A HELOC offers flexibility when you need cash, and rate-shopping can help you find the best deal. As of March 2026, average current HELOC rates hover around 7%, with some lenders offering introductory rates as low as 4%.

While there have been a few spikes, HELOC interest rates have largely been on a downward trend since December 2023. What affects HELOC loan rates? Are HELOC rates likely to drop soon? We’ll answer those questions and more to help you decide if now is the right time to borrow.

Table of Contents

Who offers the best HELOC loan rates?

The best HELOC rate is the lowest rate you qualify for based on your credit, income, debt, and home equity. That being said, some lenders stand out more than others for their competitive HELOC interest rates and added benefits for borrowers.

Below are some HELOC lenders we recommend, along with their corresponding rates. Read more about each lender in our roundup of the best HELOC lenders.

How are HELOC interest rates calculated?

HELOC rates are most often calculated based on two things: a benchmark rate, like the prime rate, and a margin. Here’s a quick rundown of key terms:

- Prime rate is the lowest rate banks offer to their most creditworthy customers.

- Margin is a percentage banks add to the benchmark rate. For example, a bank may set HELOC loan rates at prime + 3%.

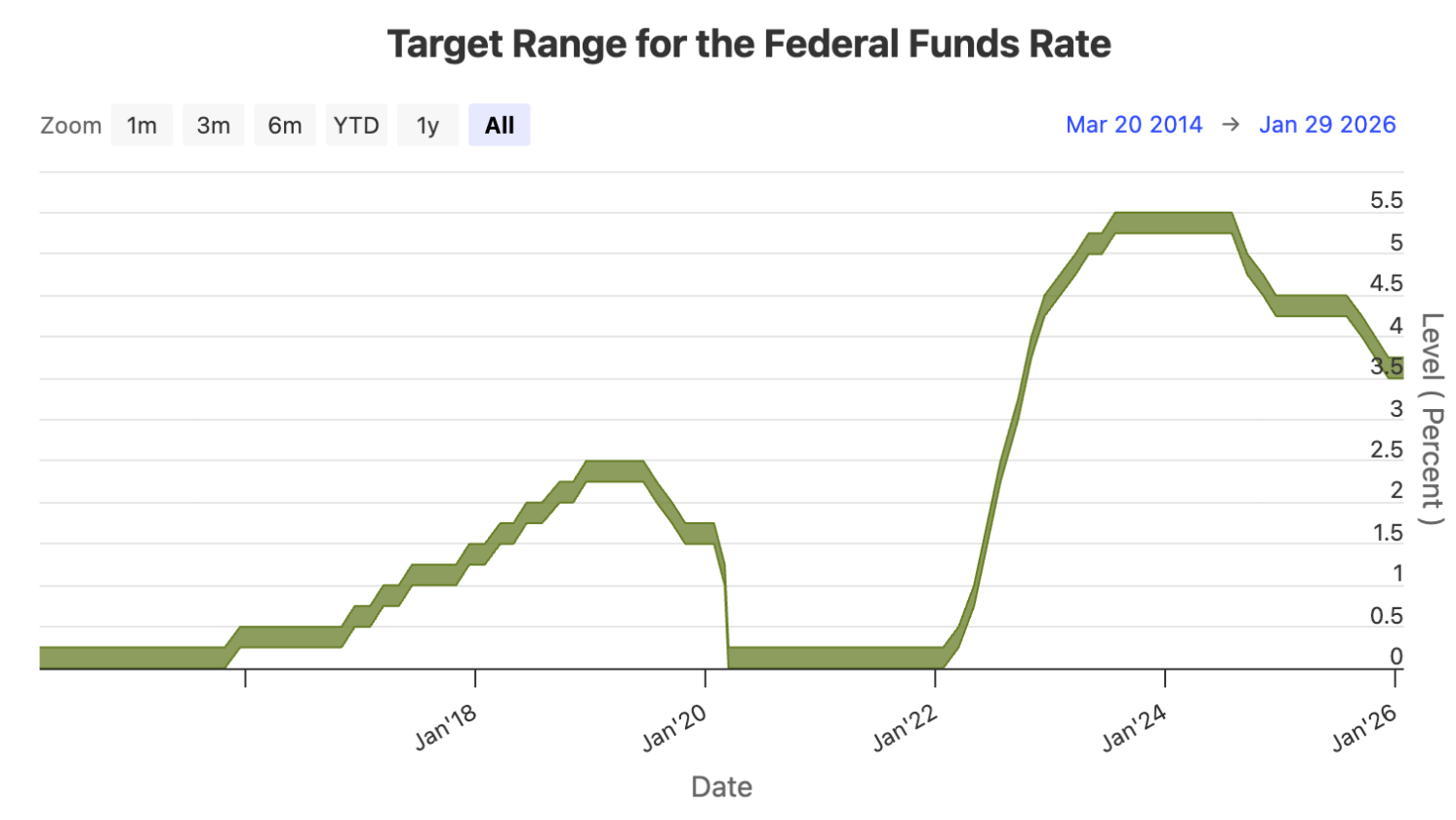

- The prime rate is influenced by the federal funds rate, which is the rate that banks charge to lend money to one another overnight.

Historical Prime rates February 2014 – February 2026

When the federal funds rate changes, it affects benchmark rates. Banks then adjust HELOC interest rates based on changes to the benchmark. Those adjustments may move rates up or down, depending on how the benchmark rate moves.

HELOC rates usually operate on a range, with the lowest rates reserved for the most creditworthy borrowers. What you actually pay for a HELOC depends on current HELOC rates and your:

- Credit scores

- Income

- Debt-to-income (DTI) ratio

- Loan amount and term

- Home equity

Here’s an example of what two borrowers might pay for a $50,000 HELOC with a 10-year interest-only draw period and a 10-year repayment term. We’ll assume they have the same income, DTI, and equity, but Borrower A has excellent credit while Borrower B has fair credit.

| Borrower A | Borrower B | |

| HELOC rate | 7.44% | 13.24% |

| Draw period payment | $310.00 | $551.67 |

| Regular monthly payment | $591.94 | $753.65 |

| Interest paid | $58,233.47 | $106,637.62 |

Note that these calculations assume you don’t make any additional draws over the $50,000 and you don’t pay an annual fee for your HELOC. But at a glance, you can see how much of a difference HELOC rates can make in what you pay.

It’s important to know what the current market averages are vs. what the lender is quoting [when shopping for a HELOC]. If your rate is near or below the average, that is typically competitive. If your credit isn’t excellent, you’ll want to take that into account knowing that you may not get the best advertised rate, but when you compare it to other lenders, are they all coming in right around the same APR?

Are HELOC rates higher than home equity or personal loans?

Current HELOC rates are slightly below current home equity loan rates, which is typical for these types of loans. The average home equity loan rate is around 8% as of February 2026. Personal loan rates, by comparison, average just above 12%.

What’s the difference between these loans?

- A HELOC is a revolving line of credit that’s secured by your home. You can draw against your HELOC as needed, and you only pay interest on the portion of your credit line you use.

- Home equity loans let you access a lump sum of money that you repay monthly, in fixed installments. Like HELOCs, home equity loans are also secured by your home.

- Personal loans are loans you can take out for virtually any reason, often without the need for collateral. They aren’t tied to your home.

HELOC rates may start off lower when the benchmark rate is low, but increase over time if the benchmark rate rises. Home equity loan rates and personal loan rates remain the same for the loan term, but they may be higher overall than HELOC loan rates. Unsecured personal loans also have higher rates since there’s no collateral to mitigate risk.

Are HELOC rates going down?

HELOC rates have been up and down since 2022, with rates down as of February 2026. Whether HELOC interest rates will continue to drop depends largely on the Federal Reserve’s direction for monetary policy and changes to the federal funds rate.

- If the Fed raises rates, HELOC rates could rise.

- If the Fed cuts rates, HELOC rates could go down.

Which way will the Fed move? FedWatch, a tool developed by CME Group, monitors Fed Funds futures prices to determine the probability of rate changes. As of February 2026, the FedWatch tool shows a 68.1% probability of a rate cut by June 2026. The likelihood of more rate easing remains high through December 2027.

Get the best HELOC rates

Getting the best HELOC rates requires a little planning before you apply. Here are some strategies to help you find the lowest HELOC rate.

- Check your credit. Knowing your credit score can help you guesstimate which HELOC rate range you might fall into.

- Review rate trends. Checking HELOC rate movements and trends can help you decide on the best time to apply for low rates.

- Compare lenders. Whether you use a marketplace like LendingTree or shop around on your own, it’s helpful to check out multiple lenders to see who has the lowest HELOC rates.

- Get prequalified. Prequalification doesn’t guarantee approval but it can give you an idea of what rate you might be able to get.

HELOC rate trends point to a possible decline later in 2026, which could affect your borrowing plans. Learn more about the best HELOC lenders, so you know what options you have when you’re ready to apply.

I recommend reaching out to multiple lenders and getting at least four to five quotes before choosing the right lender. It’s also important to look at smaller lenders like credit unions, as well as larger lenders, and online lenders. Keep all of the information in a spreadsheet because it can get overwhelming when you’re hearing back from multiple lenders. Compare the annual percentage rate (APR) since it will include the lender’s additional costs that isn’t always transparent. In your comparison spreadsheet, make sure you have a column to verify whether there is an intro rate and the ongoing rate, rate cap limits, the repayment structure (e.g. interest-only vs. full amortization), and whether there is a conversion option to a fixed rate loan.

Article sources

At LendEDU, our writers and editors rely on primary sources, such as government data and websites, industry reports and whitepapers, and interviews with experts and company representatives. We also reference reputable company websites and research from established publishers. This approach allows us to produce content that is accurate, unbiased, and supported by reliable evidence. Read more about our editorial standards.

- Bankrate, HELOC Data Center

- Aven, Our Products

- Figure, HELOC Rates

- FourLeaf Credit Union, Current Rates

- LendingTree, Home Equity Line of Credit (HELOC) Rates

- Bank of America, Home Equity Rates

- Board of Governors of the Federal Reserve System, What Is the Prime Rate, and How Does the Federal Reserve Set the Prime Rate?

- Board of Governors of the Federal Reserve System, Policy Rate

- FedWatch, Interest Rates

About our contributors

-

Written by Rebecca Lake, CEPF®

Written by Rebecca Lake, CEPF®Rebecca Lake is a certified educator in personal finance (CEPF®) and freelance writer specializing in finance.

-

Edited by Amanda Hankel

Edited by Amanda HankelAmanda Hankel is a managing editor at LendEDU. She has more than seven years of experience covering various finance-related topics and has worked for more than 15 years overall in writing, editing, and publishing.

-

Reviewed by Crystal Rau, CFP®, CRPC®, AAMS®

Reviewed by Crystal Rau, CFP®, CRPC®, AAMS®Crystal Rau, CFP®, CRPC®, AAMS®, is a Certified Financial Planner based in Midland, Texas. She is the founder of Beyond Balanced Financial Planning, a fee-only registered investment advisor that helps young professionals and families balance living their ideal lives with being good stewards of their finances.