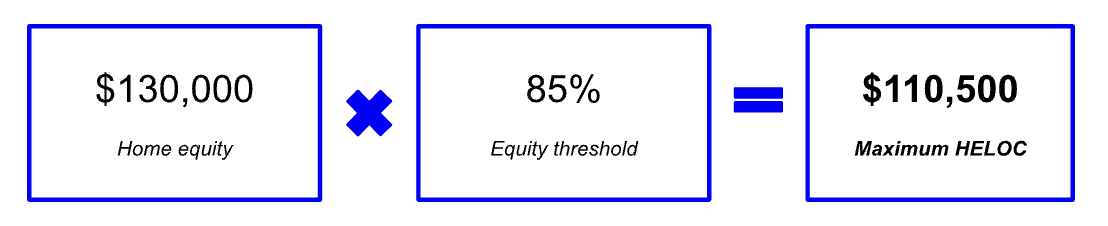

To protect themselves against loss if you sell the home or if the market dips, lenders often won’t let you borrow more than 80% to 90% of your available equity. (Hitch’s 95% equity threshold is the exception, not the rule.)

If your lender lets you borrow up to 85% of your equity, you’ll only be able to borrow up to $110,500, even though you have a hypothetical $130,000 available:

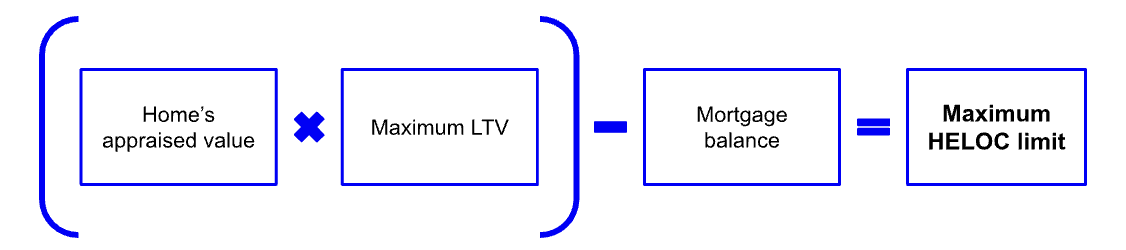

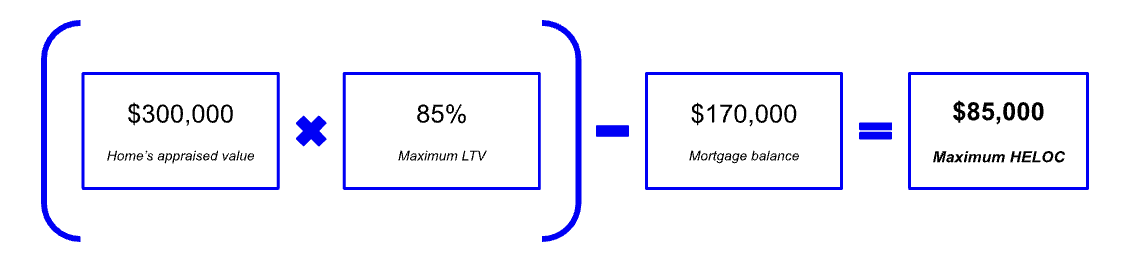

In addition to setting equity thresholds, lenders also set a maximum LTV. This is often around 85%, but like equity thresholds, it varies by lender. Essentially, the size of your HELOC is the difference between your lender’s LTV cap and your current LTV:

In this case, your maximum HELOC limit would be $85,000:

In other words, your high credit score might meet underwriting criteria, but you still need an LTV below your lender’s maximum and enough home equity to qualify for a HELOC.

How to choose a HELOC when you have excellent credit

Taking out a HELOC is no small matter. Just like your lender will evaluate you and your property, you need to evaluate your lender. Here’s how to narrow down your HELOC choices and select the best one for you:

- Prequalify with multiple lenders. We can’t stress this enough: Check your rates with four or five lenders before you consent to a hard credit check. The more lenders you prequalify with, the more HELOC offers you can choose from.

- Compare the details of each offer. How does each lender’s APR compare? How long are your draw and repayment periods? How much can you borrow?

- Read the fine print. Consider what borrowing conditions each HELOC requires. You may be subject to a minimum initial draw or minimum additional draws, for example.

- Look for unique benefits. These benefits—rate discounts or fixed-rate conversion options, for example—could be the deciding factor, especially if your HELOC offers share many similarities.

Once you’ve assessed your HELOC offers against these criteria, you can make an informed decision before committing to any one lender.

Take your time during the selection process, and if an offer doesn’t make sense, keep searching. After all, having excellent credit doesn’t just mean you’re more likely to get approved—it also means you can be picky.

Having an excellent credit score should open more options, specifically interest rates and terms, along with more bargaining power. Additional features may be available to you, depending on the financial institutions you’re shopping with, so I suggest adding those to the pros and cons list when helping to weigh the decision.

Erin Kinkade, CFP®

How does excellent credit benefit me for HELOC repayment?

Having excellent credit translates to a lower overall borrowing cost, thanks to more favorable interest rates. Sometimes, it’s hard to conceptualize just how impactful your interest rate can be, so let’s walk through an example.

Imagine you owe $85,000 on your HELOC by the time you enter repayment. Here’s how your payments would look, assuming an 8.50% interest rate and a 20-year repayment period:

| Example 1: | |

| HELOC balance | $85,000 |

| Rate | 8.50% |

| Repayment length | 20 years |

| Monthly payment | $738 |

Now, let’s see how a higher APR—say, 11.99%—would change your payments:

| Example 2: | |

| HELOC balance | $85,000 |

| Rate | 11.99% |

| Repayment length | 20 years |

| Monthly payment | $935 |

Of course, your actual HELOC payments are likely to fluctuate if you have a variable rate, but this scenario illustrates the necessity of locking in a low rate.

With excellent credit, you stand a good chance of doing that. Your low rate will, in turn, minimize the cost of your HELOC and save you considerable money on interest over time.

If you’re on the cusp of having excellent credit but not quite there, prequalify to see what rates you can get now. If you don’t qualify for rates as low as you’d like, it may be worth waiting to get a HELOC until you’ve had a chance to raise your score.

The longer your positive payment history and the older your credit profile, the higher your score will climb. Keep making on-time payments, and don’t open any new accounts. Eventually, you’ll see a score increase that could bump you into the next credit bracket.

How to apply for a HELOC with excellent credit

Applying for a HELOC is similar to applying for traditional loans or credit cards—with a couple of added steps. Here’s what you’ll do:

- Gather your documents. To get a HELOC, you’ll need to furnish proof of income and identity, as well as provide recent mortgage statements, property tax bills, and homeowners insurance records. Track down this paperwork now to save time later.

- Get an informal property assessment. You don’t need a full appraisal at this stage, but you want a rough estimate of what your property is worth. Use online real estate listing sites to get an idea of your home’s value.

- Fill out your lender’s application. You already prequalified, so by this step, you should only need to fill in and confirm any additional personal or financial information. You’ll also consent to a credit check.

- Upload your documents. Attach the paperwork you gathered in step one to your application. More is better in this case. If your lender needs additional documentation, it could delay your approval.

- Schedule an appraisal. You may get an initial approval, but you usually can’t close on a HELOC without an appraisal. (FourLeaf is one of the few lenders that allows borrowers to skip an appraisal in select cases.) Depending on your lender, your appraisal may be in person or online, like Figure’s process.

- Review and sign your HELOC agreement. After the appraisal, your lender will finalize your HELOC offer. Read through your HELOC disclosure, noting your draw and repayment commitments, any applicable fees, and your APR details.

After you close on your HELOC, your lender will grant you access to your credit line. The application itself can take as little as a few minutes to complete, but scheduling the appraisal can take a bit longer, depending on your lender’s process.

Funding timelines, too, can vary from lender to lender. Some lenders can fund your HELOC within a matter of days, while others take several weeks.

Due to a Federal Trade Commission rule that gives you three days to cancel your HELOC, the earliest you can withdraw from your HELOC is four days after closing.

Once your credit line is funded and ready to go, you can start making withdrawals. Because HELOC limits are sizable, and because there are so many ways to use your HELOC, you’ll find no shortage of ways to spend the money.

Perhaps you’ll use your HELOC to pay off student loans, eliminate your mortgage, or get rid of your car loan. Maybe you’ll convert part of that credit line into fun money and take that vacation you’ve put off for years. Maybe you’ll do both.

However you use your HELOC, borrow wisely, and monitor your future monthly payments. You know firsthand how much effort it takes to build excellent credit, and you want to maintain that high score for as long as possible.

Recap of the best HELOCs for excellent credit

| Company | Best for… | Rates (APR) | Rating (0-5) |

|---|---|---|---|

|

|

Best Overall | 8.60% – 17.25% fixed |

|

|

|

Best Customer Reviews | 8.00% – 16.00% fixed |

|

|

|

Best Credit Union | 12-month intro rate of 6.99% for VantageScores of 720+, then a variable rate |

|

About our contributors

-

Written by Sarah Sheehan, MAT

Written by Sarah Sheehan, MATSarah Sheehan is a writer, educator, and analyst who focuses on the impact of health, gender, and geography on financial equity. Her ultimate goal? To live beyond the confines of chasing the next dollar—and to teach everyone else how to do the same.

-

Reviewed by Erin Kinkade, CFP®

Reviewed by Erin Kinkade, CFP®Erin Kinkade, CFP®, ChFC®, works as a financial planner at AAFMAA Wealth Management & Trust. Erin prepares comprehensive financial plans for military veterans and their families.